Chapter 07 – Internal Control and Cash

Copyright Cengage Learning. Powered by Cognero.

Page 51

DIFFICULTY:

Moderate

Difficulty: Moderate

Bloom’s: Remembering

QUESTION TYPE:

Matching

HAS VARIABLES:

False

LEARNING OBJECTIVES:

FNMN.WAJO.19.07-05 – LO: 07–05

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.11 – Bank Reconciliation

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

DATE CREATED:

7/22/2017 6:21 PM

DATE MODIFIED:

10/16/2017 5:17 PM

131. outstanding checks

ANSWER:

d

POINTS:

1

132. bank service charge

ANSWER:

b

POINTS:

1

133. deposit in transit

ANSWER:

c

POINTS:

1

134. NSF check

ANSWER:

b

POINTS:

1

135. EFT deposit from a customer

ANSWER:

a

POINTS:

1

136. charges for some other company’s safe deposit box were posted to your account

ANSWER:

c

POINTS:

1

137. a $1,000 note from one of your customers was collected by the bank

ANSWER:

a

POINTS:

1

138. interest revenue earned by the note above

ANSWER:

a

POINTS:

1

139. Identify each of the following as relating to (a) the control environment, (b) risk assessment, or (c) control

procedures.

1. Mandatory vacations

2. Personnel policies

Copyright Cengage Learning. Powered by Cognero.

Page 52

3. Report of outside consultants on future market changes

ANSWER:

1. (c) control procedures

2. (a) the control environment

3. (b) risk assessment

POINTS:

1

DIFFICULTY:

Easy

Bloom’s: Remembering

QUESTION TYPE:

Subjective Short Answer

HAS VARIABLES:

False

LEARNING OBJECTIVES:

FNMN.WAJO.19.07-02 – LO: 07–02

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.10 – Internal Control

ACCT.AICPA.BB.01 – Industry

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

DATE CREATED:

7/22/2017 6:21 PM

DATE MODIFIED:

10/16/2017 5:17 PM

140. List the objectives of internal control and give an example of how each is implemented.

ANSWER:

Internal control provides reasonable assurance that

(1)

assets are safeguarded and used for business purposes

(2)

business information is accurate

(3)

employees and managers comply with laws and regulations

Examples are

(1)

duties are separated

(2)

duties are rotated

(3)

reports are submitted to management

There are many other examples that would be correct.

POINTS:

1

DIFFICULTY:

Easy

Bloom’s: Understanding

QUESTION TYPE:

Subjective Short Answer

HAS VARIABLES:

False

LEARNING OBJECTIVES:

FNMN.WAJO.19.07-02 – LO: 07–02

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.10 – Internal Control

ACCT.AICPA.BB.01 – Industry

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

DATE CREATED:

7/22/2017 6:21 PM

DATE MODIFIED:

10/16/2017 5:17 PM

141. You began your new job as the accountant at Bolivar Industries during the month of December. During your first

month, you found several interesting issues.

1) While looking through the invoices, you found Invoices 213–242, 245–271, and 275–290. It appears that invoices

243, 244, 272, 273, and 274 are missing.

2) During the month, Clerk # 3 issued $250 in refunds as compared to Clerks #1, #2, and #4 who issued less than

$50 each.

3) The daily cash receipts and bank deposits reconcile, except on Tuesdays during the month.

Chapter 07 – Internal Control and Cash

DATE MODIFIED:

10/16/2017 5:17 PM

4) Business is generally brisk during the holiday season, but two weeks before Christmas there was a sudden

increase in slow payments.

Part A: What kind of warning signs could be associated with these issues?

Part B: What control could you put in place regarding cash refunds mentioned in Part A (2)?

ANSWER:

Part A:

1) Missing invoices or gaps in transaction numbers could mean that the invoices

are being used for fraudulent transactions.

2) An unusually high number of refunds for Clerk #3 could mean that the

individual is creating fictitious refunds and pocketing the cash.

3) The difference could mean that receipts are being pocketed before being

deposited. Maybe there is a person responsible for making the deposits on

Tuesdays that is the culprit.

4) A sudden increase in slow payments could mean that an employee is

pocketing the payments.

Part B:

Surveillance cameras at customer service area.

Place supervisor as a second authorizer on refund transactions.

Prohibit cash refunds and require exchanges of merchandise instead.

Provide employee training.

Incorporate special alerts for critical dollar thresholds through company software.

Require information about the original transaction to be part of the refund process.

POINTS:

1

DIFFICULTY:

Challenging

Bloom’s: Analyzing

QUESTION TYPE:

Subjective Short Answer

HAS VARIABLES:

False

LEARNING OBJECTIVES:

FNMN.WAJO.19.07-02 – LO: 07–02

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.10 – Internal Control

ACCT.AICPA.BB.01 – Industry

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

DATE CREATED:

7/22/2017 6:21 PM

Chapter 07 – Internal Control and Cash

(4)

Monitoring. Monitoring locates deficiencies in the internal control

system and improves control effectiveness.

POINTS:

1

Bloom’s: Understanding

(3)

A bill for services rendered to Cole Co. was erroneously posted to the account of

Coleman Co. in the customer‘s ledger.

(4)

No entry was made in the accounting records for services rendered to a customer.

(b)

Both cash and credit charges for services rendered are recorded on prenumbered invoices.

At the end of the day, all invoices are accounted for before the duplicate copies of the

invoices are routed to the accounting department for entry into the accounts and the cash is

sent to the cashier‘s department for deposit.

(1)

Some charge customers complained that the monthly statements of account did not

add all amounts correctly.

(2)

Some clerks used incorrect hourly rates in preparing invoices.

(3)

Some clerks destroyed duplicate copies of cash invoices and misappropriated the

cash.

(4)

Some charge customers complained that the monthly statement of account did not

indicate credits for payments made.

ANSWER:

(a)

(2)

(b)

(3)

POINTS:

1

DIFFICULTY:

Moderate

Bloom’s: Understanding

QUESTION TYPE:

Subjective Short Answer

HAS VARIABLES:

False

LEARNING OBJECTIVES:

FNMN.WAJO.19.07-02 – LO: 07–02

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.10 – Internal Control

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

DATE CREATED:

7/22/2017 6:21 PM

DATE MODIFIED:

10/16/2017 5:17 PM

143. List and define each of the five elements of internal control.

ANSWER:

(1)

Control Environment. The control environment is the overall attitude

of management and employees about the importance of internal

controls.

(2)

Risk assessment. Risk assessment is the identification of risks faced

by an organization so that management can take necessary actions to

control them.

(3)

Control Procedures. The control procedures are the policies and

procedures designed to provide reasonable assurance that the business

goals are met and fraud is prevented.

Chapter 07 – Internal Control and Cash

DATE CREATED:

7/22/2017 6:21 PM

DATE MODIFIED:

10/16/2017 5:17 PM

(a) At the end of the day, cash register clerks are required to use their own funds to make up any cash shortages

in their registers.

(b) At the end of the day, an accounting clerk compares the duplicate copy of the daily cash deposit slip with the

deposit receipt obtained from the bank.

(c) After necessary approvals have been obtained for the payment of a voucher, the treasurer signs and mails the

check. The treasurer then stamps the voucher and supporting documentation as paid and returns the voucher

and supporting documentation to the accounts payable clerk for filing.

(d) Along with the petty cash receipts for postage, office supplies, etc., several postdated employee

checks are in the petty cash fund.

ANSWER:

(a) This is a weakness. Requiring cash register clerks to make up any cash

shortages from their own funds gives the clerks an incentive to shortchange

customers. That is, the clerks will want to make sure that they don’t have a

shortage at the end of the day. In addition, one might also assume that the

clerks can keep any overages. This would again encourage clerks to

shortchange customers. The shortchanging of customers will create customer

complaints, etc.

The best policy is to report any cash shortages or overages at

the end of each day. If there is consistently a cash short or over, then

corrective action (training, removal, etc.) could be taken.

(b) This is a strength.

(c) This is a strength.

(d) This is a weakness. Employees should not be allowed to use the petty cash

fund to cash personal checks. In any case, postdated checks should not be

accepted. In effect, postdated checks represent a receivable from the

employees.

POINTS:

1

DIFFICULTY:

Moderate

Bloom’s: Analyzing

QUESTION TYPE:

Subjective Short Answer

HAS VARIABLES:

False

LEARNING OBJECTIVES:

FNMN.WAJO.19.07-02 – LO: 07–02

FNMN.WAJO.19.07-03 – LO: 07–03

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.10 – Internal Control

ACCT.AICPA.BB.01 – Industry

Copyright Cengage Learning. Powered by Cognero.

Page 58

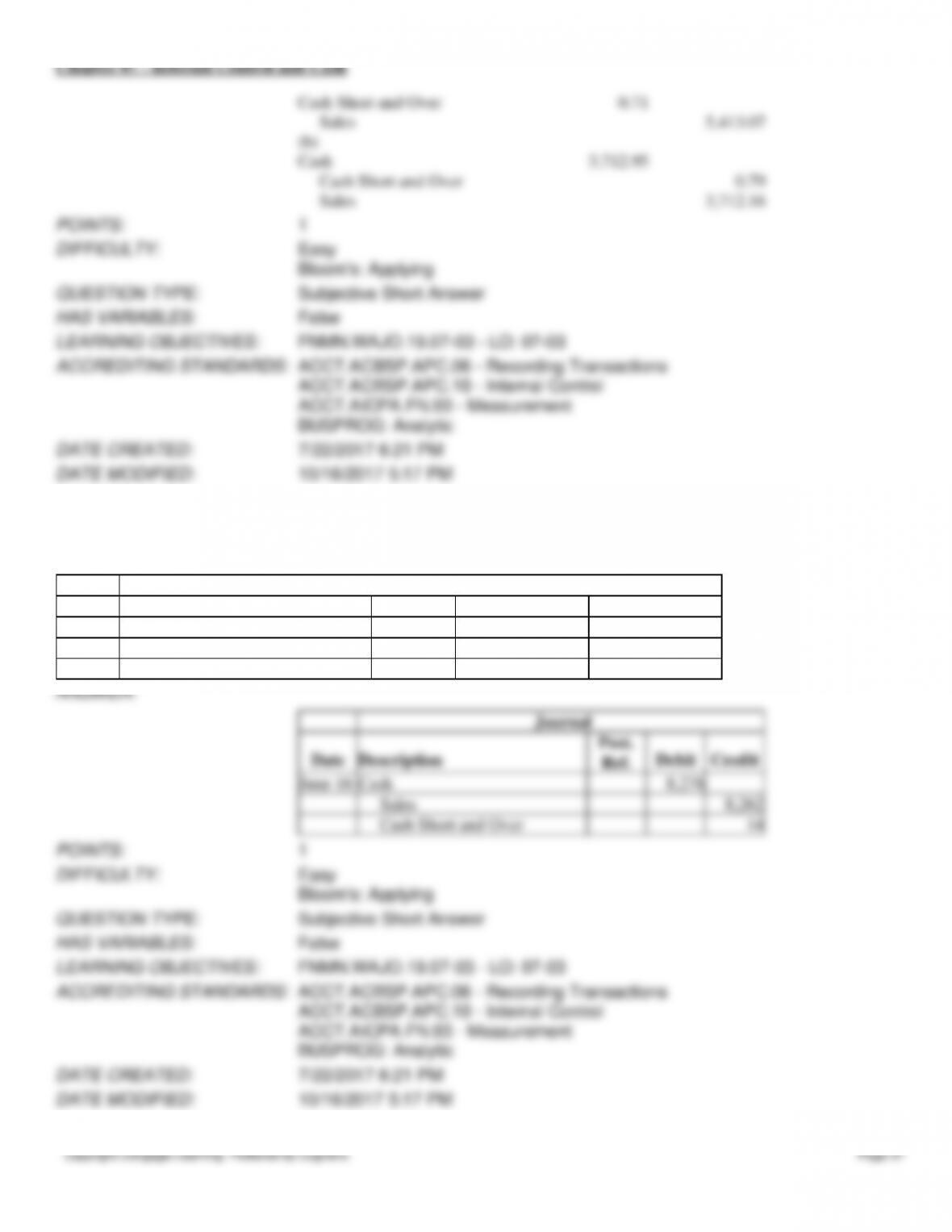

148. The actual cash received during the week ended October 31 for cash sales was $23,447 and the amount indicated by

the cash register total was $23,457. Journalize the entry to record the cash receipts and cash sales.

Journal

Date

Description

Post. Ref.

Debit

Credit

ANSWER:

Journal

Date

Description

Post. Ref.

Debit

Credit

Oct. 31

Cash

23,447

Cash Short and Over

10

Sales

23,457

POINTS:

1

DIFFICULTY:

Easy

Bloom’s: Applying

QUESTION TYPE:

Subjective Short Answer

HAS VARIABLES:

False

LEARNING OBJECTIVES:

FNMN.WAJO.19.07-03 – LO: 07–03

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.06 – Recording Transactions

ACCT.ACBSP.APC.10 – Internal Control

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

DATE CREATED:

7/22/2017 6:21 PM

DATE MODIFIED:

10/16/2017 5:17 PM

149. Consider the following information from the cash account. Assume cash payments were 84% of collections.

Cash

??

Beg. balance

$245,000

Collections

??

Disbursements

$80,275

End balance

How much was the beginning balance of the cash account?

ANSWER:

$245,000 × 84% = $205,800

Beg. Cash = $41,075 ($80,275 + $205,800 – $245,000)

POINTS:

1

DIFFICULTY:

Bloom’s: Applying

Easy

QUESTION TYPE:

Subjective Short Answer

HAS VARIABLES:

False

LEARNING OBJECTIVES:

FNMN.WAJO.19.07-04 – LO: 07–04

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.06 – Recording Transactions

ACCT.ACBSP.APC.15 – Current Assets Reporting

ACCT.AICPA.BB.01 – Industry

ACCT.AICPA.FN.03 – Measurement