Depreciation, in accounting, is a process that results in:

A. depreciable assets being reported in the balance sheet at their fair value.

B. accumulating cash for the replacement of the asset.

C. an accurate measurement of the economic usefulness of an asset.

D. spreading the cost of an asset over its useful life to the entity.

A journal entry recording an accrual:

A. results in a better matching of revenues and expenses.

B. will involve a debit or credit to cash.

C. will affect balance sheet accounts only.

D. will most likely include a debit to a liability account.

The intangible asset goodwill:

A. represents the management team’s assessment of its value to the company.

B. may arise when one company purchases another company.

C. arises because the fair value of a company’s assets is greater than cost.

D. all of the above are correct.

The largest item of the Deferred Tax Liability for most companies is caused by:

A. providing the allowance for doubtful accounts for book purposes.

B. differences in inventory cost flow assumptions (FIFO vs. LIFO) for tax versus

financial accounting purposes.

C. differences in depreciation methods (accelerated vs. straight-line) for tax versus

financial accounting purposes.

D. amortizing bond premium or discount for tax purposes.

Which of the following is not a category of financial statement ratios?

A. Financial leverage.

B. Liquidity.

C. Profitability.

D. Prospectus.

Krultz Corp. has annual revenues of $760,000, an average contribution margin ratio of

30 percent, and fixed expenses of $75,000.

(a.) Management is considering adding a new product to the company’s product line.

The new item will have $21 of variable costs per unit. Calculate the selling price that

will be required if this product is not to affect the average contribution margin ratio.

(b.) If the new product adds an additional $36,000 to Krultz’s fixed expenses, how

many units of the new product must be sold to break even on the new product?

(c.) If 12,000 units of the new product could be sold at a price of $32 per unit, and the

company’s other business did not change, calculate Krultz’s total operating income and

average contribution margin ratio.

An unqualified auditors’ opinion about an entity’s financial statements:

A. is a clean bill of health.

B. means that all of the entity’s transactions during the audited period were checked out.

C. guarantees that the entity was not involved in or the victim of any fraudulent

activities during the audited period.

D. states that they are presented in conformance with U.S. generally accepted

accounting principles.

The predetermined overhead application rate based on direct labor hours is computed

as:

A. actual total overhead costs divided by actual direct labor hours.

B. estimated total overhead costs divided by estimated direct labor hours.

C. actual total overhead costs divided by estimated direct labor hours.

D. estimated total overhead costs divided by actual direct labor hours.

________________ is a technique used to filter cost information contained in

performance reports to each manager within the organization at an appropriate level of

detail or summarization.

A. Managerial reporting

B. Responsibility reporting

C. Financial reporting

D. Segment reporting

Direct costs pertain to costs that:

A. are traceable to a cost object.

B. are not traceable to a cost object.

C. are commonly incurred.

D. are variable costs.

Management’s use of resources can best be evaluated by focusing on measures of:

A. liquidity.

B. activity.

C. leverage.

D. book value.

Which of the following is not a topic that is likely to be discussed as a significant

accounting policy?

A. Depreciation method.

B. Earnings per share of common stock calculation details.

C. Inventory valuation method.

D. Method of estimating uncollectible accounts receivable.

Moped, Inc. purchased machinery at a cost of $44,000 on January 1, 2017. The

expected useful life is 5 years and the asset is expected to have salvage value of $4,000.

Moped depreciates its assets using the double-declining balance method.

What is the firm’s depreciation expense for the year ended December 31, 2017?

A. $4,000

B. $8,800

C. $12,000

D. $17,600

A journal:

A. is where transactions are initially recorded.

B. is where transactions are posted to after they are initially recorded.

C. serves as an index to the ledger.

D. is the same as a source document, such as an invoice from a supplier or a copy of a

credit purchase made by a customer.

ABC Company’s standard direct labor cost per unit includes 3 hours @ $15 per hour.

During May ABC Company produced 380 units and incurred total labor cost of $16,200

for 1,200 actual direct labor hours worked. ABC’s labor rate variance for May is:

A. $1,200 U.

B. $1,200 F.

C. $1,800 U.

D. $1,800 F.

A predetermined overhead rate is used to:

A. keep track of actual overhead costs as they are incurred.

B. assign indirect costs to cost objects.

C. establish prices for manufactured products.

D. allocate selling and administrative expenses to manufactured products.

The accrual of interest on short-term marketable securities results in:

A. an increase in current assets and a decrease in net income.

B. an increase in current assets and an increase in net income.

C. an increase in noncurrent assets and an increase in liabilities.

D. an increase in current liabilities and an increase in net income.

Standards are likely to be most useful when expressed in:

A. dollars per unit of input to the manufacturing process.

B. quantities per unit of output from the process being evaluated.

C. total costs for the accounting period for the department being evaluated.

D. terms easily related to by the individual whose performance is being evaluated.

The principal weakness of the payback method for evaluating proposed investments is

that it does not:

A. provide a way of ranking projects in order of desirability.

B. consider cash flows that continue after the investment has been recovered.

C. result in an easily understood “answer”.

D. recognize the time value of money.

Indirect costs pertain to costs that:

A. are traceable to a cost object.

B. are not traceable to a cost object.

C. are commonly incurred.

D. are variable costs.

Financial ratios:

A. help financial statement users to evaluate the financial characteristics of companies

by putting the large dollar amounts reported in financial statements into relative terms

for comparison purposes.

B. provide for a more meaningful analysis when the trends of financial ratios for a

company are compared to the industry average trends over a period of time.

C. are required reporting disclosures in the notes to the consolidated financial

statements of U.S. companies that are regulated by the SEC.

D. All of the above statements are true.

E. A and B are true, but C is not true.

Which of the following lists the components of the master budget in correct

chronological order?

A. direct labor budget, production budget, cost of goods sold budget.

B. sales budget, production budget, cash budget.

C. sales budget, raw materials budget, production budget.

D. cash budget, production budget, manufacturing overhead budget.

A firm’s independent auditors have the responsibility to:

A. assess the firm’s accounting policies.

B. ascertain the firm’s profit potential.

C. uncover all fraudulent activities.

D. assess management’s discussion and analysis.

Which of the following accounts/captions are not ever included in the calculation for

Gross Profit?

A. Revenues.

B. Cost of Goods Sold.

C. Net Sales.

D. General and Selling Expenses.

A cash budget would include:

A. gain on sale of equipment.

B. sale of common stock.

C. building depreciation.

D. accounts receivable.

The distinction between a current asset and other assets:

A. is based on how long the asset has been owned.

B. is based on amounts that will be paid to other entities within a year.

C. is based on the ability to determine the current fair value of the asset.

D. is based on when the asset is expected to be converted to cash, or used to benefit the

entity.

The preferred format for a segmented income statement emphasizes:

A. direct and common fixed costs.

B. variable and fixed costs.

C. operating expenses and fixed costs.

D. variable costs and operating expenses.

If the net of all variances is immaterial relative to the total production costs incurred

during the period, the net variance is:

A. treated as an adjustment to cost of goods sold.

B. ignored.

C. treated as an adjustment to work in process, finished goods, and cost of goods sold.

D. treated as an adjustment to manufacturing overhead.

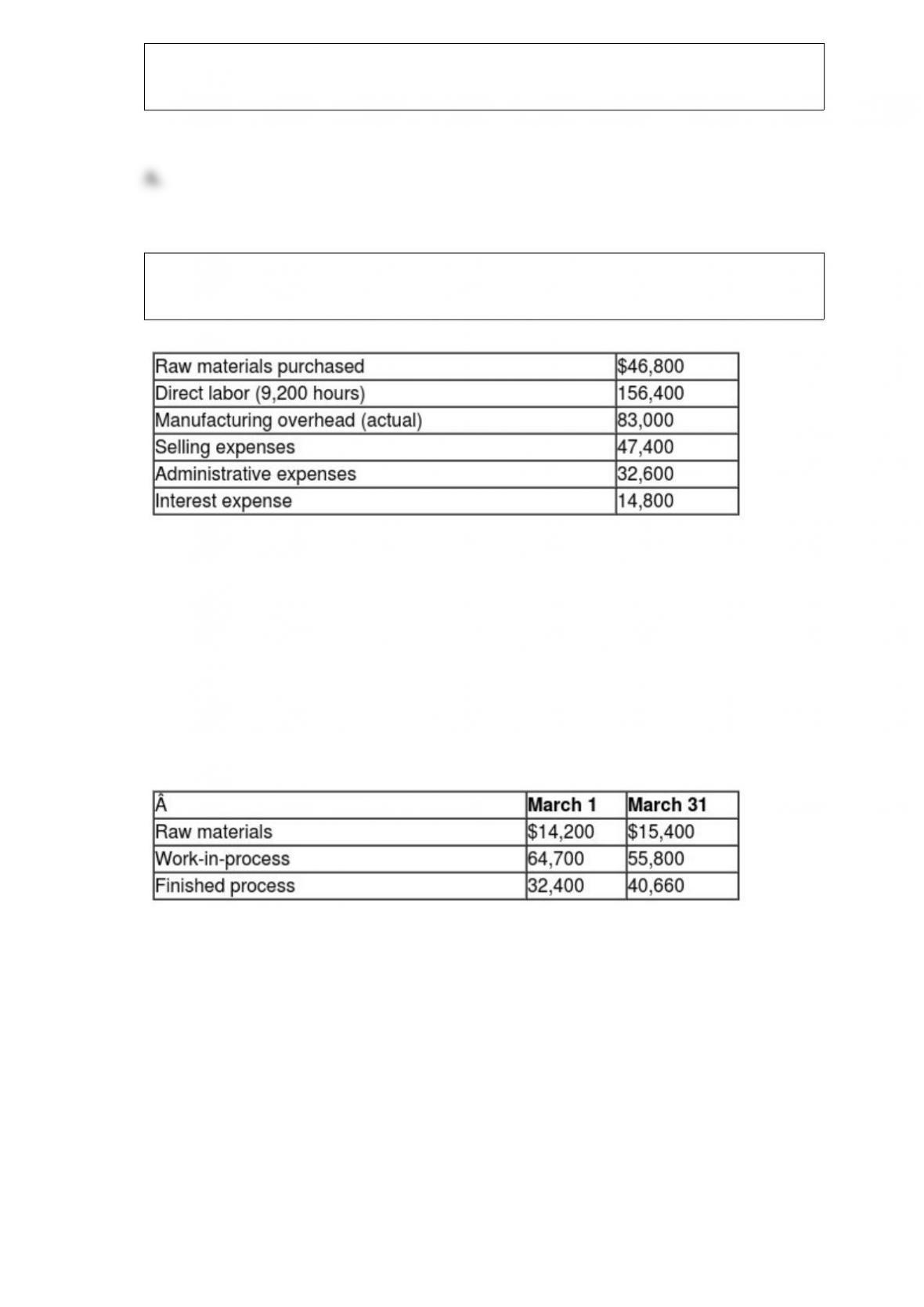

Partridge, Inc. incurred the following costs during March:

Manufacturing overhead is applied on the basis of $8.50 per direct labor hour. Assume

that overapplied or underapplied overhead is transferred to cost of goods sold only at the

end of the year. During the month, 3,500 units of product were manufactured and 3,400

units of product were sold. On March 1 and March 31, Partridge carried the following

inventory balances:

(a.) Prepare a Statement of Cost of Goods Manufactured for the month of March, and

calculate the average cost per unit produced.

(b.) Calculate the cost of goods sold during March.

(c.) Where in the financial statements will the difference between cost of goods

manufactured and cost of goods sold be classified?

A potential creditor’s judgment about granting credit would be most influenced by the

potential customer’s:

A. current ratio at the end of the prior fiscal year.

B. most recent acid-test ratio.

C. trend of acid-test ratio over the past three years.

D. practice with respect to taking cash discounts offered by current suppliers.

XYZ Company has a variable cost ratio of 40%, fixed expenses of $200,000, and

desires to earn operating income of $100,000. Total sales revenue required to achieve

XYZ Company’s desired operating income is:

A. $340,000.

B. $380,000.

C. $420,000.

D. $500,000.

When a corporation has both common stock and preferred stock outstanding:

A. dividends on preferred stock are paid only if the company has current earnings.

B. dividends on preferred stock must be paid before dividends on common stock can be

paid.

C. preferred stockholders receive the same dividend per share as common stockholders.

D. dividends on preferred stock are paid only if dividends are to be paid on the common

stock.

The principal reason for a company having a common stock split is to:

A. increase the total cash dividends paid to stockholders.

B. capitalize retained earnings.

C. decrease total stockholders’ equity.

D. decrease the market value per share of common stock.