The fixed asset turnover ratio is a profitability ratio.

Generally Accepted Accounting Principles (GAAP) require profitable companies to

distribute some of their earnings to their stockholders.

The use of internal controls guarantees protection against losses due to fraud, errors,

and inefficiencies.

The effective-interest method of amortization is considered a conceptually superior

method of accounting for bonds.

The periodic inventory system uses the Inventory account to keep track of the amount

of inventory that is purchased.

The payment of interest on bonds is classified as a cash outflow from operating

activities on the statement of cash flows.

The accounts receivable account for each customer is called a subsidiary account.

Depreciation is a measure of the decline in market value of an asset.

FICA payments consist of Social Security taxes and Medicare taxes.

When duties are properly segregated, the accounting department should compare the

cash in the register with the cash count sheet.

FOB shipping point means that ownership of goods passes to the buyer when the goods

reach the buyer.

When a company prepares a classified balance sheet, stockholders ‘ equity accounts

must be shown in subcategories of current and noncurrent.

Assuming nothing else changes, a decrease in average net fixed assets will cause the

fixed asset turnover ratio to increase.

The primary goals of inventory managers are to maintain a sufficient quantity of

inventory to meet customers ‘ needs, ensure inventory quality meets customers ‘

expectations and company standards, and minimize the cost of acquiring and carrying

inventory.

Which of the following statements about the concepts underlying the balance sheet is

correct?

A) A company bought land for $5 million dollars 10 years ago. The land is now worth

$15 million. The company should increase the book value of this asset on its balance

sheet to reflect its current value.

B) All events affecting the current value of a company are reported on the balance

sheet.

C) According to the cost principle, assets are valued at their replacement cost.

D) If an asset ‘s value increases, the increase in value is generally not recorded under

GAAP.

If the market rate of interest is 6%, a $10,000, 10-year bond with a stated annual

interest rate of 8% would be issued at an amount:

A) less than face value.

B) equal to the face value.

C) greater than face value.

D) equal to the face value minus a discount.

An increasing balance in the Inventory account accompanied by an increase in the

inventory turnover ratio would imply that the inventory build-up is occurring because:

A) inventory is not selling as fast as anticipated.

B) the company is expecting to sell more inventory in the future.

C) inventory is selling, but it is taking longer to collect payment from customers.

D) the economy is slowing down.

A company lent $10,000 to an employee who signed a 9%, 6-month promissory note.

The entry made by the company to record this loan to the employee will include a:

A) debit to Accounts Receivable for $10,000.

B) credit to Sales for $10,000.

C) debit to Notes Receivable for $10,000.

D) credit to Notes Payable for $10,000.

Which of the following is calculated by dividing (net income less preferred dividends)

by average common stockholders’ equity?

A) Return on assets ratio

B) Return on equity ratio

C) Earnings per share

D) Net profit margin ratio

On a common size balance sheet what is the percentage that would be shown next to the

dollar amount of current assets?

A) 100%

B) 44%

C) 30%

D) 33%

Which of the following statements about the calculations used for the weighted average

inventory costing method is correct?

A) Under the weighted average cost method, if the goods in inventory were purchased

at three different prices, the three different prices would be added and then divided by

three to find the weighted average cost per unit.

B) When the weighted average inventory costing method is used, ending inventory and

cost of goods sold are calculated using different costs per unit.

C) There is no difference in the calculations under the weighted average method

whether a perpetual or periodic inventory system is used.

D) The weighted-average method will produce an inventory cost which is between the

results of FIFO and LIFO inventory costing methods.

Which of the following statements about a company’s fiscal year is correct?

A) All companies have a December 31 year end.

B) It usually corresponds to a company’s slow period.

C) It always corresponds to the calendar year.

D) The Financial Accounting Standards Board assigns a year end to each company.

Mansfield Company has a periodic inventory system and uses the LIFO method to

assign costs to inventory and cost of goods sold. Consider the following information:

What amounts would be reported as the cost of goods sold and ending inventory

balances for the period?

A) Cost of goods sold $625; Ending inventory $175

B) Cost of goods sold $755; Ending inventory $225

C) Cost of goods sold $550; Ending inventory $250

D) Cost of goods sold $600; Ending inventory $200

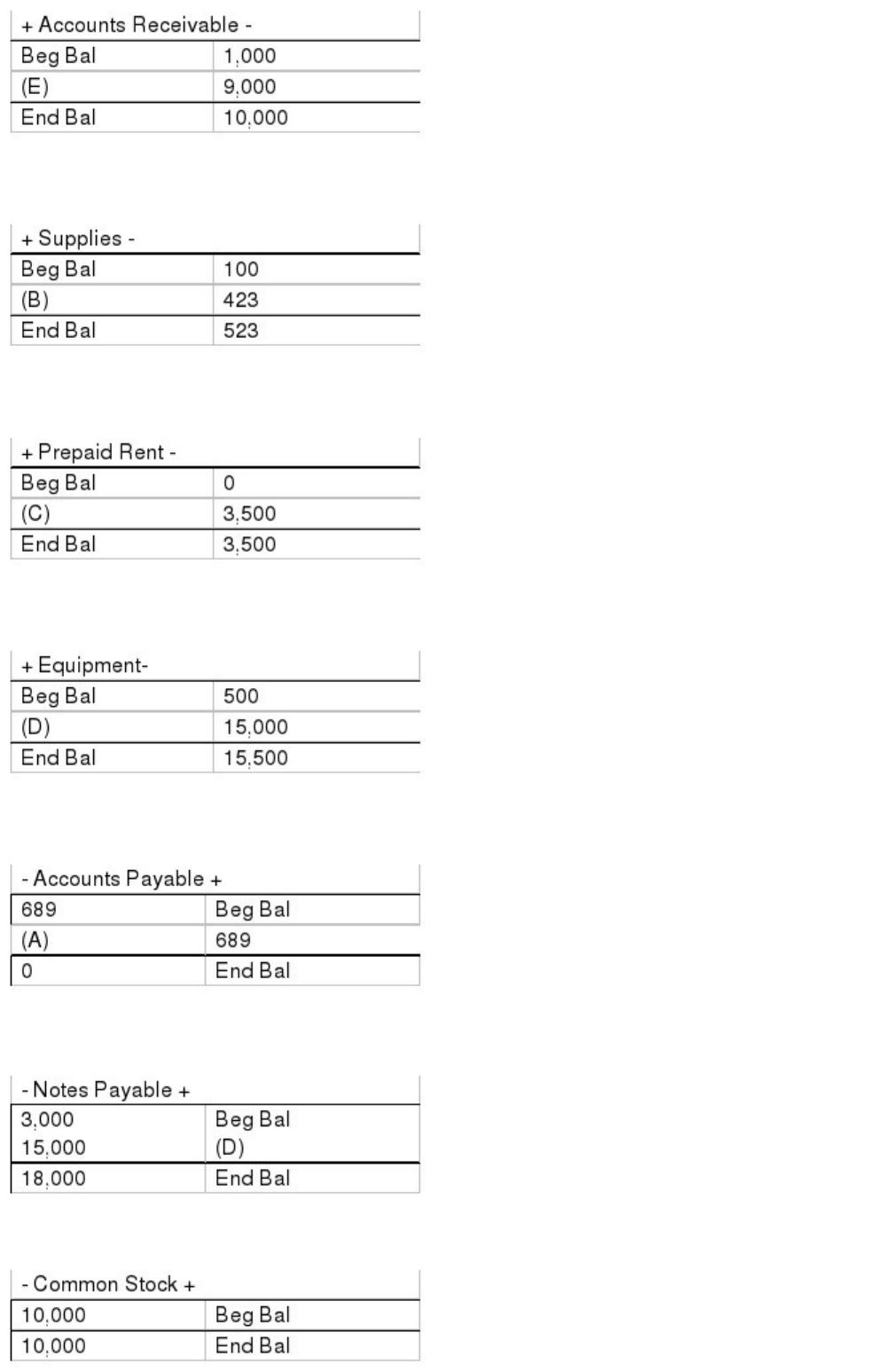

Geo Inc. had the following account balances on January 1, Year 2:

During January, Year 2, Geo entered into the following transactions:

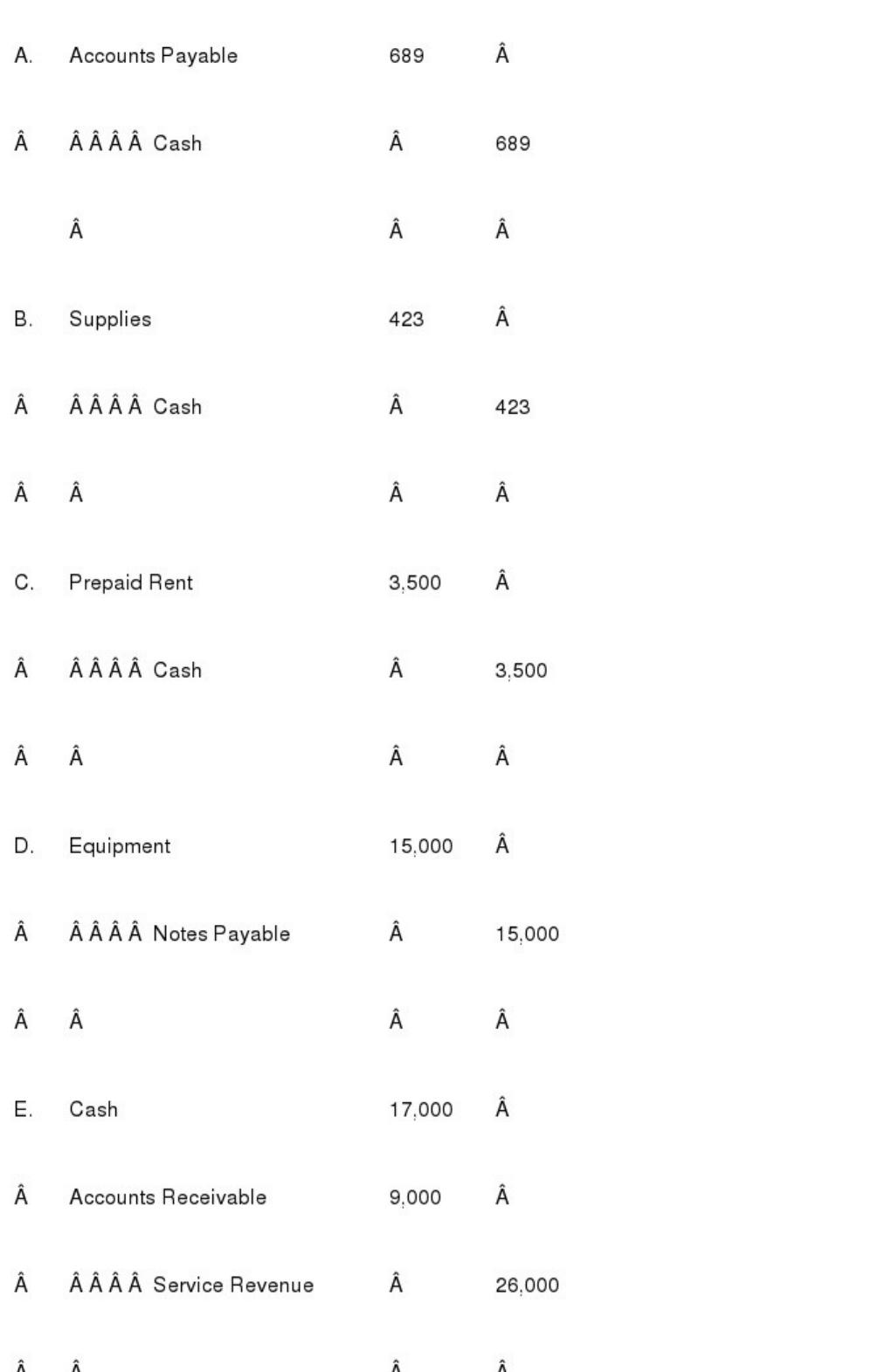

A. Paid $689 on account for utilities that were used during December Year 1.

B. Purchased $423 of supplies for cash.

C. Signed a rental agreement for office space and paid $3,500 in advance for six months

of rent beginning February 1, Year 2.

D. Purchased $15,000 of new equipment, signing a promissory note.

E. Provided $26,000 of services. $17,000 was received in cash and $9,000 was

provided on credit.

F. Paid workers $8,300 for work done in January.

Required:

Part a. Prepare journal entries to record the transactions identified among activities (A)

through (F).

Part b. Set up T-accounts for Cash, Accounts Receivable, Supplies, Prepaid Rent,

Equipment, Accounts Payable, Note Payable, Common Stock, Retained Earnings,

Service Revenue, and Salaries and Wages Expense. The beginning balance in each

T-account should be the amount shown in the list of account balances above or $0 if the

account does not appear above. Then, summarize the effects of each transaction in the

appropriate T-accounts.

Part c. After posting the journal entries to the T-accounts, compute ending balances for

each of the T-accounts.

The unadjusted trial balance at the end of the year includes the following:

Both accounts have normal balances. The company uses the aging of accounts

receivable method. Its estimate of uncollectible receivables resulting from the aging

analysis equals $5,800. What is the amount of Bad Debt Expense to be recorded for the

year?

A) $5,800

B) $4,800

C) $6,800

D) $7,800

Jay-Cee Corporation had 20,000 shares of $4 par value common stock outstanding on

January 1. On January 20, the company purchased 2,000 of its stock for $16 per share.

On July 3, the company reissued 1,000 of the shares at $20 per share. Jay-Cee uses the

cost method to account for its treasury stock.

Use the information above to answer the following question. What journal entry will

record the purchase of the stock on January 20?

A) Debit Treasury Stock for $8,000, debit Additional Paid-in Capital for $24,000, and

credit Cash for $32,000

B) Debit Treasury Stock and credit Cash for $32,000

C) Debit Treasury Stock for $8,000, debit Common Stock for $24,000, and credit Cash

for $32,000

D) Debit Common Stock and credit Cash for $32,000

Choose the appropriate letter to match the term and the definition. Not all definitions

will be used.

Term:

1> _____ Current liabilities

2> _____ Effective interest method of amortization

3> _____ Straight-line method of amortization

4> _____ Times interest earned ratio

5> _____ Long-term liabilities

6> _____ Present value

Definition:

A. A bond feature that puts a creditor ahead of other creditors in order of payment.

B. Current liabilities divided by current assets.

C. These are liabilities that have to be paid in one year or less.

D. Net income before taxes and interest expense divided by interest expense.

E. Spreads a bond discount or premium evenly over the lifetime of the bond.

F. The amount of all the liabilities currently on the balance sheet at the close of the

period.

G. Where interest expense is the market interest rate times the bond’s carrying value.

H. Net income after taxes and interest expense divided by interest expense.

I. These are liabilities that do not have to be paid within the upcoming year.

J. The ability to pay current obligations.

K. Liquid assets divided by current liabilities.

L. A calculation that determines what some future payments are worth today.

Assets totaled $24,250 and liabilities totaled $8,500 at the beginning of the year. During

the year, assets decreased by $3,500 and liabilities increased by $2,800.

Use the information above to answer the following question. What is the amount of

stockholders ‘ equity at the end of the year?

A) $9,450.

B) $15,750.

C) $15,050.

D) $14,450.

A times interest earned ratio of 11 means that the company’s:

A) net income is large enough to pay interest and taxes 11 times.

B) net cash flow from operations before taxes and interest is large enough to pay

interest and taxes 11 times.

C) net cash flow from operations is large enough to pay interest and taxes 11 times.

D) income before taxes and interest is large enough to pay interest 11 times.

Which of the following statements about financing activities is not correct?

A) Cash dividends paid to a company’s stockholders are reported as cash outflows from

financing activities.

B) When a company issues stock for cash, it reports a cash inflow from financing

activities.

C) When a company repurchases stock with cash, it reports a cash outflow for financing

activities.

D) When a company repays a loan, it reports a cash inflow from financing activities.