Accounting for the pledging of accounts receivable as collateral for a loan requires:

a. Reporting the receivables net of the borrowed amount.

b. Removal of the pledged receivables from current assets and including them with

noncurrent investments.

c. Disclosure of the arrangement in notes to the financial statements.

d. None of these answer choices are correct.

Gain contingencies usually are recognized in a company’s income statement when:

a. Realized.

b. The amount can be reasonably estimated.

c. The gain is reasonably possible and the amount can be reasonable estimated.

d. The gain is probable and the amount can be reasonably estimated.

Early in 2016, Benton Well Supplies discovered that a five-year insurance premium

payment of $50,000 at the beginning of 2013 was debited to insurance expense. The

correcting entry would include:

a. A credit to retained earnings of $20,000.

b. A debit to insurance expense of $20,000.

c. A debit to prepaid insurance of $30,000.

d. A debit to prepaid insurance of $50,000.

For the current year ($ in millions), Centipede Corp. had $80 in pretax accounting

income. This included warranty expense of $6 and $20 in depreciation expense. Two

million of warranty costs were incurred, and MACRS depreciation amounted to $35. In

the absence of other temporary or permanent differences, what was Centipede’s taxable

income?

a. $73 million.

b. $69 million.

c. $63 million.

d. $49 million.

Assume that at the beginning of the current year, a company has a net gain-AOCI of

$25,000,000. At the same time, assume the PBO and the plan assets are $200,000,000

and $150,000,000, respectively. The average remaining service period for the

employees expected to receive benefits is 10 years. What is the amount of amortization

to pension expense for the year?

a. $3,000,000.

b. $ 500,000.

c. $2,500,000.

d. $1,500,000.

During 2016, Deluxe Leather Goods sold 800,000 reversible belts under a new sales

promotional program. Each belt carried one coupon, which entitles the customer to a

$5.00 cash rebate. Deluxe estimates that 70% of the coupons will be redeemed, even

though only 350,000 coupons had been processed during 2016. At December 31, 2016,

Deluxe should report a liability for unredeemed rebates of:

a. $ 560,000.

b. $1,050,000.

c. $1,225,000.

d. $1,750,000.

If restricted stock is forfeited because an employee leaves the company, the appropriate

accounting procedure is to:

a. Reverse related entries previously made.

b. Do nothing.

c. Prepare correcting entries.

d. Record an income item.

Diversified Systems, Inc., reports consolidated financial statements this year in place of

statements of individual companies reported in previous years. This results in:

a. An accounting change that should be reported prospectively.

b. An accounting change that should be reported by restating the

financial statements of all prior periods presented.

c. A correction of an error.

d. Neither an accounting change nor a correction of an error.

Purchases equal the invoice amount:

a. Plus freight-in, plus discounts lost.

b. Less purchase returns, plus purchase allowances.

c. Plus freight-in, less purchase discounts.

d. Plus discounts, less purchase returns.

Which of the following would never require reporting deferred tax assets or deferred

tax liabilities?

a. Depreciation on equipment.

b. Accrual of warranty expense.

c. Life insurance premiums for the payer’s benefit.

d. Rent revenue received in advance.

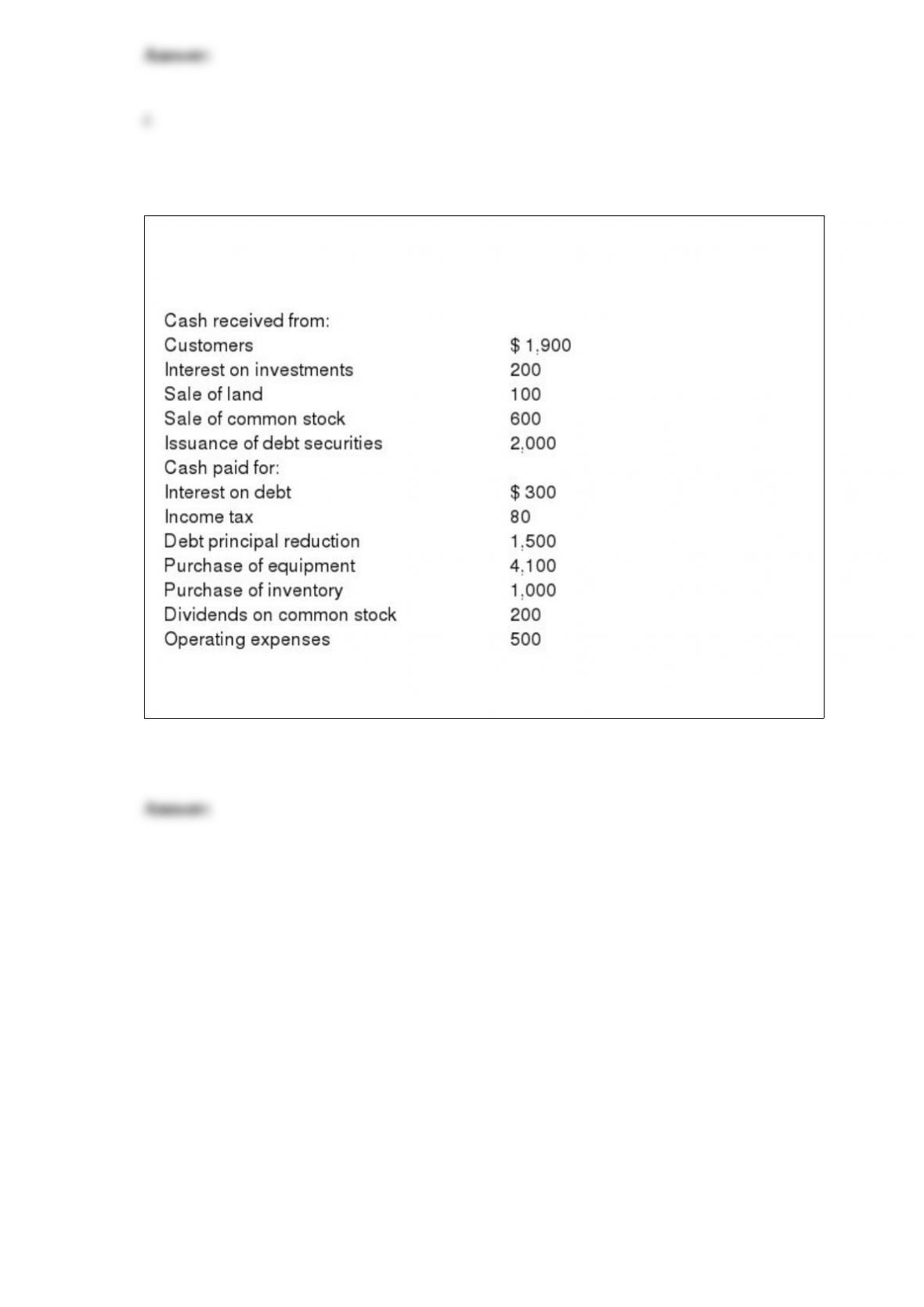

The following information is for Redwood Inc. for the year ended December 31, 2016.

Redwood had a cash and cash equivalents balance of $5,200 on January 1, 2016.

Required: Prepare a statement of cash flows for the year using the direct method for

operating activities.

On January 1, 2015, ECT Co. adopted the dollar-value LIFO method for its one

inventory pool. The pool’s value on this date was $600 million. The 2015 and 2016

ending inventory valued at year-end costs were $702 million and $840 million,

respectively. The appropriate cost indexes are 1.08 for 2015 and 1.20 for 2016.

Required:

Calculate the inventory balance that ECT Co. would report on its year-end balance

sheets for 2015 and 2016, using the dollar-value LIFO method.

Beaumont Company enters into a contract to provide a high quality diving-certification

preparation package, including goggles, snorkels, air tanks, fins, a wetsuit, and 5 private

lessons to get ready for diving certifications. The entire package sells for $2,500.

Other competing sellers in the same region charge an average of $250 for a set of

goggles and $750 for the lessons, if sold separately. Beaumont Company usually sells at

a 5% discount compared to other shops, since it is a bit farther away from the ocean.

Required: What would be Beaumont’s stand-alone selling price of the goggles and the

lessons, based on adjusted market assessment approach?

Walker Corporation exchanged land and $4,500 cash for material handling equipment.

The land had a book value of $45,000 and a fair value of $58,000. Assume the

exchange has commercial substance.

Required:

Prepare the journal entry to record the exchange.

Reacting to opposition to the FASB’s “Share-Based Payment” Exposure Draft, Senator

Carl Levin stated, “Stock options are the 800-pound gorilla that has yet to be caged by

corporate reform.” In reference to a bill that would thwart the FASB’s position, Senator

John McCain said, “This legislation blocking stock option expensing not only

undermines FASB’s independence, but undermines the effort to restore confidence in

our financial markets as well.” Discuss what these two senators meant by their

statements.

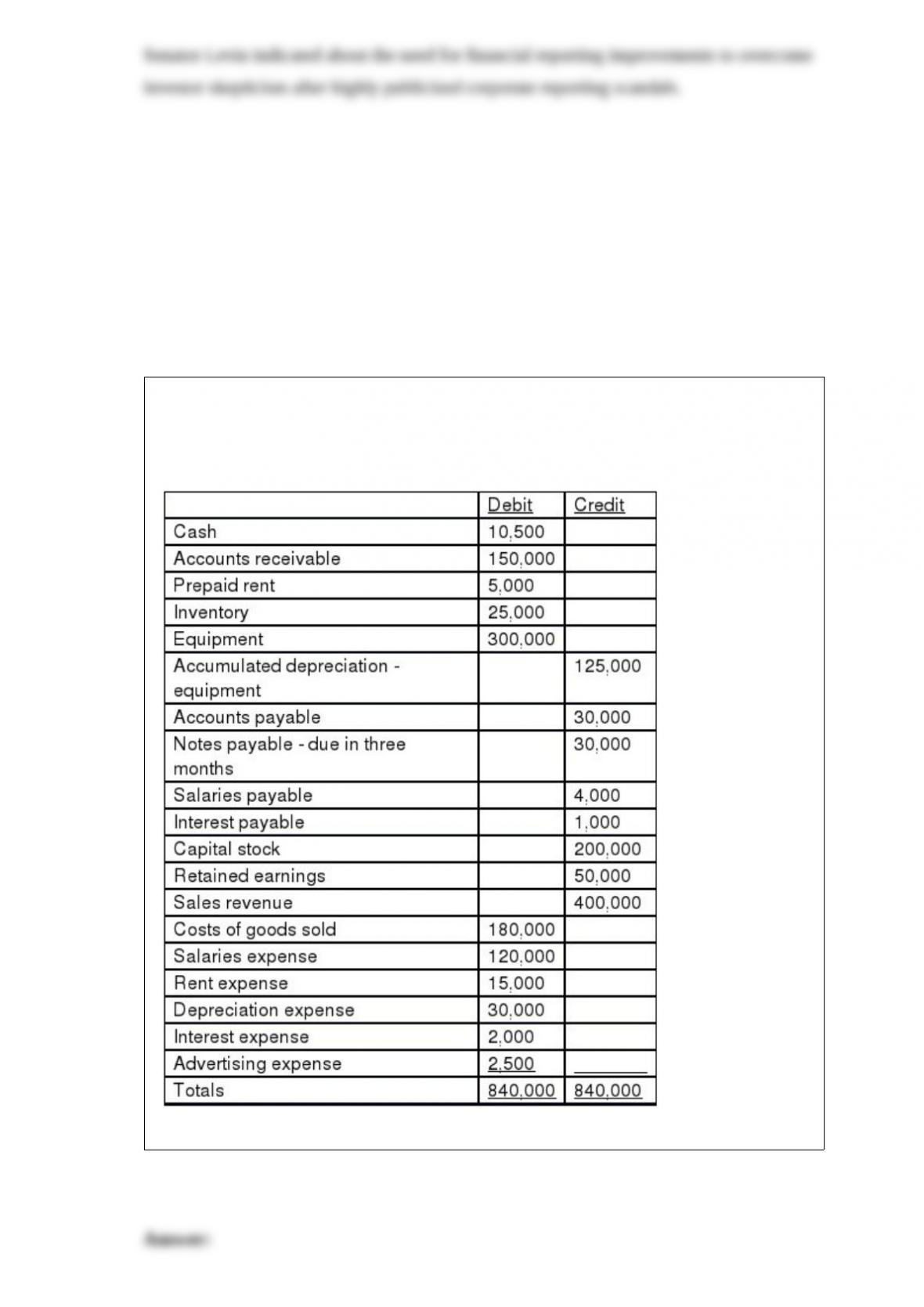

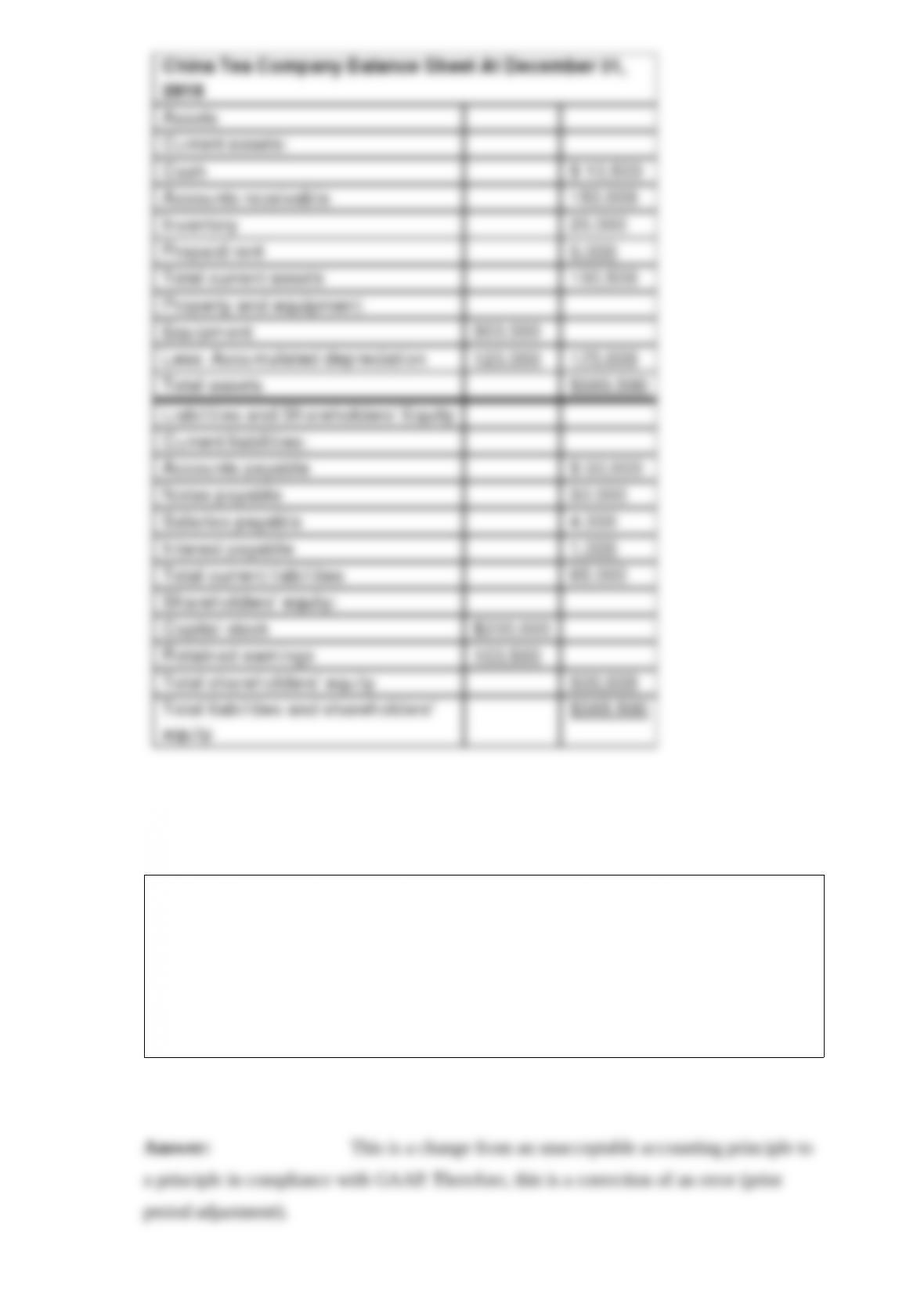

The adjusted trial balance for China Tea Company at December 31, 2016, is presented

below:

Prepare a classified balance sheet for China Tea Company as of December 31, 2016.

Nash Industries changed its method of accounting for warranties from the cash basis to

the accrual basis on January 1, 2016. The company’s accountant determined that a

liability of $70,000 should be established. Ignore income taxes.

Required:

Prepare the journal entry to record the accounting change.

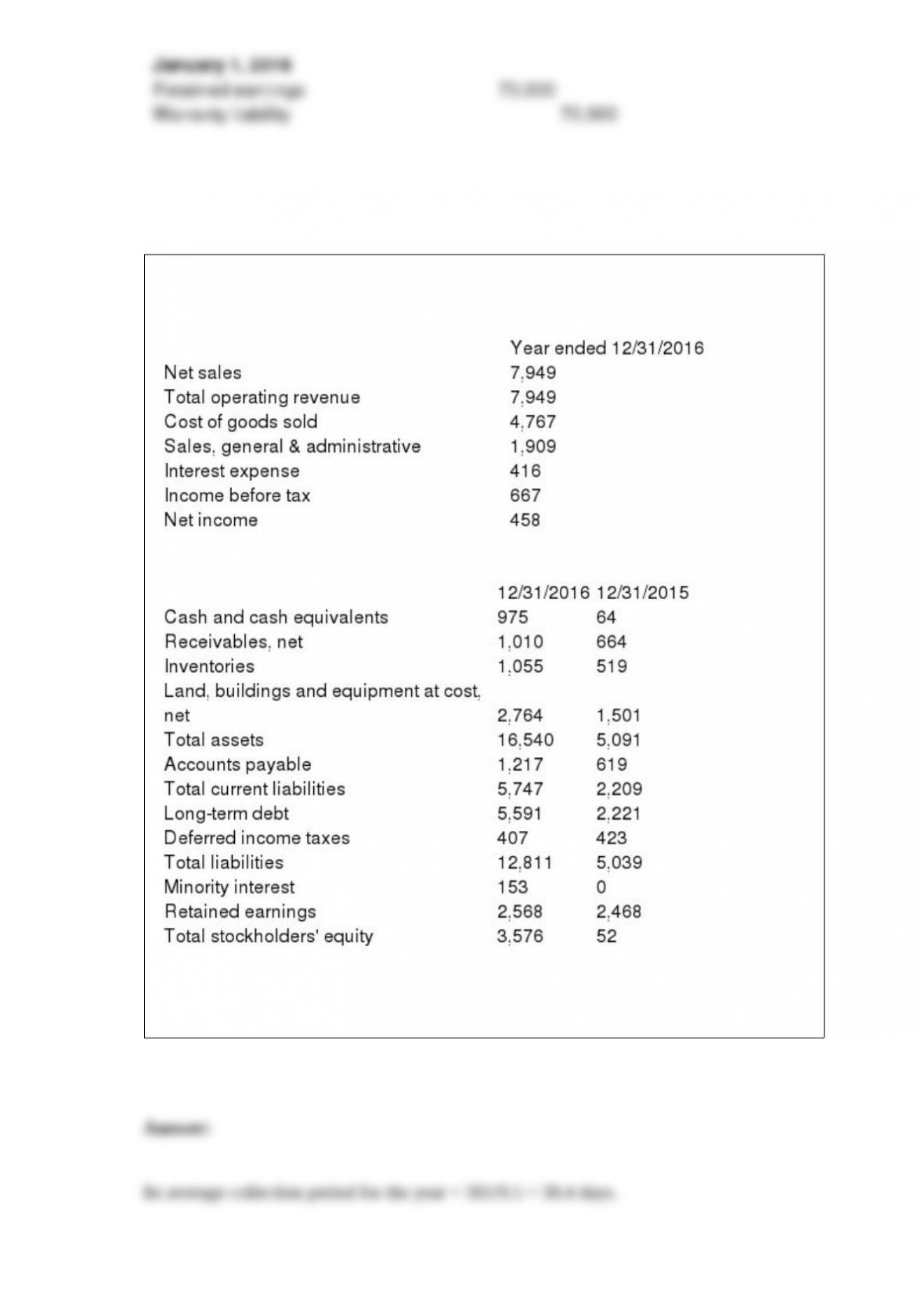

The following partial income statement and balance sheet information (in $ millions)

comes from the Annual Report of Saratoga Springs Co. for the year ending 12/31/2016:

Required: Compute the following amounts for Saratoga Springs Co.

Its average collection period for 2016. Round your final answer to one decimal place.

In its 2016 annual report to shareholders, the Goodday Chemical Company included the

following disclosure note excerpts on CONTINGENCIES in its annual report to

shareholders: At December 31, 2016, Goodday had recorded liabilities aggregating

$66.5 million for anticipated costs related to various environmental matters, primarily

the remediation of numerous waste disposal sites and certain properties sold by

Goodday. These costs include legal and consulting fees, site studies, the design and

implementation of remediation plans, post-remediation monitoring and related activities

and will be paid over several years. The amount of Goodday’s ultimate liability in

respect of these matters may be affected by several uncertainties, primarily the ultimate

cost of required remediation and the extent to which other responsible parties

contribute. At December 31, 2016, Goodday had recorded liabilities aggregating $218.7

million for potential product liability and other tort claims, including related legal fees

expected to be incurred, presently asserted against Goodday. The amount recorded was

determined on the basis of an assessment of potential liability using an analysis of

available information with respect to pending claims, historical experience, and, where

available, current trends. Goodday is a defendant in numerous lawsuits involving at

December 31, 2016, approximately 63,000 claimants alleging various asbestos-related

personal injuries purported to result from exposure to asbestos in certain rubber-coated

products manufactured by Goodday in the past or in certain Goodday facilities.

Typically, these lawsuits have been brought against multiple defendants in state and

federal courts. In the past, Goodday has disposed of approximately 22,000 cases by

defending and obtaining the dismissal thereof or by entering into a settlement. Goodday

has policies and coverage-in-place agreements with certain of its insurance carriers that

cover a substantial portion of estimated indemnity payments and legal fees in respect of

the pending claims. At December 31, 2016, Goodday has recorded an asset in the

amount it expects to collect under the policies and coverage-in-place agreements with

certain carriers related to its estimated asbestos liability. Goodday has also commenced

discussions with certain of its excess coverage insurance carriers to establish

arrangements in respect of their policies. Subject to the uncertainties referred to above,

Goodday has concluded that in respect of any of the above described liabilities, it is not

reasonably possible that it would incur a loss exceeding the amount recognized at

December 31, 2016, with respect thereto which would be material relative to the

consolidated financial position, results of operations, or liquidity of Goodday.

What is the point of the last paragraph of the Goodday disclosure? Explain in terms of

authoritative GAAP.

Briefly explain the differences between the terms depreciation, depletion, and

amortization.