When there is an ethical conflict, the management accountant should resign if the

immediate supervisor is involved in the conflict.

If a bond with a face value of $1,000 and a face interest rate of 7 percent is issued for

$970, the market interest rate at the date of issuance must have been less than 7 percent.

It is necessary to know the budgeted number of unit sales to prepare production budget.

A process costing system first assigns the costs to the products manufactured by the

departments, and then traces the costs of direct materials, direct labor, and overhead to

departments.

The four stages of the management process are: planning, performing, evaluating, and

communicating.

The balances of all the real (permanent) accounts are the same on the adjusted trial

balance as they are on a post-closing trial balance.

Vertical analysis is the same as trend analysis.

Regulatory agencies are considered information users with an indirect financial interest.

Cost centers have well-defined links between the cost of the resources and the resulting

products.

On a statement of cash flows prepared using the direct method, if accounts receivable

decrease from one accounting period to the next, cash receipts from sales will not be as

great as sales.

FOB shipping point means that the seller incurs the shipping costs.

Which of the following is a document prepared every period for each process?

A.Process cost card

B.Process cost report

C.Process cost control sheet

D.Process cost recognition card

Which of the following is not included in conversion costs?

A.Indirect labor

B.Direct labor

C.Direct materials

D.Overhead

Closing entries ultimately will affect

A.total liabilities.

B.the Cash account.

C.the owner’s Capital account.

D.total assets.

Greco Co. issued ten-year term bonds on January 1, 20×5, with a face value of

$1,600,000. The face interest rate is 6 percent and interest is payable semi-annually on

June 30 and December 31. The bonds were issued for $1,381,920 to yield an effective

annual rate of 8 percent. The effective interest method of amortization is to be used. The

carrying value of the bonds payable on the December 31, 20×5, balance sheet date

should be

A.$1,392,824.

B.$1,396,472.

C.$1,396,764.

D.$1,381,920.

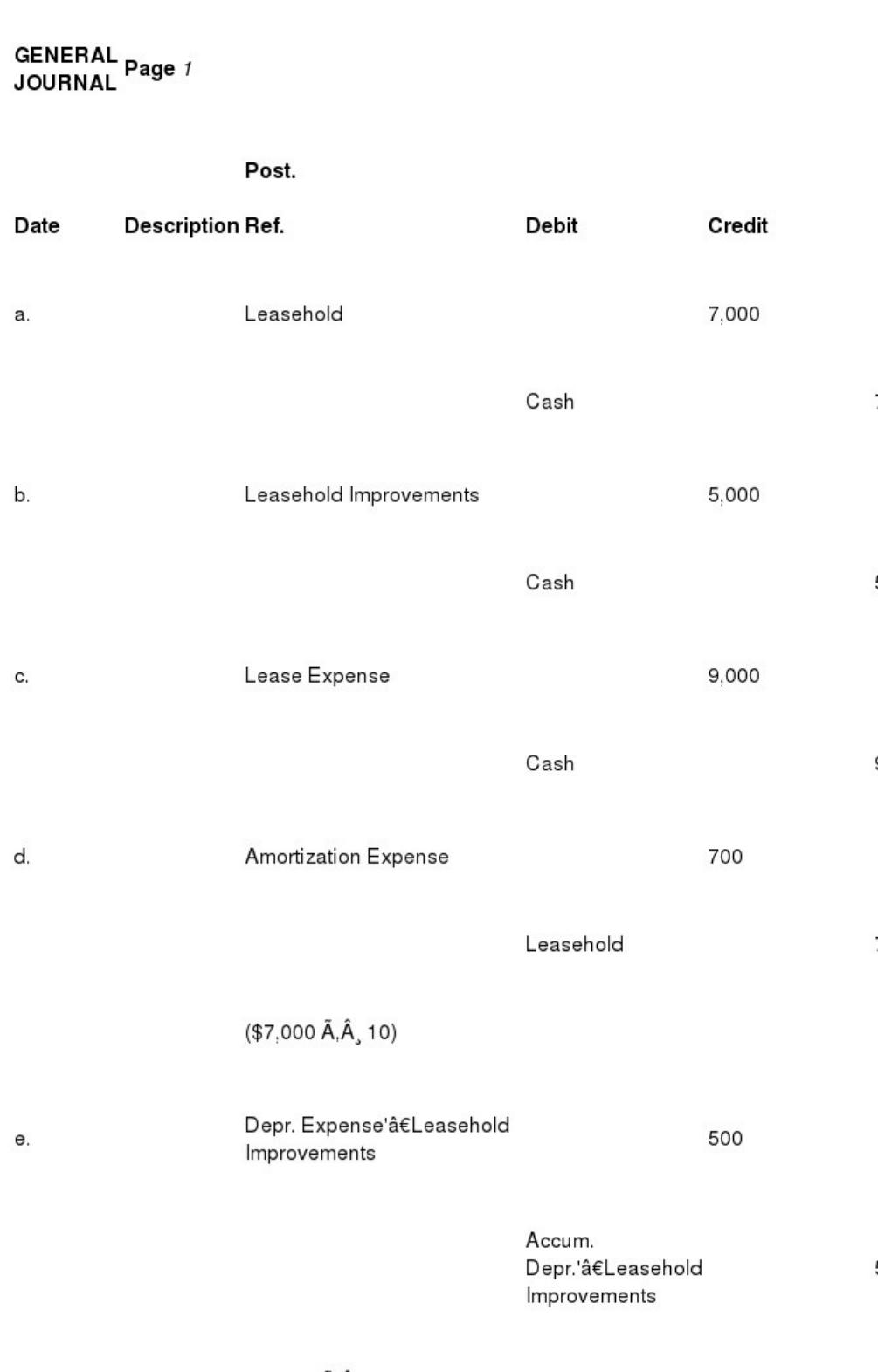

Mike Nickell obtained a ten-year sublease on a busy corner to open a used car business.

To obtain the sublease, he had to pay $7,000 to the current tenant, who had 12 years to

go on his lease. The annual cost of the lease is $9,000. In addition to paying for the

sublease, Mike paid $5,000 to pave the lot. The paving will have no residual value after

its useful life of ten years. Prepare entries in journal form to record the following (omit

explanations):

a. The payment for the sublease

b. The payment for the paving

c. The lease payment for the first year

d. The expense, if any, associated with the sublease for the first year

e. The expense, if any, associated with the paving, using the straight-line method for the

first year

The account Allowance for Uncollectible Accounts is classified as a(n)

A.contra account to Uncollectible Accounts Expense.

B.expense.

C.liability.

D.contra account to Accounts Receivable.

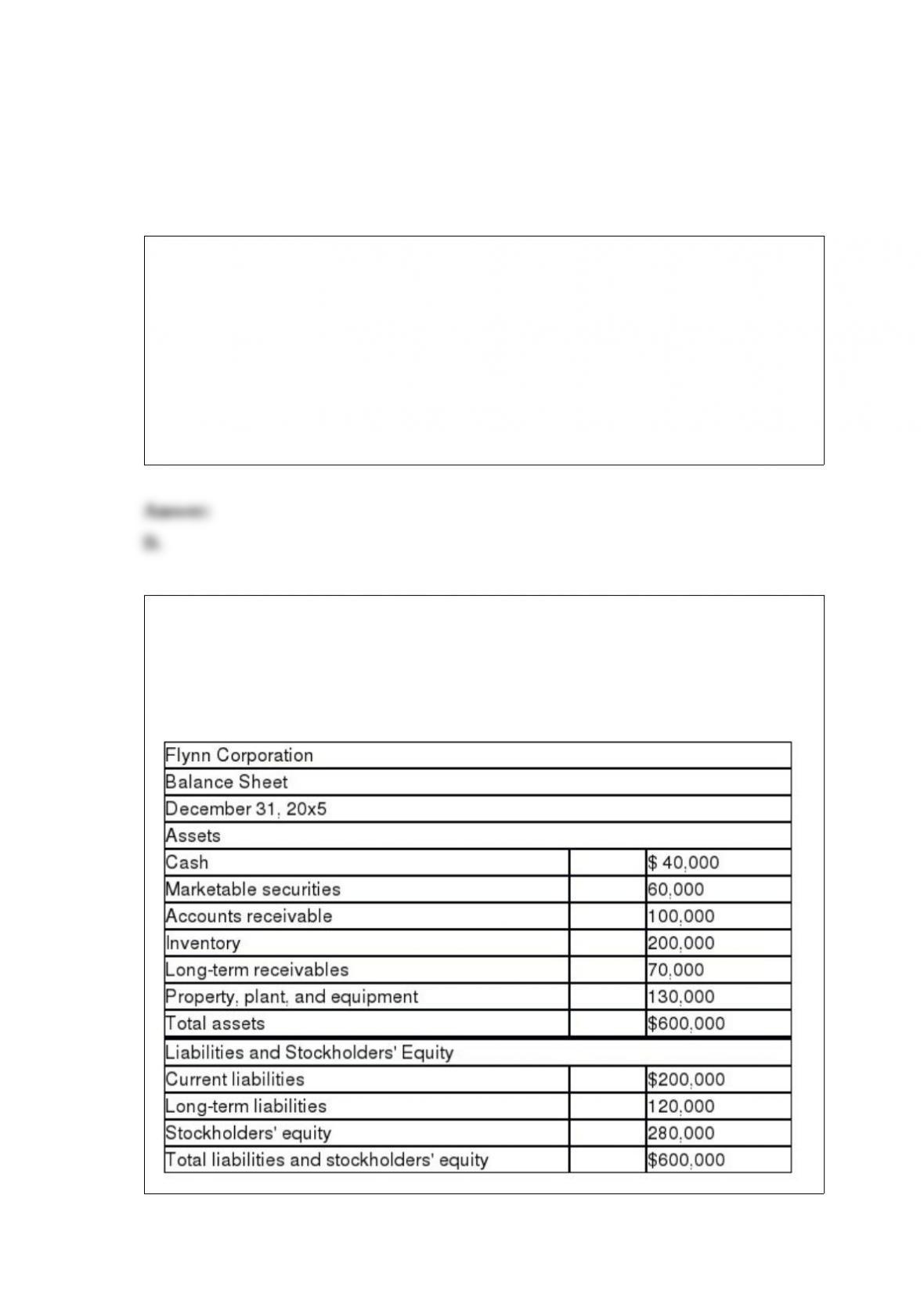

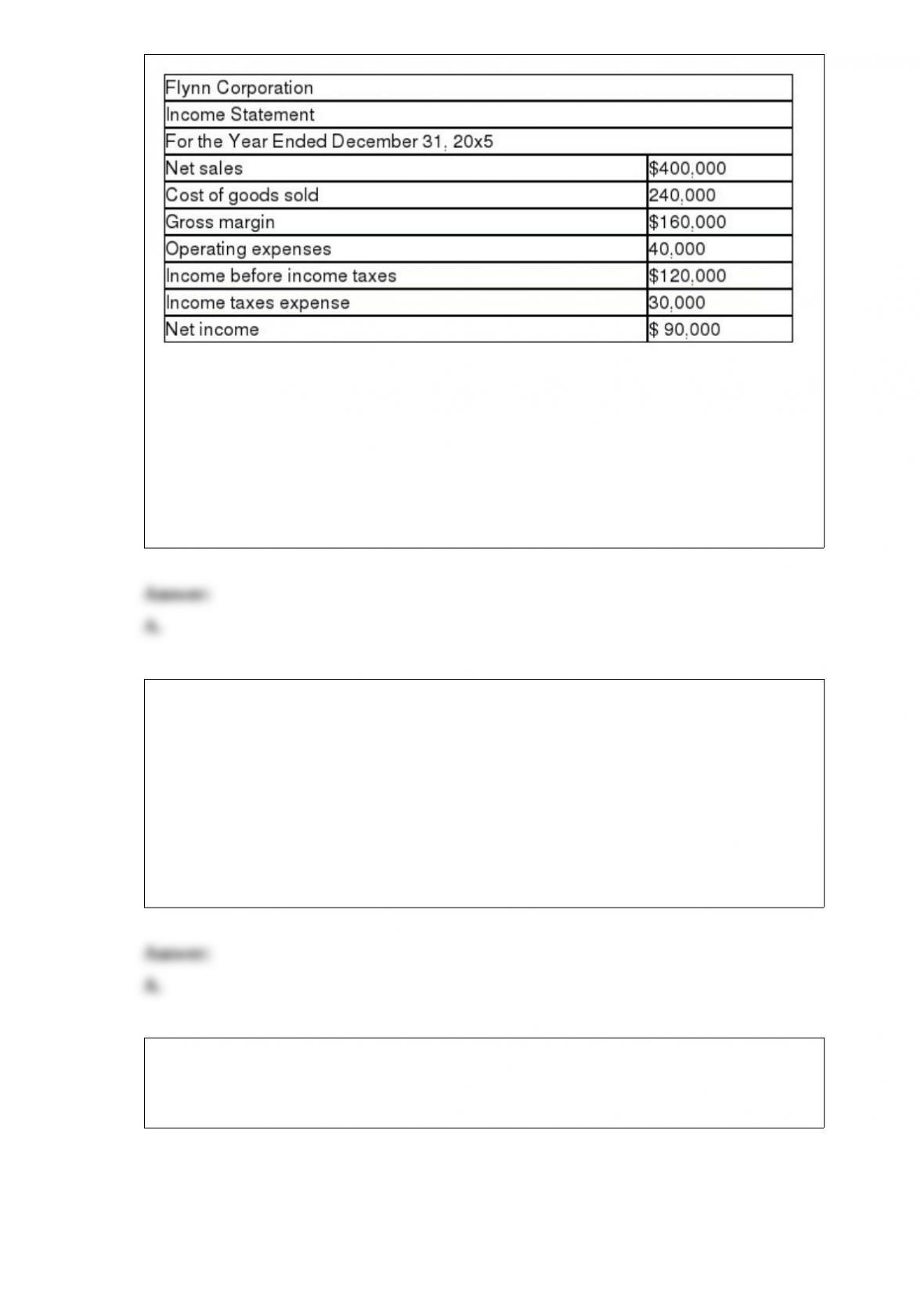

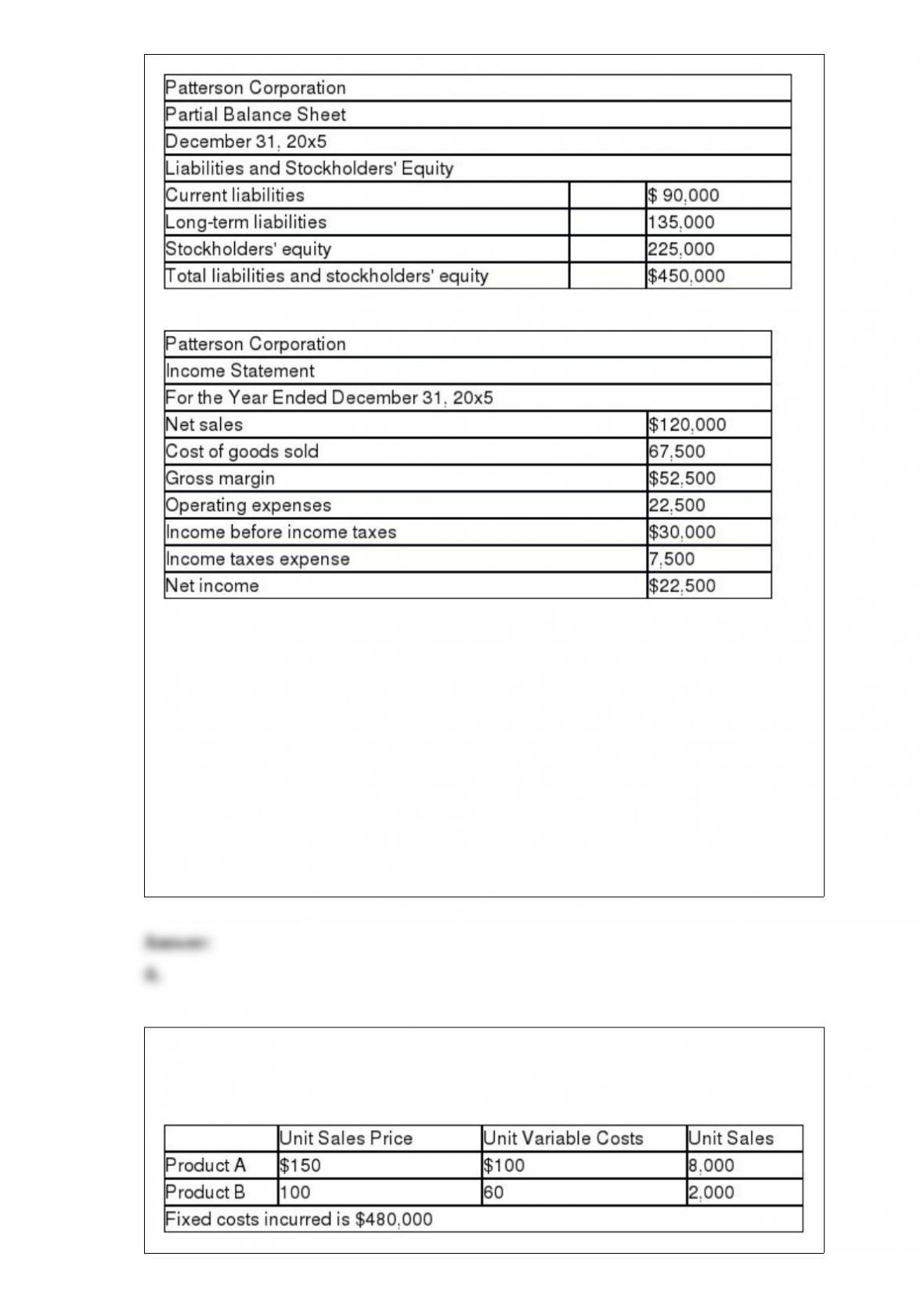

Following are the financial statements for Flynn Corporation for the year ended

December 31, 20×5. Assume that all balance sheet amounts represent both average and

ending figures.

What is the receivable turnover for this corporation? Round your answer to one decimal

place.

A.4.0 times

B.3.0 times

C.2.4 times

D.0.9 times

A process costing system accounts for product costs

A.for a specific period of time.

B.always in a single Work in Process Inventory account.

C.without regard to the process that created the cost.

D.for specific orders.

The following information pertains to Patterson Corporation. Assume that all balance

sheet amounts represent both average and ending figures.

Patterson Corporation had 6,000 shares of common stock issued and outstanding. The

market price of Patterson common stock on December 31, 20×5, was $20. Patterson

paid dividends of $2.50 per share during 20×5.

What is the dividend yield of this corporation? Round your answer to two decimal

places.

A.12.5 percent

B.18.75 percent

C.9.90 percent

D.6.25 percent

Lakeside has gathered the following data in order to calculate the weighted-average

breakeven point:

The weighted-average breakeven point is

A.11,429 units.

B.10,000 units.

C.5,333 units.

D.10,667 units.

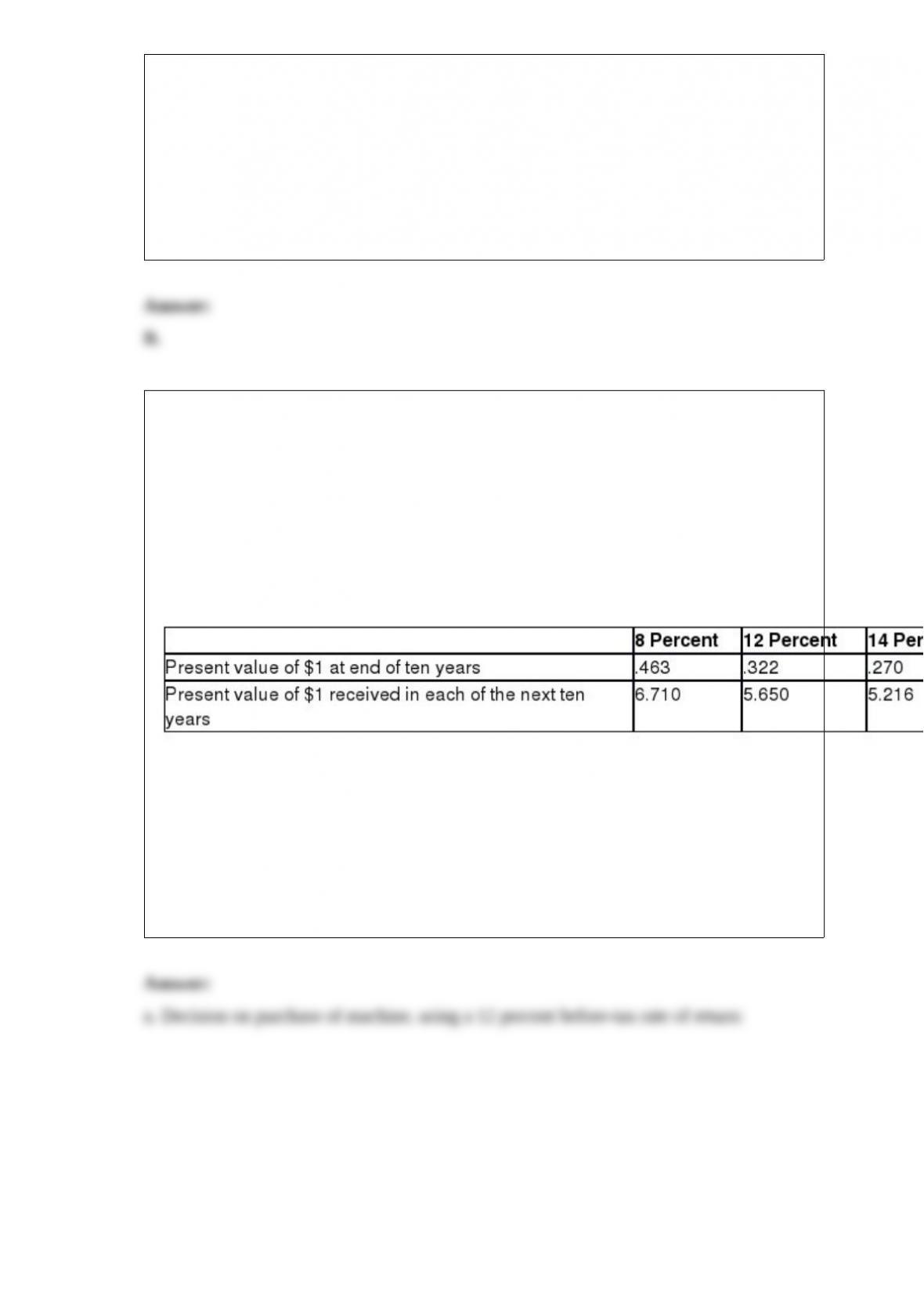

Management of the Krausse Savings and Loan Association is in the process of

evaluating the purchase of a new check sorting machine. The model under review will

cost $70,000 and will require installation costs of $10,000. Similar machines have a

ten-year life, and management has estimated that this sorter will have a residual value

of $10,000 at the end of its life. Annual cost savings to be generated by the sorter will

average $14,000 over the ten-year period. Management’s minimum desired rate of

return is 12 percent.

Present value multipliers:

a. Using before-tax information and the net present value method to evaluate this

capital investment, determine whether the company should purchase the check sorting

machine. Support your answer.

b. If management had decided on a minimum desired before-tax rate of return of 14

percent, should the check sorting machine be purchased? Show all computations to

support your answer.

Wean Corporation’s budgeted balance sheet for the coming year shows total assets of

$5,000,000 and total liabilities of $2,000,000. Common stock and retained earnings

make up the entire stockholders’ equity section of the balance sheet. Common stock

remains at its beginning balance of $1,500,000. The projected net income for the year is

$333,000. The company pays no dividends. What is the balance of retained earnings at

the beginning of the budget period?

A.$1,067,000

B.$1,167,000

C.$1,833,000

D.$1,500,000

Working capital measures

A.the excess of current assets over current liabilities’”what is on hand to fund business

operations.

B.the ability to earn a satisfactory income.

C.the amount of debt in the company.

D.the profitability of the business.

The other revenues and expenses section of a multistep income statement could include

all the following except

A.interest expense.

B.interest income.

C.dividend income.

D.insurance expense.

The following data were taken from the accounting records of a company that uses the

FIFO method in its process costing system:

Beginning work in process inventory:

20,000 units (materials 100% complete, conversion costs 60% complete)

Started in process during the period:

80,000 units

Ending work in process inventory:

30,000 units (materials 100% complete, conversion costs 70% complete)

The equivalent units are

A.materials, 90,000 units; conversion costs, 89,000 units.

B.materials, 100,000 units; conversion costs, 91,000 units.

C.materials, 60,000 units; conversion costs, 53,000 units.

D.materials, 80,000 units; conversion costs, 79,000 units.

Assume that the forecasted cost of goods sold is $800,000, budgeted selling and

administrative expenses are $320,000, planned capital expenditures are $320,000, and

the tax rate is 40 percent. What is the forecasted net income if 15,000 units are expected

to be sold at $150 per unit?

A.$678,000

B.$452,000

C.$805,000

D.$483,000

Stephen Company uses the FIFO method in its process costing system. Beginning

inventory in the mixing department consisted of 5,000 units that were 65 percent

complete with respect to conversion costs. Ending work in process inventory consisted

of 5,000 units that were 70 percent complete with respect to conversion costs. If 12,000

units were transferred to the next processing department during the period, the

equivalent units for conversion costs would be

A.13,750 units.

B.12,250 units.

C.10,250 units.

D.13,000 units.

Equipment is purchased for $40,000. It has an eight-year useful life and a $21,375

residual value. Under the double-declining-balance method, what is the depreciation

expense for year 3?

A.$875

B.$1,125

C.$1,375

D.$5,625

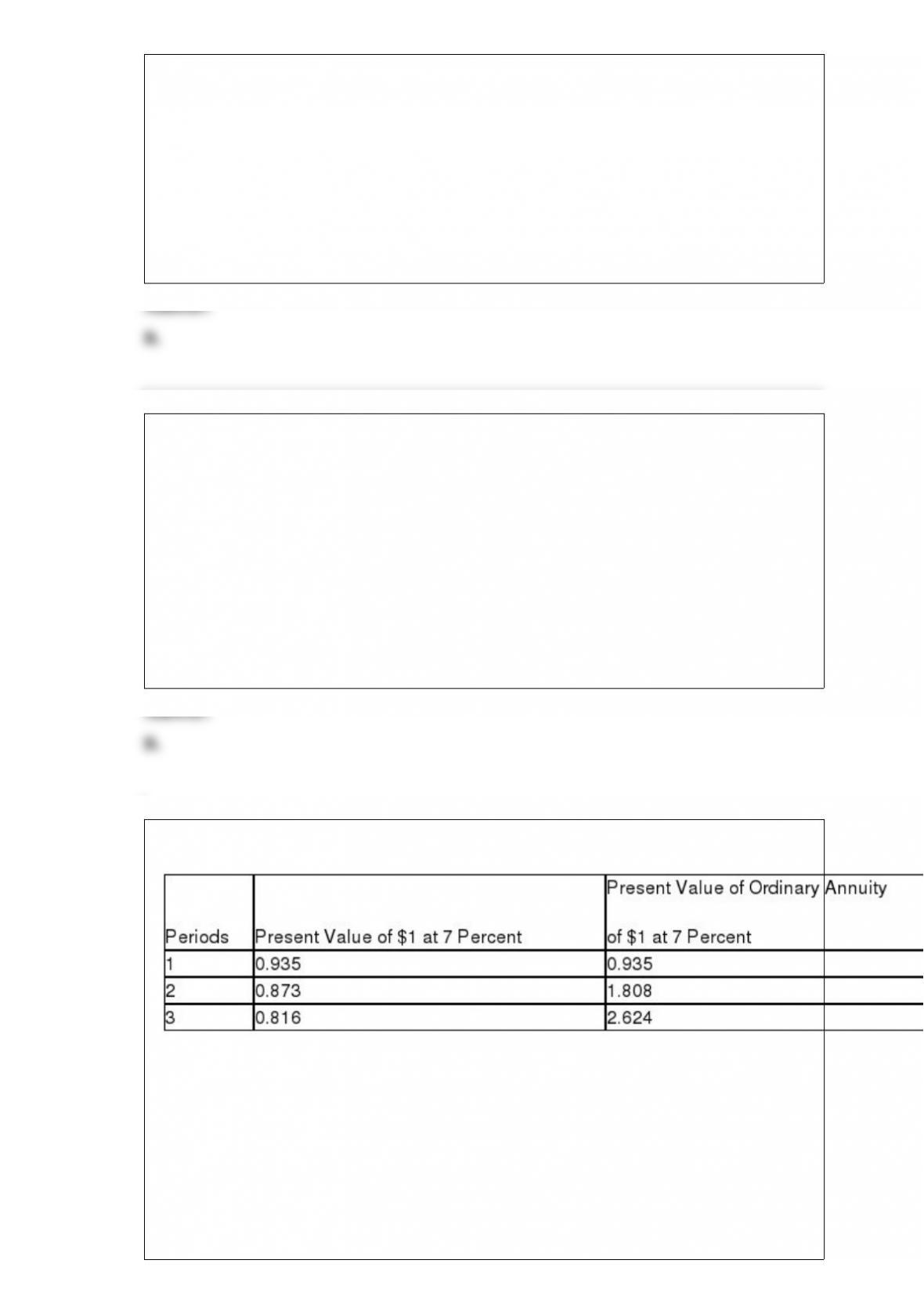

Use this information to answer the following question.

What amount must be deposited today to grow to $900 in three years, assuming an APR

of 7 percent?

A.$662.00

B.$734.40

C.$342.98

D.$841.50

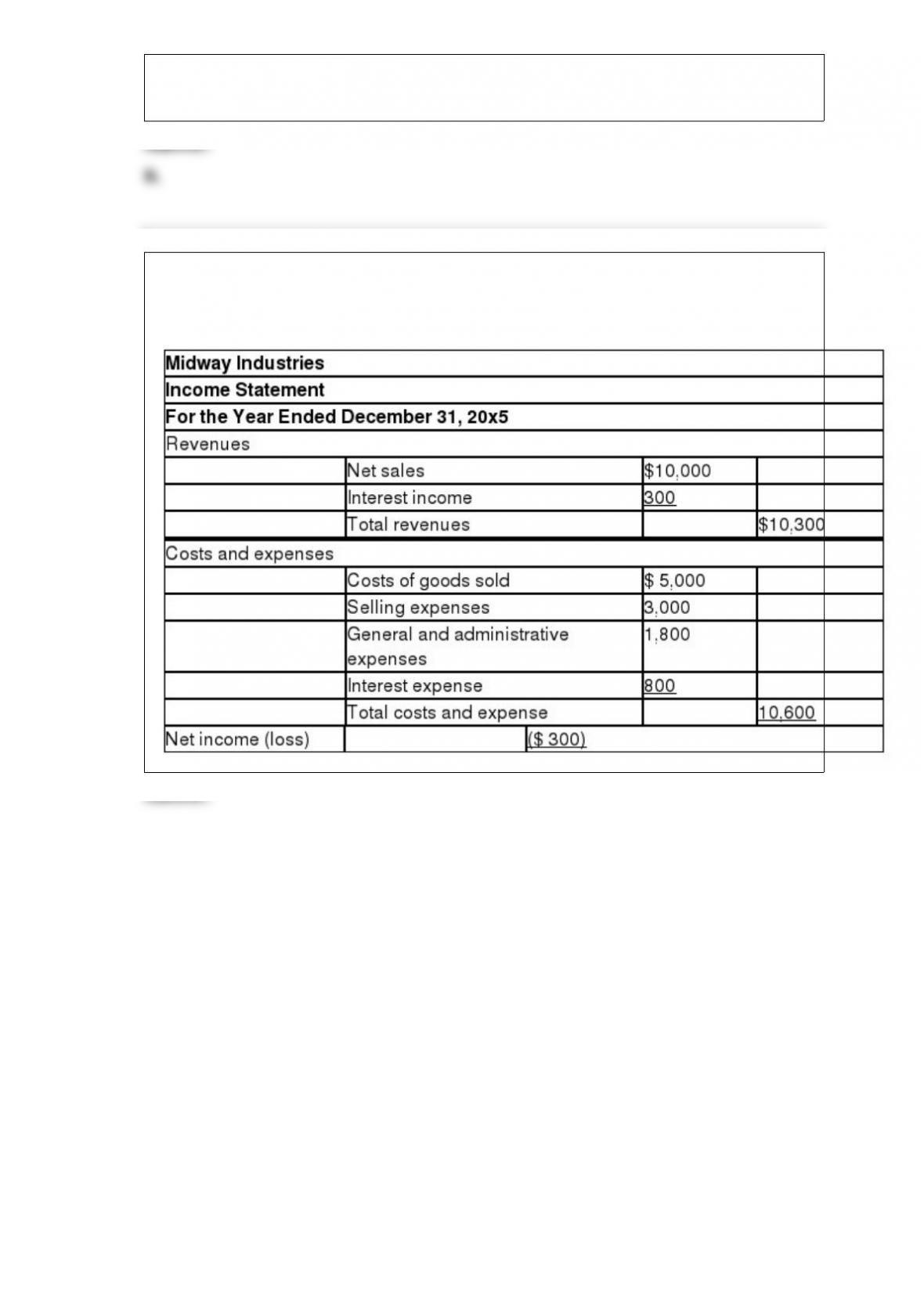

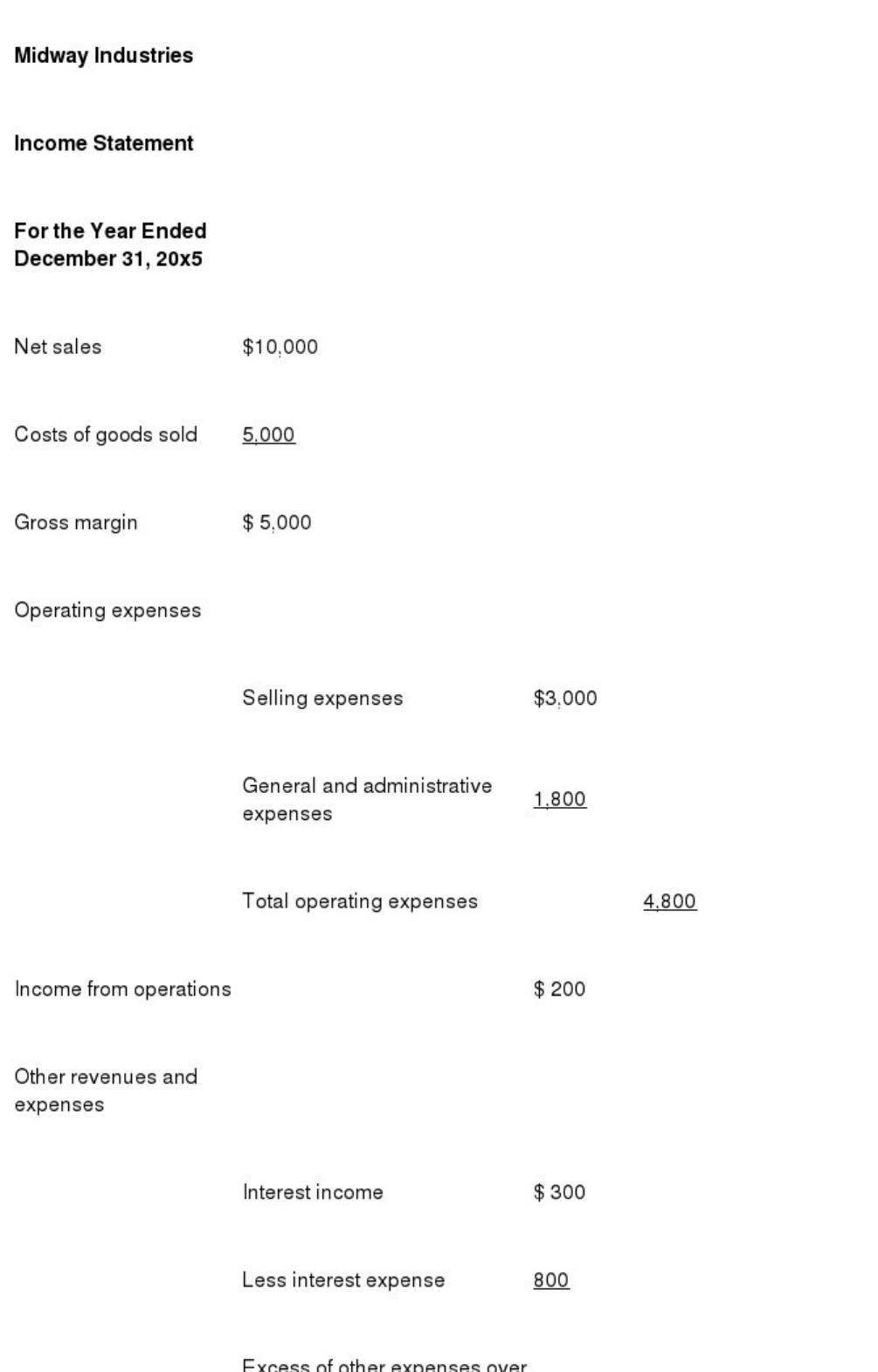

Use the information from the following single-step income statement to prepare a

multistep income statement in proper form.

Chelsea, Jack, and Connor have a partnership. Chelsea wishes to withdraw from the

partnership by removing assets that represent less than her current capital balance.

Discuss how this transaction is accounted for on the partnership books.

Joan contributes cash of $48,000, and Jamie contributes office equipment that cost

$40,000 but is valued at $32,000 to the formation of a new partnership. The entry to

record the investments in the partnership is:

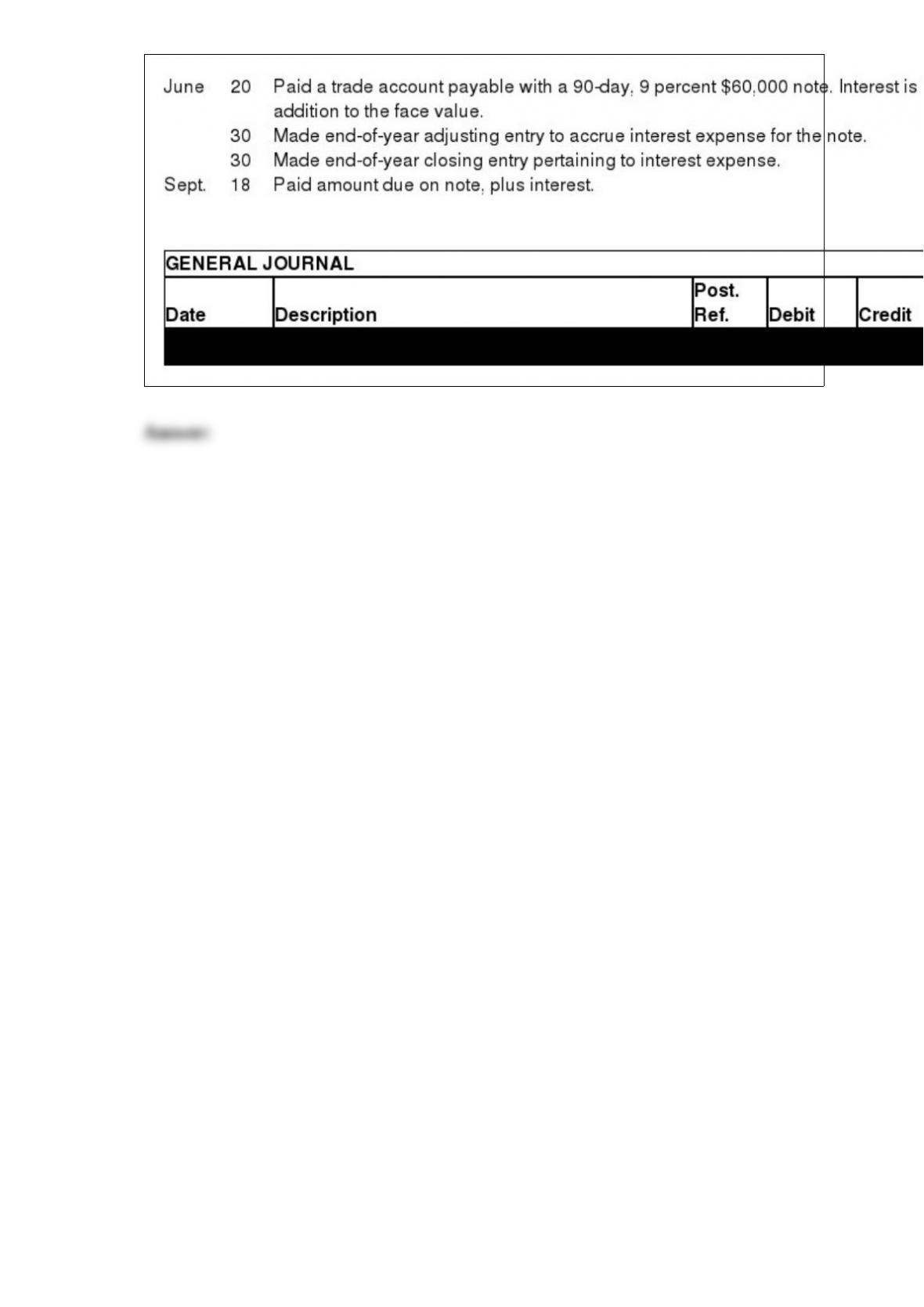

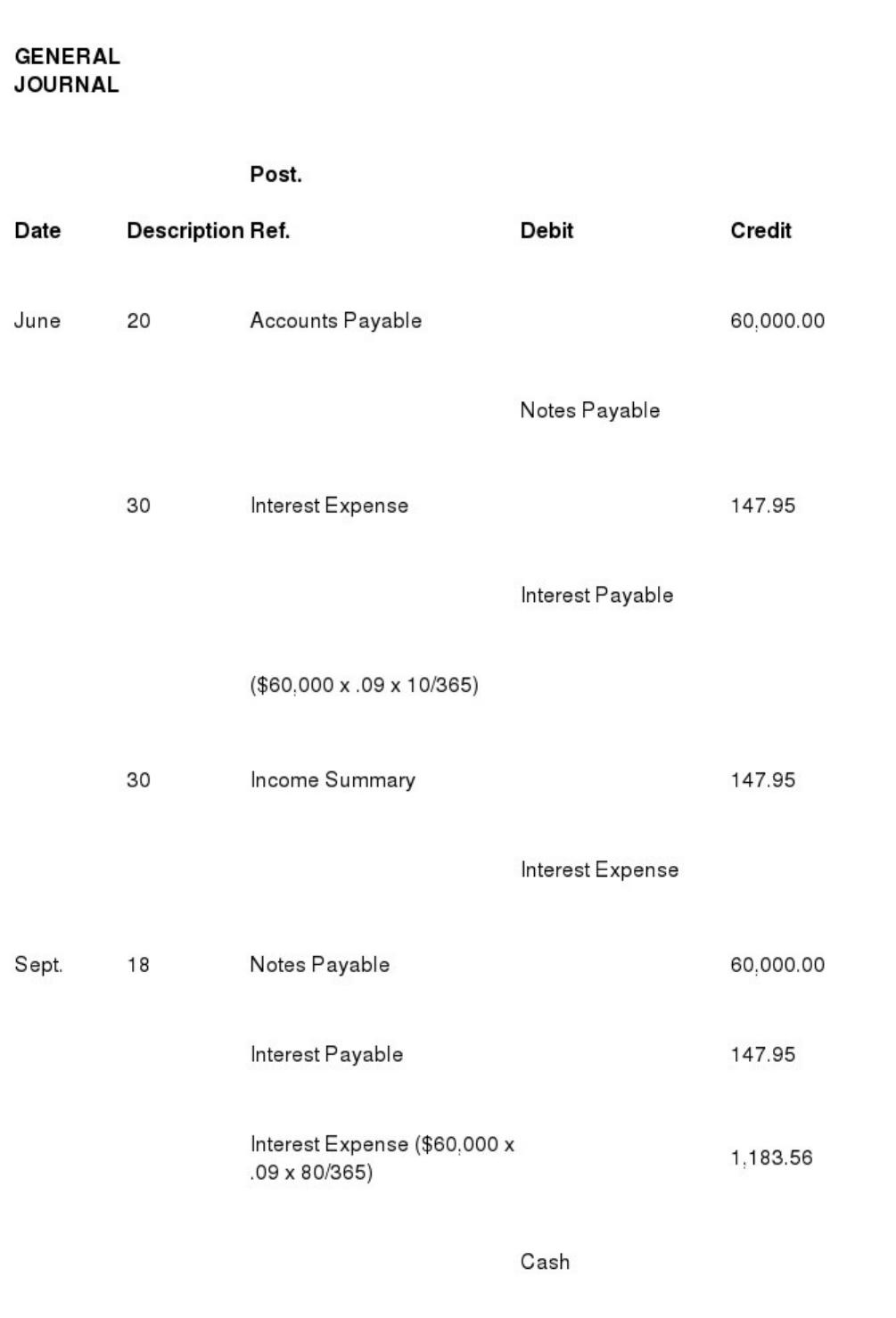

Prepare journal entries for the following transactions involving notes payable for

Homer Company, whose fiscal year ends June 30. Omit explanations.

Doug Riley is the only accountant employed at Carmen Enterprises. When asked by the

company president if the financial statements had been prepared yet, Doug answered

that he had completed all of his work except the preparation of the statements. He

added that the net income that would appear on the current income statement would be

$392,180. Identify the two instances where Doug would have determined the net

income before he actually prepared the financial statements.