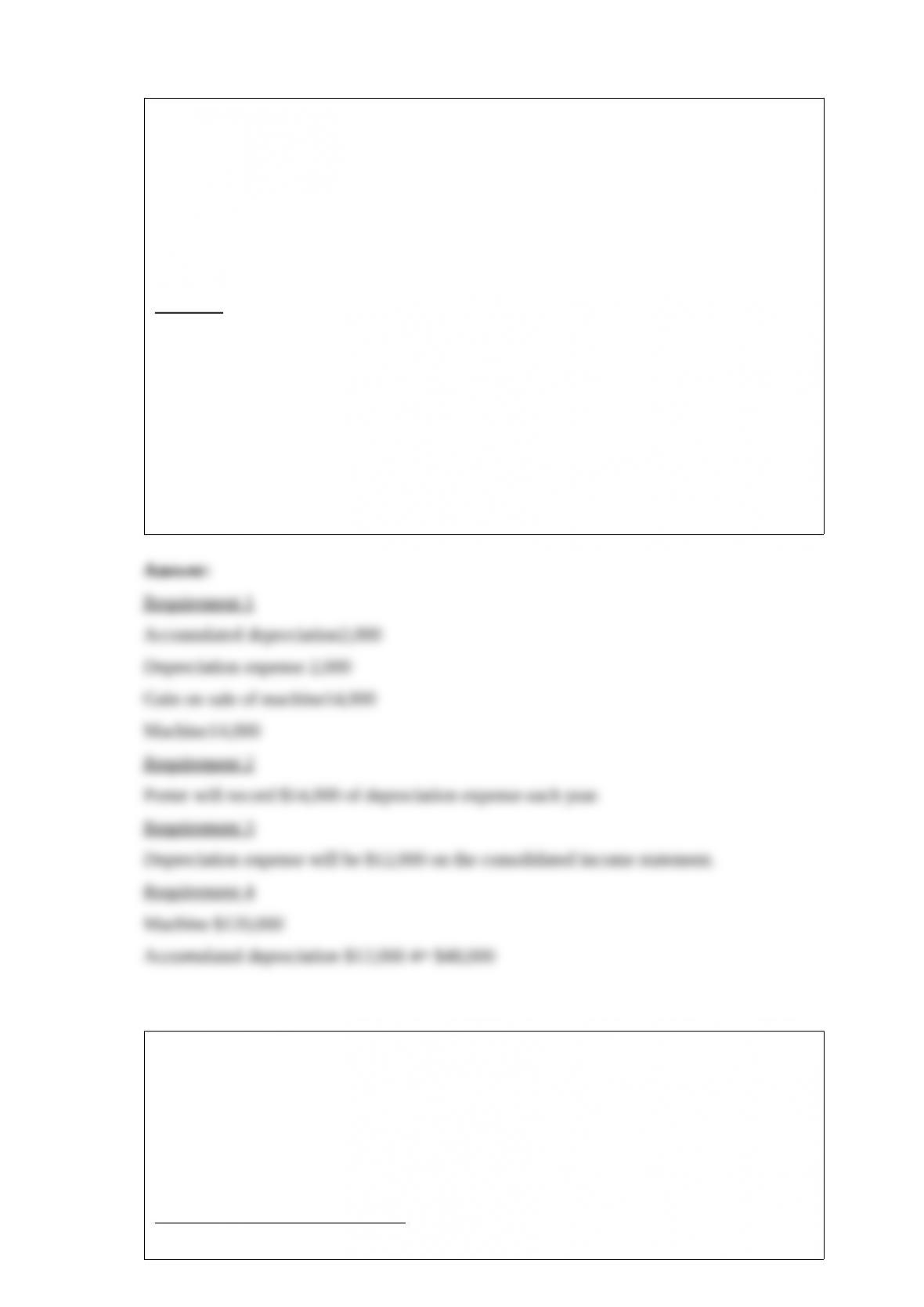

1) Porter Corporation acquired 70% of the outstanding voting common stock of

Sherman Inc. in 2004 . On January 1, 2005, Sherman Inc. purchased a depreciable

machine for $120,000 cash with an estimated useful life of 10 years that was

depreciated on a straight-line basis. The machine has no estimated salvage value.

Sherman used the machine until the end of 2007 . On January 2, 2008, Sherman sold

the machine to Porter who continued to use the same estimated life (seven years

remaining), salvage value and depreciation method that was used by Sherman. At the

end of 2008, Sherman reported a gain on sale of the machine of $14,000.

Required:

Answer the following questions concerning Porter and Sherman.

1>Prepare elimination/adjusting entries for the consolidated working papers for the year

ended December 31, 2008 .

2>How much depreciation expense relating to the transferred asset did Porter record in

2008 on the company’s separate books?

3>How much depreciation expense relating to the transferred asset was reported on the

consolidated income statement in 2008?

4>What amounts were reported for the Machine and the Accumulated Depreciation in

the consolidated balance sheet on December 31, 2008?

2) On December 31, 2010, Patenne Incorporated purchased 60% of Smolin

Manufacturing for $300,000. The book value and fair value of Smolin’s assets and

liabilities were equal with the exception of plant assets which were undervalued by

$60,000 and had a remaining life of 10 years, and a patent which was undervalued by

$40,000 and had a remaining life of 5 years. At December 31, 2012, the companies

showed the following balances on their respective adjusted trial balances:

PatenneSmolinSmolin

Book ValueBook ValueFair Value

Assets (includes

Investment in Smolin)$950,000300,000320,000

Plant assets – net 590,000150,000150,000

Patent 310,000200,000280,000

Expenses800,000300,000

Liabilities 480,000120,000120,000

Common Stock300,000100,000

Retained Earnings890,000330,000

Revenue980,000400,000

Requirement 1: Calculate the balance in the Plant assets – net and the Patent accounts

on the consolidated balance sheet as of December 31, 2012 .

Requirement 2: Calculate consolidated net income for 2012, and the amount allocated

to the controlling and noncontrolling interests.

Requirement 3: Calculate the balance of the noncontrolling interest in Smolin to be

reported on the consolidated balance sheet at December 31, 2012 .

3) Lesher Corporation lost their primary contract and entered into voluntary Chapter 7

bankruptcy in the early part of 2012 . By July 1, all assets were converted into cash, the

secured creditors were paid, and $124,500 in cash was left to pay the remaining claims

as follows:

Accounts payable$50,000

Claims incurred between the date of filing an involuntary

bankruptcy petition and the date an interim trustee is appointed8,000

Payroll taxes withheld14,000

Wages payable (all under $10,000 per employee; earned within

90 days of filing bankruptcy petition)56,000

Unsecured note payable37,500

Accrued interest on the note payable2,000

Administrative expenses of the trustee22,000

Total$189,500

Required:

Classify the claims by their Chapter 7 priority ranking, and analyze which amounts will

be paid and which amounts will be written off.

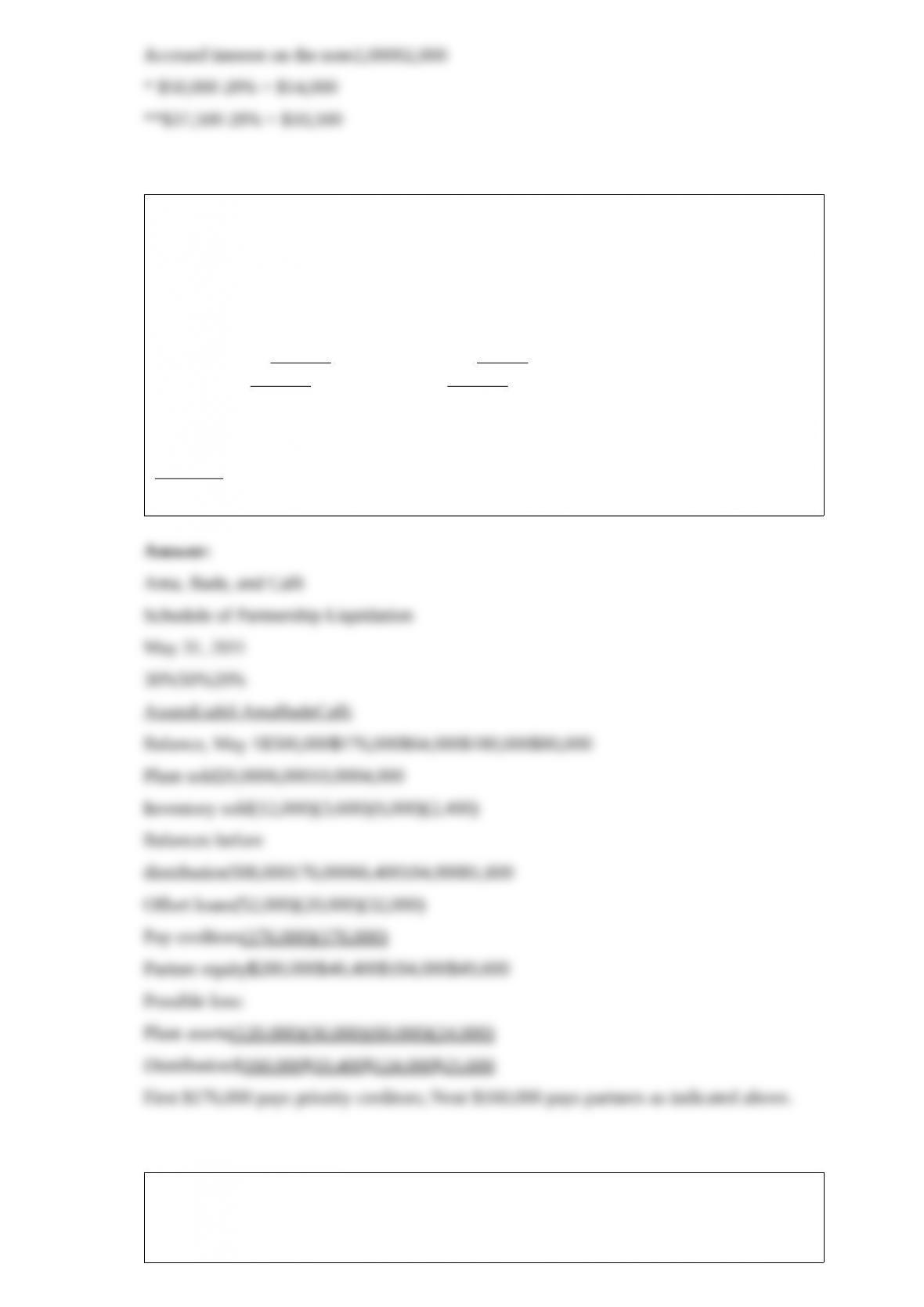

4) The balance sheet of the Ama, Bade, and Calli partnership on May 1, 2011 (before

commencement of partnership liquidation) was as follows:

Cash$108,000Accounts payable$56,000

Inventory120,000Notes payable120,000

Loan to Ama20,000Ama, capital (30%)64,000

Loan to Calli32,000Bade, capital (50%)180,000

Plant assets-net220,000Calli, capital (20%)80,000

Total assets$500,000Total liab./equity$500,000

Liquidation events in May were as follows:

– The inventory was sold for $12,000 below book value;

– Plant assets with a book value of $100,000 were sold for $120,000.

Required:

Determine how the available cash on May 31, 2011 should be distributed.

5) On January 1, 2011, Palling Corporation purchased 70% of the common stock of

Sam’s Storage Systems for $320,000 when Sam’s had Common Stock outstanding of

$100,000 and Retained Earnings of $200,000. Any excess differential was attributed to

goodwill.

At the end of 2011, Palling and Sam’s had unrealized inventory profits from

intercompany sales of $6,000 and $8,000, respectively. These year-end profit amounts

were realized in 2012 . At the end of 2012, Palling held inventory acquired from Sam’s

with a $10,000 unrealized profit. Palling reported separate income of $100,000 for 2012

and paid dividends of $30,000. Sam’s reported separate income of $70,000 for 2012 and

paid dividends of $20,000.

Required:

Compute the controlling interest share of consolidated net income for 2012 .

6) Wild West, Incorporated (a U.S. corporation) sold inventory to a company in the

Philippines for 1,600,000 pesos on account on February 1, 2011, with payment

expected in 90 days. Wild West entered into a forward contract to hedge this

transaction, and properly accounts for the transaction as a cash flow hedge. Wild West

has a March 31 fiscal year end, and uses an 8% discount rate, resulting in a 30-day

present value factor of .9934. The forward contract is settled net. The relevant exchange

rates are shown below:

Required:

Record the journal entries needed by Wild West on February 1, March 31, and May 2 .

Round all entries to the nearest whole dollar.

7) Wilhelman University, a not-for-profit, nongovernmental university, had the

following transactions in 2011 .

1>Tuition bills were sent amounting to $4,000,000, with tuition waivers granted on that

amount of $200,000.

2>State funding was received in the amount of $2,000,000.

3>The bookstore and cafeteria sales amounted to $1,600,000, and their cost of sales

was $1,500,000. Assume cash sales and cash purchases for these auxiliary operations.

4>Endowment income amounted to $100,000 that was restricted to chair the accounting

department, and $200,000 of unrestricted income.

5>Expenses were incurred and paid as follows: faculty, $3,800,000 (including faculty

chair, paid in part by endowment income); Student services, $250,000; Facilities

operations, $350,000; and scholarships (excluding tuition waived), $400,000.

Required:

Prepare the journal entries for 2011 for Wilhelman University.

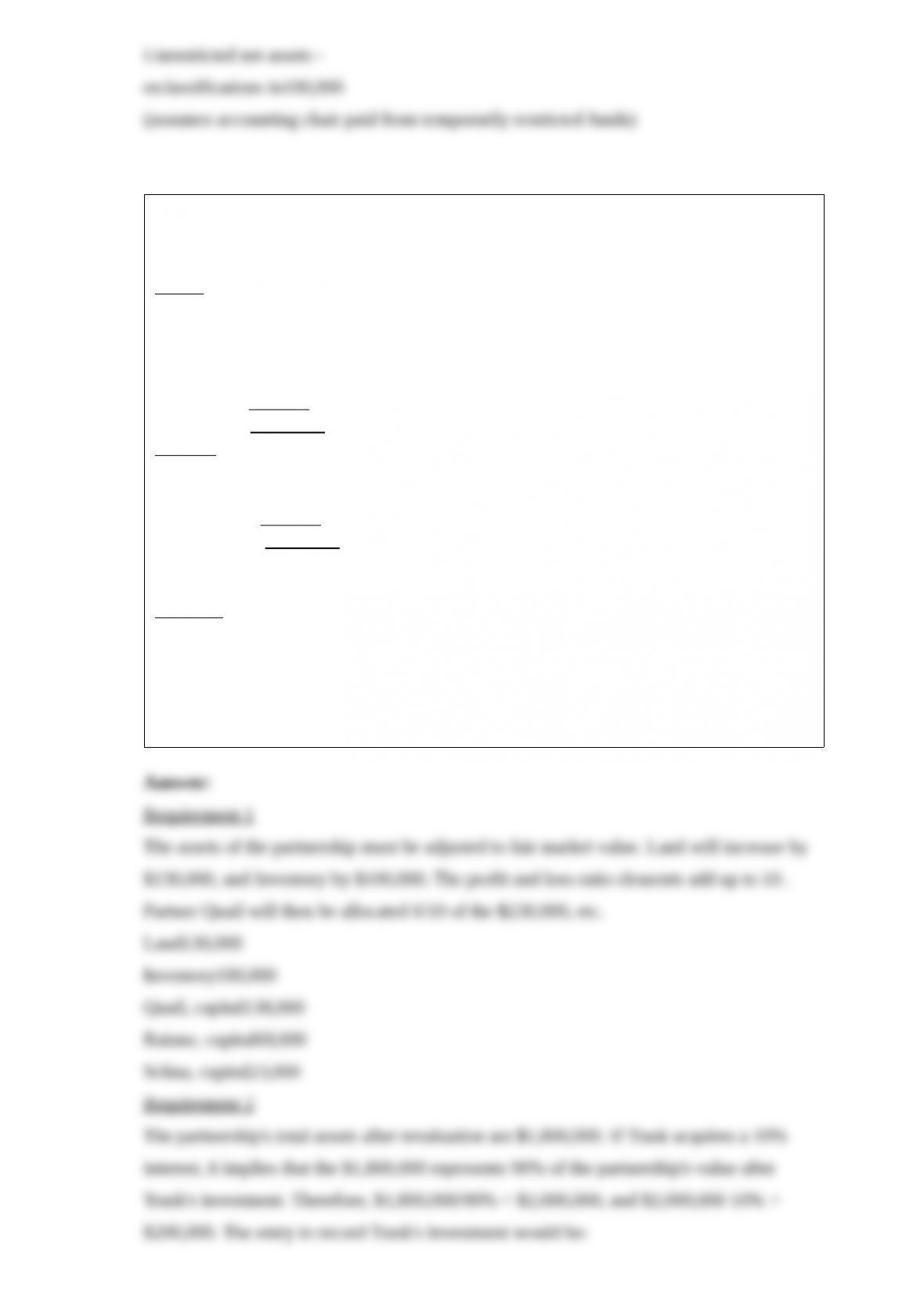

8) A summary balance sheet for the partnership of Quail, Rainne and Selma on

December 31, 2011 is shown below. Partners Quail, Rainne and Selma allocate profit

and loss in their respective ratios of 6:3:1.

Assets

Cash$ 320,000

Marketable securities640,000

Inventory270,000

Land130,000

Building-net210,000

Total assets$1,570,000

Equities

Quail, capital$ 670,000

Rainne, capital580,000

Selma, capital320,000

Total equities$1,570,000

The partners agree to admit Trask for a one-tenth interest. The fair market value for

partnership land is $260,000, and the fair market value of the inventory is $370,000.

Required:

1>Record the entry to revalue the partnership assets prior to the admission of Trask.

2>Calculate how much Trask will have to invest to acquire a 10% interest.

3>Assume the partnership assets are not revalued. If Trask paid $300,000 to the

partnership in exchange for a 10% interest, what would be the bonus that is allocated to

each partner’s capital account?

9) On September 1, 2011, Nelson Corporation acquired a 90% interest in Corbin

Corporation for $900,000. Corbin’s stockholders’ equity at January 1, 2011 consisted of

$200,000 of Common Stock and $600,000 of Retained Earnings. The book values of its

assets and liabilities were equal to their respective fair values on this date. All excess

purchase cost was attributed to goodwill.

During 2011, Corbin uniformly earned $98,000 and paid dividends of $19,000 on each

of four dates: February 1, June 1, August 1, and December 1 .

Required: Compute the following:

1> Implied goodwill associated with Corbin Corporation based on Nelson’s purchase

price on September 1, 2011 .

2> Nelson’s income from Corbin for 2011 .

3> Preacquisition income for Nelson Corporation and Subsidiary for 2011 .

4> Noncontrolling interest share for 2011 .

5> What is the balance in Nelson’s Investment in Corbin account at December 31,

2011?

10) On December 31, 2011, Lorna Corporation has the following information available:

Common stock, $10 par$200,000

Additional paid-in capital60,000

Retained earnings40,000

Total stockholders’ equity$300,000

On December 31, 2011, Gerald Corporation buys an 80% interest in Lorna Corporation

for $240,000. On December 31, 2011, the fair value of Lorna’s assets and liabilities are

equal to the respective book values.

Required:

1> On January 1, 2012, Lorna Corporation buys 500 shares of common stock from

noncontrolling stockholders at $20 per share. Prepare the journal entry for Gerald

Corporation on January 1, 2012 . Use four decimal places for the ownership percentage.

2> On January 1, 2012, Lorna Corporation buys 500 shares of common stock from

noncontrolling stockholders at $30 per share. Prepare the journal entry for Gerald

Corporation on January 1, 2012 . Use four decimal places for the ownership percentage.

3> On January 1, 2012, Lorna Corporation buys 500 shares of common stock from

noncontrolling stockholders at $10 per share. Prepare the journal entry for Gerald

Corporation on January 1, 2012 . Use four decimal places for the ownership percentage.