The FASB”s due process invites various interested parties to indicate their opinions

about whether financial accounting standards should be changed.

Some liabilities are not contractual obligations and may not be payable in cash.

Most changes in accounting principle require a disclosure justifying the change in the

first set of financial statements that the change is made.

Under IFRS No. 9, debt investments are classified as either “amortized cost,” or “fair

value through profit and loss (FVPL),” or “fair value through other comprehensive

income (FVOCI).”

For a loss contingency to be accrued, the claim must have been made before the

accounting period ended.

A company’s market value is generally less than its book value.

A payment on account has no effect on working capital but will increase the current

ratio if it is already greater than 1.0.

Companies recognize revenue when goods or services are transferred to customers for

the amount the company expects to be entitled to receive in exchange for those goods or

services.

Staff Accounting Bulletin No. 101 was issued by the FASB to clarify its guidelines on

revenue recognition.

If the seller is a principal, the seller typically is vulnerable to risks associated with

collecting payment from the customer.

Sellers are only required to adjust the transaction price to reflect the time value of

money when the contract has a significant financing component.

Stock dividends cause a reduction in retained earnings, but they never reduce total

shareholders’ equity.

Cash paid for taxes and interest must be disclosed on the face of the statement or in the

disclosure notes under both the direct and indirect methods of reporting cash flows from

operating activities.

Rent collected in advance results in deferred tax assets.

When the expected collection of accounts receivable is difficult to estimate, companies

must use the cost recovery method.

Bonds are issued on June 1 that have interest payment dates of April 1 and October 1.

Bond interest expense for the year ended December 31, 2016, is for a period of:

a. Three months.

b. Four months.

c. Six months.

d. Seven months.

Which of the following is not required by generally accepted accounting principles?

a. Cash flow per share.

b. Earnings per share.

c. Statement of cash flows.

d. Disclosure notes.

Nonconvertible bonds affect the calculation of:

a. Basic earnings per share.

b. Diluted earnings per share.

c. Both A and B.

d. None of these answer choices is correct.

Drebin Security Systems sold merchandise to a customer in exchange for a $50,000,

five-year, noninterest-bearing note when an equivalent loan would carry 10% interest.

Drebin would record sales revenue on the date of sale equal to:

a. $50,000.

b. Zero.

c. The future value of $50,000 using a 10% interest rate.

d. The present value of $50,000 using a 10% interest rate.

Hepburn Company bought a copyright for $90,000 on January 1, 2013, at which time

the copyright had an estimated useful life of 15 years. On January 5, 2016, the company

determined that the copyright would expire at the end of 2021. How much should

Hepburn record as amortization expense for this copyright for 2016?

a. $14,400.

b. $ 7,200.

c. $ 8,000.

d. $12,000.

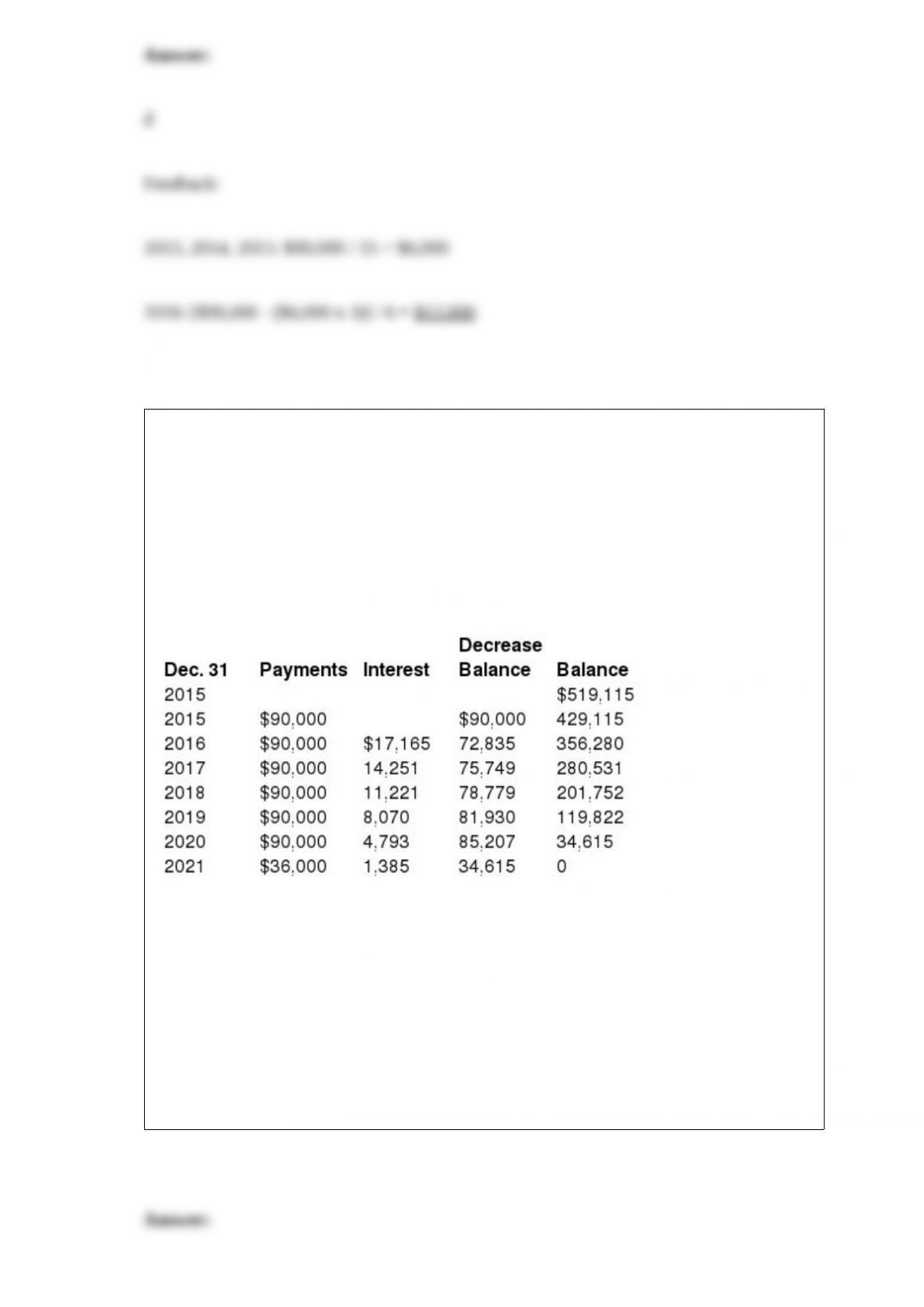

On December 31, 2015, Reagan Inc. signed a lease for some equipment having a

nine-year useful life with Silver Leasing Co. The lease payments are made by Reagan

annually, beginning at signing date. Title does not transfer to the lessee, so the

equipment will be returned to the lessor on December 31, 2021. There is no bargain

purchase option, and Reagan guarantees a residual value to the lessor on termination of

the lease.

Reagan’s lease amortization schedule appears below:

What is the book value of the lease liability on Reagan’s December 31, 2017, balance

sheet (after the third lease payment is made)?

a. $280,531.

b. $190,530.

c. $266,280.

d. $356,280.

Mars Inc. has a defined benefit pension plan. On December 31 (the end of the fiscal

year), the company received the PBO report from the actuary. The following

information was included in the report: ending PBO, $110,000; benefits paid to retirees,

$10,000; interest cost, $7,200. The discount rate applied by the actuary was 8%. What

was the beginning PBO?

a. $ 90,000.

b. $100,000.

c. $107,200.

d. $112,000.

When bonds are sold at a premium and the effective interest method is used, at each

interest payment date, the interest expense:

a. Remains constant.

b. Is equal to the change in book value.

c. Increases.

d. Decreases.

Major Co. reported 2016 income of $300,000 from continuing operations before

income taxes and a before-tax loss on discontinued operations of $80,000. All income is

subject to a 30% tax rate. In the 2016 income statement, Major Co. would show the

following line-item amounts for income tax expense and net income:

a. $66,000 and $210,000.

b. $90,000 and $154,000.

c. $90,000 and $276,000.

d. $66,000 and $220,000.

Under International Financial Reporting Standards, development expenditures are:

a. Expensed in the period incurred.

b. Expensed in the period they are determined to be unsuccessful.

c. Capitalized if certain criteria are met.

d. All of these answer choices are incorrect.

Heidi Aurora Imports issued shares of the company”s Class B stock. Heidi Aurora

Imports should report the stock in the company”s statement of financial position:

a. Among liabilities if the shares are mandatorily redeemable or redeemable at the

option of the shareholder.

b. As equity unless the shares are mandatorily redeemable.

c. As equity unless the shares are redeemable at the option of the issuer.

d. Among liabilities unless the shares are mandatorily redeemable.

Jaycom Enterprises has invested its excess cash in the stock of several different

companies and desires to maximize income over the short run. Jaycom is unsure about

the appropriate investment policy and thus what reporting practice to follow.

Required:

What classification procedure and subsequent classification could Jaycom follow in

order to meet its objective? How will Jaycom justify its choice to the Jaycom auditors?

Colombo Coffee sells gift cards that can be used at its 55 branches. During 2015,

customers purchased $25,000 of gift cards, of which $3,000 were redeemed during

2016. It is estimated that a balance of $1,500 of cards sold in 2015 remains unused as of

the end of 2016, and Colombo determines that this amount will never be redeemed,

based on historical experience. During 2016, Colombo further sold $32,000 of gift

cards, of which $26,000 were redeemed and $6,000 remain unused but may be used by

customer in 2017. Required: How much gift card revenue should Colombo recognize

in 2016?

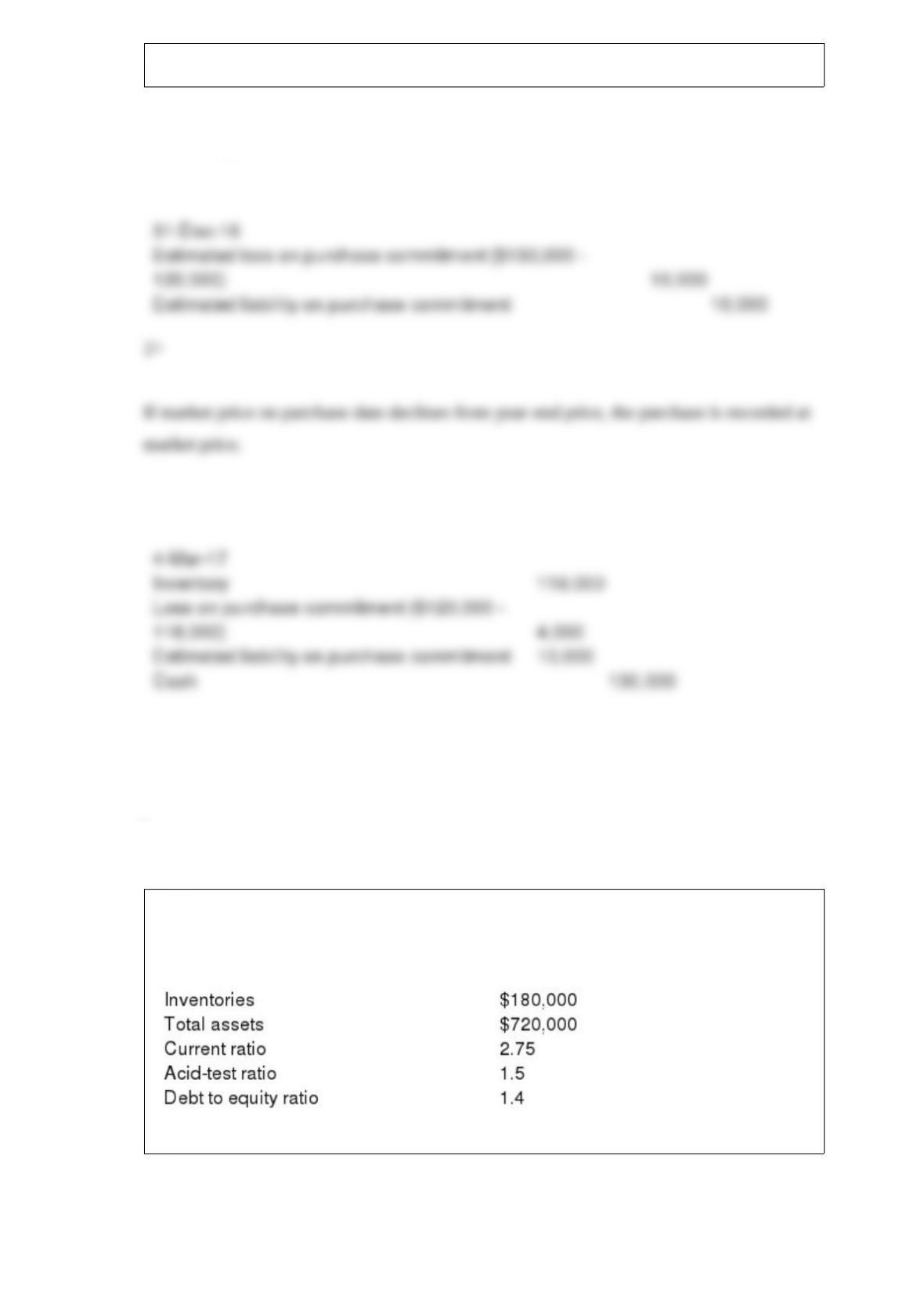

On September 5, 2016, Howard Corporation signed a purchase commitment to purchase

inventory for $130,000 on or before March 31, 2017. The company’s fiscal year-end is

December 31. The contract was exercised on March 4, 2017, and the inventory was

purchased for cash at the contract price. On the purchase date of March 4, the market

price of the inventory was $116,000. The market price of the inventory on December

31, 2016, was $120,000. The company uses a perpetual inventory system. Required:

1> Prepare the necessary adjusting journal entry (if any is required) on December 31,

2016.

2> Prepare the journal to record the purchase on March 4, 2017.

Spartan Sportswear’s current assets consist of cash, marketable securities, accounts

receivable, and inventories. The following data were abstracted from a recent financial

statement:

Required: Compute the following for Spartan: Current assets

It is the end of the accounting period, and your boss asks you to help determine the

inventory balance to place in the company’s balance sheet. Explain which physical

quantities of inventory that you will include and which you will exclude.

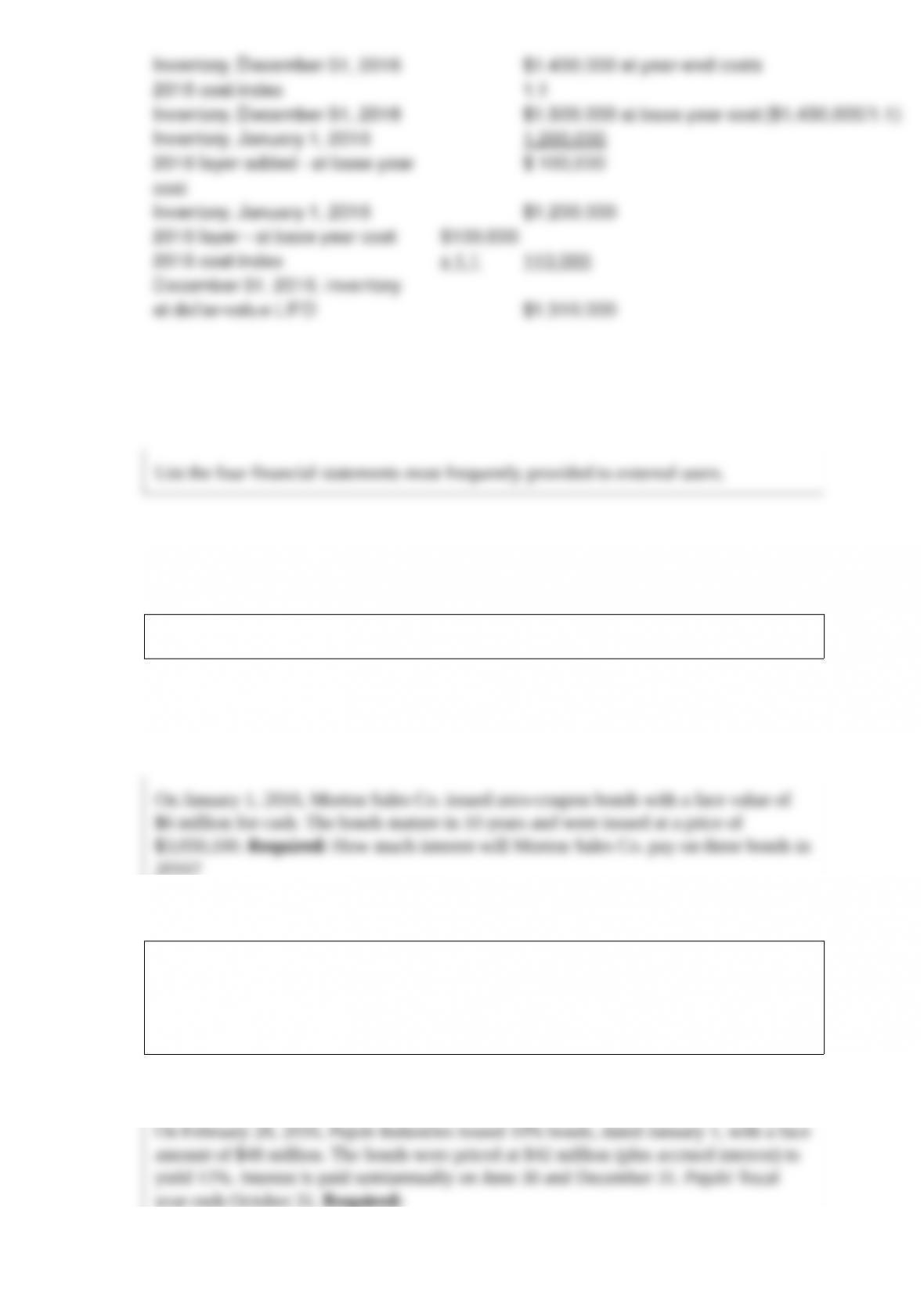

Appleton Inc. adopted dollar-value LIFO on January 1, 2016, when the inventory value

was $1,200,000. The December 31, 2016, ending inventory at year-end costs was

$1,430,000 and the cost index for the year is 1.1.

Required:

Compute the dollar-value LIFO inventory valuation for the December 31, 2016,

inventory.

List the four financial statements most frequently provided to external users.

On January 1, 2016, Morton Sales Co. issued zero-coupon bonds with a face value of

$6 million for cash. The bonds mature in 10 years and were issued at a price of

$3,050,100. Required: How much interest will Morton Sales Co. pay on these bonds in

2016?

On February 28, 2016, Pujols Industries issued 10% bonds, dated January 1, with a face

amount of $48 million. The bonds were priced at $42 million (plus accrued interest) to

yield 12%. Interest is paid semiannually on June 30 and December 31. Pujols’ fiscal

year ends October 31. Required:

1> What would be the amount(s) related to the bonds Pujols would report in its balance

sheet at October 31, 2016?

2> What would be the amount(s) related to the bonds that Pujols would report in its

income statement for the year ended October 31, 2016?

3> What would be the amount(s) related to the bonds that Pujols would report in its

statement of cash flows for the year ended October 31, 2016?

On January 1, 2016, Jeans-R-Us Company awarded 15 million of its $1 par common

shares to key personnel, subject to forfeiture if employment is terminated within three

years. On the date of the grant, the stock had a market price of $3 per share.

Required:

(1) Determine the total compensation cost pertaining to the restricted shares.

(2) Prepare the appropriate journal entry to record the award on January 1, 2016.

(3) Prepare the appropriate journal entry to record compensation expense on December

31, 2016.

(4) Prepare the appropriate journal entry to record compensation expense on December

31, 2017.

(5) Prepare the appropriate journal entry to record compensation expense on December

31, 2018.

(6) Prepare the appropriate journal entry to record the lifting of restrictions on

December 31, 2018.