Chapter 09 – Long-Term Assets: Fixed and Intangible

(c)

Accumulated Depreciation—Machinery

8,000

Cash

8,000

POINTS:

1

DIFFICULTY:

Moderate

Bloom’s: Remembering

QUESTION TYPE:

Subjective Short Answer

HAS VARIABLES:

False

LEARNING OBJECTIVES:

FNMN.WAJO.19.09–01 – LO: 09–01

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.13 – Long-term Assets Reporting

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

DATE CREATED:

7/22/2017 6:24 PM

DATE MODIFIED:

10/16/2017 5:33 PM

178. On April 15, Compton Co. paid $2,800 to upgrade a delivery truck and $125 for an oil change. Journalize the entries

for the upgrade to delivery truck and oil change expenditures.

ANSWER:

April 15

Delivery Truck

2,800

Cash

2,800

15

Repairs and Maintenance Expense

125

Cash

125

POINTS:

1

DIFFICULTY:

Bloom’s: Remembering

Easy

QUESTION TYPE:

Subjective Short Answer

HAS VARIABLES:

False

LEARNING OBJECTIVES:

FNMN.WAJO.19.09–02 – LO: 09–02

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.13 – Long-term Assets Reporting

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

DATE CREATED:

7/22/2017 6:24 PM

DATE MODIFIED:

10/16/2017 5:33 PM

179. XYZ Co. incurred the following costs related to the office building used in operating its sports supply company:

(a)

Replaced a broken window.

(b)

Replaced the roof that had been on the building 23 years.

(c)

Serviced all the air conditioners before summer started.

(d)

Replaced the air conditioners in the customer service areas.

(e)

Added a warehouse to the back of the building.

(f)

Repainted the interior walls.

(g)

Installed window shutters on all windows.

Classify each of the costs as a capital expenditure or a revenue expenditure.

ANSWER:

(a) Revenue expenditure

(b) Capital expenditure

(c) Revenue expenditure

(d) Capital expenditure

(e) Capital expenditure

Copyright Cengage Learning. Powered by Cognero.

Page 63

182. The double-declining-balance rate for calculating depreciation expense is determined by doubling the straight-line

rate. Assuming that an asset has a useful life of 25 years, determine the rate to be used if using the double-declining-

balance method.

ANSWER:

4% × 2 = 8%

POINTS:

1

DIFFICULTY:

Easy

Bloom’s: Applying

QUESTION TYPE:

Subjective Short Answer

HAS VARIABLES:

False

LEARNING OBJECTIVES:

FNMN.WAJO.19.09–02 – LO: 09–02

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.13 – Long-term Assets Reporting

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

DATE CREATED:

7/22/2017 6:24 PM

DATE MODIFIED:

10/16/2017 5:33 PM

183. Copy equipment was acquired at the beginning of the year at a cost of $72,000 that has an estimated residual value of

$9,000 and an estimated useful life of 5 years. It is estimated that the machine will output an estimated 1,000,000

copies. This year, 315,000 copies were made. Determine the (a) depreciable cost, (b) depreciation rate, and (c) the units-

of-output depreciation for the year.

ANSWER:

(a)

$63,000 (Initial cost – Estimated residual value = $72,000 – $9000)

(b)

$0.063 per copy (Depreciable cost / Total units of output = $63,000 / 1,000,000

copies)

(c)

$19,845 (315,000 copies × $0.063)

POINTS:

1

DIFFICULTY:

Moderate

Bloom’s: Applying

QUESTION TYPE:

Subjective Short Answer

HAS VARIABLES:

False

LEARNING OBJECTIVES:

FNMN.WAJO.19.09–02 – LO: 09–02

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.13 – Long-term Assets Reporting

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

DATE CREATED:

7/22/2017 6:24 PM

DATE MODIFIED:

10/16/2017 5:33 PM

184. A machine costing $57,000 with a 6-year life and $54,000 depreciable cost was purchased January 1. Compute the

yearly depreciation expense using straight-line depreciation.

ANSWER:

$54,000 ÷ 6 years = $9,000 per year

POINTS:

1

DIFFICULTY:

Easy

Bloom’s: Applying

QUESTION TYPE:

Subjective Short Answer

HAS VARIABLES:

False

LEARNING OBJECTIVES:

FNMN.WAJO.19.09–02 – LO: 09–02

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.13 – Long-term Assets Reporting

Chapter 09 – Long-Term Assets: Fixed and Intangible

(b)

Depreciation Expense—Trucks

(e)

25 years

(f)

40 years

(g)

50 years

ANSWER:

(a) 50% (1/2)

(b) 12.5% (1/8)

(c) 10% (1/10)

(d) 5% (1/20)

(e) 4% (1/25)

(f) 2.5% (1/40)

(g) 2% (1/50)

POINTS:

1

DIFFICULTY:

Easy

Bloom’s: Applying

QUESTION TYPE:

Subjective Short Answer

HAS VARIABLES:

False

LEARNING OBJECTIVES:

FNMN.WAJO.19.09–02 – LO: 09–02

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.13 – Long-term Assets Reporting

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

DATE CREATED:

7/22/2017 6:24 PM

DATE MODIFIED:

10/16/2017 5:33 PM

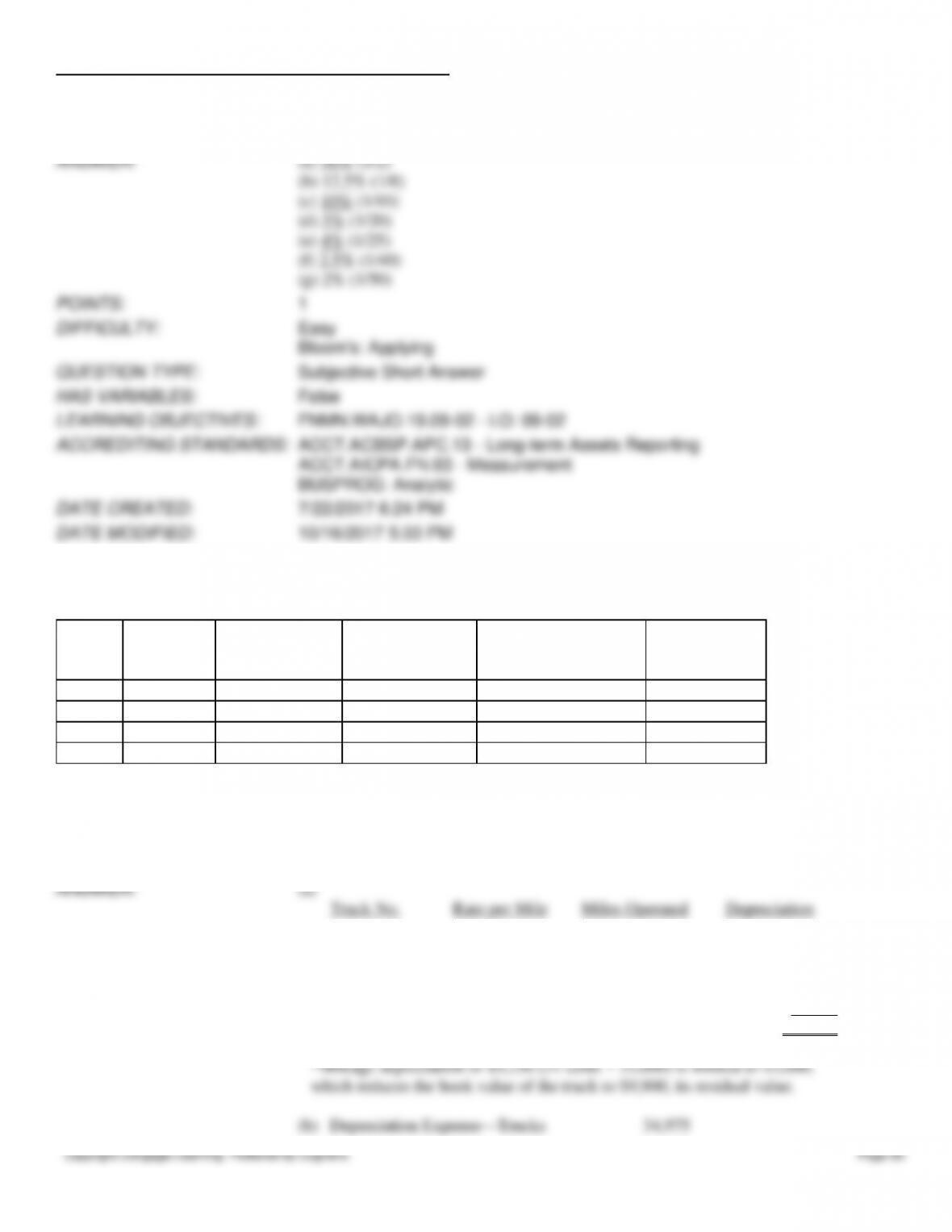

188. Prior to adjustment at the end of the year, the balance in Trucks is $300,900 and the balance in Accumulated

Depreciation—Trucks is $88,200. Details of the subsidiary ledger are as follows:

Truck

No.

Cost

Estimated

Residual Value

Estimated Useful

Life

Accumulated

Depreciation at

Beginning of Year

Miles Operated

During Year

1

$100,000

$13,000

300,000

—

30,000

2

72,900

9,900

300,000

$60,000

25,000

3

38,000

3,000

200,000

8,050

45,000

4

90,000

13,000

200,000

20,150

40,000

Required:

(a)

Based on the units-of-output method, determine the depreciation rates per mile and the

amount to be credited to the accumulated depreciation section of each of the subsidiary

accounts for the miles operated during the current year.

(b)

Journalize the entry to record depreciation for the year.

ANSWER:

(a)

Truck No.

Rate per Mile

Miles Operated

Depreciation

1

29.0 cents

30,000

$ 8,700

2

21.0

25,000

3,000*

3

17.5

45,000

4

38.5

40,000

15,400

Chapter 09 – Long-Term Assets: Fixed and Intangible

Copyright Cengage Learning. Powered by Cognero.

Page 68

(a)

straight-line

(b)

double-declining-balance

(c)

units-of-output (used for 1,600 hours during the current year)

ANSWER:

(a)

$28,125 [($240,000 – $15,000) ÷ 4 × 6/12]

(b)

$60,000 ($240,000 × 0.50 × 6/12)

(c)

$14,400 [($240,000 – $15,000) ÷ 25,000 hours × 1,600 hours]

POINTS:

1

DIFFICULTY:

Challenging

Bloom’s: Applying

QUESTION TYPE:

Subjective Short Answer

HAS VARIABLES:

False

LEARNING OBJECTIVES:

FNMN.WAJO.19.09–02 – LO: 09–02

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.13 – Long-term Assets Reporting

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

DATE CREATED:

7/22/2017 6:24 PM

DATE MODIFIED:

10/16/2017 5:33 PM

193. Determine the depreciation, for the year of acquisition and for the following year of a fixed asset acquired on

October 1 for $500,000, with an estimated life of 5 years, and residual value of $50,000, using (a) the double declining-

balance method and (b) the straight-line method. Assume a fiscal year ending December 31.

ANSWER:

(a)

Year of acquisition: $50,000 ($500,000 × 0.40 × 3/12)

Following year: $180,000 ($500,000 – $50,000 × 0.40)

(b)

Year of acquisition: $22,500 [($500,000 – $50,000 / 5) × 3/12]

Following year: $90,000 [($500,000 – $50,000) / 5]

POINTS:

1

DIFFICULTY:

Moderate

Bloom’s: Applying

QUESTION TYPE:

Subjective Short Answer

HAS VARIABLES:

False

LEARNING OBJECTIVES:

FNMN.WAJO.19.09–02 – LO: 09–02

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.13 – Long-term Assets Reporting

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

DATE CREATED:

7/22/2017 6:24 PM

DATE MODIFIED:

10/16/2017 5:33 PM

194. Equipment costing $80,000 with a useful life of 10 years and a residual value of $8,000 has been depreciated for 6

years by the straight-line method. Assume a fiscal year ending December 31.

(a)

What is the book value at the end of the sixth year of use?

(b)

If early in the seventh year it is estimated that the remaining useful life is 5 years

(instead of 4) and the residual value is $6,000, what is the amount of depreciation for

the seventh year?

ANSWER:

(a)

($80,000 – $8,000) = $72,000

$72,000 / 10 = $7,200

$7,200 × 6 = $43,200

$80,000 – $43,200 = $36,800