1) In a leading securities law and CPA liabilities case, the U.S. Supreme Court ruled in

1976 in Hochfelder v. Ernst & Ernst that before CPAs could be held liable for Rule

10b-5 of the Securities Exchange Act of 1934, what would be required to be shown to

the court was the auditor’s:

A) ordinary negligence

B) gross negligence

C) knowledge and intent to deceive

D) financial gain at the expense of the plaintiff

2) The auditor is performing substantive tests of balances for accounts payable. What

documentation would provide the best evidence for the ending balance?

A) Vendor Invoices

B) Vendor Statements

C) Receiving reports

D) Purchase orders

3) A major consideration in verifying the ending balance in fixed assets is the

possibility of existing legal encumbrances. Tests to identify possible legal

encumbrances would satisfy the audit objective of:

A) existence

B) presentation and disclosure

C) detail tie-in

D) classification

4) The auditor’s best defense when material misstatements are not uncovered is to have

conducted the audit:

A) in accordance with generally accepted auditing standards

B) as effectively as reasonably possible

C) in a timely manner

D) only after an adequate investigation of the management team

5) Substantive tests of transactions focus on the changes in the beginning and ending of

the year balances, particularly for the balance sheet.

A) True

B) False

6) The purpose of stratification is to permit auditors to emphasize certain aspects of a

population and deemphasize others.

A) True

B) False

7) The auditor is examining the accounting entries made to the accumulated

depreciation account during the year and notices a significant amount of debits to the

account. Which of the following provides the most logical explanation?

A) Large number of asset retirements

B) Salvage values were revised downward

C) Useful lives were revised downward

D) Allocation of fixed overhead were revised

8) Which of the following results in a conclusion that represents positive assurance?

A) review

B) compilation

C) examination

D) agreed upon procedure engagement

9) Fraudulent financial reporting is most likely to be committed by whom?

A) line employees of the company

B) outside members of the company’s board of directors

C) company management

D) the company’s auditors

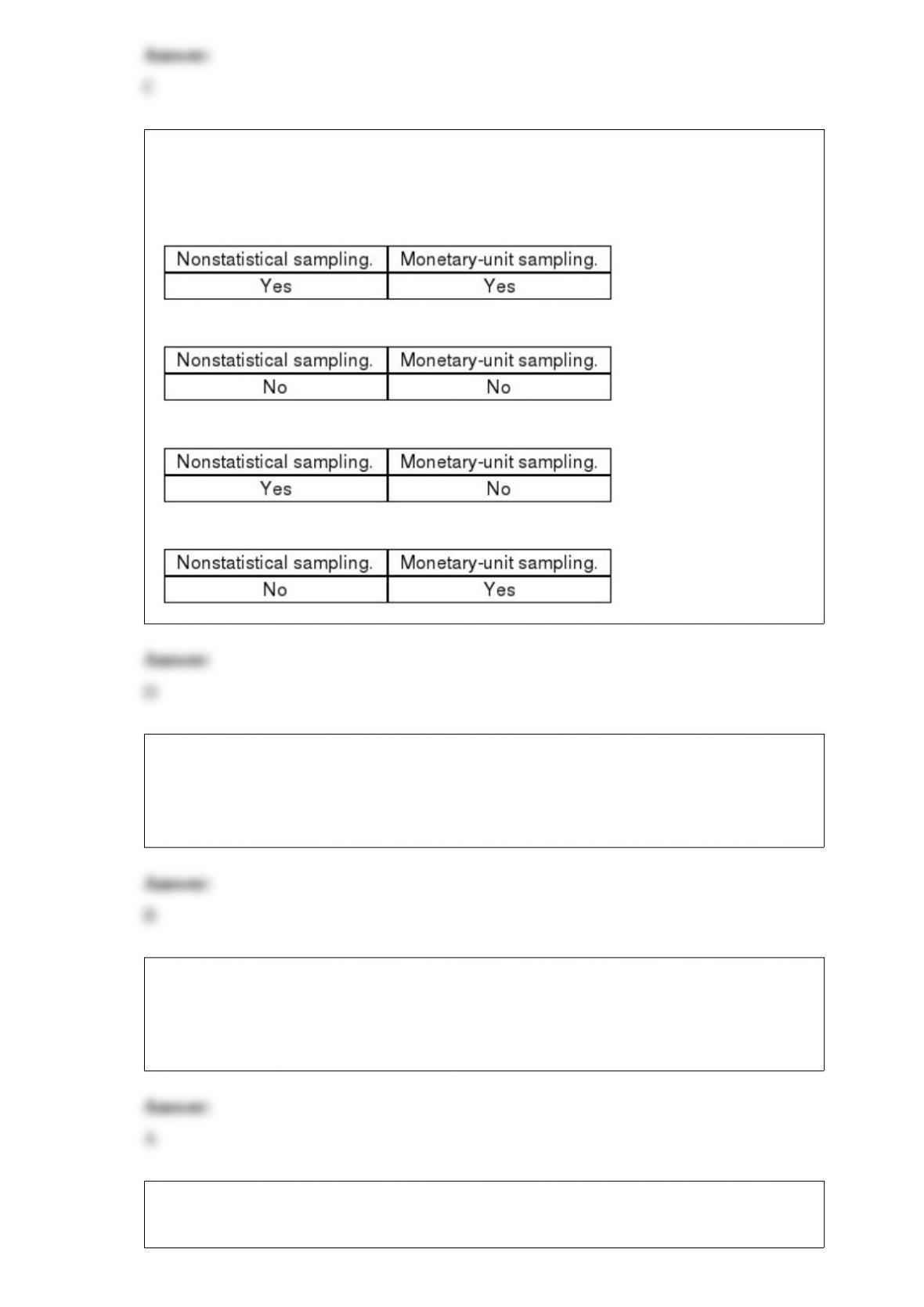

10) A principal advantage of statistical methods of attributes sampling over

nonstatistical methods is that they provide a scientific basis for establishing the:

A) risk of assessing control risk too low

B) tolerable exception rate

C) expected population exception rate

D) sample size

11) Ethical Rulings are:

I.Explanations relating to broad hypothetical circumstances.

II.Not enforceable, but one must justify departure.

III.Explanations relating to specific factual circumstances.

A) I and II

B) I and III

C) II and III

D) I, II, and III

12) When one material weakness is present at the end of the year, management of a

public company must conclude that internal control over financial reporting is:

A) insufficient

B) inadequate

C) ineffective

D) inefficient

13) Which of the following is a component of general controls?

A) processing controls

B) output controls

C) back-up and contingency planning

D) input controls

14) Preliminary judgments about materiality are often changed during the course of the

engagement.

A) True

B) False

15) Tests of controls provide evidence about the likelihood for misstatements in a

client’s financial statements.

A) True

B) False

16) In the

A) True

B) False

17) Parallel testing is used when old and new systems are operated simultaneously in all

locations.

A) True

B) False

18) Confirmations would almost always be used, assuming all the accounts below are

material, for:

A) individual transactions between organizations, such as sales transactions

B) bank balances and accounts receivable

C) fixed asset additions

D) payroll expenses

19) The risk the auditor is willing to take of accepting a balance as correct when the

true misstatement in the balance under audit is greater than the tolerable misstatement

is:

A) the upper bound

B) the tolerable risk

C) the acceptable risk of incorrect acceptance

D) the lower bound

20) The auditor must consider the possibility that the true population misstatement is

greater than the amount of misstatement that is tolerable when the auditor is

performing:

A)

B)

C)

D)

21) Statements on Auditing Standards (SASs) are issued by the Public Company

Accounting Oversight Board.

A) True

B) False

22) Items that materially affect the comparability of the financial statements generally

require disclosure in the footnotes.

A) True

B) False

23) Which audit tests involve physical examination and confirmation?

A) tests of controls

B) tests of transactions

C) tests of balances

D) analytical procedures

24) Which of the following types of audit tests is usually emphasized due to a lack of

independent third-party evidence related to payroll transactions?

A) Analytical procedures

B) Tests of details of balances

C) Tests of controls

D) Each of the above is emphasized

25) Which of the following would be a violation of the rule requiring “objectivity” by

the CPA?

I.The auditor accepts management’s opinion regarding the collection of accounts

receivable without an independent evaluation.

II.In preparing a client’s tax return, the CPA encourages a client to take a deduction

which the CPA believes is risky.

A) I only

B) II only

C) I and II

D) Neither I nor II

26) Insert risk and control risk are normally assessed for the each segment but sets audit

risk at the financial statement level.

A) True

B) False

27) For effective internal control purposes, the vouchers payable department generally

should:

A) obliterate the quantity ordered on the receiving department copy of the purchase

order

B) stamp, perforate, or otherwise cancel supporting documentation after payment is

mailed

C) establish the agreement of the vendor’s invoice with the receiving report and

purchase order

D) ascertain that each requisition is approved as to price, quantity, and quality by an

authorized employee

28) Before performing a review of a nonpublic entity’s financial statements, an

accountant should:

A) complete a series of inquiries concerning the entity’s procedures for recording,

classifying, and summarizing transactions

B) obtain a sufficient level of knowledge of the accounting principles and practices of

the industry in which the entity operates

C) inquire whether management has omitted substantially all of the disclosures required

by generally accepted accounting principles

D) apply analytical procedures to provide limited assurance that no material

modifications should be made to the financial statements

29) Client representation letters are required by professional auditing standards,

whereas management letters are optional.

A) True

B) False

30) Which of the following is not a SysTrust Services principle as defined by the

A) Online privacy

B) Availability

C) Processing integrity

D) Operational integrity

31) The audit procedure that provides the auditor with the most appropriate evidence

when performing test of details of balances for accounts receivable is:

A) confirmations

B) recalculation of the aged receivables and uncollectible accounts

C) tracing credit memos for returned merchandise to receiving room reports

D) tracing from shipping documents to journals to the accounts receivable ledger

32) Control risk may be reduced for a company with a complex IT system when

compared to a company that relies primarily on manual controls.

A) True

B) False

33) The use of statistical sampling is less common for the audit of accounts payable

than for accounts receivable because it is more difficult to define the population and

determine the population size in accounts payable.

A) True

B) False

34) The exception rate the auditor will permit in the population and still be willing to

reduce the assessed level of control risk is called the:

A) tolerable exception rate

B) estimated population exception rate

C) acceptable risk of overreliance

D) sample exception rate

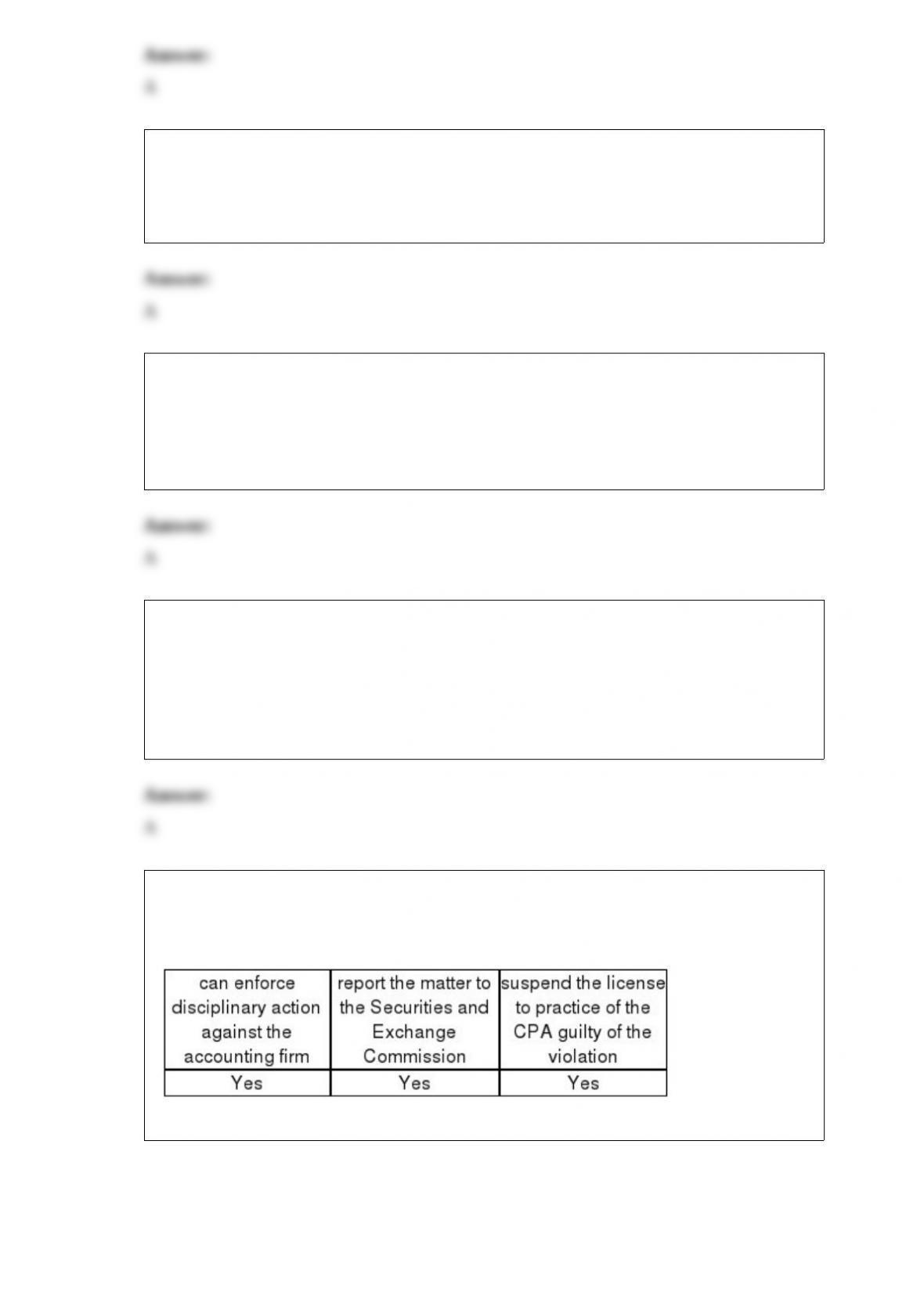

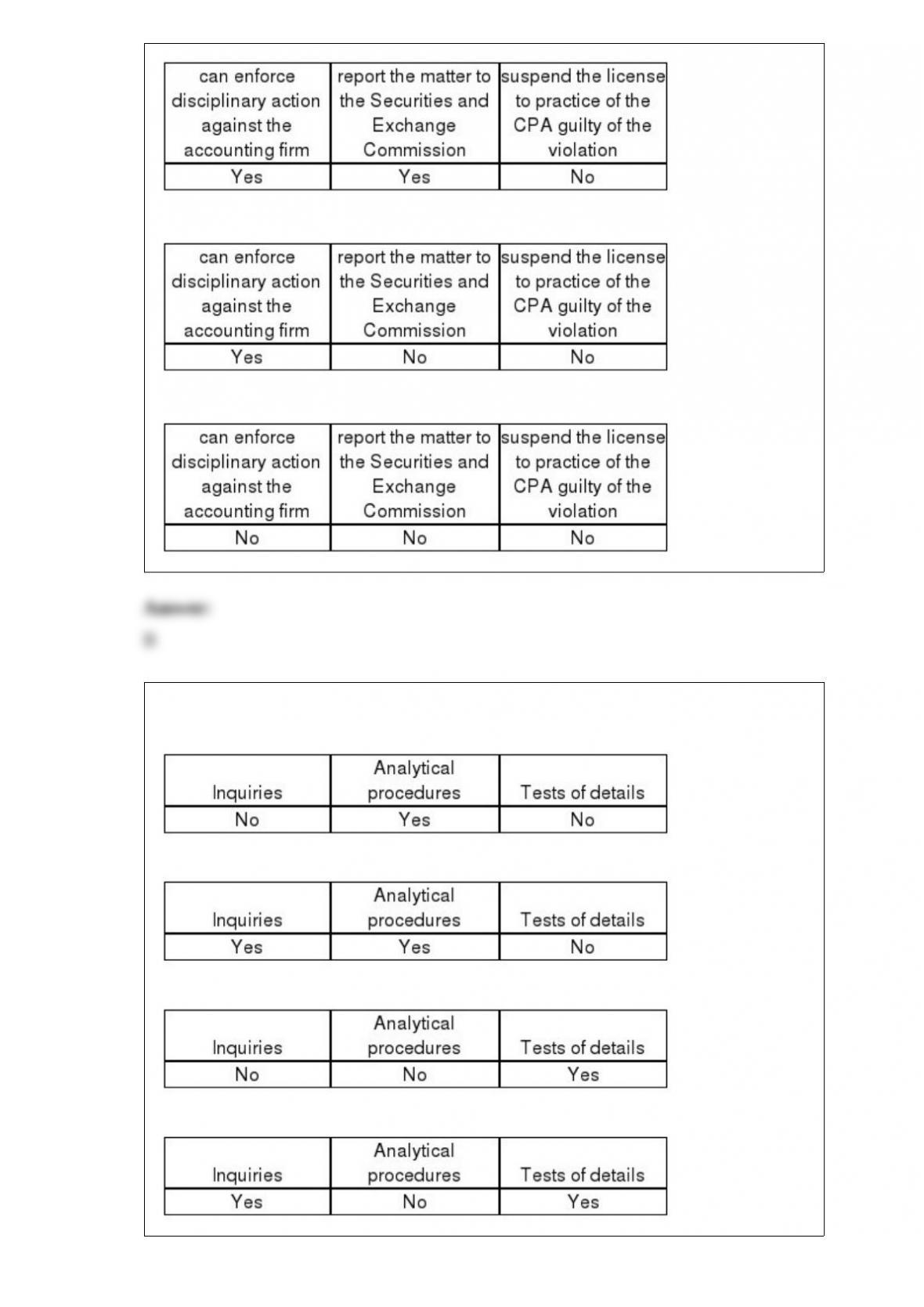

35) Assume the Public Company Accounting Oversight Board (PCAOB) identifies a

violation during its inspection of a registered accounting firm. The PCAOB:

A)

B)

C)

D)

36) Evidence for a review engagement consists primarily of:

A)

B)

C)

D)

37) Describe the methods used by the

38) Describe each of the major types of cash accounts maintained by business entities.

39) What are several similarities between internal and external auditors?

40) Describe each of the four types of sample selection methods commonly associated

with statistical audit sampling.

41) Discuss the relationship between quality control and generally accepted auditing

standards.

42) What is an engagement to attest on internal control over financial reporting?

43) Discuss the procedures involved in, and the purpose of, a surprise payroll payoff.