Chapter 07 – Internal Control and Cash

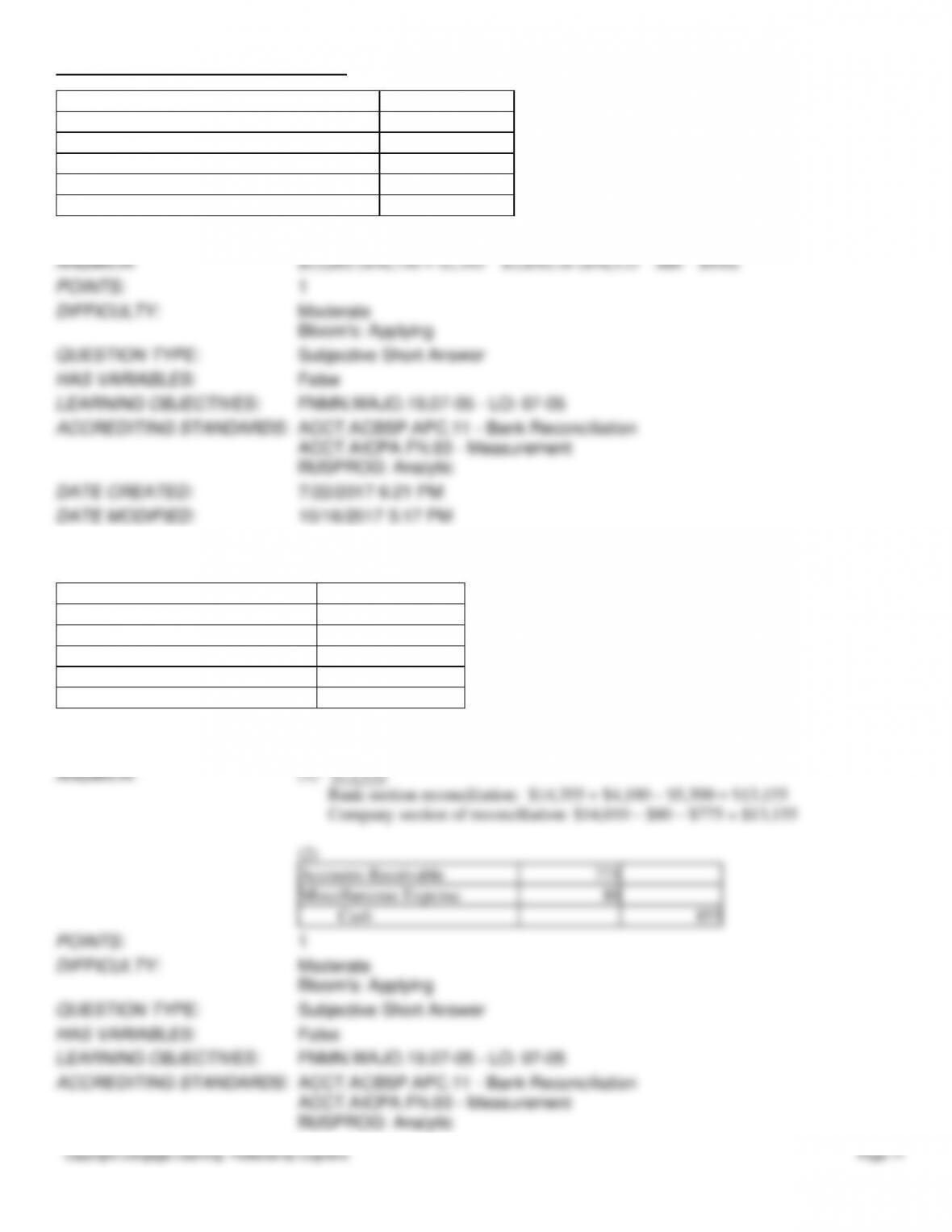

Balance per bank

$16,750

Balance per company records

16,125

Bank service charges

80

Deposit in transit

2,195

NSF check

950

Outstanding checks

3,850

What is the adjusted balance on the bank reconciliation?

ANSWER:

$15,095 ($16,750 + $2,195 – $3,850) or ($16,125 – $80 – $950)

POINTS:

1

DIFFICULTY:

Moderate

Bloom’s: Applying

QUESTION TYPE:

Subjective Short Answer

HAS VARIABLES:

False

LEARNING OBJECTIVES:

FNMN.WAJO.19.07-05 – LO: 07–05

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.11 – Bank Reconciliation

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

DATE CREATED:

7/22/2017 6:21 PM

DATE MODIFIED:

10/16/2017 5:17 PM

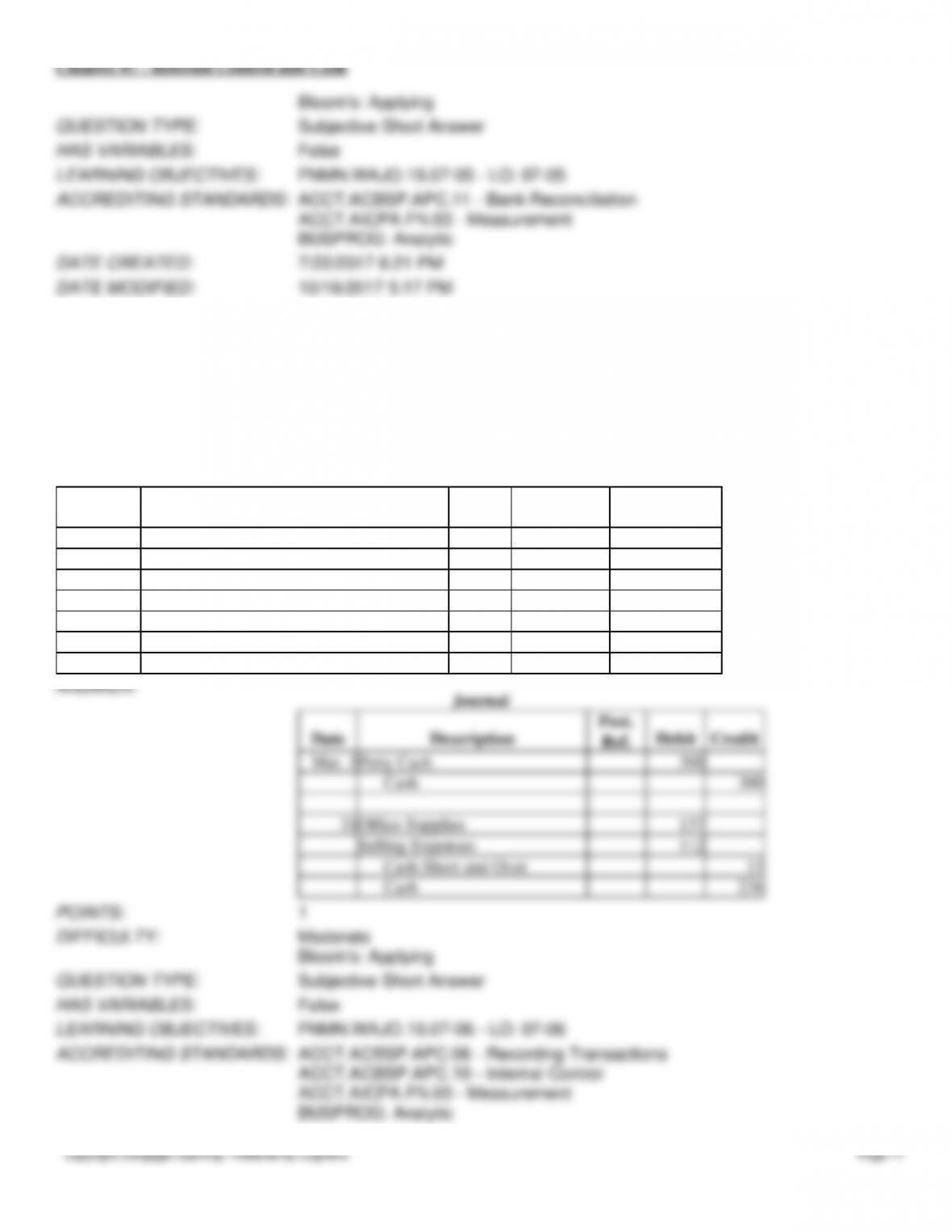

167. The following data were gathered to use in reconciling the bank statement of Build-A-Lot:

Balance per bank

$14,355

Balance per company records

14,010

Bank service charges

80

Deposits in transit

4,100

NSF checks

775

Outstanding checks

5,300

(1) What is the adjusted balance on the bank reconciliation?

(2) Journalize any necessary entries for Build-A-Lot based on the bank reconciliation.

ANSWER:

(1) $13,155

Bank section reconciliation: $14,355 + $4,100 – $5,300 = $13,155

Company section of reconciliation: $14,010 – $80 – $775 = $13,155

(2)

Accounts Receivable

775

Miscellaneous Expense

80

Cash

855

POINTS:

1

DIFFICULTY:

Moderate

Bloom’s: Applying

QUESTION TYPE:

Subjective Short Answer

HAS VARIABLES:

False

LEARNING OBJECTIVES:

FNMN.WAJO.19.07-05 – LO: 07–05

Chapter 07 – Internal Control and Cash

May 31

Cash

Note Receivable

Interest Revenue

31

Accounts Payable

Miscellaneous Expense

Accounts Receivable

Cash

had been posted, the cash account had a balance of $8,998.

ANSWER:

(a)

Santiago Co.

Bank Reconciliation

May 31

Cash balance according to bank statement

$25,645

Adjustments:

Deposits not recorded by bank

$3,796

Outstanding checks

(5,975)

Total adjustments

(2,179)

Adjusted balance

$23,466

Cash balance according to company’s records

$20,915

Adjustments:

Proceeds of note and interest collected by bank

$4,515

Error in recording check

(1,000)

Bank service charges

(70)

Nonsufficient funds check

(894)

Total adjustments

2,551

Adjusted balance

$23,466

Chapter 07 – Internal Control and Cash

Copyright Cengage Learning. Powered by Cognero.

Page 76

(a)

Cash sales of $945 had been erroneously recorded in the cash receipts journal as $495.

(b)

Deposits in transit not recorded by bank, $778.

(c)

Bank debit memo for service charges, $40.

(d)

Bank credit memo for note collected by bank, $23,985 plus $885 interest.

(e)

Bank debit memo for $756 NSF (not sufficient funds) check from Calin Sams, a customer.

(f)

Checks outstanding, $1,860.

Record the appropriate journal entries that would be necessary for Jeffrey Co.

ANSWER:

Cash

25,320

Notes Receivable

23,985

Interest Revenue

885

Sales

450

Accounts Receivable—Calin Sams

756

Miscellaneous Expense

40

Cash

796

POINTS:

1

DIFFICULTY:

Moderate

Bloom’s: Applying

QUESTION TYPE:

Subjective Short Answer

HAS VARIABLES:

False

LEARNING OBJECTIVES:

FNMN.WAJO.19.07-05 – LO: 07–05

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.11 – Bank Reconciliation

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

DATE CREATED:

7/22/2017 6:21 PM

DATE MODIFIED:

10/16/2017 5:17 PM

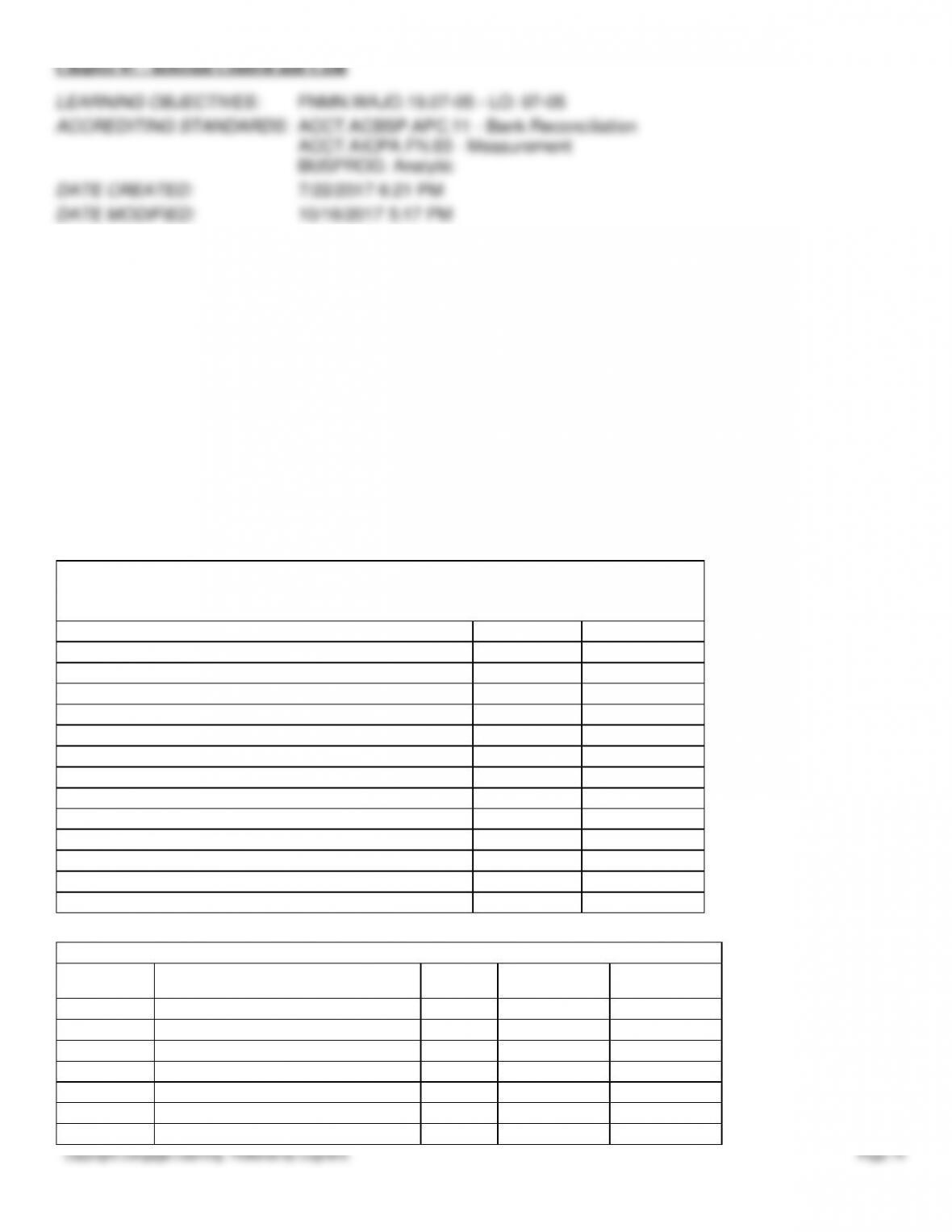

172. The bank statement for Gatlin Co. indicates a balance of $7,735 on June 30. After the journal entries for June had

been posted, the cash account had a balance of $4,098.

(a)

Cash sales of $742 had been erroneously recorded in the cash receipts journal as $724.

(b)

Deposits in transit not recorded by bank, $425.

(c)

Bank debit memo for service charges, $35.

(d)

Bank credit memo for note collected by bank, $2,475 including $75 interest.

(e)

Bank debit memo for $256 NSF (not sufficient funds) check from Janice Smith, a customer.

(f)

Checks outstanding, $1,860.

Record the appropriate journal entries that would be necessary for Gatlin Co.

ANSWER:

Cash

2,493

Notes Receivable

2,400

Interest Revenue

75

Sales

18

Accounts Receivable—Janice Smith

256

Miscellaneous Expense

35

Cash

291

POINTS:

1

DIFFICULTY:

Moderate