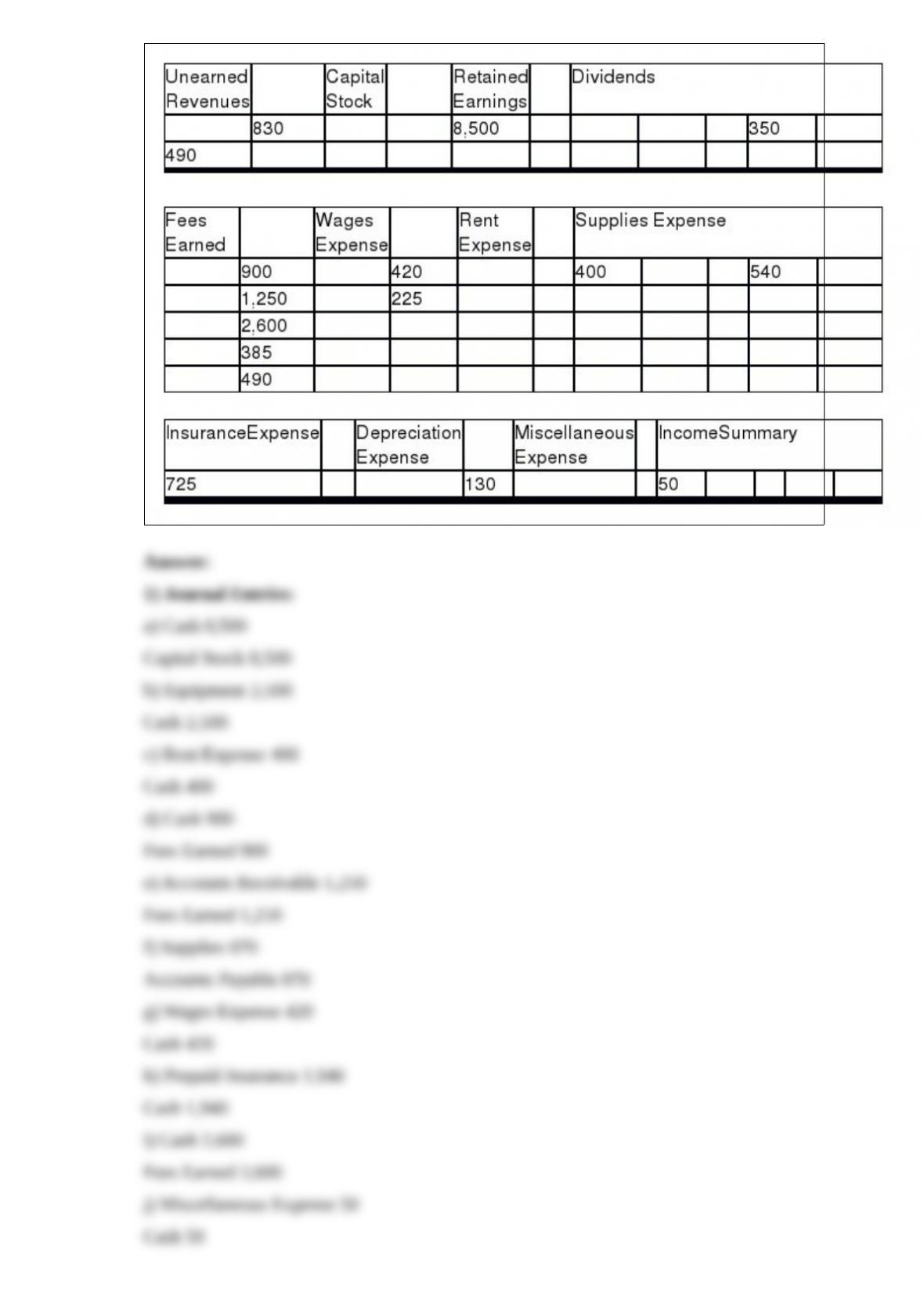

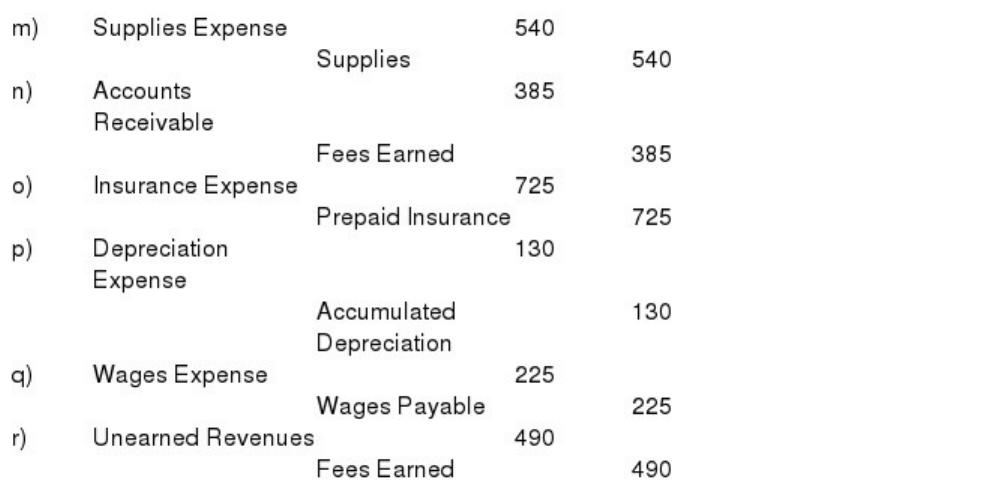

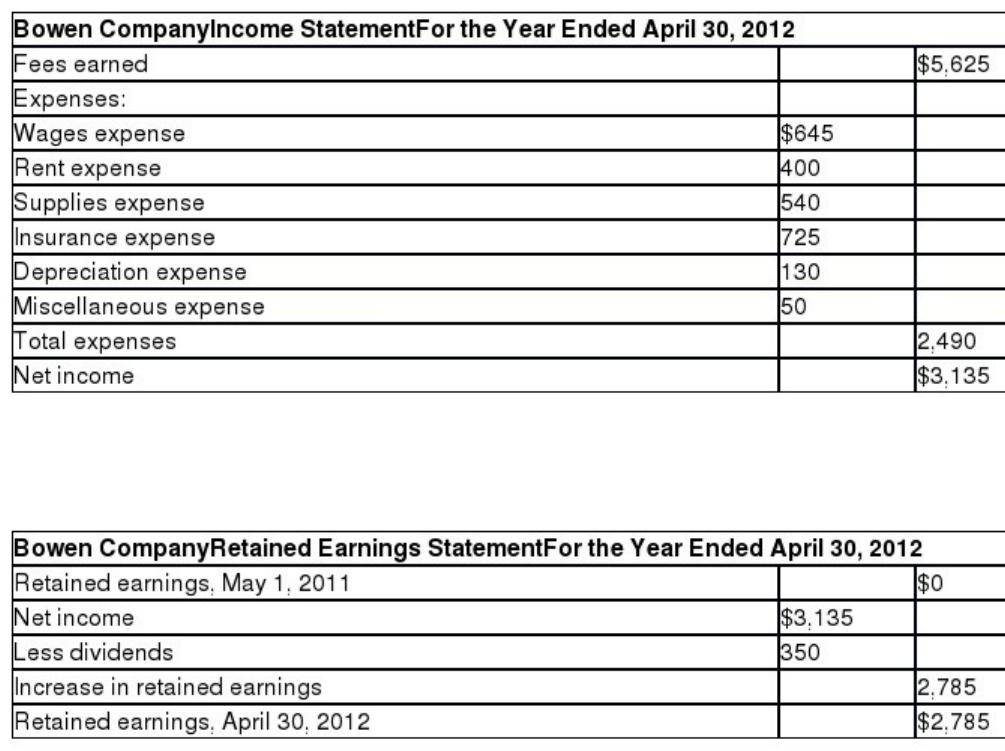

1) A manager in a cost center also has responsibility and authority over the revenues

and the costs.

2) When a business receives a bill from the utility company, no entry should be made

until the invoice is paid.

3) Once the adjusted trial balance is in balance, the flow of accounts will now go into

the financial statements.

4) A company can use comparisons of its financial data to the data of other companies

and industry values to evaluate its position.

5) When a corporation issues bonds, it executes a contract with the bondholders, known

as a bond debenture.

6) When a clerk enters a sale and the customer can see the amount displayed and is

given a cash receipt, this is an example of a preventive control.

7) If the debit portion of an adjusting entry is to an asset account, then the credit portion

must be to a liability account.

8) In applying the first-in, first-out method of costing inventories, if 8,000 units which

are 30% completed are in process at June 1, 28,000 units are completed during June,

and 4,000 units were 80% completed at June 30, the number of equivalent units of

production for June was 28,600.

9) Planning is the process of developing the companys objectives or goals and

translating these objectives into courses of action.

10) The accounting equation can be expressed as Assets – Liabilities = Stockholders

Equity.

11) The costs of initially producing an intermediate product should be considered in

deciding whether to further process a product, even though the costs will not change,

regardless of the decision.

12) An installment note is a debt that requires the borrower to make equal periodic

payments to the lender for the term of the note.

13) A company realizes that the last two day’s revenue for the month was billed but not

recorded. The adjusting entry on December 31 is debit Accounts Receivable and credit

Fees Earned.

14) The service department will determine its service department charge rate and charge

the companys divisions or departments according to their use of that particular service

department.

15) Which type of accountant typically practices as an individual or as a member of a

public accounting firm?

A.Certified Public Accountant

B.Certified Payroll Professional

C.Certified Internal Auditor

D.Certified Management Accountant

16) Which of the following are features of the just-in-time manufacturing system?

(a) maintaining excess inventory to ensure that products will always be available

(b) cross training of employees

(c) giving employees additional authority and responsibility

(d) product oriented layout

(e) increased set-up time

17) A company with $70,000 in current assets and $50,000 in current liabilities pays a

$1,000 current liability. As a result of this transaction, the current ratio and working

capital will

A.both decrease

B.both increase

C.increase and remain the same, respectively

D.remain the same and decrease, respectively

18) An employee of Morgan Corporation has found some partially completed units of

Model X in a dusty corner of the warehouse. A job ticket attached to the units indicates

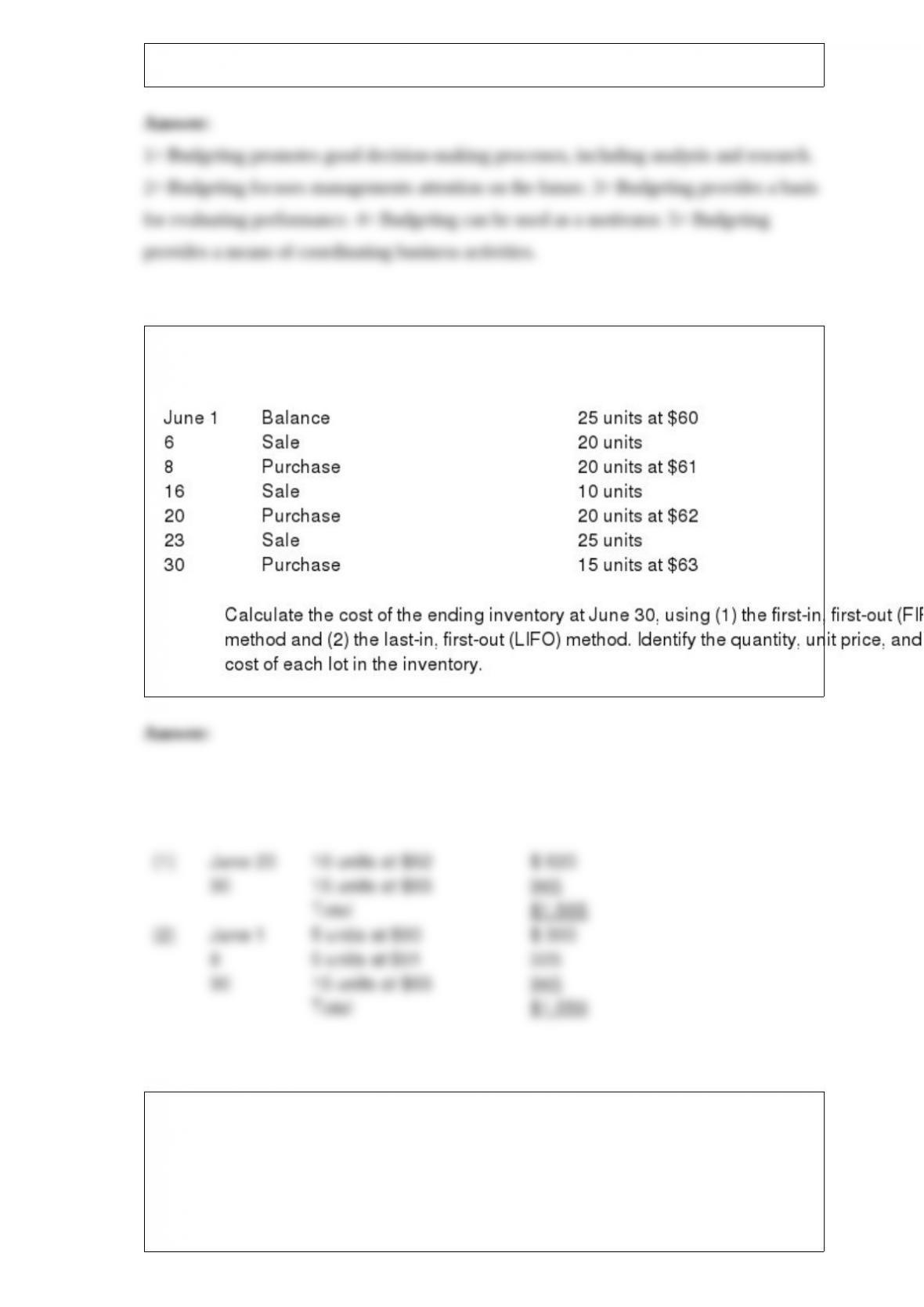

that a total of $750 in manufacturing costs have been used to bring the materials to this

point in the manufacturing process. The units can be sold in their current condition for

$275 to a scrap metal dealer. If Morgan spends $250 to complete the units, they could

be sold for $600.

Required: A. What should Morgan do? Why?

B. Identify the sunk cost, if any.

19) The budgeted finished goods inventory and cost of goods sold for a manufacturing

company for the year 2012 are as follows: January 1 finished goods, $765,000;

December 31 finished goods, $640,000; cost of goods sold for the year, $2,560,000.

The budgeted costs of goods manufactured for the year is?

A.$1,405,000

B.$2,560,000

C.$2,435,000

D.$3,965,000

20) A responsibility center in which the department manager is responsible for costs,

revenues, and assets for a department is called:

A.a cost center

B.a profit center

C.an operating center

D.an investment center

21) Which of the following would not normally operate as a service business?

A.pet groomer

B.supermarket

C.lawn care company

D.styling salon

22) In a job order cost accounting system, the entry to record the flow of direct

materials into production is:

A.debit Work in Process, credit Materials

B.debit Materials, credit Work in Process

C.debit Factory Overhead, credit Materials

D.debit Work in Process, credit Supplies

23) For accounting purposes, the method used to account for investments in common

stock is determined by

A.the amount paid for the stock by the investor

B.whether the acquisition of the stock by the investor was “friendly” or “hostile.”

C.the extent of an investor’s influence over the operating and financial affairs of the

investee

D.whether the stock has paid dividends in past years

24) On the statement of cash flows prepared by the indirect method, the cash flows

from operating activities section would include

A.receipts from the sale of investments

B.amortization of premium on bonds payable

C.payments for cash dividends

D.receipts from the issuance of capital stock

25) The interest rate specified in the bond indenture is called the

A.discount rate

B.contract rate

C.market rate

D.effective rate

26) Which of the following is not a right possessed by common stockholders of a

corporation?

A.the right to vote in the election of the board of directors

B.the right to receive a minimum amount of dividends

C.the right to sell their stock to anyone they choose

D.the right to share in assets upon liquidation

27) Rent expense on a factory building would be treated as a(n):

A.period cost

B.product cost

C.direct cost

D.both A and C are correct

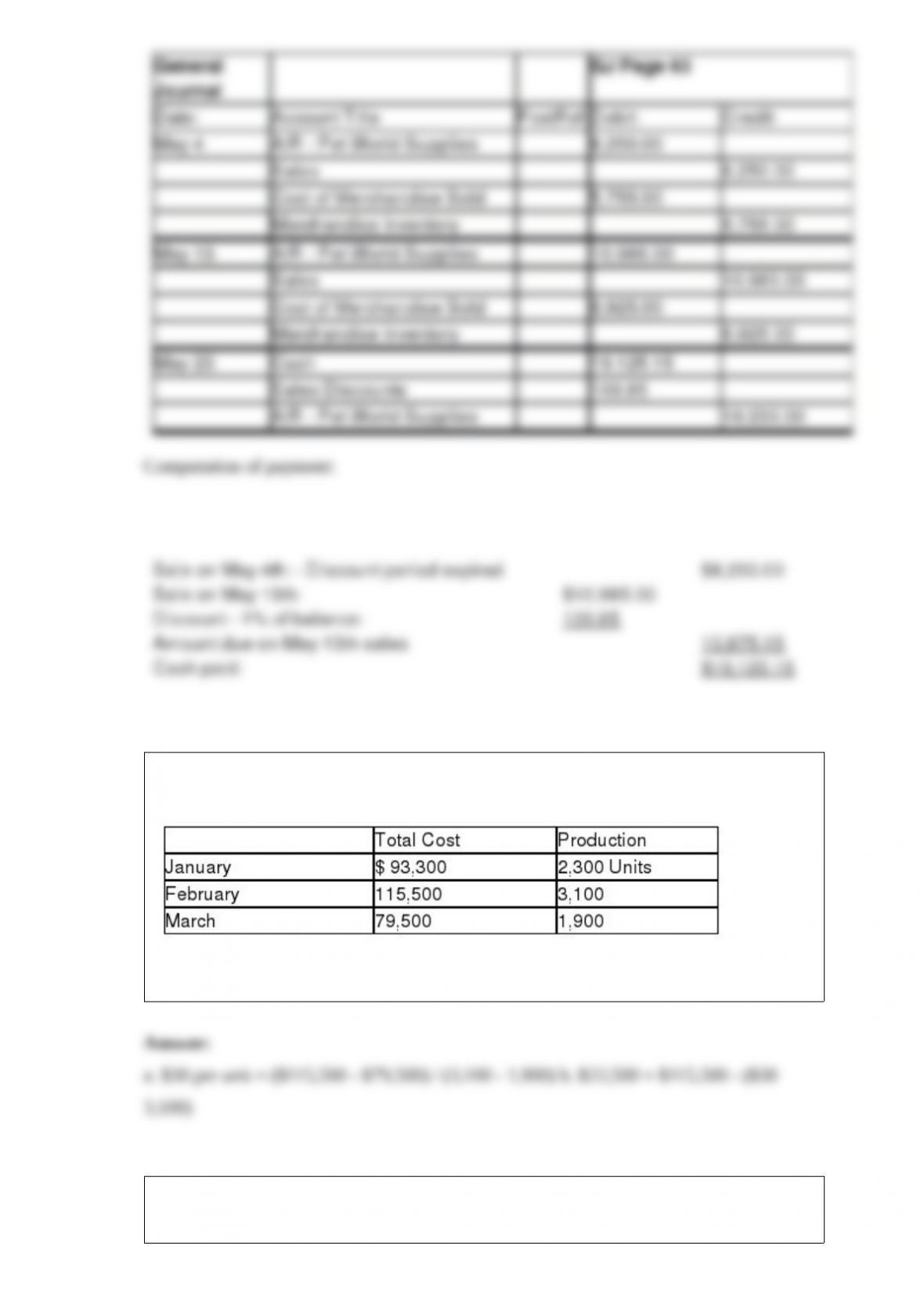

28) Bargain Wholesalers sells pet supplies to retailers including Pet World Supplies.

Bargain Wholesalers uses perpetual inventory. Use a General Journal to journalize the

following three transactions during the month of May:

(a) On May 4th, Bargain Wholesalers sells inventory to Pet World Supplies for

$8,250.00 with terms 1/10, n/30. The cost of the merchandise is $5,755.00.

(b) On May 13th, Bargain Wholesalers sells an additional $10,985 in inventory to Pet

World Supplies with terms 1/10, n/30. The cost of the merchandise is $6,925.00.

(c) On May 23rd, Bargain Wholesalers receives a check from Pet World Supplies

paying the balance due.

29) The manufacturing cost of Carrie Industries for the first three months of the year are

provided below:

Using the high-low method, determine the (a) variable cost per unit, and (b) the total

fixed cost.

30) As time passes, fixed assets other than land lose their capacity to provide useful

services. To account for this decrease in usefulness, the cost of fixed assets is

systematically allocated to expense through a process called

A.equipment allocation

B.depreciation

C.accumulation

D.matching

31) If variable selling and administrative expenses totaled $120,000 for the year

(80,000 units at $1.50 each) and the planned variable selling and administrative

expenses totaled $136,500 (78,000 units at $1.75 each), the effect of the unit cost factor

on the change in variable selling and administrative expenses is:

A.$19,500 decrease

B.$19,500 increase

C.$20,000 decrease

D.$20,000 increase

32) Which of the following entries records the collection of cash from cash customers?

A.Fees Earned, debit; Cash, credit

B.Fees Earned, debit; Accounts Receivable, credit

C.Cash, debit; Fees Earned, credit

D.Accounts Receivable, debit; Fees Earned, credit

33) Complete the missing items in the following chart:

Prepaid Expenses

Examples Adjusting Entry Financial Statement Impact if Adjusting Entry is

Omitted

Supplies,(a) Dr. Expense Cr. Asset Income Statement: Revenues: No effect Expenses:

Understated Net income: (b)Balance Sheet: Assets: (c) Liabilities: (d) Stockholders

equity: Overstated

Unearned Revenues

Examples Adjusting Entry Financial Statement Impact if Adjusting Entry is

Omitted

Unearned rent,(e) (f) Income Statement: Revenues: (g) Expenses: No effect Net

income: (h)Balance Sheet: Assets: (i) Liabilities: Overstated Stockholders equity: (j)

Accrued Revenues

Examples Adjusting Entry Financial Statement Impact if Adjusting Entry is

Omitted

Interest income due on a note,(k) Dr. Asset Cr. Revenue Income Statement: Revenues:

(l) Expenses: (m) Net income: UnderstatedBalance Sheet: Assets: (n) Liabilities: (o)

Stockholders equity: Understated

Accrued Expenses

Examples Adjusting Entry Financial Statement Impact if Adjusting Entry is

Omitted

Interest due on a notes payable, (p) (q) Income Statement: Revenues: No effect

Expenses: (r) Net income: (s)Balance Sheet: Assets: (t) Liabilities: Understated

Stockholders equity: (u)

34) Which of the following describes the classification and normal balance of the fees

earned account?

A.an asset with a credit balance

B.a liability with a credit balance

C.an expense with a debit balance

D.a revenue with a credit balance

35) The Cunningham Factory has determined that its budgeted factory overhead budget

for the year is $6,750,000 and budgeted direct labor hours are 5,000,000. If the actual

direct labors for the period are 175,000 how much overhead would be allocated to the

period?

A.$675,000

B.$129,630

C.$236,250

D.$175,000

36) Determine the activity-based cost for each tape drive unit.

A.$97.73

B.$232.69

C.$394.12

D.$103.84

37) Which of the following is not a short-cut in finding errors on the trial balance?

A.Determine the difference between debits and credits and look for the amount

B.Determine the amount and change any account to make the trial balance correct

C.Determine the difference between debits and credits, divide the amount by 2, look for

the amount

D.Determine the difference between debits and credits, divide the amount by 9, if it

divides evenly, look for a transposition or slide error

38) Identify the following as a Fixed Asset (FA), or Intangible Asset (IA), or Natural

Resource (NR), or Neither (N)

(a) computer

(b) patent

(c) oil reserve

(d) goodwill

(e) U. S. Treasury note

(f) land used for employee parking

(g) gold mine

39) In a lease contract, the party who legally owns the asset is the

A.lessee

B.lessor

C.operator

D.banker

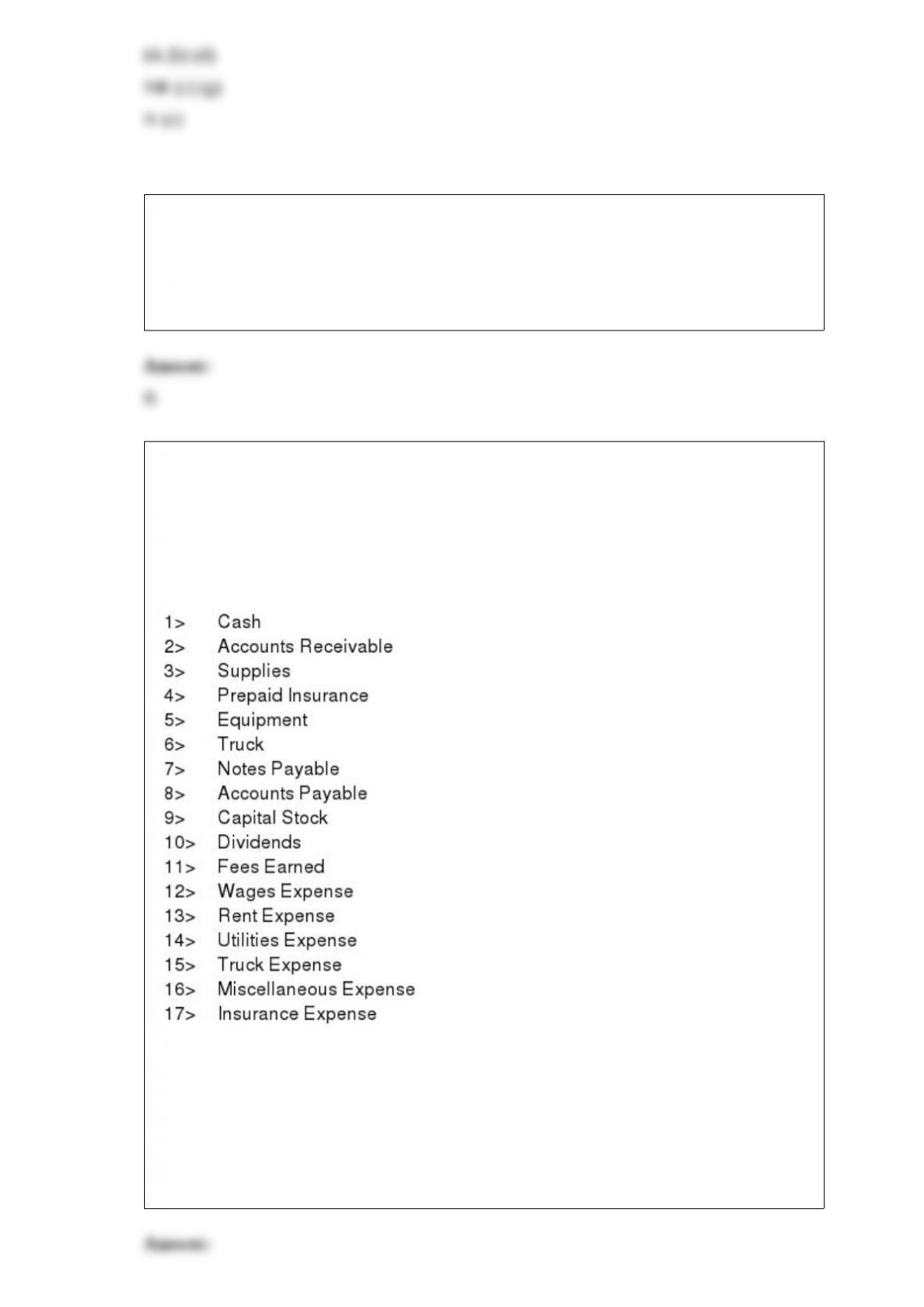

40) On January 1, 2011, Cary Parsons established Carys Catering Service. Listed below

are accounts to use for transactions (a) through (e), each identified by a number.

Following this list are the transactions that occurred during the first month of

operations. You are to indicate for each transaction the accounts that should be debited

and credited by placing the account number(s) in the appropriate box.

Transactions Account(s) Debited Account(s) Credited

a. Purchased supplies for cash.

b. Paid the annual premiums on property and casualty insurance.

c. Received cash for a job previously recorded on account.

d. Paid a creditor a portion of the amount owed for equipment previously purchased on

account.

e. Received cash for a completed job.

41) The production budgets are used to prepare which of the following budgets.

A.Operating expenses

B.Direct materials purchases, direct labor cost, factory overhead cost

C.Sales in dollars

D.Sales in units

42) If sales are $400,000, variable costs are 75% of sales, and operating income is

$50,000, what is the operating leverage?

A.2.5

B.7.5

C.2.0

D.0

43) Which of the following groups of accounts have a normal debit balance?

A.revenues, liabilities

B.assets, liabilities

C.liabilities, expenses

D.assets, expenses

44) After net income is entered on the work sheet, the Balance Sheet Debit and Credit

columns must

A.be the same amount as the total amount of the Income Statement Debit and Credit

columns

B.equal each other

C.be the same amount as the total amount in the Adjusted Trial Balance Debit and

Credit columns

D.not be equal to each other and need not be the same total amounts as any other pair of

columns on the work sheet

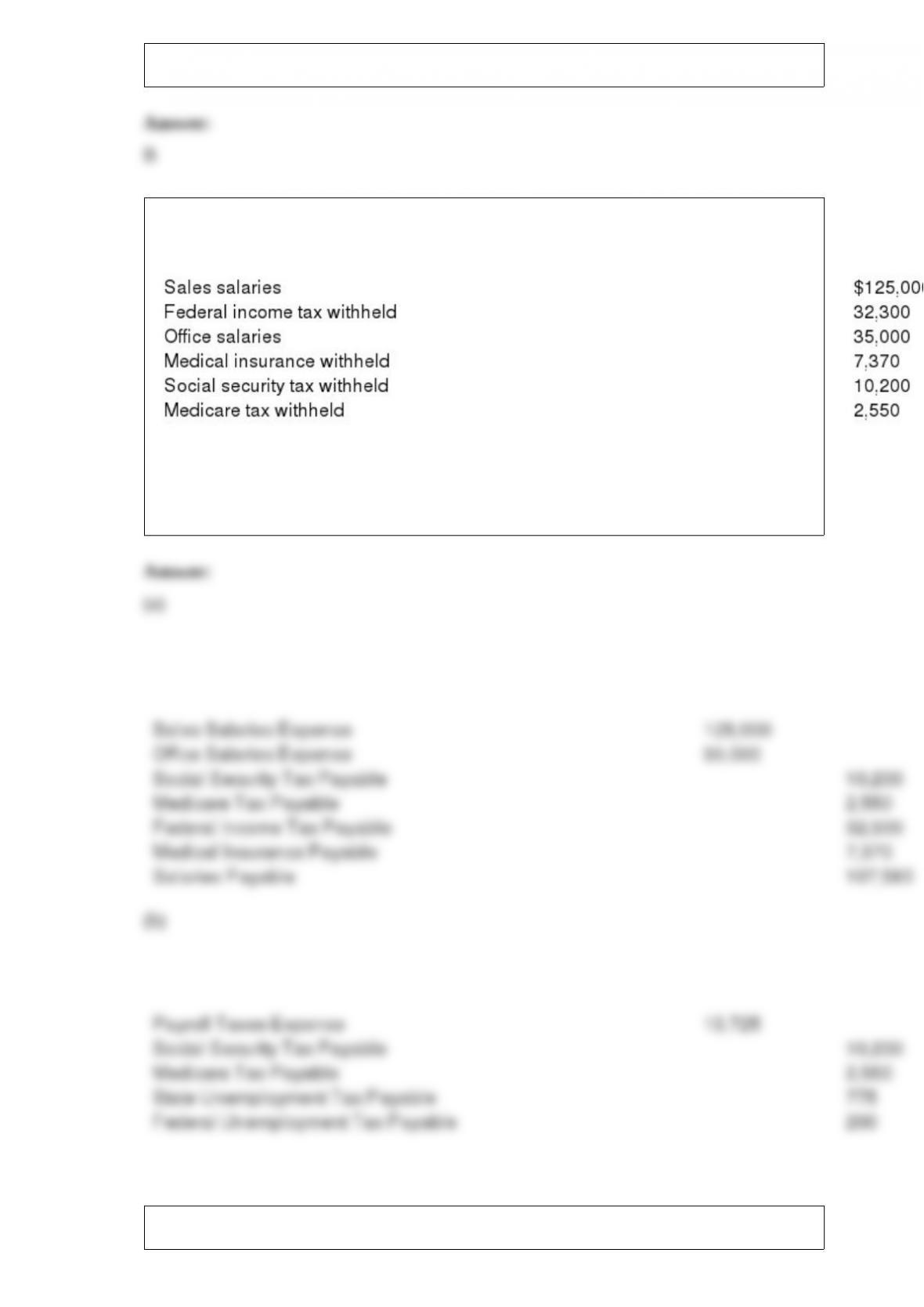

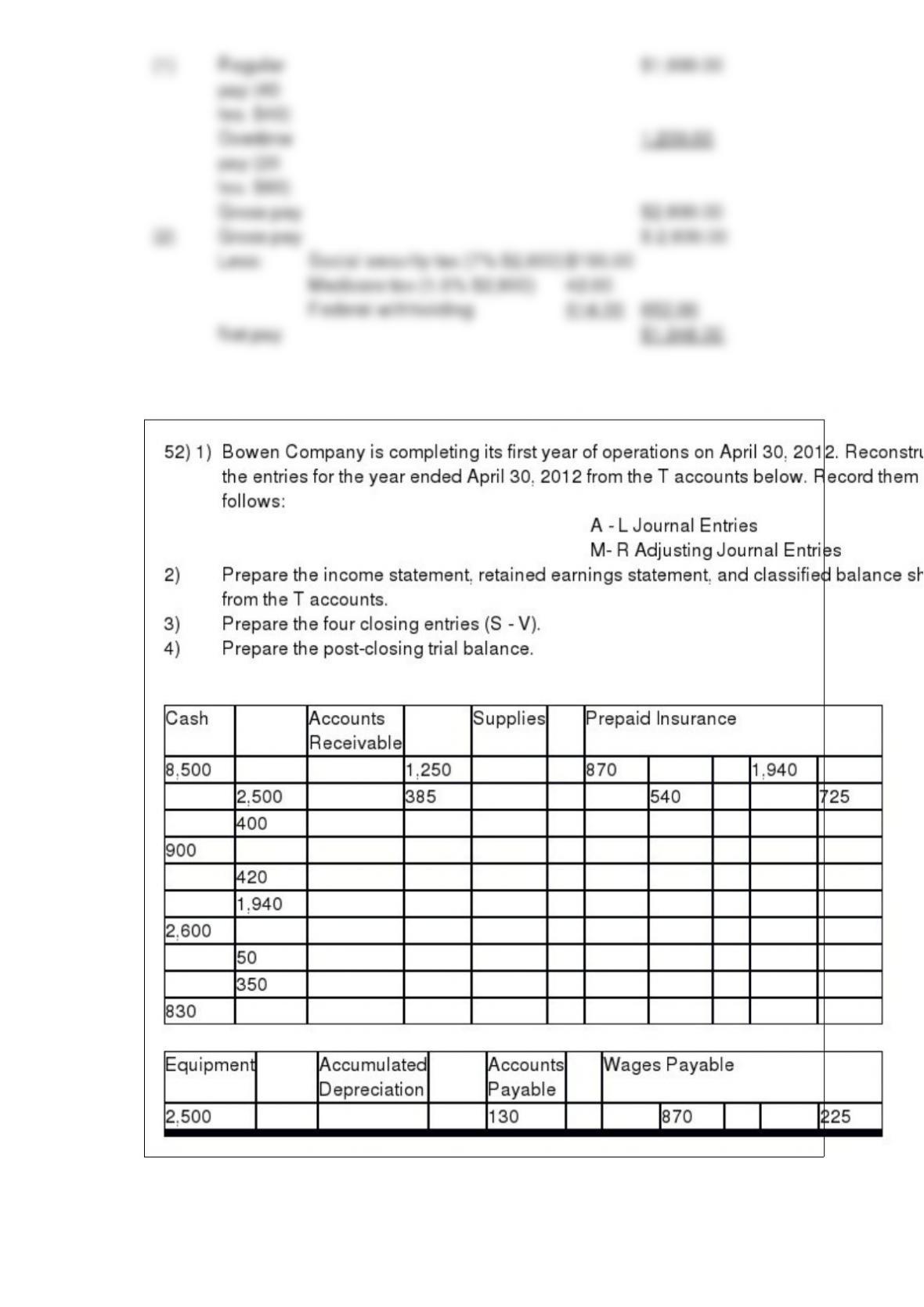

45) The summary of the payroll for the monthly pay period ending July 15 indicated the

following:

Journalize the entries to record (a) the payroll and (b) the employer’s payroll tax

expense for the month. The state unemployment tax rate is 3.1%, and the federal

unemployment tax rate is 0.8%. Only $25,000 of salaries are subject to unemployment

taxes.

46) Mocha Company manufactures a single product by a continuous process, involving

three production departments. The records indicate that direct materials, direct labor,

and applied factory overhead for Department 1 were $100,000, $125,000, and

$150,000, respectively. The records further indicate that direct materials, direct labor,

and applied factory overhead for Department 2 were $55,000, $65,000, and $80,000,

respectively. In addition, work in process at the beginning of the period for Department

1 totaled $75,000, and work in process at the end of the period totaled $60,000.

The journal entry to record the flow of costs into Department 2 during the period for

applied overhead is:

A.Factory Overhead–Department 280,000

Work in Process–Department 280,000

B.Work in Process–Department 2230,000

Factory Overhead–Department 2230,000

C.Work in Process–Department 280,000

Factory Overhead–Department 280,000

D.Work in Process–Department 2150,000

Factory Overhead–Department 2150,000

47) A voucher is usually supported by

A.a supplier’s invoice

B.a purchase order

C.a receiving report

D.all of the above

48) On October 1, Black Company receives a 9% interest bearing note from Reese

Company to settle a $20,000 account receivable. The note is due in six months. At

December 31, Black should record interest revenue of

A.$0

B.$450

C.$900

D.$1,800

49) If variable cost of goods sold totaled $80,000 for the year (16,000 units at $5.00

each) and the planned variable cost of goods sold totaled $86,250 (15,000 units at $5.75

each), the effect of the quantity factor on the change in variable cost of goods sold is:

A.$5,000 decrease

B.$5,000 increase

C.$5750 increase

D.$5,750 decrease

50) Perfect Stampers makes and sells aftermarket hub caps. The variable cost for each

hub cap is $4.75 and the hub cap sells for $9.95. Perfect Stampers has fixed costs per

month of $3,120. Compute the contribution margin per unit and break-even sales in

units and in dollars for the month.

51) An employee earns $40 per hour and 1.5 times that rate for all hours in excess of 40

hours per week. Assume that the employee worked 60 hours during the week, and that

the gross pay prior to the current week totaled $58,000. Assume further that the social

security tax rate was 7.0% (on earnings up to $100,000), the Medicare tax rate was

1.5%, and the federal income tax to be withheld was $614.

Required:

(1) Determine the gross pay for the week.

(2) Determine the net pay for the week.

53) Describe at least five benefits of budgeting.

54) The following data regarding purchases and sales of a commodity were taken from

the related perpetual inventory account:

55) On April 10, Maranda Corporation issued for cash 11,000 shares of no-par common

stock at $25. On May 5, Maranda issued at par 1,000 shares of 4%, $50 par preferred

stock for cash. On May 25, Maranda issued for cash 15,000 shares of 4%, $50 par

preferred stock at $55.

Journalize the entries to record the April 10, May 5, and May 25 transactions.