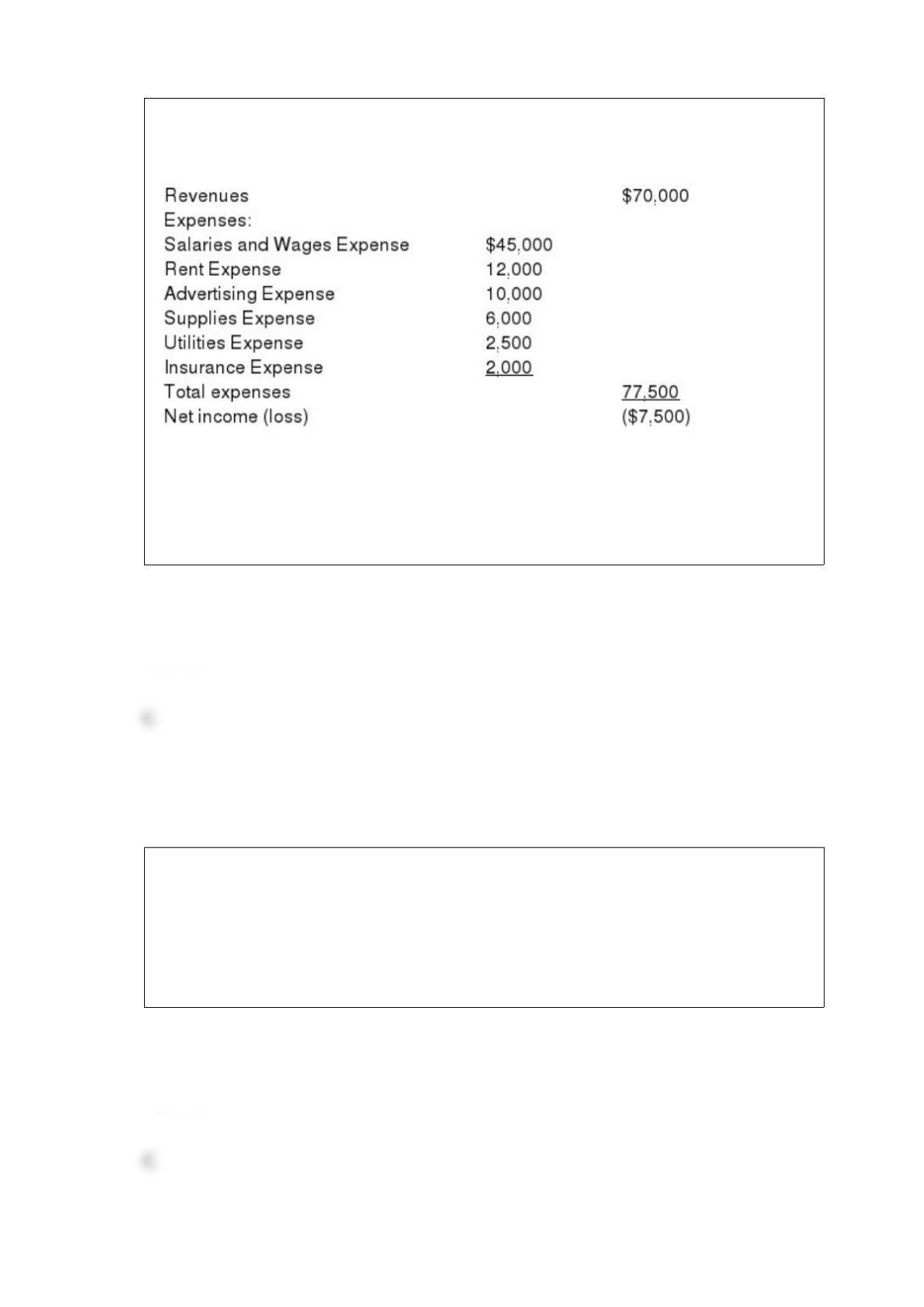

The income statement for the year 2015 of Fugazi Co. contains the following

information:

The entry to close the expense accounts includes a

a. debit to Income Summary for $7,500.

b. credit to Income Summary for $7,500.

c. debit to Income Summary for $77,500.

d. debit to Utilities Expense for $2,500.

Answer:

If a mining company extracts 1,500,000 tons in a period but only sells 1,200,000 tons,

a. total depletion on the mine is based on the 1,200,000 tons.

b. depletion expense is recognized on the 1,500,000 tons extracted.

c. depletion expense is recognized on the 1,200,000 tons extracted and sold.

d. a separate accumulated depletion account is set up to record depletion on the 300,000

tons extracted but not sold.

Answer:

A small company may be able to justify using a cash basis of accounting if they have

a. sales under $1,000,000.

b. no accountants on staff.

c. few receivables and payables.

d. all sales and purchases on account.

Answer:

Cash equivalents could include each of the following except

a. bank certificates of deposit.

b. money market funds.

c. petty cash.

d. U.S. Treasury bills.

Answer:

Megan’s Products is undecided about which base to use in estimating uncollectible

accounts. On December 31, 2015, the balance in Accounts Receivable was $680,000

and net credit sales amounted to $3,800,000 during 2015. An aging analysis of the

accounts receivable indicated that $40,000 in accounts are expected to be uncollectible.

Past experience has shown that about 1% of net credit sales eventually are

uncollectible.

Instructions

Prepare the adjusting entries to record estimated bad debt expense using the (1)

percentage-of-sales basis and (2) the percentage-of-receivables basis under each of the

following independent assumptions:

(a) Allowance for Doubtful Accounts has a credit balance of $3,200 before adjustment.

(b) Allowance for Doubtful Accounts has a debit balance of $730 before adjustment.

Answer:

The cash effects of transactions that create revenues and expenses are

a. financing activities.

b. investing activities.

c. operating activities.

d. processing activities.

Answer:

Assets normally show

a. credit balances.

b. debit balances.

c. debit and credit balances.

d. debit or credit balances.

Answer:

Hazel Company has just purchased equipment that requires annual payments of

$40,000 to be paid at the end of each of the next 4 years. The appropriate discount rate

is 15%. What is the present value of the payments?

a. $114,199

b. $160,000

c. $46,975

d. $150,135

Answer:

The use of special journals to record transactions

a. eliminates the need for a general ledger.

b. can save time in the posting process.

c. eliminates the need for a general journal.

d. should only be used if the volume of transactions is small.

Answer:

Liabilities

a. are future economic benefits.

b. are existing debts and obligations.

c. possess service potential.

d. are things of value used by the business in its operation.

Answer:

The following data is available for Blaine Corporation at December 31, 2015:

Common stock, par $10 (authorized 30,000 shares) $250,000

Treasury Stock (at cost $15 per share) 900

Based on the data, how many shares of common stock are outstanding?

a. 30,000

b. 25,000

c. 29,940

d. 24,940

Answer:

Employee payroll deductions include each of the following except

a. federal unemployment taxes.

b. federal income taxes.

c. FICA taxes.

d. insurance and pensions.

Answer:

Which one of the following would be classified as an extraordinary item?

a. Expropriation of property by a foreign government

b. Losses attributed to a labor strike

c. Write-down of inventories

d. Gains or losses from sales of equipment

Answer:

Which one of the following is usually performed only at the end of a company’s annual

accounting period?

a. Preparing financial statements

b. Journalizing and posting adjusting entries

c. Journalizing and posting closing entries

d. Preparing an adjusted trial balance

Answer:

Comparative balance sheets are usually prepared for

a. one year.

b. two years.

c. three years.

d. four years.

Answer:

Spa Company uses the direct method in determining net cash provided by operating

activities. The income statement shows income tax expense $85,000. Income taxes

payable were $35,000 at the beginning of the year and $20,000 at the end of the year.

Cash payments for income taxes are

a. $70,000.

b. $85,000.

c. $100,000.

d. $140,000.

Answer:

Which permits partial derecognition of receivables?

Answer:

Internal control over payroll is not necessary because employees will complain if they

do not receive the correct amount on their payroll checks.

Answer:

The maturity date of a 1-month note receivable dated June 30 is July 30.

Answer:

The Accumulated Depreciation account is a contra asset account that is reported on the

balance sheet.

Answer:

Amy Brown plans to buy a surround sound stereo system for $1,100 after 3 years. If the

interest rate is 6%, how much money should Amy set aside today for the purchase?

Answer:

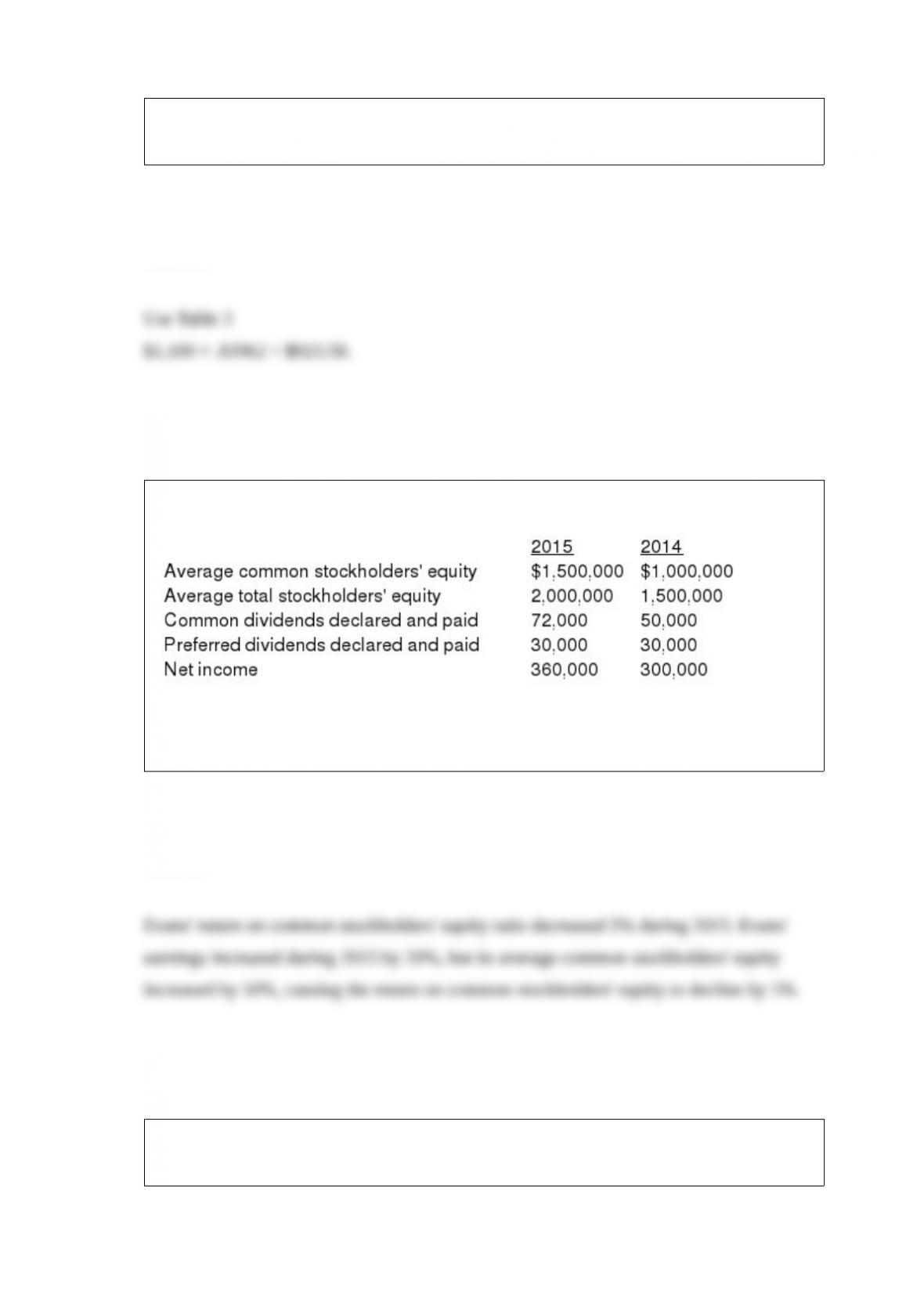

The following information is available for Evans Corporation:

Instructions

Compute the return on common stockholders’ equity ratio for both years. Briefly

comment on your findings.

Answer:

The time period assumption states that the economic life of a business entity can be

divided into artificial time periods.

Answer:

The mere recording of economic events is called ______________, and is just one part

of the _______________ process.

Answer:

Identify the internal control procedures applicable to cash disbursements followed by

Downey Company in each of the following cases.

1> Company checks are prenumbered.

2> Only the treasurer is authorized to sign checks.

3> All employees are required to take vacations.

4> Blank checks are stored in a locked safe.

5> The bookkeeper, not the treasurer, records cash disbursements.

Answer: