Chapter 11 – Liabilities: Bonds Payable

Year 3

Oct. 1

Bonds Payable

1,000,000

Loss on Redemption of Bonds

40,000

Cash

1,040,000

POINTS:

1

Moderate

(c)

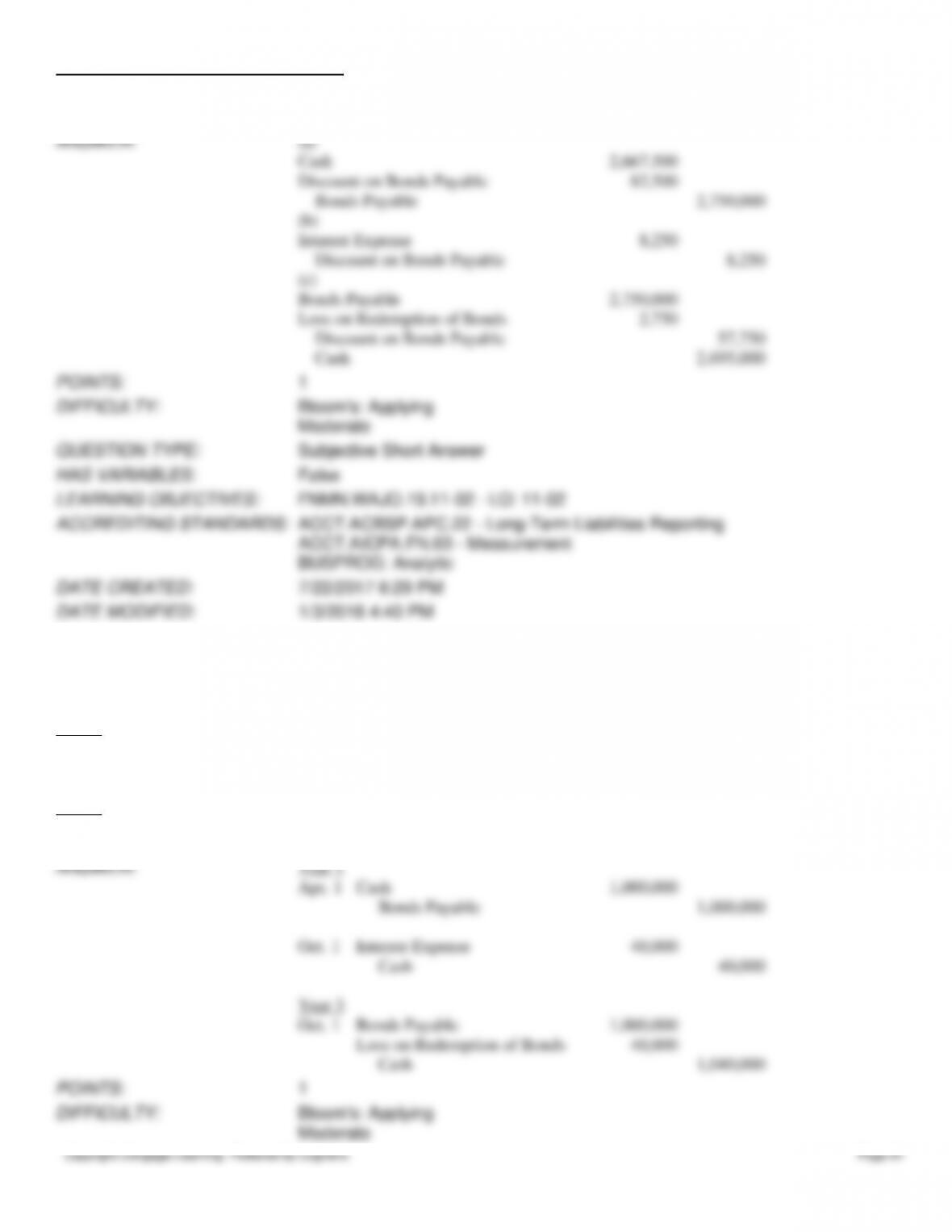

Called bonds at 98. Assume the bonds were carried at $2,692,250 at the time of the

redemption.

ANSWER:

(a)

Cash

2,667,500

Discount on Bonds Payable

82,500

Bonds Payable

2,750,000

(b)

Interest Expense

8,250

Discount on Bonds Payable

8,250

(c)

Bonds Payable

2,750,000

Loss on Redemption of Bonds

2,750

Discount on Bonds Payable

57,750

Cash

2,695,000

POINTS:

1

DIFFICULTY:

Bloom’s: Applying

Moderate

QUESTION TYPE:

Subjective Short Answer

HAS VARIABLES:

False

LEARNING OBJECTIVES:

FNMN.WAJO.19.11-02 – LO: 11–02

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.22 – Long-Term Liabilities Reporting

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

DATE CREATED:

7/22/2017 6:29 PM

DATE MODIFIED:

1/3/2018 4:40 PM

149. A company issued $1,000,000 of 30-year, 8% callable bonds on April 1, with interest payable on April 1 and October

1. The fiscal year of the company is the calendar year. Journalize the entries to record the following selected

transactions:

Year 1

Apr. 1

Issued the bonds for cash at their face amount.

Oct. 1

Paid the interest on the bonds.

Year 3

Oct. 1

Called the bond issue at 104, the rate provided in the bond indenture. (Omit entry for

payment of interest.)

ANSWER:

Year 1

Apr. 1

Cash

1,000,000

Bonds Payable

1,000,000

Oct. 1

Interest Expense

40,000

Cash

40,000

Chapter 11 – Liabilities: Bonds Payable

BUSPROG: Analytic

DATE CREATED:

7/22/2017 6:29 PM

DATE MODIFIED:

10/16/2017 6:10 PM

ANSWER:

(a)

Cash

2,580,000

Premium on Bonds Payable

80,000

Bonds Payable

2,500,000

(b)

Interest Expense

100,000

Cash

100,000

(c)

Premium on Bonds Payable

4,000

Interest Expense

4,000

POINTS:

1

DIFFICULTY:

Bloom’s: Applying

Challenging

QUESTION TYPE:

Subjective Short Answer

HAS VARIABLES:

False

LEARNING OBJECTIVES:

FNMN.WAJO.19.11-02 – LO: 11–02

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.22 – Long-Term Liabilities Reporting

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

DATE CREATED:

7/22/2017 6:29 PM

DATE MODIFIED:

10/16/2017 6:10 PM

152. Calculate the total amount of interest expense over the life of the bonds for the following independent situations.

(a) $100,000 face value, 10%, 10-year bonds issued at 101.

(b) $240,000 face value, 5%, 5-year bonds issued at 100.

(c) $300,000 face value, 9%, 6-year bonds issued at 98.

ANSWER:

(a) $100,000 × 0.01 = $1,000 premium

$100,000 × 0.10 = $10,000 annual cash payment

$10,000 × 10 years = $100,000

$100,000 – $1,000 = $99,000 total interest expense

(b) $240,000 × 0.05 = $12,000 annual cash payment

$12,000 × 5 years = $60,000 total interest expense

(c) $300,000 × 0.02 = $6,000 discount

$300,000 × 0.09 = $27,000 annual cash payment

$27,000 × 6 years = $162,000

$162,000 + $6,000 = $168,000 total interest expense

POINTS:

1

DIFFICULTY:

Bloom’s: Applying

Moderate

QUESTION TYPE:

Subjective Short Answer

HAS VARIABLES:

False

LEARNING OBJECTIVES:

FNMN.WAJO.19.11-02 – LO: 11–02

Copyright Cengage Learning. Powered by Cognero.

Page 64

153. Given the following data, prepare the journal entry to record interest expense and any related amortization on

December 31 of the first year using the effective interest rate method. Assume interest is paid annually on January 1. The

bonds were issued on January 1 for $7,411,233.

Bonds payable, maturing in 10 years = $8,000,000

Contract interest rate = 5%

Market (effective) interest rate = 6%

Round answers to nearest dollar.

ANSWER:

Interest Expense 444,674

Discount on Bonds Payable 44,674

Interest Payable 400,000

POINTS:

1

DIFFICULTY:

Bloom’s: Applying

Moderate

QUESTION TYPE:

Subjective Short Answer

HAS VARIABLES:

False

LEARNING OBJECTIVES:

FNMN.WAJO.19.11-02 – LO: 11–02

FNMN.WAJO.19.11-APP2 – LO: 11–APP2

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.22 – Long-Term Liabilities Reporting

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

DATE CREATED:

7/22/2017 6:29 PM

DATE MODIFIED:

10/16/2017 6:10 PM

154.

(a)

Prepare the journal entry to issue $100,000 bonds that sold for $94,000.

(b)

Prepare the journal entry to issue $100,000 bonds that sold for $104,000.

ANSWER:

(a)

Cash

94,000

Discount on Bonds Payable

6,000

Bonds Payable

100,000

(b)

Cash

104,000

Premium on Bonds Payable

4,000

Bonds Payable

100,000

POINTS:

1

DIFFICULTY:

Bloom’s: Applying

Easy

QUESTION TYPE:

Subjective Short Answer

HAS VARIABLES:

False

LEARNING OBJECTIVES:

FNMN.WAJO.19.11-02 – LO: 11–02

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.22 – Long-Term Liabilities Reporting

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

DATE CREATED:

7/22/2017 6:29 PM

DATE MODIFIED:

10/16/2017 6:10 PM

155. Glover Corporation issued $2,000,000 of 7.5%, 6-year bonds dated March 1, with semiannual interest payments on

Chapter 11 – Liabilities: Bonds Payable

POINTS:

1

DIFFICULTY:

Bloom’s: Applying

September 1 and March 1. The bonds were issued on March 1, at 97. Glover’s year-end is December 31.

(a) Were the bonds issued at a premium, a discount, or at par?

(b) Was the market rate of interest higher, lower, or the same as the contract rate of interest?

(c) If the company uses the straight-line method of amortization, what is the amount of interest expense Glover

Corporation will show for the year ended December 31?

(d) What is the carrying value of the bonds on December 31?

ANSWER:

(a) The bonds were issued at a discount.

(b) The market rate of interest was higher than 7.5% since the bonds were issued at a

discount.

(c) $2,000,000 × 0.075 × 10/12 = $125,000 interest expense prior to amortization

$2,000,000 – $1,940,000 = $60,000 discount on bonds payable

$60,000/6 = $10,000 annual amortization of discount

$10,000 × 10/12 = $8,333 current year’s amortization of discount

$125,000 + $8,333 = $133,333

(d) $2,000,000 – $60,000 + $8,333 = $1,948,333

POINTS:

1

DIFFICULTY:

Bloom’s: Applying

Challenging

QUESTION TYPE:

Subjective Short Answer

HAS VARIABLES:

False

LEARNING OBJECTIVES:

FNMN.WAJO.19.11-02 – LO: 11–02

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.22 – Long-Term Liabilities Reporting

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

DATE CREATED:

7/22/2017 6:29 PM

DATE MODIFIED:

10/16/2017 6:10 PM

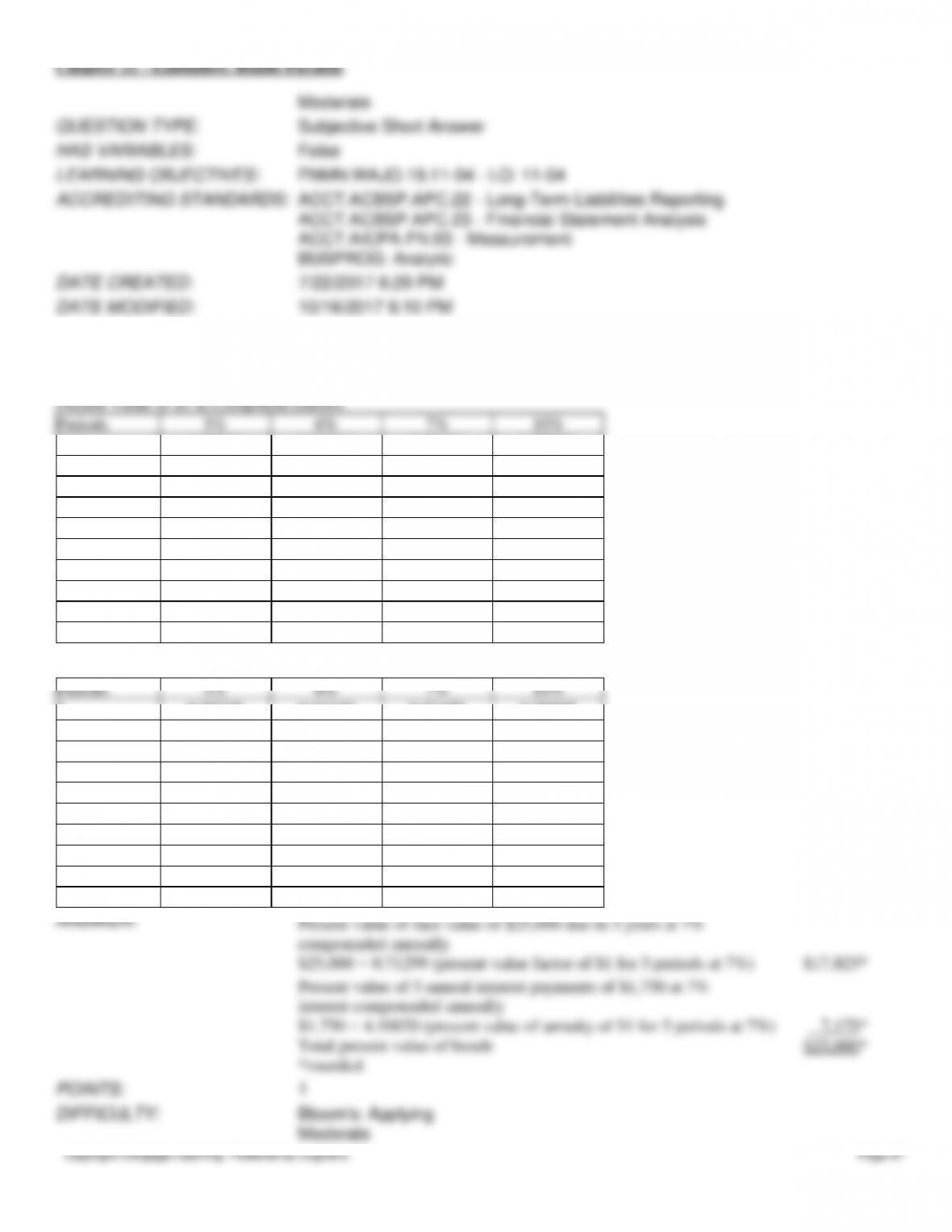

156. On January 1, Year 1, Kennard Co. issued $2,000,000, 5%, 10-year bonds, with interest payable on June 30

and December 31 to yield 6%. Use the following format and round figures to nearest dollar. The bonds were issued for

$1,851,234.

(a) Prepare an amortization schedule for Year 1 and Year 2 using the effective interest rate method.

Date Interest Paid Interest Expense Amortization Bond Carrying Amount

(b) Show how this bond would be reported on the balance sheet at December 31, Year 2.

ANSWER:

(a)

Date

Interest

Paid

Interest

Expense

Amortization

Bond

Carrying

Amount

1/1/Year 1

$1,851,234

6/30/Year 1

$50,000

$55,537

$5,537

1,856,771

12/31/Year 1

50,000

55,703

5,703

1,862,474

6/30/Year 2

50,000

55,874

5,874

1,868,348

12/31/Year 2

50,000

56,050

6,050

1,874,398

Copyright Cengage Learning. Powered by Cognero.

Page 69

10

0.61391

0.55840

0.50835

0.38554

ANSWER:

$40,000 × 0.71299 = $28,519.60

POINTS:

1

DIFFICULTY:

Easy

Bloom’s: Applying

QUESTION TYPE:

Subjective Short Answer

HAS VARIABLES:

False

LEARNING OBJECTIVES:

FNMN.WAJO.19.11-APP1 – LO: 11–APP1

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.22 – Long-Term Liabilities Reporting

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

DATE CREATED:

7/22/2017 6:29 PM

DATE MODIFIED:

10/16/2017 6:10 PM

162. A company issued $1,000,000 of 30-year, 8% callable bonds on April 1, with interest payable on April 1 and October

1. The fiscal year of the company is the calendar year. What is the journal entry needed when the bonds are issued at face

value?

a.

debit Bonds Payable, credit Cash

b.

debit Cash and Discount on Bonds Payable, credit Bonds Payable

c.

debit Cash, credit Premium on Bonds Payable and Bonds Payable

d.

debit Cash, credit Bonds Payable

ANSWER:

d

POINTS:

1

DIFFICULTY:

Bloom’s: Applying

Moderate

QUESTION TYPE:

Multiple Choice

HAS VARIABLES:

False

LEARNING OBJECTIVES:

FNMN.WAJO.19.11-02 – LO: 11–02

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.22 – Long-Term Liabilities Reporting

ACCT.AICPA.FN.03 – Measurement

BUSPROG – Analytic

DATE CREATED:

9/29/2017 6:52 PM

DATE MODIFIED:

10/16/2017 6:10 PM

163. A company issued $1,000,000 of 30-year, 8% callable bonds on April 1, with interest payable on April 1 and October

1. The fiscal year of the company is the calendar year. The bonds are called at the end of year 3 for 104. What is the

entry to record the redemption? (Assume the interest payment has been recorded separately.)

a.

Bonds Payable 1,000,000

Gain on Redemption of Bonds 40,000

Cash 1,040,000

b.

Bonds Payable 1,000,000

Loss on Redemption of Bonds 40,000

Cash 1,040,000

c.

Bonds Payable 1,000,000

Cash 1,000,000

d.

Bonds Payable 1,040,000

Cash 1,000,000

Chapter 11 – Liabilities: Bonds Payable

Copyright Cengage Learning. Powered by Cognero.

Page 70

Loss on Redemption of Bonds 40,000

ANSWER:

b

POINTS:

1

DIFFICULTY:

Bloom’s: Applying

Moderate

QUESTION TYPE:

Multiple Choice

HAS VARIABLES:

False

LEARNING OBJECTIVES:

FNMN.WAJO.19.11-02 – LO: 11–02

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.22 – Long-Term Liabilities Reporting

ACCT.AICPA.FN.03 – Measurement

BUSPROG – Analytic

DATE CREATED:

9/29/2017 6:57 PM

DATE MODIFIED:

10/16/2017 6:10 PM

164. Luke Corp. issued $2,000,000 of 20-year, 9% callable bonds on July 1, Year 1, with interest payable on June 30 and

December 31. The fiscal year of the company is the calendar year. What is the entry to record the payment of interest on

December 31 in the year the bonds were issued?

a.

Interest Expense 180,000

Cash 180,000

b.

Interest Payable 90,000

Interest Expense 90,000

Cash 180,000

c.

Interest Expense 90,000

Cash 90,000

d.

Cash 90,000

Interest Expense 90,000

ANSWER:

c

POINTS:

1

DIFFICULTY:

Bloom’s: Applying

Moderate

QUESTION TYPE:

Multiple Choice

HAS VARIABLES:

False

LEARNING OBJECTIVES:

FNMN.WAJO.19.11-02 – LO: 11–02

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.22 – Long-Term Liabilities Reporting

ACCT.AICPA.FN.03 – Measurement

BUSPROG – Analytic

DATE CREATED:

9/29/2017 7:01 PM

DATE MODIFIED:

10/16/2017 6:10 PM

165. Luke Corp. issued $2,000,000 of 20-year, 9% callable bonds on July 1, Year 1, with interest payable on June 30 and

December 31. The fiscal year of the company is the calendar year. What is the entry to record the calling of the bonds at

the end of year 5 at 97? (Assume interest for the period has been separately recorded.)

a.

Bonds Payable 2,000,000

Gain on Redemption of Bonds 60,000

Cash 1,940,000

b.

Bonds Payable 2,000,000

Gain on Redemption of Bonds 60,000