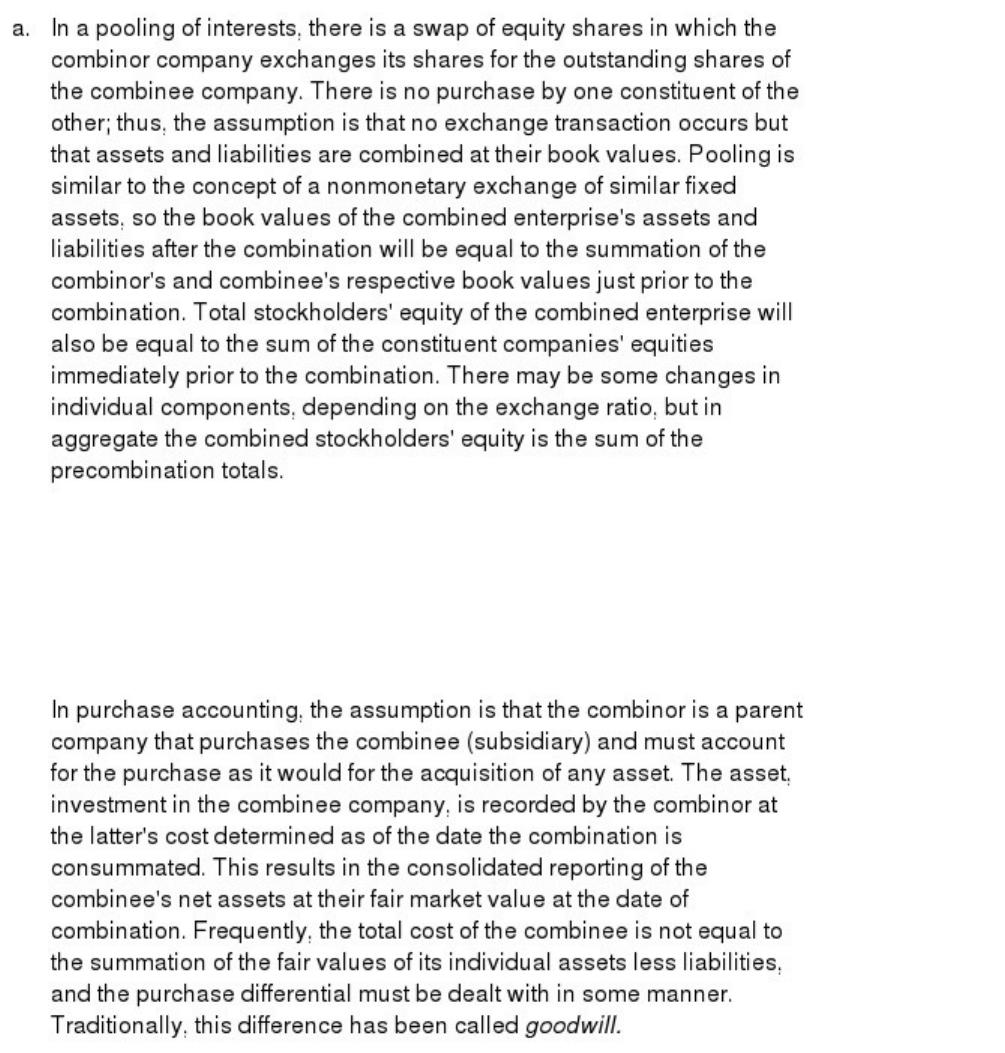

The International Accounting Standards Committee was formed in an attempt at

economic integration of member countries.

Economic profit is equal to net operating profit less taxes paid minus a charge on

invested capital.

How did the definition of accounting change from the period before ASOBAT to the

issuance of SATTA in 1977?

SFAC No. 1 maintains that financial statements should be geared toward specific needs

of particular user groups.

The importance of the auditing function relative to the management consulting function

is declining in major auditing firms.

Measurement is an integral part of accounting theory.

Good financial reporting will lower a firm’s cost of capital.

An important difference between deductive and inductive research is that inductive

research is sometimes global in content, whereas deductive research is usually

particularistic.

Agency theory explains that firms have an incentive to report voluntarily to the capital

market because they are competing for risk capital.

The efficient-markets hypothesis refers to the speed with which financial analysts are

able to predict a firm’s cash flows.

Research studies have predominantly supported the naive-investor hypothesis.

Rigid uniformity has been formulated as an alternative to finite uniformity.

The objectives of business financial reporting detailed in the conceptual framework

proceeded directly from which of the following documents?

a. The Trueblood Report

b. SATTA

c. APB Statement 4

d. ASOBAT

Which of the following organizations was formed in an attempt at economic

integration, and has also been concerned with harmonization of accounting standard of

its member nations?

a. The International Accounting Standards Committee

b. The International Federation of Accountants

c. The European Union

d. The International Organization of Security Commissions

In which of the following ways did the charge to the Financial Accounting Standards

Board (FASB) differ from that given to the Accounting Principles Board (APB)?

a. The FASB was to establish standards of financial accounting and reporting in the

most efficient and complete manner possible.

b. The FASB was to work toward standard setting with a two-pronged approach.

c. The FASB was expected to stipulate principles of accounting as an underlying

framework.

d. The accounting standards established by the FASB were to be advisory rather than

mandatory.

Which of the following is not a reason cited in the text for the failure of the CAP and

the APB as regulatory bodies?

a. The SEC did not officially endorse private-sector standard setting until 1973.

b. The CAP and the APB lacked the necessary political structure to ensure their

survival.

c. Policy making was exposed to outside influence.

d. There appeared to be no due process in the determination of accounting and

disclosure rules.

Respond to the following:

What was the first pension accounting standard?

a. FASB Interpretation 3

b. ARB 36

c. SFAS No. 87

d. ERISA

Prior to the FASB, accounting regulation was done primarily by:

a. The SEC.

b. The FTC.

c. AICPA subcommittees.

d. Large accounting firms.

In 1918, the American Institute of Accountants (AIA) worked with which of the

following organizations to publish minimum standards for conducting a balance sheet

audit?

a. The Federal Trade Commission (FTC)

b. The Securities and Exchange Commission (SEC)

c. The American Society of Certified Public Accountants

d. The New York Stock Exchange (NYSE)

Which of the following represented the first formal attempt to develop “generally

accepted accounting principles”?

a. “Approved Methods for the Preparation of Balance Sheet Statements” in 1918

b. “Five broad accounting principles” in 1932

c. Accounting Research Bulletin (ARB) 43

d. The FASB’s conceptual framework project

Which of the following are defined in the text as basic assumptions concerning the

business environment?

a. Concepts

b. Principles

c. Postulates

d. Axioms

Which of the following brought accrual accounting to post retirement benefits other

than pensions (OPEB)?

a. SFAS No. 87

b. SFAS No. 106

c. SFAS No. 132

d. ERISA

Under which of the following theories would the accounting equation be Total Assets =

Total Equities (including liabilities)?

a. Residual equity theory

b. Proprietary theory

c. Entity theory

d. Commander theory

Which of the following represents the attribute(s) that must be measurable before

revenue is recognized?

a. Sales price and cash collections

b. Sales price

c. Cash collections

d. Sales price, cash collections, and future costs

Which of the following is considered a social goal related justification for imposing

financial reporting regulation?

a. Information symmetry

b. Comparability

c. A competitive capital market

d. All of the above

Which of the following is a true statement regarding deferred taxes under APB No. 11?

a. They were adjusted for tax rate changes.

b. They were viewed as deferred credits.

c. They resulted in balance sheet taking precedence over the income statement in

accounting for income taxes.

d. They were considered liabilities.

Which of the following is not a true statement?

a. ARB 51 prohibited consolidation of a subsidiary company unless majority ownership

exists.

b. ARB 51 took the view that majority ownership per se did not indicate control if

ownership were temporary or if for some reason control did not reside with the majority

owner.

c. ARB 51 permitted separate reporting for heterogeneous subsidiaries instead of

consolidation.

d. ARB 43 permitted separate reporting for foreign subsidiaries instead of

consolidation.

Of the valuation systems discussed in your text, which one is purely theoretical, with

virtually no operable practicability on a statement-wide basis?

a. Current value

b. Discounted cash flows

c. General price-level adjustment

d. Historical cost

Comprehensive income as displayed on the income statement represents:

a. An asset-liability approach.

b. A revenue-expense approach.

c. A current operating approach.

d. None of the above

Which of the following is not a reason why ARS 1 and ARS 3 fell short of the goal of

obtaining a framework for APB accounting opinions?

a. The authors refused to abandon historical cost.

b. The postulates were not complete and therefore could not exclude all value systems

other than the one prescribed in the principles.

c. At least one of the principles was not derived from any of the postulates.

d. The question of whether valuations of various assets were additive became an issue.

Respond to the following:

Which of the following is not true regarding the discussion memorandum that preceded

the conceptual framework?

a. It represented the end product of the FASB’s deliberations related to the conceptual

framework project.

b. The most important new issue brought up in the document was capital maintenance.

c. It brought up three views of financial accounting and financial statements.

d. It presented various definitions for basic accounting terms.

Which of the following is an assumption of fundamental analysis?

a. Securities markets are efficient.

b. Prices of securities rapidly reflect all publicly available information.

c. The strong form of the efficient-markets hypothesis is true.

d. Under-priced shares can be found in the securities market by means of financial

statement analysis.

_________ refers to the importance of an item to financial statement users in terms of

its relevance to decision making.

a. Comparability

b. Materiality

c. Consistency

d. Objectivity

Pre-SFAC No. 8, the three components of reliability are:

a. Predictive value, feedback value, timeliness.

b. Verifiability, neutrality, representational faithfulness.

c. Verifiability, predictive value, feedback value.

d. Relevance, comparability, materiality.

The treatment of loss contingencies required in SFAS No. 5 is an example of:

a. Elastic uniformity.

b. Conservatism.

c. Flexible uniformity.

d. Rigid uniformity.