Chapter 11: The Basics of Capital Budgeting

Copyright Cengage Learning. Powered by Cognero.

Page 53

96. Malholtra Inc. is considering a project that has the following cash flow and WACC data. What is the project’s MIRR?

Note that a project’s projected MIRR can be less than the WACC (and even negative), in which case it will be rejected.

WACC: 10.00%

Year 0 1 2 3 4

Cash flows –$975 $300 $320 $340 $360

a. 13.04%

b. 9.16%

c. 14.10%

d. 11.98%

e. 11.75%

97. Hindelang Inc. is considering a project that has the following cash flow and WACC data. What is the project’s MIRR?

Note that a project’s projected MIRR can be less than the WACC (and even negative), in which case it will be rejected.

Chapter 11: The Basics of Capital Budgeting

Copyright Cengage Learning. Powered by Cognero.

Page 54

WACC: 11.50%

Year 0 1 2 3 4

Cash flows –$850 $300 $320 $340 $360

a. 19.67%

b. 17.23%

c. 16.26%

d. 15.77%

e. 16.91%

98. Stern Associates is considering a project that has the following cash flow data. What is the project’s payback?

Year 0 1 2 3 4 5

Cash flows -$1,000 $300 $310 $320 $330 $340

a. 2.89 years

b. 2.92 years

c. 3.40 years

d. 3.21 years

e. 3.92 years

Copyright Cengage Learning. Powered by Cognero.

Page 56

100. Masulis Inc. is considering a project that has the following cash flow and WACC data. What is the project’s

discounted payback?

WACC: 10.00%

Year 0 1 2 3 4

Cash flows -$1,300 $525 $485 $445 $405

a. 2.62 years

b. 3.32 years

c. 2.75 years

d. 3.42 years

e. 3.05 years

101. Tesar Chemicals is considering Projects S and L, whose cash flows are shown below. These projects are mutually

exclusive, equally risky, and not repeatable. The CEO believes the IRR is the best selection criterion, while the CFO

advocates the NPV. If the decision is made by choosing the project with the higher IRR rather than the one with the higher

NPV, how much, if any, value will be forgone, i.e., what’s the chosen NPV versus the maximum possible NPV? Note that

(1) “true value” is measured by NPV, and (2) under some conditions the choice of IRR vs. NPV will have no effect on the

value gained or lost.

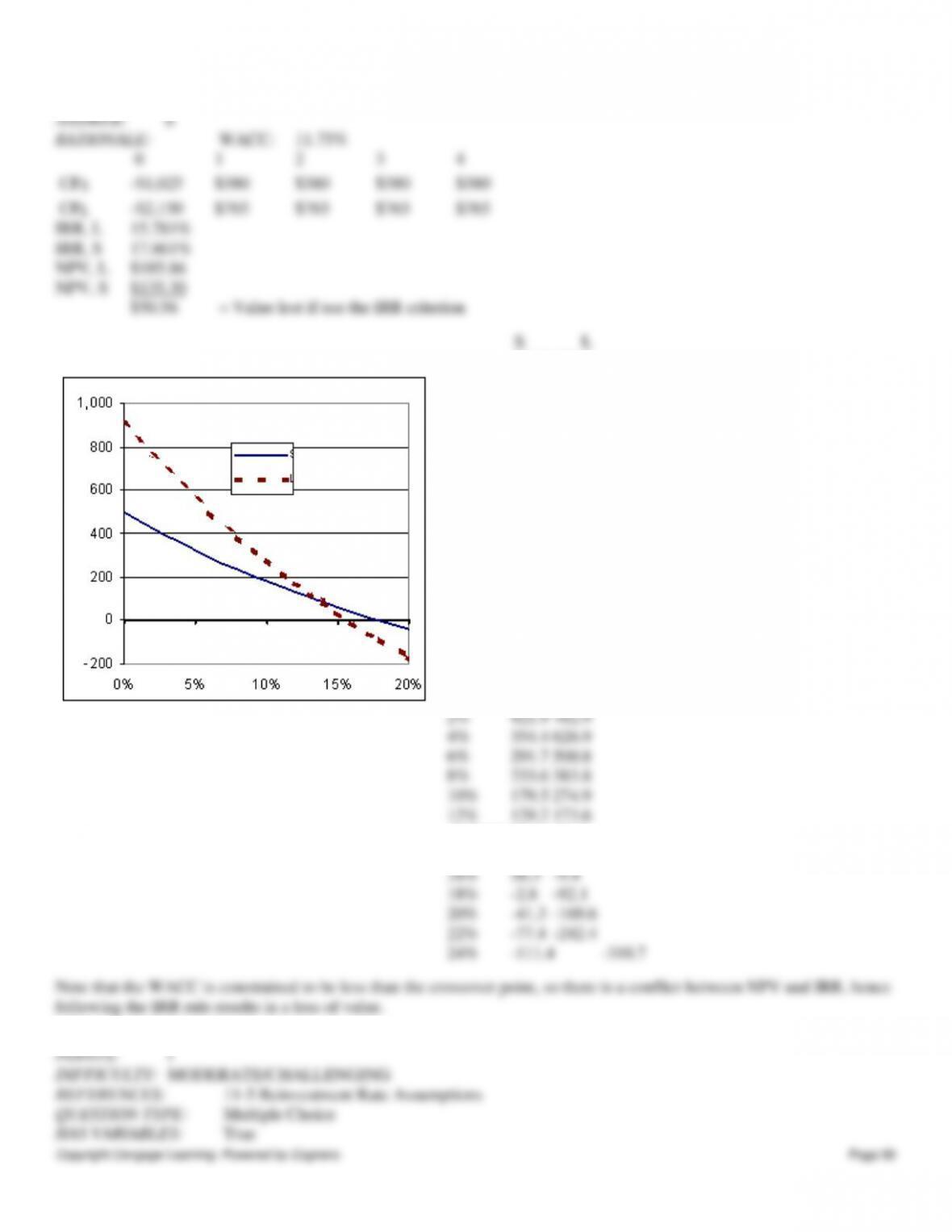

WACC: 8.75%

0 1 2 3 4

CFS -$1,100 $550 $600 $100 $100

CFL -$2,700 $650 $725 $800 $1,400

a. $79.93

b. $70.65

c. $71.36

d. $88.49

Chapter 11: The Basics of Capital Budgeting

Copyright Cengage Learning. Powered by Cognero.

Page 57

e. $68.51

102. A firm is considering Projects S and L, whose cash flows are shown below. These projects are mutually exclusive,

equally risky, and not repeatable. The CEO wants to use the IRR criterion, while the CFO favors the NPV method. You

were hired to advise the firm on the best procedure. If the wrong decision criterion is used, how much potential value

would the firm lose?

WACC: 11.75%

0 1 2 3 4

CFS -$1,025 $380 $380 $380 $380

CFL -$2,150 $765 $765 $765 $765

a. $45.51

b. $50.56

c. $62.70

d. $57.64

Chapter 11: The Basics of Capital Budgeting

Copyright Cengage Learning. Powered by Cognero.

Page 58

e. $45.00

135.3 185.9

0% 495.0 910.0

13.860% 85.4 85.4

14% 82.2 79.0

Copyright Cengage Learning. Powered by Cognero.

Page 60

104. Moerdyk & Co. is considering Projects S and L, whose cash flows are shown below. These projects are mutually

exclusive, equally risky, and not repeatable. If the decision is made by choosing the project with the higher IRR, how

much value will be forgone? Note that under certain conditions choosing projects on the basis of the IRR will not cause

any value to be lost because the one with the higher IRR will also have the higher NPV, i.e., no conflict will exist.

WACC: 7.75%

0 1 2 3 4

CFS -$1,025 $650 $450 $250 $50

CFL -$1,025 $100 $300 $500 $700

a. $35.63

b. $42.42

c. $40.30

d. $50.06

e. $52.18

Copyright Cengage Learning. Powered by Cognero.

Page 62

106. Nast Inc. is considering Projects S and L, whose cash flows are shown below. These projects are mutually exclusive,

equally risky, and not repeatable. If the decision is made by choosing the project with the higher MIRR rather than the one

with the higher NPV, how much value will be forgone? Note that under some conditions choosing projects on the basis of

the MIRR will cause $0.00 value to be lost.

WACC: 9.00%

0 1 2 3 4

CFS -$1,100 $375 $375 $375 $375

CFL -$2,200 $725 $725 $725 $725

a. $34.24

b. $26.78

c. $33.90

d. $27.80

e. $25.77

485.64 445.54 408.75 375.00 $1,714.92 11.74%

938.90 861.37 790.25 725.00 $3,315.52 10.80%

MIRR, L 10.80%

MIRR, S 11.74%

107. Yonan Inc. is considering Projects S and L, whose cash flows are shown below. These projects are mutually

exclusive, equally risky, and not repeatable. If the decision is made by choosing the project with the shorter payback,

Chapter 11: The Basics of Capital Budgeting

Copyright Cengage Learning. Powered by Cognero.

Page 63

some value may be forgone. How much value will be lost in this instance? Note that under some conditions choosing

projects on the basis of the shorter payback will not cause value to be lost.

WACC: 10.00%

0 1 2 3 4

CFS -$950 $500 $800 $0 $0

CFL -$2,100 $400 $800 $800 $1,000

a. $35.82

b. $43.16

c. $53.08

d. $51.36

e. $38.41

108. Noe Drilling Inc. is considering Projects S and L, whose cash flows are shown below. These projects are mutually

exclusive, equally risky, and not repeatable. The CEO believes the IRR is the best selection criterion, while the CFO

advocates the MIRR. If the decision is made by choosing the project with the higher IRR rather than the one with the

higher MIRR, how much, if any, value will be forgone, i.e., what’s the NPV of the chosen project versus the maximum

possible NPV? Note that (1) “true value” is measured by NPV, and (2) under some conditions the choice of IRR vs. MIRR

will have no effect on the value lost.

WACC: 9.00%

Chapter 11: The Basics of Capital Budgeting

Copyright Cengage Learning. Powered by Cognero.

Page 64

0 1 2 3 4

CFS -$1,100 $550 $600 $100 $100

CFL -$2,750 $725 $725 $800 $1,400

a. $92.69

b. $62.57

c. $0.00

d. $95.01

e. $78.79

0.0882%