Chapter 06 – Inventories

Copyright Cengage Learning. Powered by Cognero.

Page 81

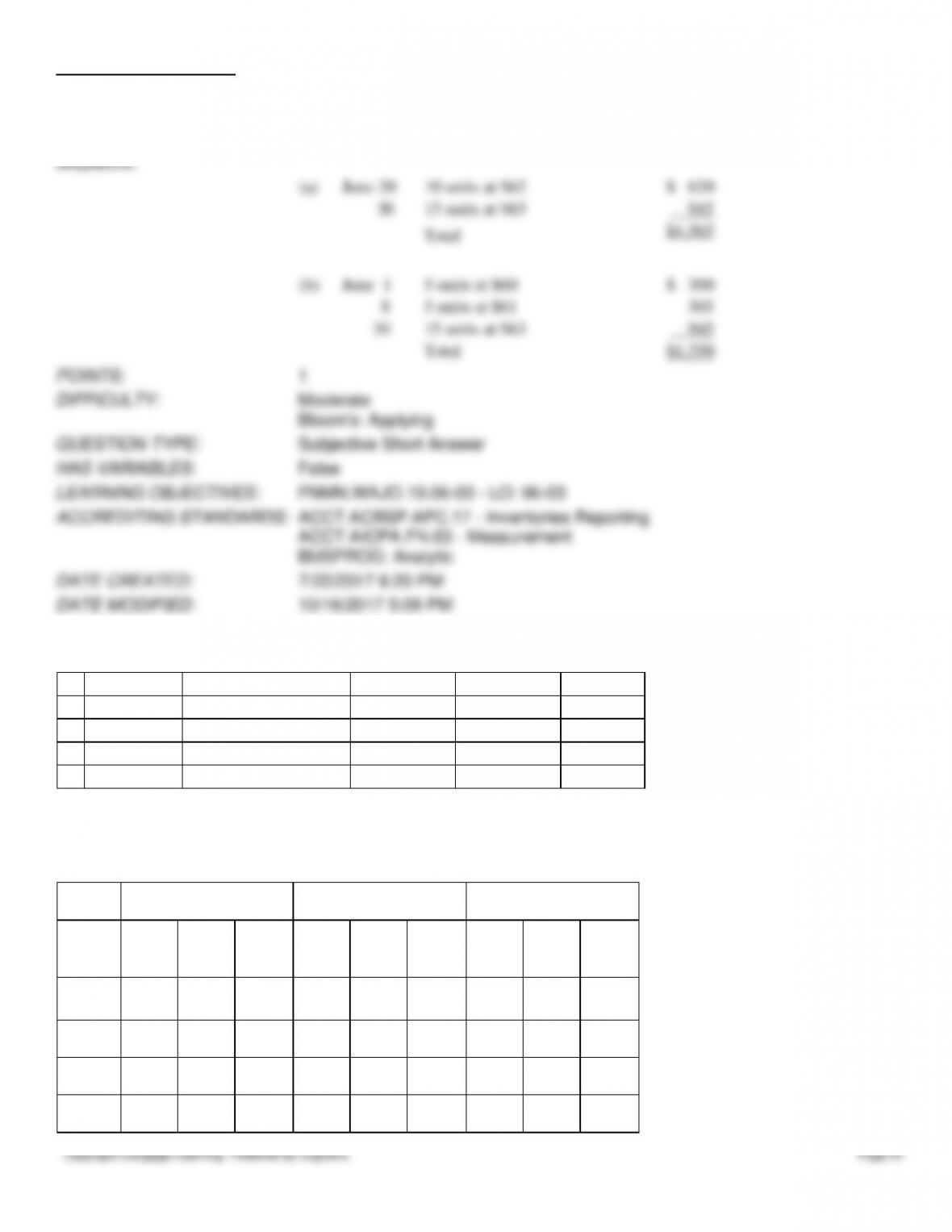

Calculate the cost of the ending inventory at June 30, using (a) the first-in, first-out (FIFO)

method and (b) the last-in, first-out (LIFO) method. Identify the quantity, unit price, and

total cost of each lot in the inventory.

ANSWER:

(a)

June 20

10 units at $62

$ 620

30

15 units at $63

945

Total

$1,565

(b)

June 1

5 units at $60

$ 300

8

5 units at $61

305

30

15 units at $63

945

Total

$1,550

POINTS:

1

DIFFICULTY:

Moderate

Bloom’s: Applying

QUESTION TYPE:

Subjective Short Answer

HAS VARIABLES:

False

LEARNING OBJECTIVES:

FNMN.WAJO.19.06-03 – LO: 06–03

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.17 – Inventories Reporting

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

DATE CREATED:

7/22/2017 6:20 PM

DATE MODIFIED:

10/16/2017 5:09 PM

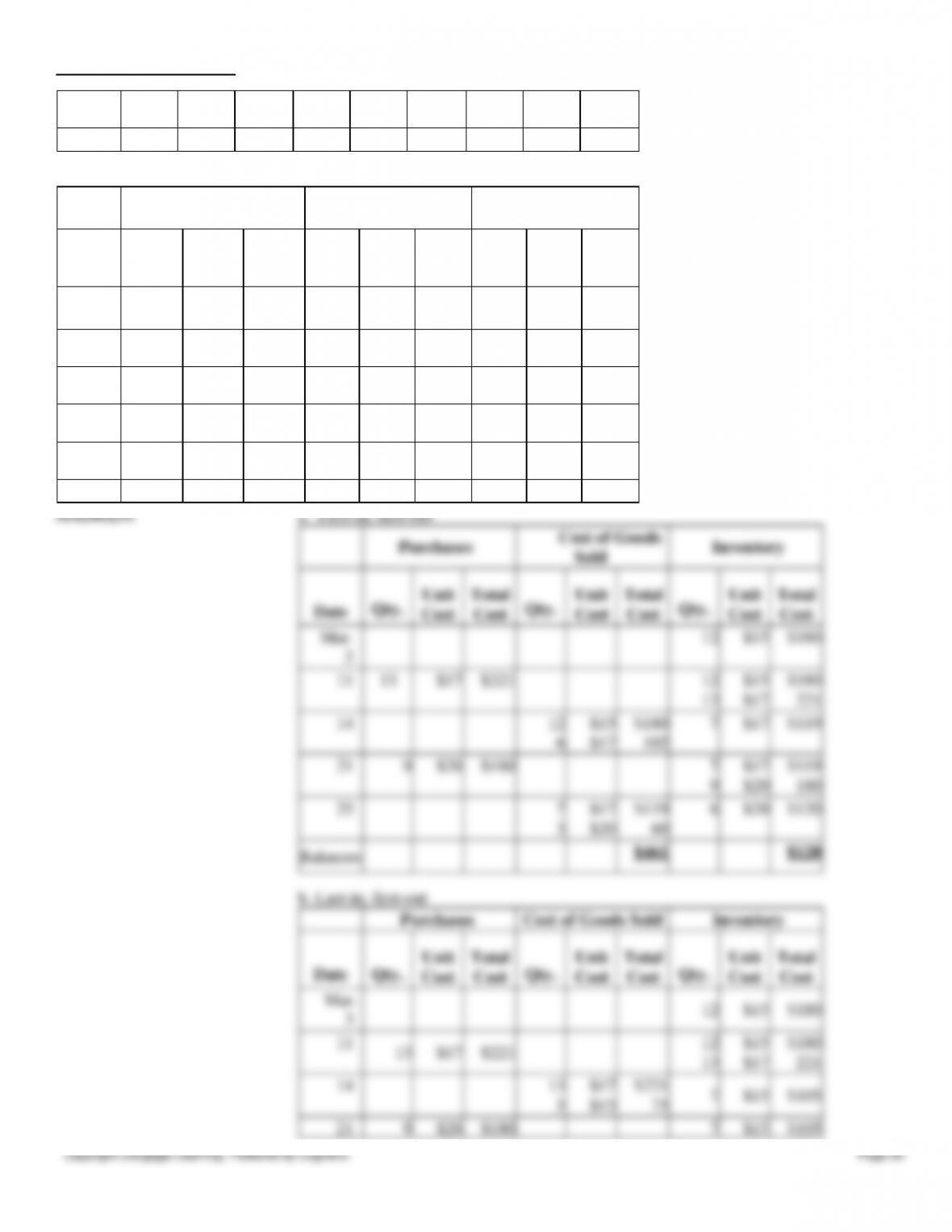

190. Beginning inventory, purchases, and sales data for hammers are as follows:

Mar. 3

Inventory

12 units

@

$15

11

Purchase

13 units

@

$17

14

Sale

18 units

21

Purchase

9 units

@

$20

25

Sale

10 units

Assuming the business maintains a perpetual inventory system, complete the inventory cards and calculate the cost of

goods sold and ending inventory under the following assumptions:

(a) First-in, first-out

Purchases

Cost of Goods Sold

Inventory

Date

Qty.

Unit

Cost

Total

Cost

Qty.

Unit

Cost

Total

Cost

Qty.

Unit

Cost

Total

Cost

Mar.

3

14

21

Chapter 06 – Inventories

25

Balances

(b) Last-in, first-out

Purchases

Cost of Goods Sold

Inventory

Date

Qty.

Unit

Cost

Total

Cost

Qty.

Unit

Cost

Total

Cost

Qty.

Unit

Cost

Total

Cost

Mar.

3

11

14

21

25

Balances

ANSWER:

a. First-in, first-out

Purchases

Cost of Goods

Sold

Inventory

Unit

Total

Unit

Total

Unit

Total

Chapter 06 – Inventories

14

Sale

24 units @ 10

$240

12 units @ 12

144

25

Sale

14 units @ 12

168

6 units @ 15

90

Cost of goods sold

56

$642

Inventory

24 units @ 10

$240

Purchase

26 units @ 12

312

21

Purchase

18 units @ 15

270

Available for sale

$822

Sale

18 units @ 15

$270

18 units @ 12

216

Sale

12 units @ 10

Cost of goods sold

$702

Inventory

24 units @ 10

Purchase

26 units @ 12

Purchase

18 units @ 15

Available for sale

68

$822/68 = $12.09

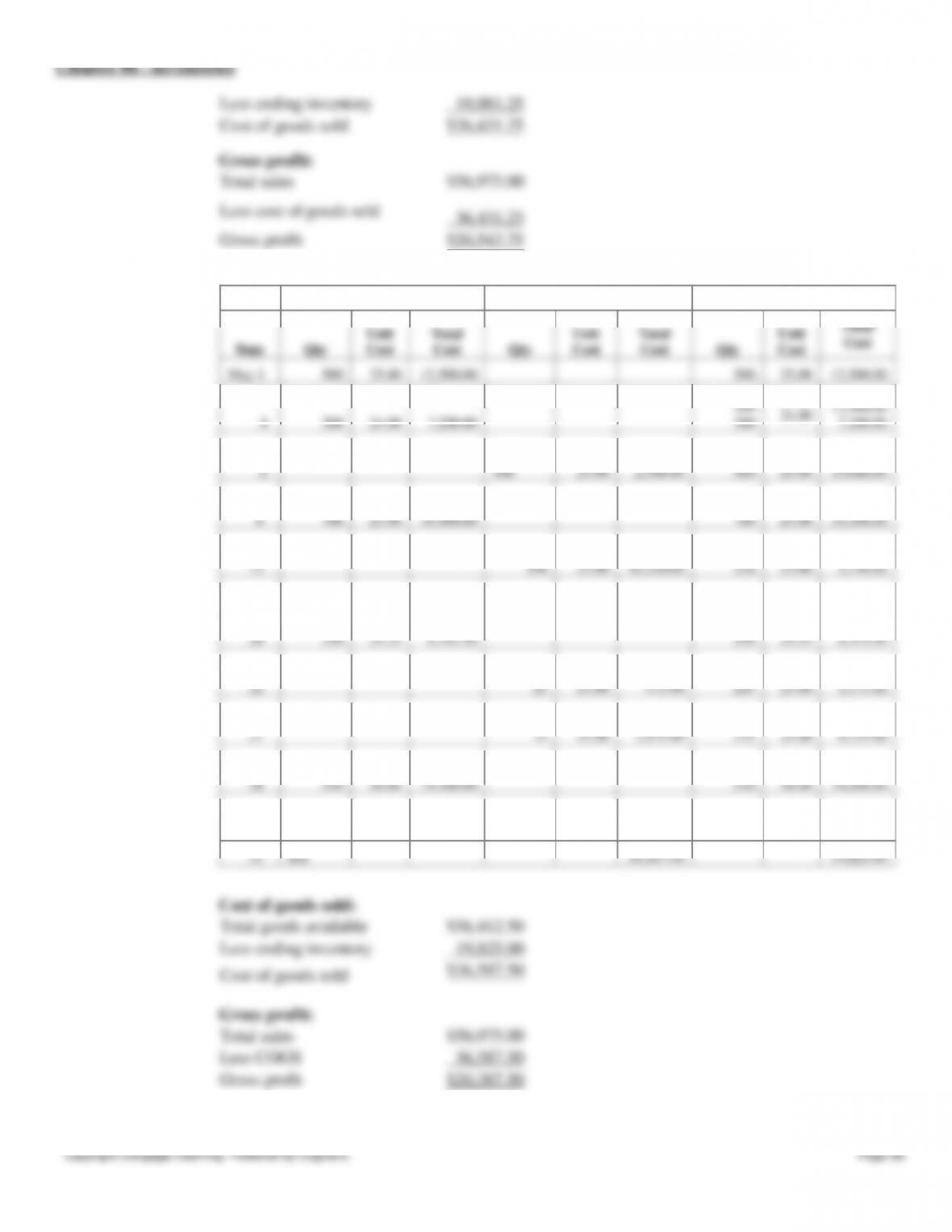

April 3

Inventory

24 units

@

$10

11

Purchase

26 units

@

$12

14

Sale

36 units

21

Purchase

18 units

@

$15

25

Sale

20 units

Assuming the business maintains a periodic inventory system, calculate the cost of goods sold and ending inventory under

the following assumptions:

a. FIFO

b. LIFO

c. Average cost (round cost of goods sold and ending inventory to the nearest dollar)

ANSWER:

a. FIFO

April 3

Inventory

24 units @ 10

$240

11

Purchase

26 units @ 12

312

21

Purchase

18 units @ 15

270

Available for sale

68

$822

Chapter 06 – Inventories

Merchandise shipped to a customer FOB destination was picked up by the freight company

(a)

no

(c)

no

(a)

Complete the table.

(b)

Determine the amount of reduction in the inventory at April 30 attributable to market

decline.

ANSWER:

(a)

Total

Commodity

Inventory

Quantity

Cost

per

Unit

Market

Value

per Unit

Cost

Market

LCM

A

35

$ 52

$ 55

$1,820

$1,925

$1,820

B

20

155

150

3,100

3,000

3,000

C

25

82

85

2,050

2,125

2,050

D

40

58

55

2,320

2,200

2,200

Total

$9,290

$9,250

$9,070

(b) $220 ($9,290 – $9,070)

POINTS:

1

DIFFICULTY:

Moderate

Bloom’s: Applying

QUESTION TYPE:

Subjective Short Answer

HAS VARIABLES:

False

LEARNING OBJECTIVES:

FNMN.WAJO.19.06-07 – LO: 06–07

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.17 – Inventories Reporting

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

DATE CREATED:

7/22/2017 6:20 PM

DATE MODIFIED:

10/16/2017 5:09 PM

198. Hampton Co. took a physical count of its inventory on December 31. In addition, it had to decide whether or not the

following items should be added to this count.

(a)

Inventory on hand had been sold earlier in the year but had been returned by customers for

various warranty repairs.

(b)

Hampton Co. sent merchandise on a consignment basis on December 31 just prior to the

physical count.

(c)

On December 22, Hampton Co. ordered merchandise on FOB destination terms. The

merchandise was shipped by the supplier on December 30 but had not been received by

December 31.

(d)

On December 27, Hampton Co. ordered merchandise on FOB shipping point terms. The

merchandise was shipped on December 29 but had not been received by December 31.

(e)

Merchandise sold FOB shipping point on December 31 was picked up by the freight