Chapter 04 – The Accounting Cycle

202. Journalize the reversing entry on January 1 of the current year for the following adjusting journal entry from the prior

year:

Journal

Date

Description

Post Ref.

Debit

Credit

Dec. 31

Insurance Expense

2,500

Insurance Payable

2,500

ANSWER:

The reversing entry is the exact opposite of the related adjusting entry:

Journal

Date

Description

Post Ref.

Debit

Credit

Jan. 1

Insurance Payable

2,500

Insurance Expense

2,500

POINTS:

1

DIFFICULTY:

Bloom’s: Applying

Easy

QUESTION TYPE:

Subjective Short Answer

HAS VARIABLES:

False

LEARNING OBJECTIVES:

FNMN.WAJO.19.04-APP2 – LO: 04–APP2

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.05 – Accounting Cycle

ACCT.AICPA.FN-03 – Measurement

BUSPROG – Analytic

DATE CREATED:

7/22/2017 6:18 PM

DATE MODIFIED:

10/16/2017 4:41 PM

203. Zeta Company has 12 workers who each earn $15 per hour and generally work a 40-hour workweek, although at

times overtime work is required, for which workers are paid 1.5 times their regular hourly wage. Zeta pays wages in cash

on Friday of each week for work performed that week. Zeta’s Wages Expense ledger account for May is shown below.

Account: Wages Expense

Account Number 65

Balance

Date

May 5

May 12

16,560

May 19

23,760

May 26

31,770

May 31

36,090

May 31

–

Chapter 04 – The Accounting Cycle

Moderate

False

You may omit posting references.

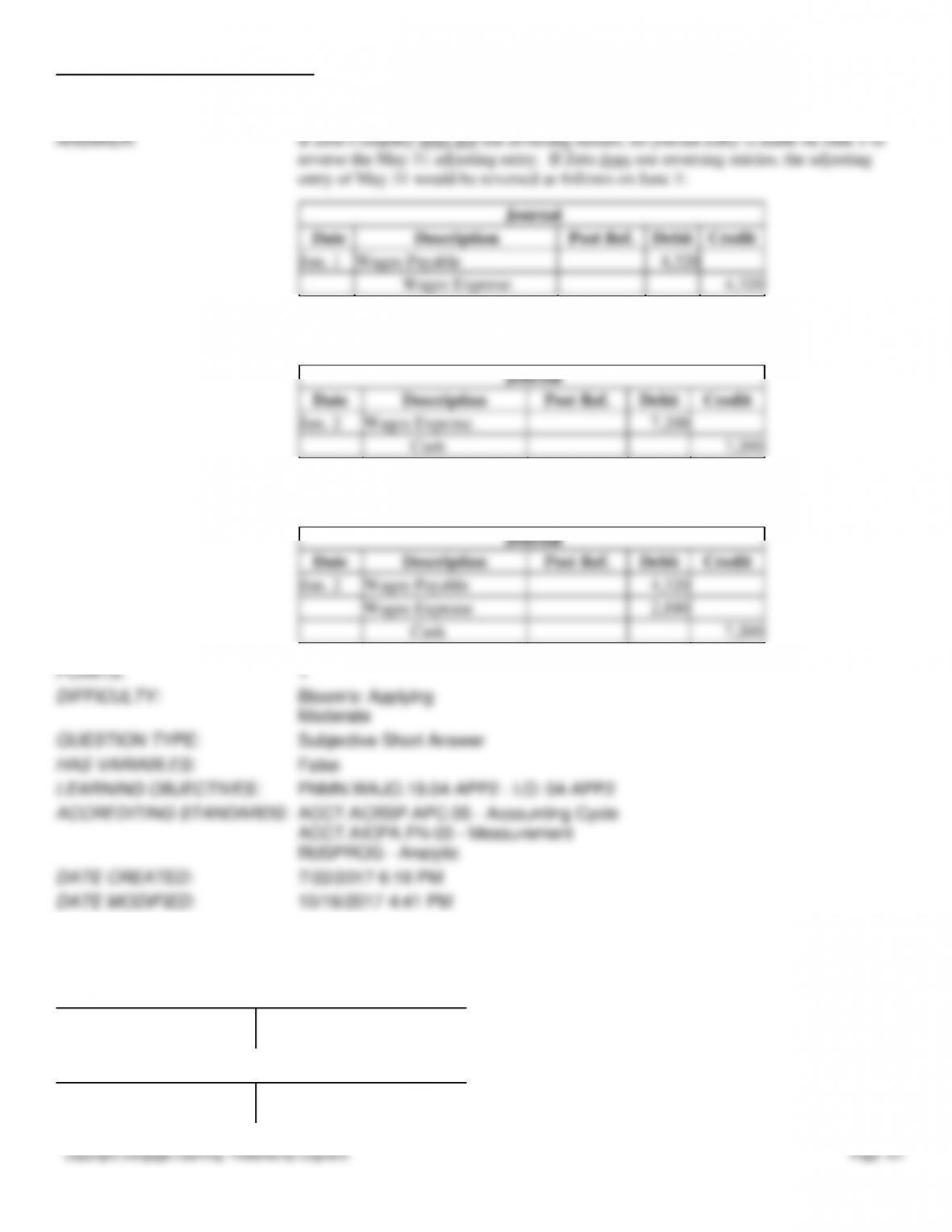

ANSWER:

If Zeta Company does not use reversing entries, no journal entry is made on June 1 to

reverse the May 31 adjusting entry. If Zeta does use reversing entries, the adjusting

entry of May 31 would be reversed as follows on June 1:

Journal

Date

Description

Post Ref.

Debit

Credit

Jun. 1

Wages Payable

4,320

Wages Expense

4,320

1. When a reversing entry is used, the journal entry to pay June 2 wages would be the

normal entry for a full week’s wages ($7,200 = $15 per hour × 40 hours × 12 workers):

Journal

Date

Description

Post Ref.

Debit

Credit

Jun. 2

Wages Expense

7,200

Cash

7,200

2. When a reversing entry is not used, the journal entry to pay June 2 wages would be

as follows:

Journal

Date

Description

Post Ref.

Debit

Credit

Jun. 2

Wages Payable

4,320

Wages Expense

2,880

Cash

7,200

POINTS:

1

DIFFICULTY:

Bloom’s: Applying

Chapter 04 – The Accounting Cycle

Copyright Cengage Learning. Powered by Cognero.

Page 102

Dividends

3/31

2,500

12/31

5,000

9/30

2,500

The $18,000 debit to Retained Earnings on December 31 must represent

a.

dividends paid

b.

net income

c.

net loss

d.

sales of common stock

ANSWER:

c

POINTS:

1

DIFFICULTY:

Moderate

Bloom’s: Applying

QUESTION TYPE:

Multiple Choice

HAS VARIABLES:

False

LEARNING OBJECTIVES:

FNMN.WAJO.19.04-03 – LO: 04–03

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.05 – Accounting Cycle

ACCT.ACBSP.APC.09 – Financial Statements

ACCT.AICPA.FN.03 – Measurement

BUSPROG – Analytic

DATE CREATED:

8/24/2017 3:41 PM

DATE MODIFIED:

10/16/2017 4:41 PM

205. A summary of selected ledger accounts appears below for Solomon’s Electrical Services for the current calendar

year-end.

Common Stock

12/31

8,500

1/1

90,000

12/31

30,000

Retained Earnings

12/31

5,000

1/1

62,000

12/31

18,000

Dividends

3/31

2,500

12/31

5,000

9/30

2,500

The balance in retained earnings that will appear on the financial statements is

a.

$62,000

b.

$57,000

c.

$205,500

d.

$85,500

ANSWER:

d

POINTS:

1

DIFFICULTY:

Bloom’s: Applying

Moderate

QUESTION TYPE:

Multiple Choice

HAS VARIABLES:

False