Regal Real Estate which maintains its accounts on the basis of a fiscal year ending June

30, began the management of an office building on June 15 for an agreed annual fee of

$4,800. The first payment is due on July 15. The adjusting entry required at June 30 is:

A. A debit to Management Fees Receivable for $200 and a credit to a revenue account

for $200.

B. A $200 debit to Unearned Management Fees and a $200 credit to Management Fees

Earned.

C. A debit to Cash for $200 and a credit to Management Fees Earned.

D. A debit to Cash for $400 offset by a credit to a revenue account for $200 and a

liability for $200.

The entry to record the issuance of common stock at a price above its par value

includes:

A. A credit to Cash.

B. A credit to a liability account for the difference between the price paid by the

stockholders and the par value of the stock.

C. A credit to Additional Paid-in Capital: Common Stock.

D. A debit to Common Stock.

Early in 2015, Larsen Corporation purchased marketable securities at a cost of $90,000.

In September, dividends of $6,600 were received; Larsen sold the securities in

December at a gain of $5,600. How would these transactions be reported on Larsen’s

statement of cash flows for 2015?

A. $95,600 net cash provided by investing activities; $6,600 included in cash provided

by operating activities.

B. $12,200 net cash provided by investing activities.

C. $95,600 cash provided by investing activities; $90,000 cash used in financing

activities.

D. $84,400 net cash used in investing activities; $95,600 cash provided by investing

activities.

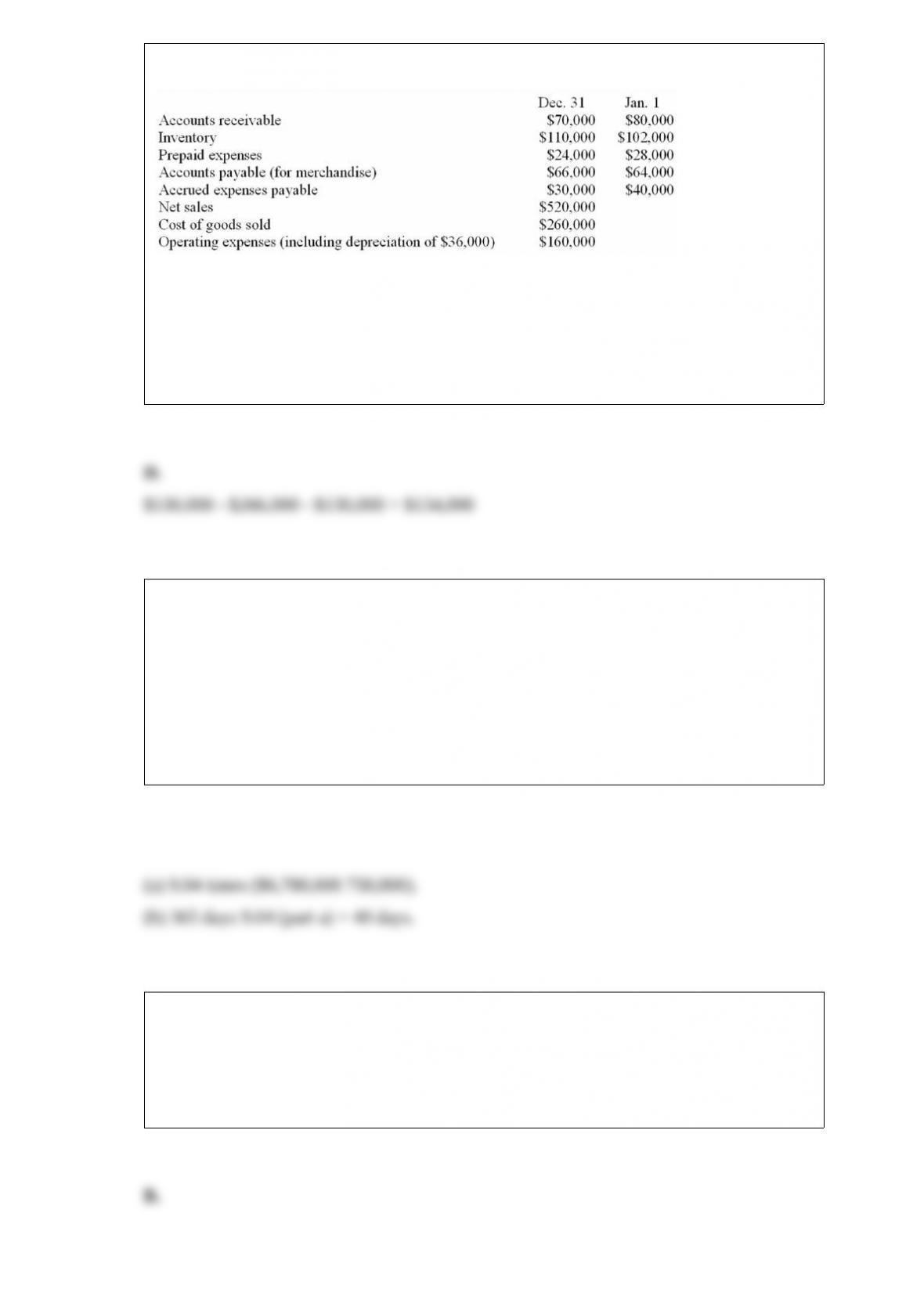

The financial statements of Garver, Inc., provide the following information for the

current year:

Refer to the information above. Net cash flow from operating activities for the current

year is:

A. $114,000.

B. $118,000.

C. $122,000.

D. $134,000.

Accounts receivable turnover rate

During 2015, Larsen Company’s accounts receivable averaged $750,000. Larsen’s 2015

income statement reported net sales of $6,780,000, uncollectible accounts expense of

$160,000, and net income of $768,000. (Assume 365 days in a year.)

Using the information, compute the following for Larsen Company:

(a) Accounts receivable turnover: (Round to the nearest two decimals.)

(b) Average number of days to collect accounts receivable

(Round to nearest day, if necessary): (Round to the nearest %.)

The accrual of interest on a note payable will:

A. Reduce total liabilities.

B. Increase total liabilities.

C. Have no effect upon total liabilities.

D. Will have no effect upon the income statement but will affect the balance sheet.

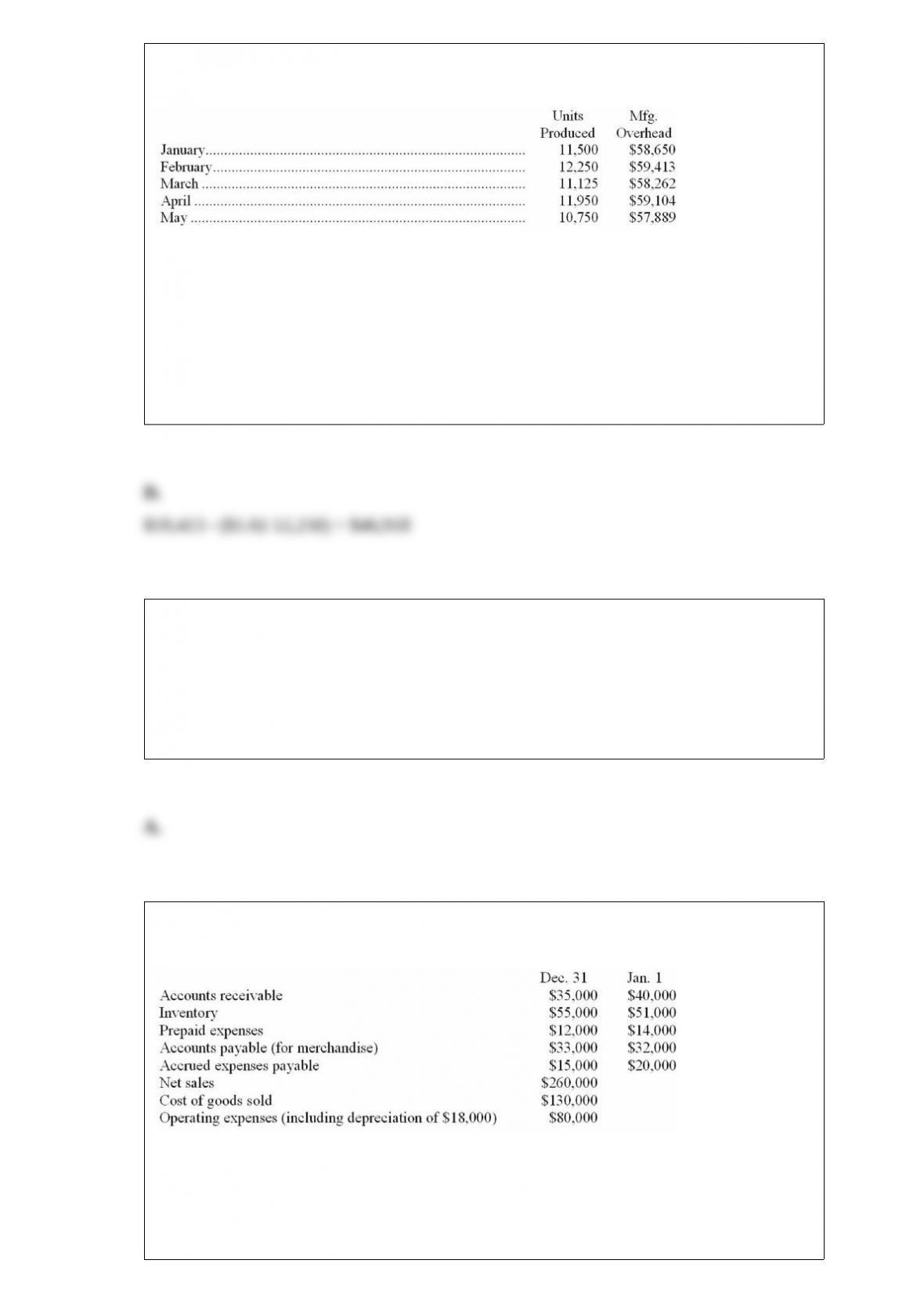

The levels of production and of manufacturing overhead for the first five months of

2015 for Duke & Duchess Products are shown below:

Refer to the information above. Using the high-low method, Duke & Duchess’s monthly

overhead cost is closest to which of the following? (Round your intermediate

computations to two decimal places.)

A. $59,413.

B. $12,495.

C. $12,250.

D. $46,918.

In which of the following situations would the largest amount be recorded as an

expense of the current year? (Assume accrual basis accounting.)

A. $4,000 is paid in January for equipment with a useful life of four years.

B. $1,800 is paid in January for a two-year fire insurance policy.

C. $1,200 cash dividends are declared and paid.

D. $900 is paid to an attorney for legal services rendered during the current year.

The financial statements of Seldin, Inc., provide the following information for the

current year:

Refer to the information above. Seldin’s net cash flow from operating activities for the

current year is:

A. $57,000.

B. $59,000.

C. $61,000.

D. $67,000.

At year-end, the perpetual inventory records of Anderson Co. indicate 60 units of a

particular product in inventory, acquired at the following dates and unit costs:

Purchased in August: 30 units at $750 per unit.

Purchased in November: 30 units at $700 per unit.

A complete physical inventory taken at year-end indicates only 50 units of this product

actually are on hand.

Refer to the information above. Under the LIFO cost flow assumption, the cost of this

item to be included as inventory in the company’s year-end balance sheet is:

A. $36,000.

B. $42,000.

C. $36,500.

D. $37,500.

When goods are completed and transferred from the assembly line:

A. Cost of Goods Sold is debited and Finished Goods Inventory is credited.

B. Work in Process Inventory is debited and Finished Goods Inventory is credited.

C. Finished Goods Inventory is debited and Cost of Goods Sold is credited.

D. Work in Process Inventory is credited and Finished Goods Inventory is debited.

Webster Company issues $1,000,000 face value, 6%, 5-year bonds payable on

December 31, 2015. Interest is paid semiannually each June 30 and December 31. The

bonds sell at a price of 97; Webster uses the straight-line method of amortizing bond

discount or premium.

Refer to the information above. The amount of bond interest expense recognized by

Webster Company in 2016 with respect to these bonds is:

A. $60,000.

B. $63,000.

C. $120,000.

D. $66,000.

Accumulated Depreciation is:

A. An asset account.

B. A revenue account.

C. A contra-asset account.

D. An expense account.

The valuation principle of “fair value accounting” applied to investments classified as

available for sale securities:

A. Affects the current period income statement, but not the balance sheet.

B. Enhances usefulness of the balance sheet in evaluating the financial position of a

business.

C. Applies to marketable securities and inventories.

D. Requires a corporation to adjust its capital stock account to reflect current market

value of its outstanding capital stock.

Which of the following is a measure of short-term liquidity?

A. Quick ratio.

B. Return on assets.

C. Dividend yield.

D. Debt ratio.

Retained Earnings at the end of a period:

A. Is equal to the balance in the Retained Earnings account in the adjusted trial balance

at the end of a period.

B. Is determined in the Statement of Retained Earnings.

C. Is equal to Retained Earnings at the beginning of the period, minus net income (or

plus net loss) for the period.

D. Appears in the Income Statement for the period.

On April 1, year 1, Cricket Corporation issues $60 million of 12%, 10-year bonds

payable at par. Interest on the bonds is payable semiannually each April 1 and October

1.

Refer to the information above. Interest expense on this bond issue reported in Cricket’s

Year 1, income statement is:

A. $2,400,000.

B. $4,800,000.

C. $5,400,000.

D. $7,200,000.

Efficient management of cash includes which of the following concepts?

A. Pay each bill as soon as the invoice is received.

B. Deposit all cash receipts and make all cash disbursements at the end of each week.

C. Prepare a control listing of cash receipts at the time and place the money is received.

D. Pay suppliers in cash out of cash sales receipts before depositing them in the bank.

Hahn Corp. has three employees. Each earns $600 per week for a five day work week

ending on Friday. This month the last day of the month falls on a Wednesday. The

company should make an adjusting entry:

A. Debiting Wage Expense for $1,080 and crediting Wages Payable for $1,080.

B. Debiting Wage Expense for $360 and crediting Wages Payable for $360.

C. Crediting Wage Expense for $1,080 and debiting Wages Payable for $1,080.

D. Crediting Wage Expense for $360 and debiting Wages Payable for $360.

Which of the following activities affects net income, but has no immediate impact upon

cash flows?

A. Collection of an account receivable.

B. Making the end-of-period adjustment to record estimated uncollectible accounts.

C. Investing excess cash in marketable securities.

D. Write-off of an uncollectible account receivable against the allowance.

Management compensation plans:

A. May be affected by adopting International Financial Reporting Standards since

earnings under IFRS are typically higher than GAAP earnings.

B. May be affected by adopting International Financial Reporting Standards since

earnings under IFRS are typically lower than GAAP earnings.

C. Will not be affected by IFRS since earnings are equivalent to GAAP.

D. Are decided by shareholders who do not consider GAAP or IFRS when deciding

how much compensation managers receive.

Master Equipment has a $17,400 liability to Arrow Paint Co. When Master Equipment

makes a partial payment of $7,600 on this liability, which of following occurs?

A. Retained earnings are debited $9,800.

B. The Accounts Payable account is credited $9,800.

C. The Cash account is debited $7,600.

D. The Accounts Payable account is debited $7,600.

Which of the following is not an objective of generally accepted accounting principles?

A. To minimize the amount of income taxes owed.

B. To ensure that both preparers and users of financial statements understand the

concepts and assumptions used in presenting information within these statements.

C. To enhance the relevance and verifiability of information contained in financial

statements.

D. To increase the comparability of financial statements prepared by different

companies.

Patterson’s Department Store prepares monthly income statements by sales

departments. These income statements are organized to show contribution margin,

performance margin, and responsibility margin for each sales department, as well as

operating income for the store as a whole.

Refer to the information above. The cost of heating and air conditioning the store

should be:

A. Allocated among the sales departments based upon their relative sales volume.

B. Allocated among the sales departments based upon their relative floor space.

C. Classified as a common fixed cost.

D. Omitted from the company’s income statements.

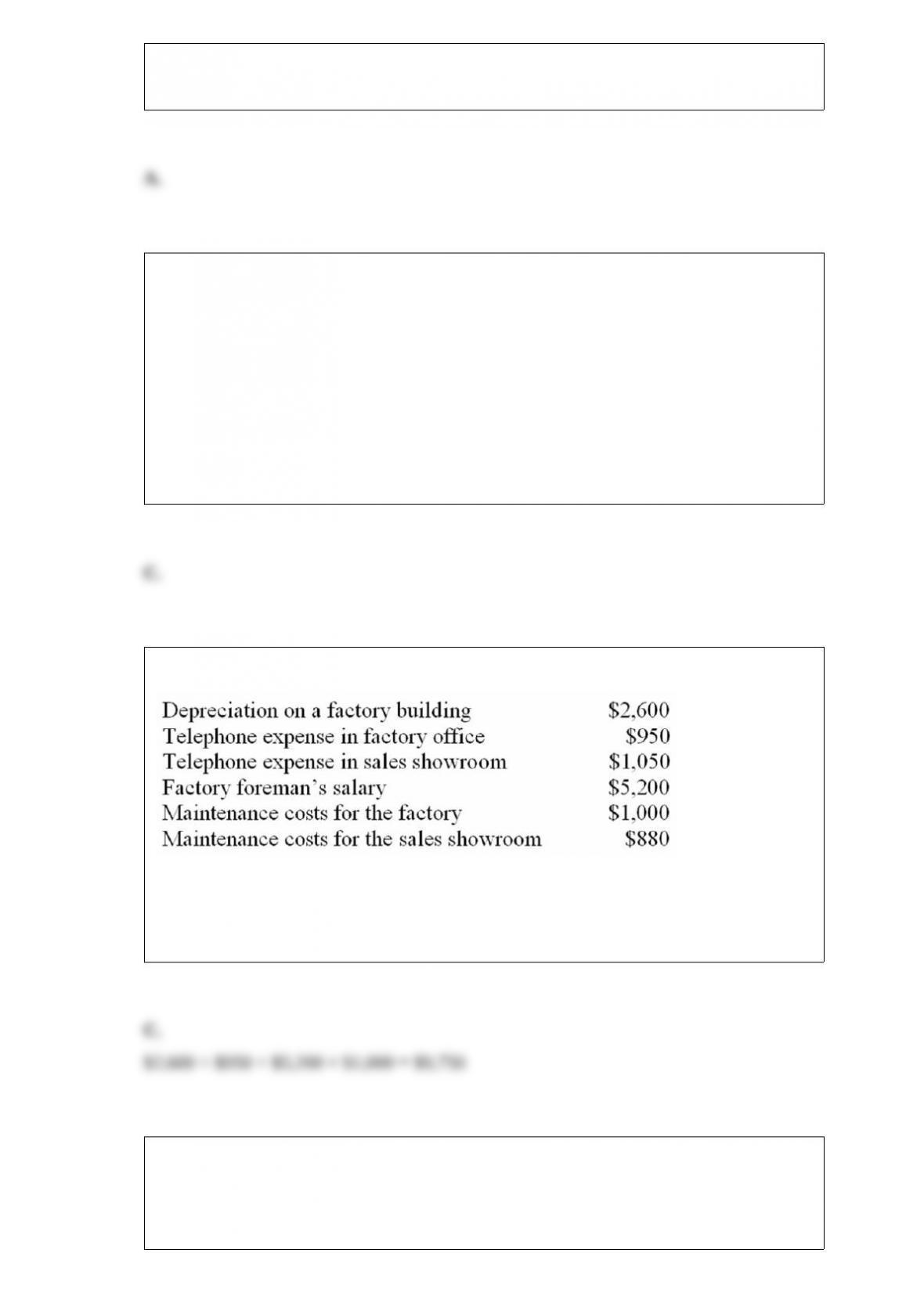

Determine the amount of manufacturing overhead given the following information:

A. $7,750.

B. $10,430.

C. $9,750.

D. $11,080.

Job order cost system

Century Pools designs and builds custom pools and spas to the customer’s order and

uses a job order system. The predetermined overhead rate for the current year is 60% of

direct labor cost.

At the end of the current year, Century Pools’ direct labor cost totaled $170,000 and

actual overhead amounted to $105,000.

A pool built for F. Becker required $32,000 of direct materials and $6,500 of direct

labor. It was completed in May of the current year.

(a) Compute the total cost of the Becker pool as shown on the job cost sheet at date of

completion.

(b) Compute the amount of under- or over-applied manufacturing overhead for

Century’s operations for the current year.

(c) What disposition is made of over- or under-applied overhead at the end of the year

(assume that the amount is not material)?

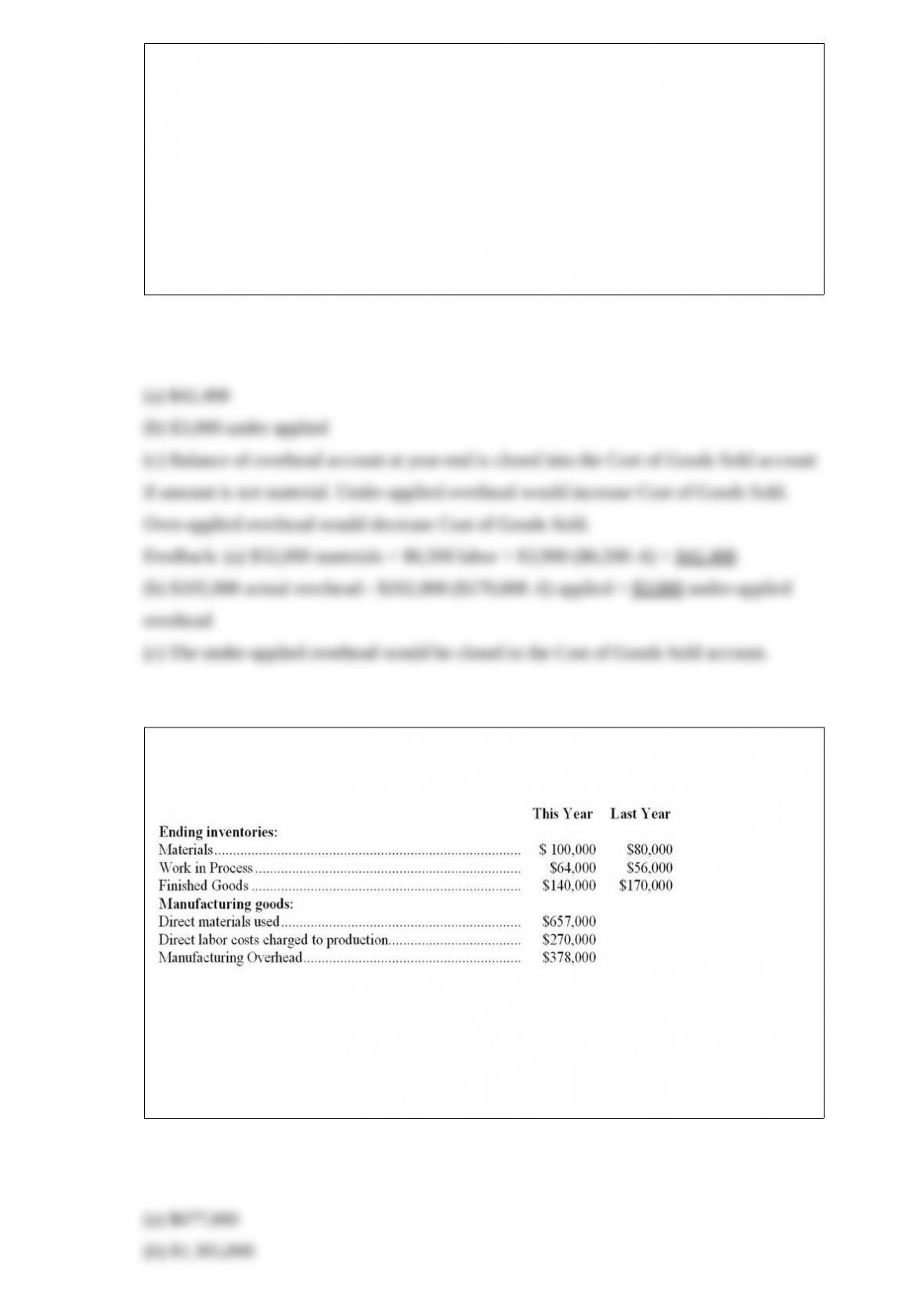

Flow of manufacturing costs

The following data are taken from the accounting records of Gregory Mfg. Co.:

Compute the following for the current year:

(a) Direct materials purchased: $___________

(b) Total manufacturing costs charged to production (the Work in Process Inventory

account): $___________

(c) The cost of finished goods manufactured: $___________

(d) The cost of goods sold: $___________

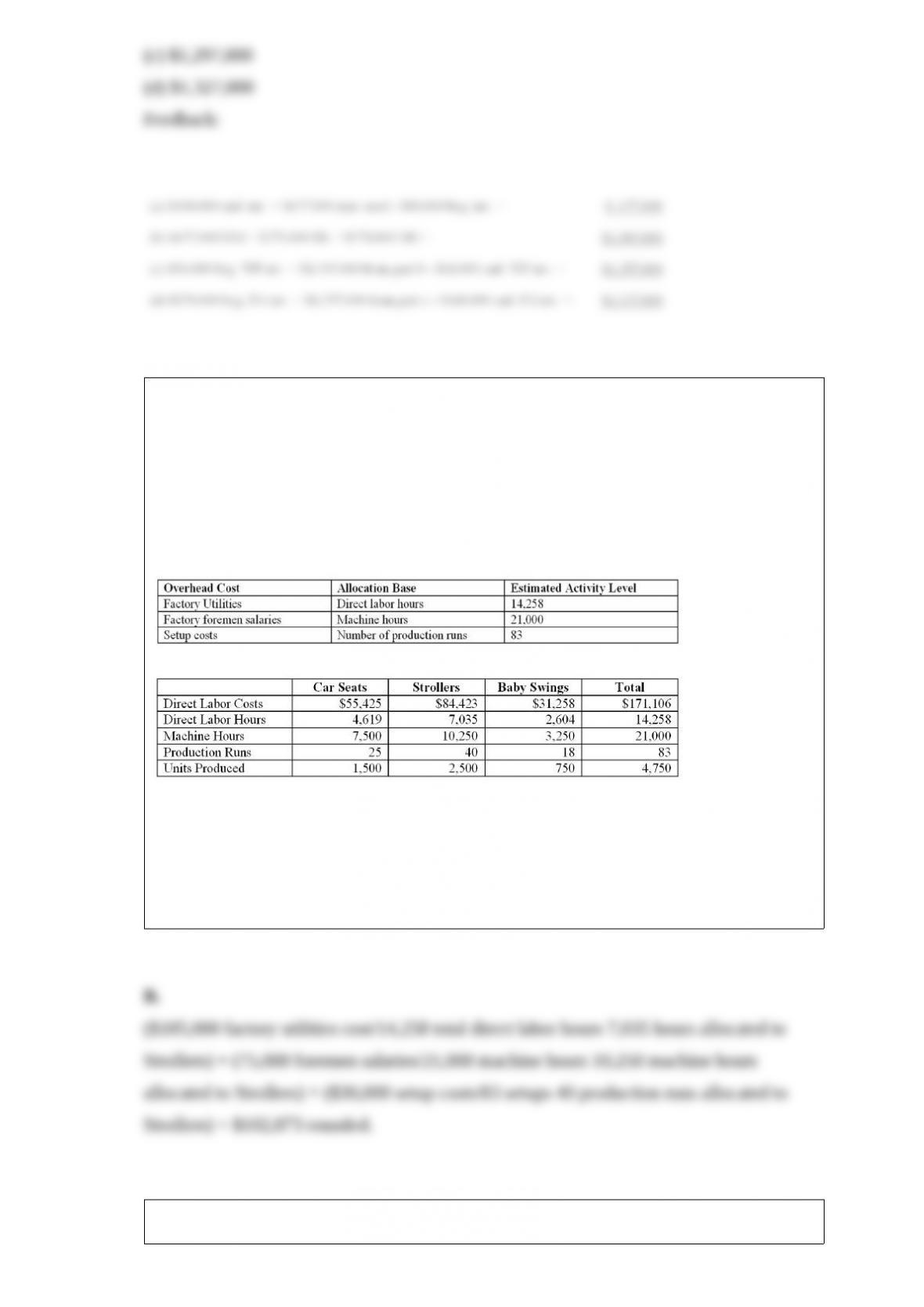

Starbright manufactures children car seats, strollers, and baby swings. Starbright’s

manufacturing costs are budgeted as follows:

Factory utilities $105,000

Factory foremen salaries $75,000

Machinery setup costs $30,000

Total manufacturing overhead $210,000

The company uses activity-based costing to allocate its manufacturing overhead costs to

products based on the following schedule:

During the current month, the following levels of activities were incurred:

What are the total manufacturing overhead costs allocated to the Strollers for the

current month?

A. $69,837.

B. $102,873.

C. $37,290.

D. $210,000.

The wages paid to employees working directly on a company’s products would be

shown as a:

A. Credit to Direct Labor.

B. Debit to Direct Labor.

C. Credit to Work in Process.

D. Debit to Manufacturing Overhead.

Temple Corporation purchased a piece of real estate, paying $400,000 cash and

financing $700,000 of the purchase price with a 10-year, 15% installment note. The

note calls for equal monthly payments that will result in the debt being completely

repaid by the end of the tenth year. In this situation:

A. The aggregate amount of the monthly payments is $700,000.

B. Each monthly payment is greater than the amount of interest accruing each month.

C. The portion of each payment representing interest expense will increase over the

10-year period, since principal is being paid off, yet the payment amount does not

decrease.

D. The portion of each monthly payment representing repayment of principal remains

the same throughout the 10-year period.

Which of the following is not one of the basic procedures related to activity-based

costing?

A. Identify the activity.

B. Create an associated activity cost pool.

C. Compute internal failure costs.

D. Calculate the cost per unit of activity.