1) Plimpton Sales uses special journals to record business transactions. Plimpton sells

office equipment. The company completed the following transactions a through j.

Identify the journal in which each transaction should be recorded.

a. Paid an installment on a bank loan.

b. Purchased inventory on credit.

c. Paid cash to a creditor.

d. Sold equipment to a customer on credit.

e. Sold equipment to a customer for cash.

f. Paid employees’ salaries in cash.

g. Received payment from a customer on credit.

h. Purchased office supplies on account.

i. Returned inventory to creditor before payment.

j. Sold equipment on account.

2) A perpetual record of a raw materials item that records data on the quantity and cost

of units purchased, units issued for use in production, and units that remain in the raw

materials inventory, is called a(n):

A.Materials ledger card.

B.Materials requisition.

C.Purchase order.

D.Materials voucher.

E.Purchase ledger.

3) A corporation is:

A.A business legally separate from its owners.

B.Controlled by the FASB.

C.Not responsible for its own acts and own debts.

D.The same as a limited liability partnership.

E.Not subject to double taxation.

4) A fixed cost:

A.Requires the future outlay of cash and is relevant for future decision making.

B.Does not change with changes in the volume of activity within the relevant range.

C.Is directly traceable to a cost object.

D.Changes with changes in the volume of activity within the relevant range.

E.Is irrelevant for cost-volume-profit and short-term decision making.

5) The building blocks of financial statement analysis do not include:

A.External analyst services.

B.Solvency.

C.Profitability.

D.Market prospects.

E.Liquidity and efficiency.

6) Memphis Company anticipates total sales for April, May, and June of $800,000,

$900,000, and $950,000 respectively. Cash sales are normally 25% of total sales. Of the

credit sales, 30% are collected in the same month as the sale, 65% are collected during

the first month after the sale, and the remaining 5% are collected in the second month.

Compute the amount of accounts receivable reported on the company’s budgeted

balance sheet for June 30.

A.$561,500.

B.$712,500.

C.$463,125.

D.$496,875.

E.$617,500.

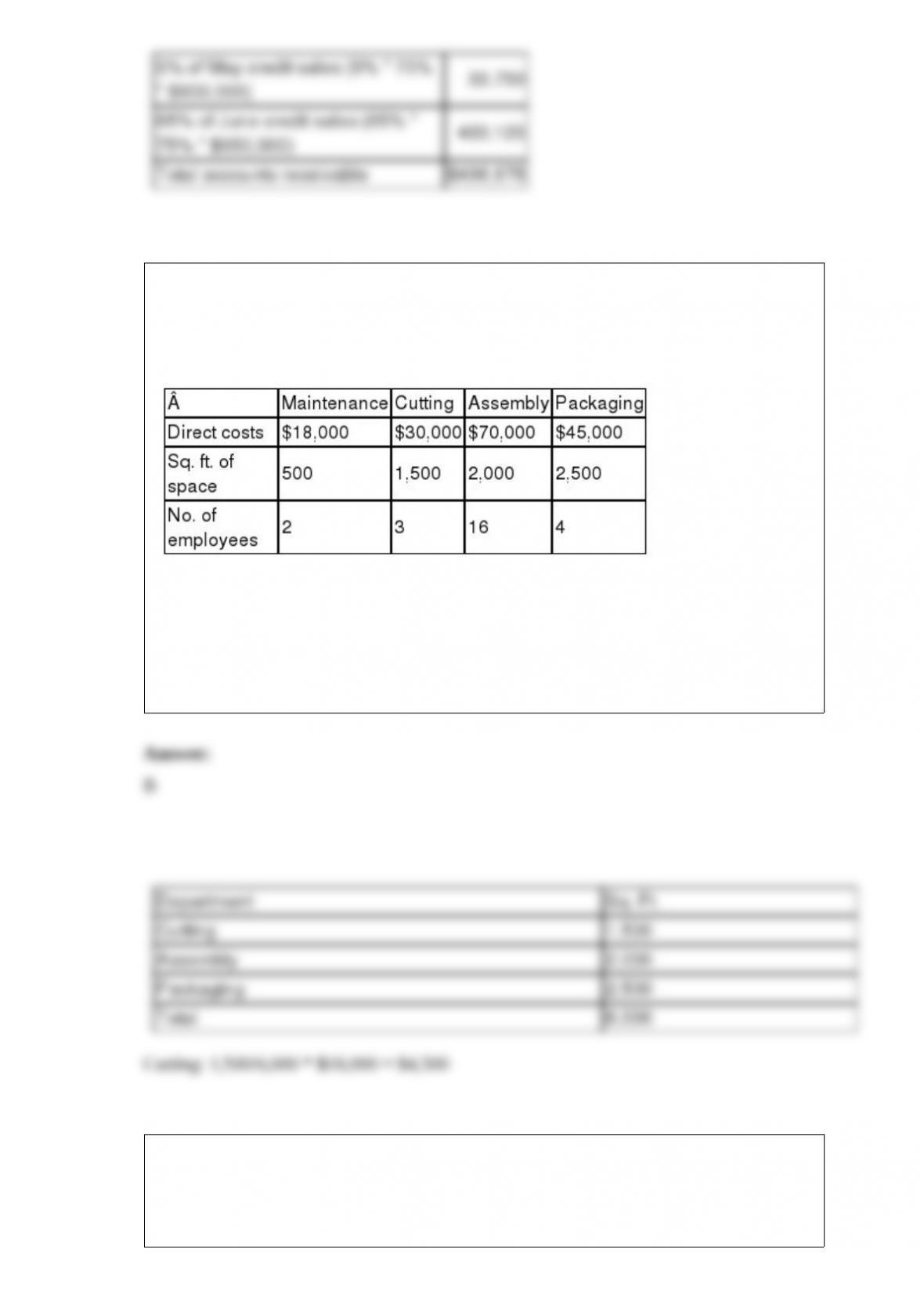

7) Riemer, Inc. has four departments. Information about these departments is listed

below. Maintenance is a service department. If allocated maintenance cost is based on

floor space occupied by each of the other departments, compute the amount of

maintenance cost allocated to the Cutting Department.

A.$500.

B.$4,500.

C.$3,724.

D.$6,000.

E.$4,153.

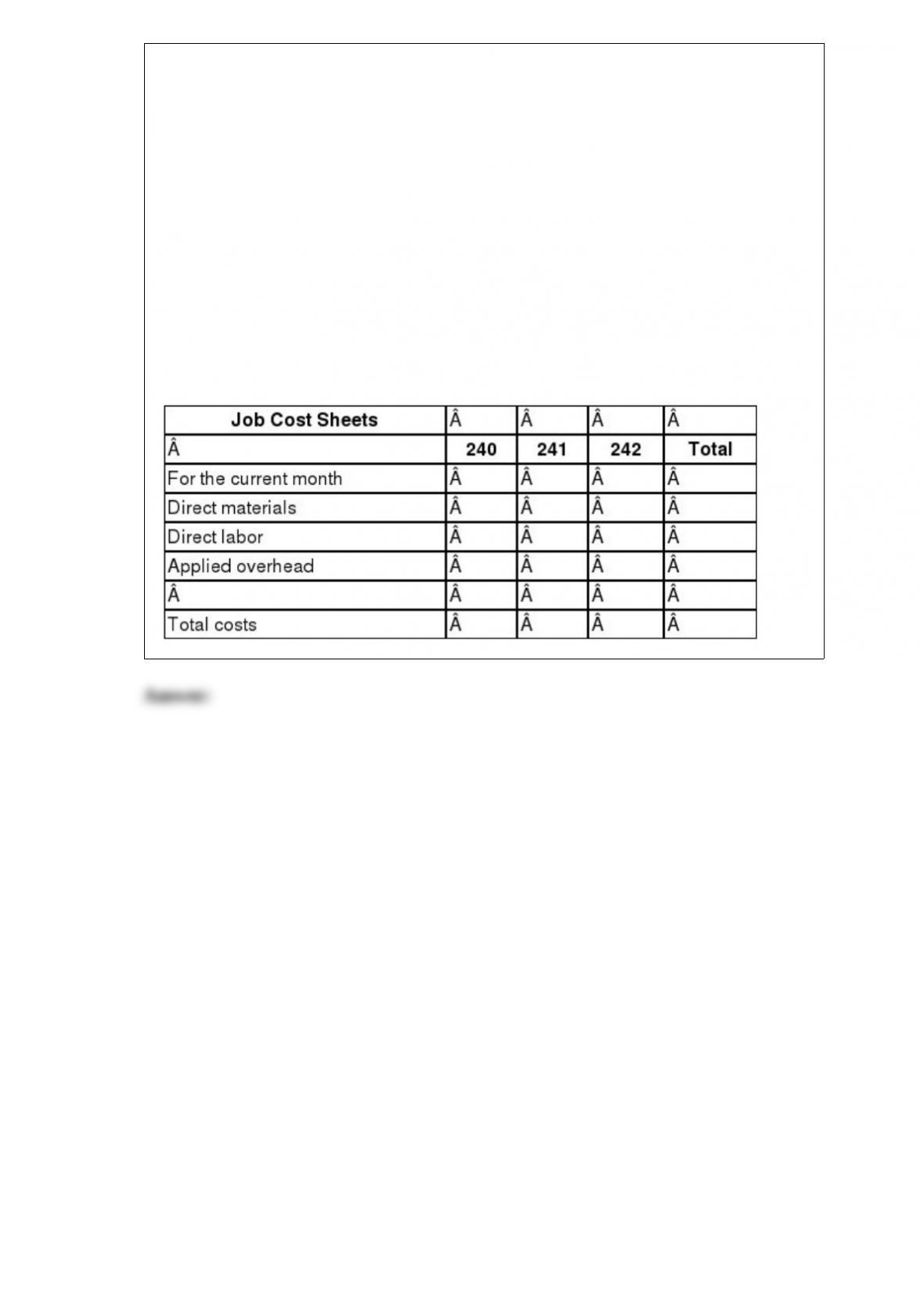

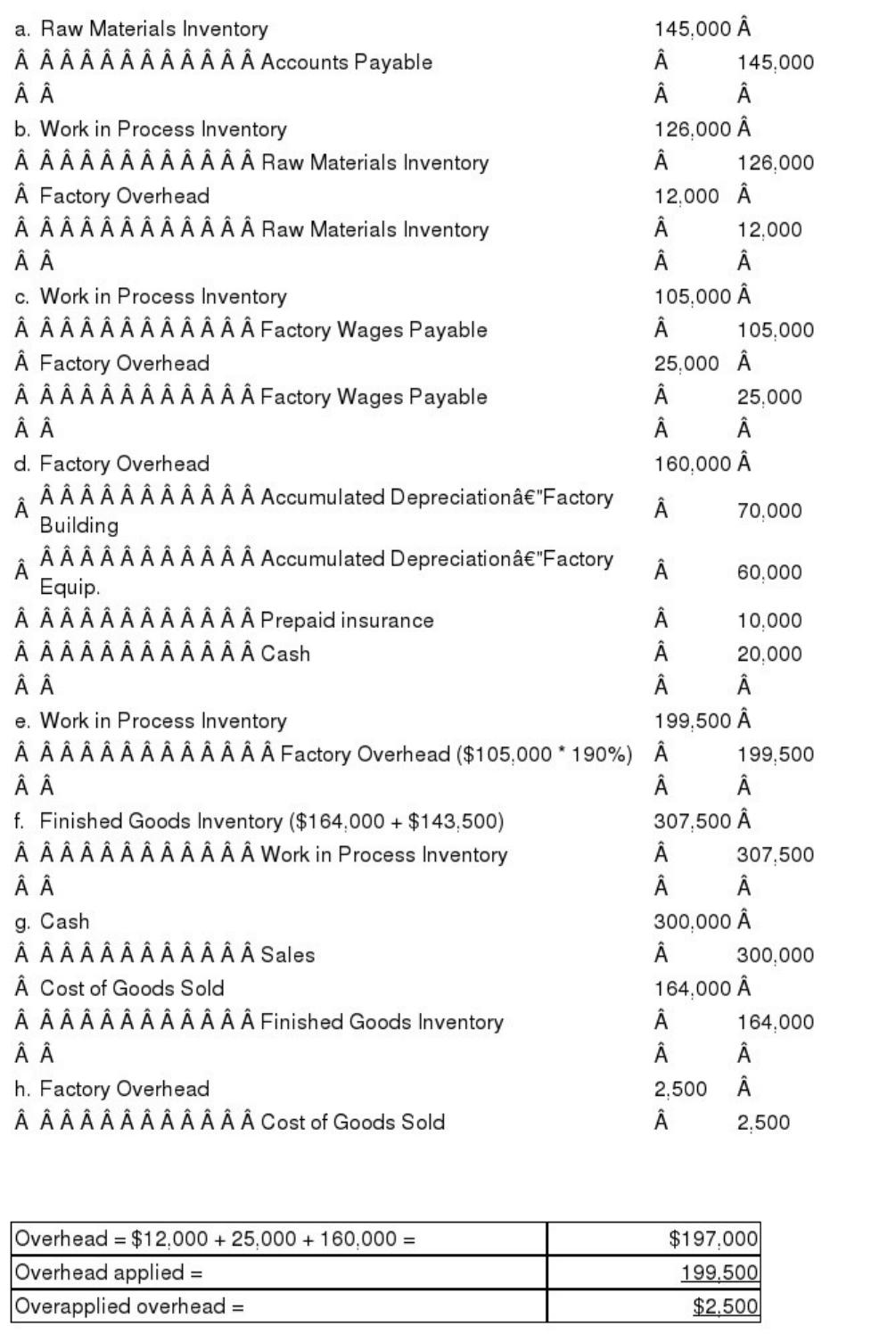

8) Drop Anchor takes special orders to manufacture sail boats for high end customers.

Complete the job cost sheets for Drop Anchor for September based on the following

information. Prepare journal entries to record the transactions as well as post to the job

cost sheets.

a. Purchased raw materials on credit, $145,000.

b. Materials requisitions: Job 240, $48,000; Job 241, $36,000; Job 242, $42,000;

indirect materials were $12,000.

c. Time tickets used to charge labor to jobs: Job 240, $40,000; Job 241, $30,000; Job

242, $35,000, indirect labor is $25,000.

d. The company incurred the following additional overhead costs: depreciation of

factory building, $70,000; depreciation of factory equipment, $60,000; expired factory

insurance, $10,000; utilities and maintenance cost of $20,000 were paid in cash.

e. Applied overhead to all three jobs. The predetermined overhead rate is 190% of direct

labor cost.

f. Transferred jobs 240 and 242 to Finished Goods Inventory.

g. Sold job 240 for $300,000 for cash.

h. Closed the under- or over-applied overhead account balance.

9) The carrying value of bonds at maturity always equals:

A.the amount of cash originally received in exchange for the bonds.

B.the par value of the bond.

C.the amount of discount or premium.

D.the amount of cash originally received in exchange for the bonds plus any

unamortized discount or less any premium.

E.$0.

10) Net sales divided by Average accounts receivable, net is the:

A.Days’ sales uncollected.

B.Average accounts receivable ratio.

C.Current ratio.

D.Profit margin.

E.Accounts receivable turnover ratio.

11) If a company uses a special payroll bank account:

A.The company does not need to issue paychecks.

B.The company draws one check for the entire payroll on the regular bank account and

deposits it in the payroll bank account.

C.The company must use a federal depository bank for the payroll bank account.

D.There is no need for a payroll register.

E.There is no need to issue W-2’s.

12) The party that has the right to exercise a call option on callable bonds is:

A.The bondholder.

B.The bond issuer.

C.The bond indenture.

D.The bond trustee.

E.The bond underwriter.

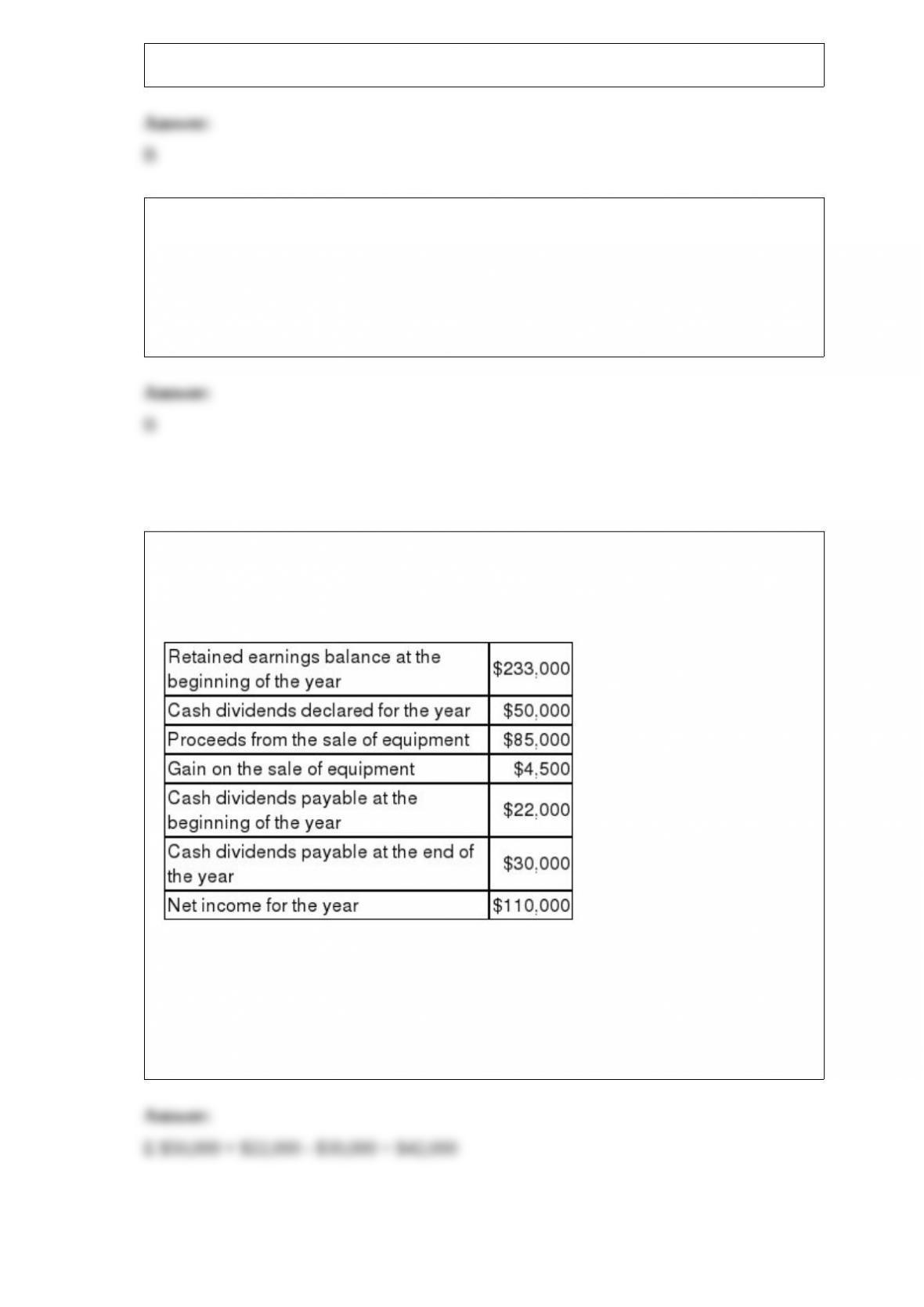

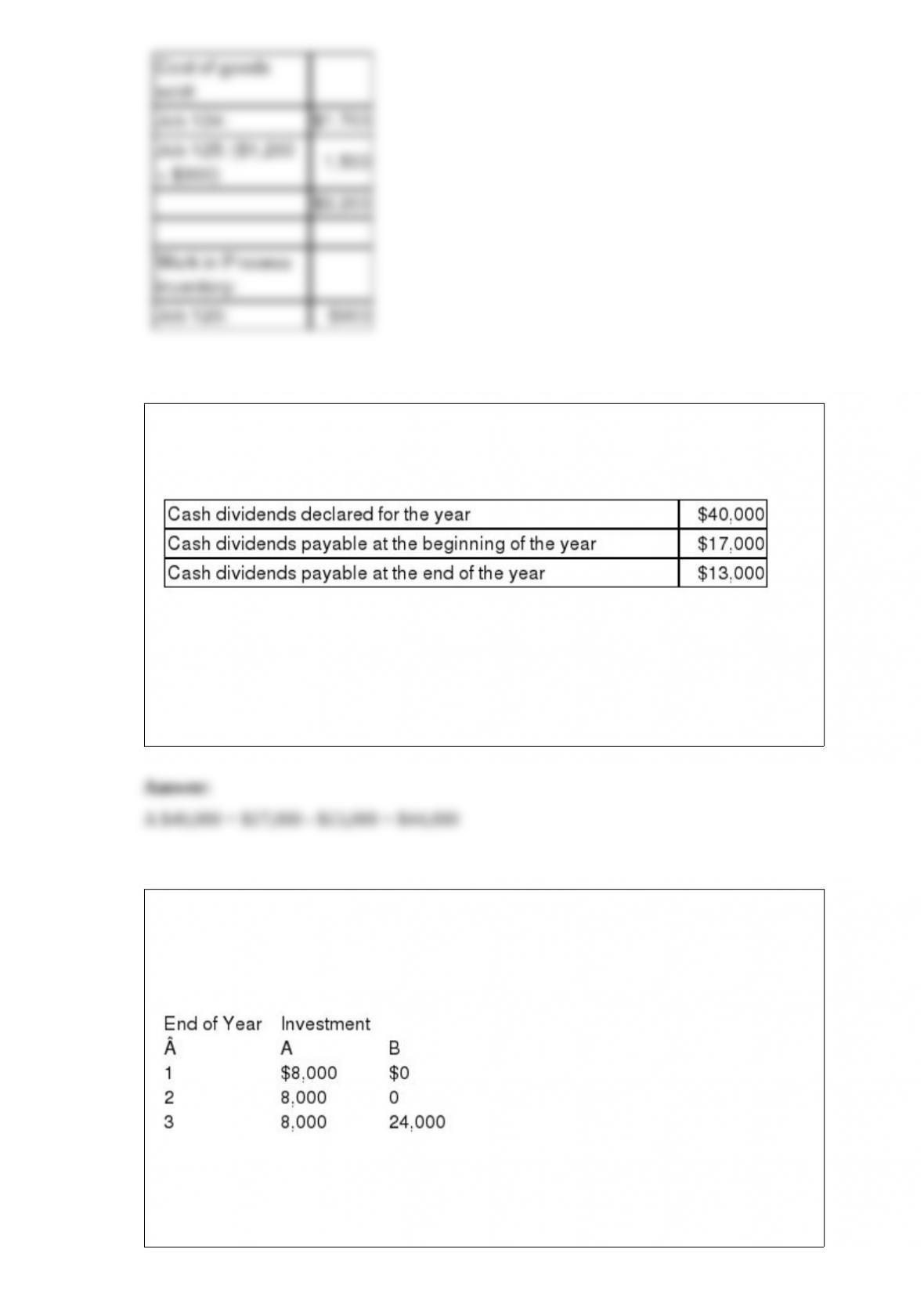

13) Fernwood Company is preparing the company’s statement of cash flows for the

fiscal year just ended. The following information is available:

The amount of cash paid for dividends was:

A.$52,000.

B.$60,000.

C.$58,000.

D.$50,000.

E.$42,000.

14) Promissory notes that require the issuer to make a series of payments consisting of

both interest and principal are:

A.Debentures.

B.Discounted notes.

C.Installment notes.

D.Indentures.

E.Investment notes.

15) Accumulated Depreciation and Service Fees Earned would be sorted to which

respective columns in completing a work sheet?

A.Balance Sheet and Statement of Owner’s Equity-Credit and Income Statement-Credit.

B.Balance Sheet and Statement of Owner’s Equity-Debit and Income Statement-Debit.

C.Income Statement-Debit and Income Statement-Credit.

D.Balance Sheet and Statement of Owner’s Equity-Debit and Balance Sheet and

Statement of Owner’s Equity-Credit.

E.Balance Sheet and Statement of Owner’s Equity-Debit; and Income Statement-Credit.

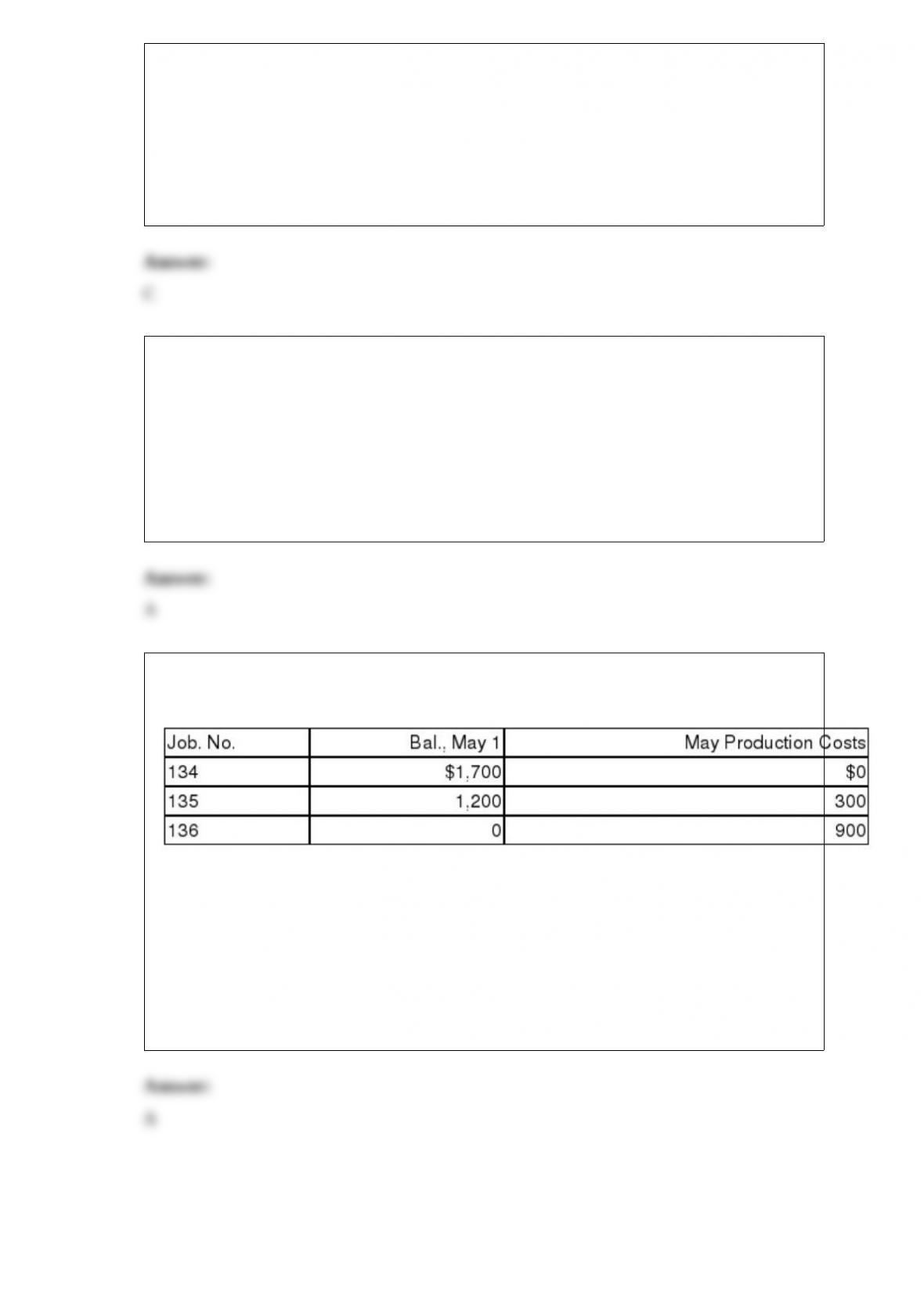

16) The job order cost sheets used by Greene Company revealed the following:

Job No. 135 was completed during May and Jobs No. 134 and 135 were shipped to

customers in May. What was the company’s cost of goods sold for May and the Work in

Process inventory on May 31?

A.$3,200; $900.

B.$2,900; $1,200.

C.$1,200; $2,900.

D.$1,700; $1,200.

E.$4,100; $0.

17) Marshland Company is preparing the company’s statement of cash flows for the

fiscal year just ended. The following information is available:

The amount of cash paid for dividends was:

A.$44,000.

B.$40,000.

C.$57,000.

D.$53,000.

E.$36,000.

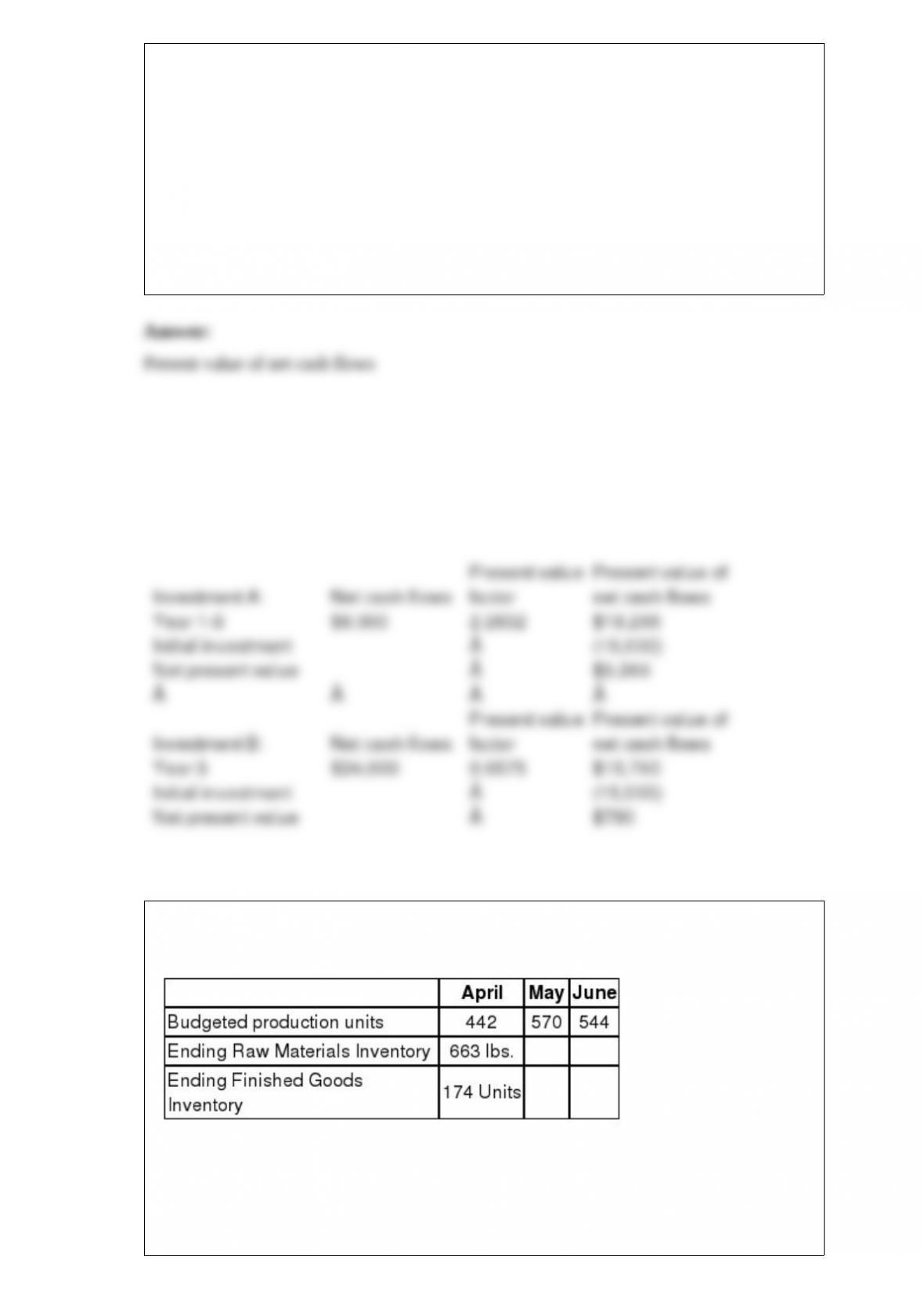

18) Alfarsi Industries uses the net present value method to make investment decisions

and requires a 15% annual return on all investments. The company is considering two

different investments. Each require an initial investment of $15,000 and will produce

cash flows as follows:

The present value factors of $1 each year at 15% are:

10.8696

20.7561

30.6575

The present value of an annuity of $1 for 3 years at 15% is 2.2832

Which investment should Alfarsi choose?

A.Only Investment A is acceptable.

B.Only Investment B is acceptable.

C.Both investments are acceptable, but A should be selected because it has the greater

net present value.

D.Both investments are acceptable, but B should be selected because it has the greater

net present value.

E. Neither machine is acceptable.

19) Snap, Inc., provides the following data for the next four months:

Desired Ending Inventory:

Raw Materials = 30% of next month’s production needs

Pounds of raw material required for each finished Unit = 5 lbs.

Required:

Calculate the amount of purchases of raw materials in pounds for April and May.

20) LJ Co. produces picture frames. It takes 3 hours of direct labor to produce a frame.

LJ’s standard labor cost is $11.00 per hour. During March, LJ produced 4,000 frames

and used 12,400 hours at a total cost of $133,920. What is LJ’s labor rate variance for

March?

21) Identify the classifications for non-influential investments in securities. What are

the accounting basics for non-influential investments in securities, including

acquisition, dividends earned, and disposition?

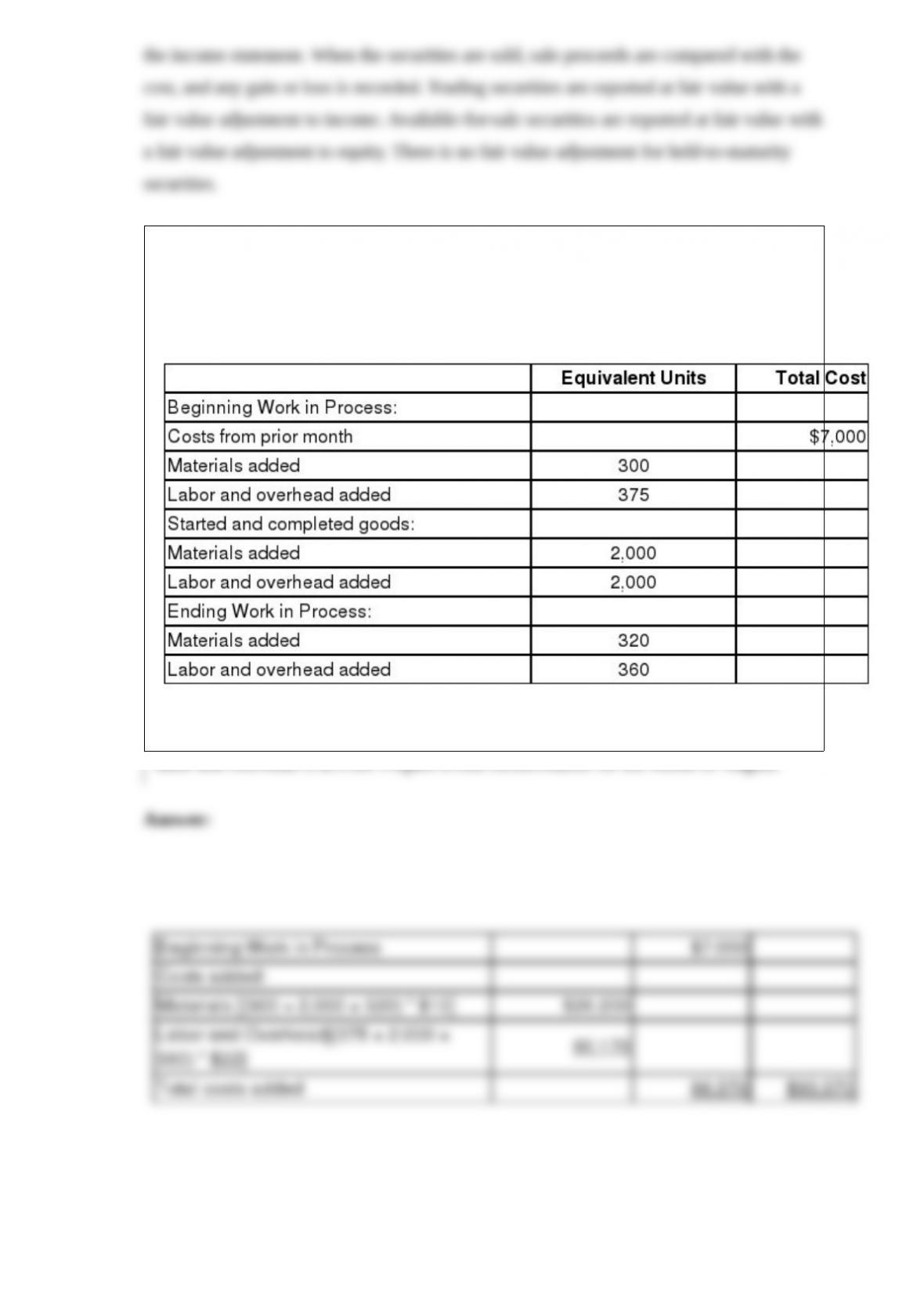

22) Refer to the following information about the Shaping Department of the Minnesota

Factory for the month of August. Minnesota Factory uses the FIFO method of inventory

costing.

The cost per equivalent unit of materials is $10.00, and the cost per equivalent unit of

labor and overhead is $22.00. Prepare a cost reconciliation for the month of August.

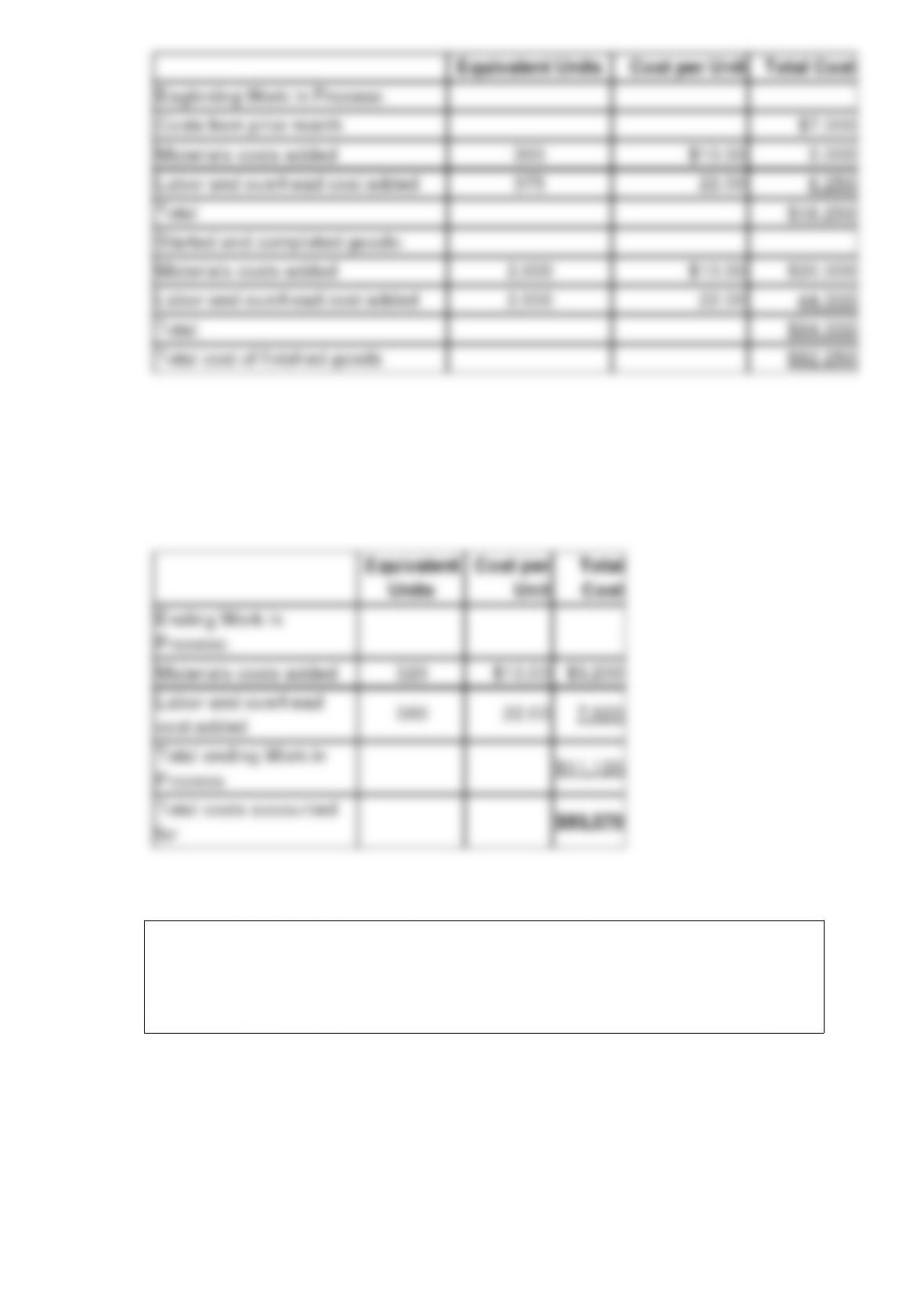

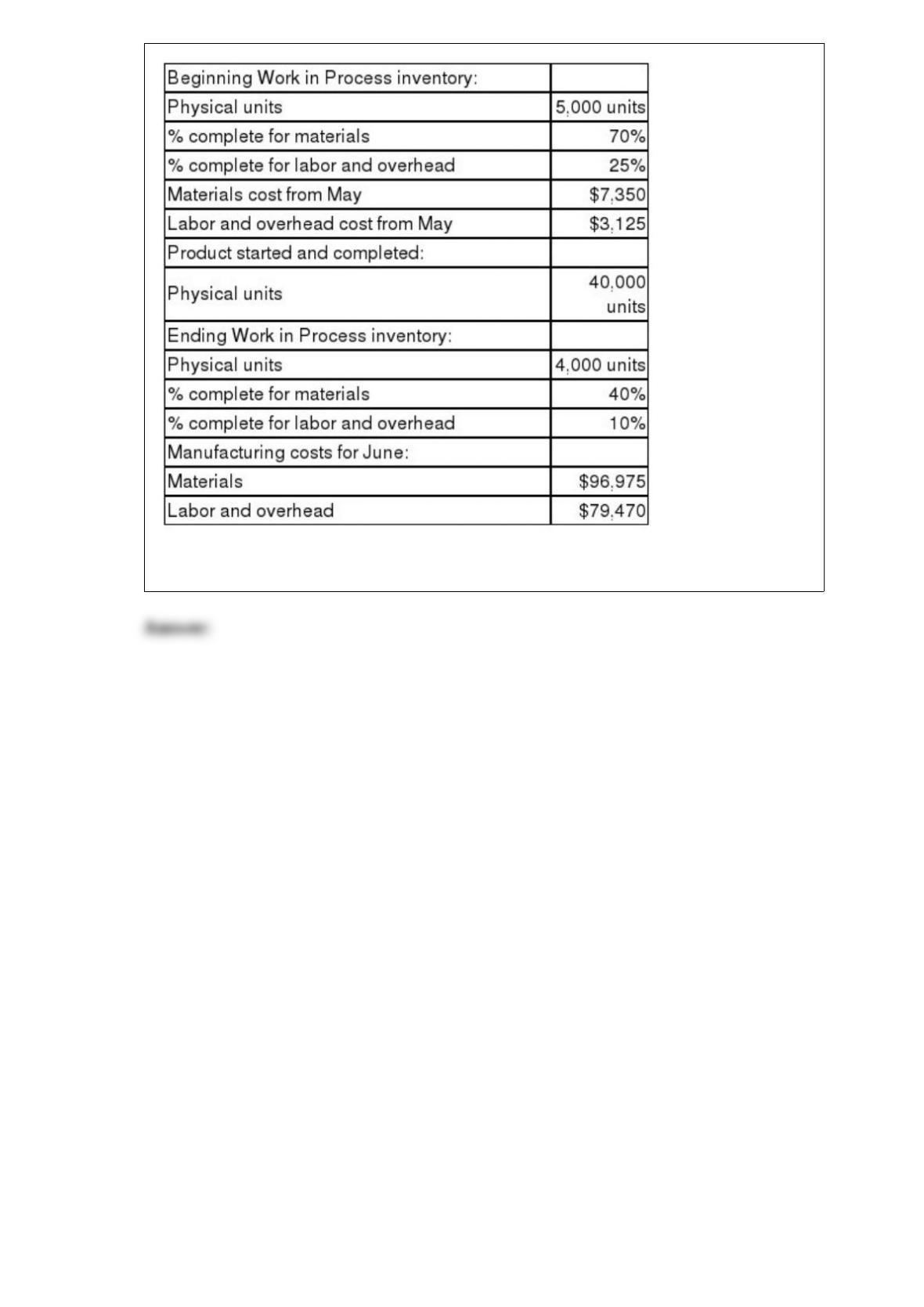

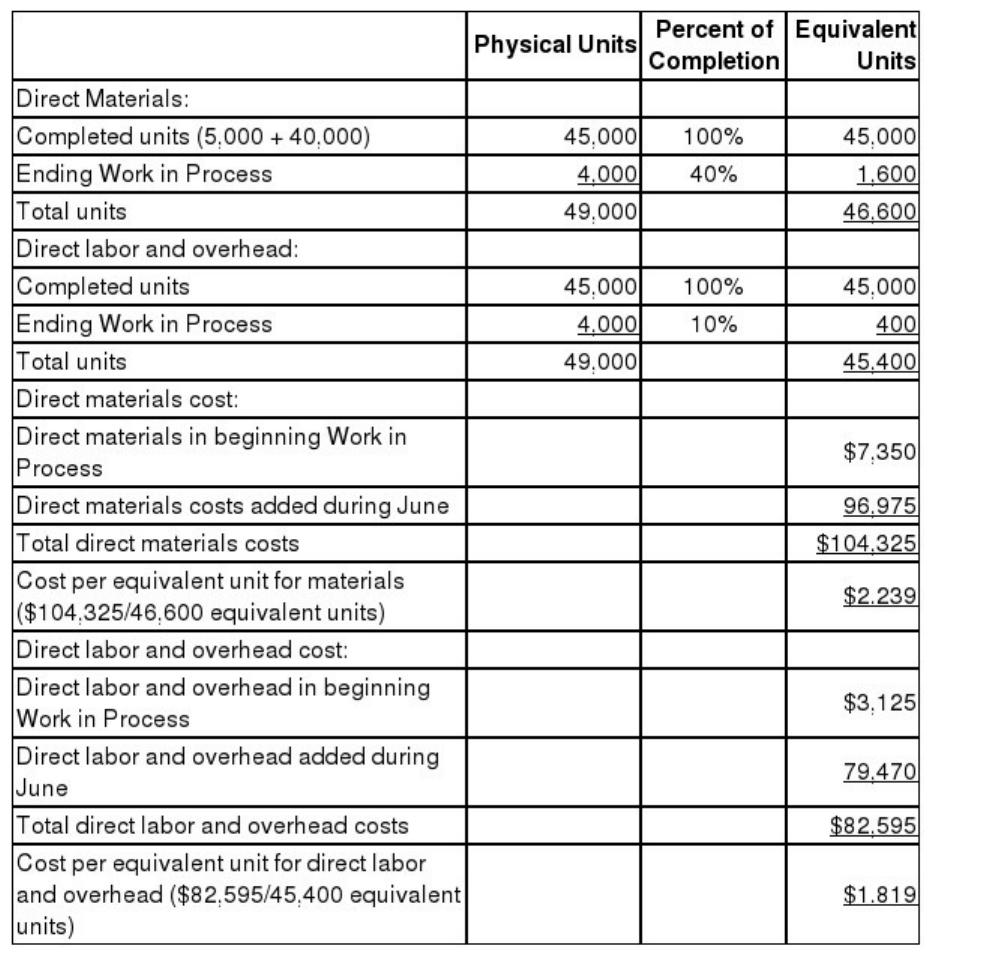

23) Refer to the following information about the Finishing Department in the Davidson

Factory for the month of June. Davidson Factory uses the weighted-average method of

inventory costing.

Compute the total cost of all units that were completed and transferred to finished

goods during June. Compute the total cost of the ending Work in Process inventory.

24) Discuss the options for the allocation of income and loss among partners, including

with and without a partnership agreement.

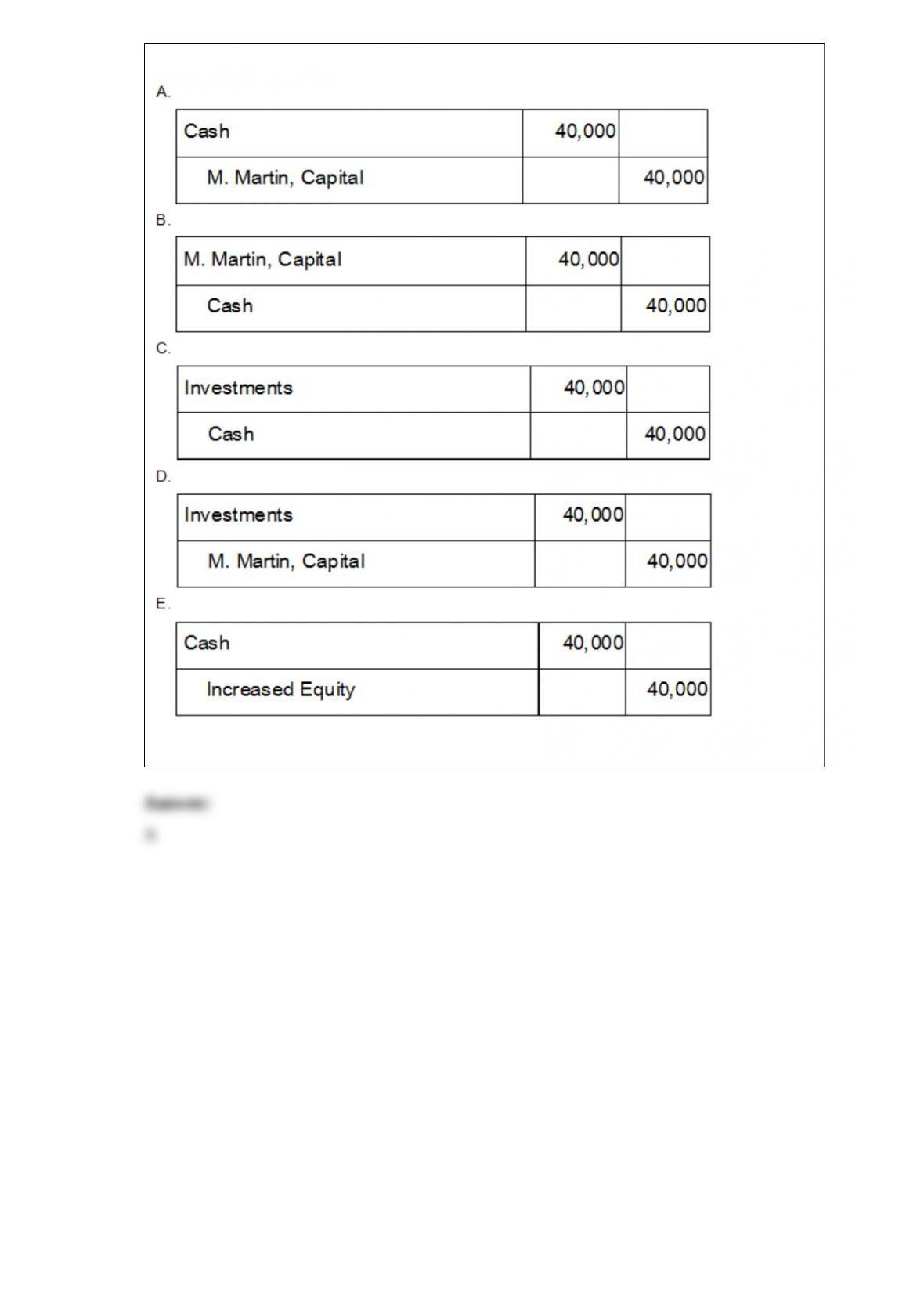

25) Mary Martin, the owner of Martin Consulting, started the business by investing

$40,000 cash. Identify the general journal entry below that Martin Consulting will make

to record the transaction.