Page 21

70.

(Table: Producer Surplus) Use Table: Producer Surplus. If the price of a ticket to see

The Nutty Nutcracker is $50, then Dudley’s producer surplus is:

A)

$0.

B)

$25.

C)

$60.

D)

$240.

71.

(Table: Producer Surplus) Use Table: Producer Surplus. If the price of a ticket to see

The Nutty Nutcracker is $75, then Caitlin’s producer surplus is:

A)

$0.

B)

$74.

C)

$75.

D)

$100.

72.

(Table: Producer Surplus) Use Table: Producer Surplus. If the price of a ticket to see

The Nutty Nutcracker is $75, then Dudley’s producer surplus is:

A)

$15.

B)

$25.

C)

$50.

D)

$240.

73.

(Table: Producer Surplus) Use Table: Producer Surplus. If the price of a ticket to see

The Nutty Nutcracker is $50 and there is no other market for tickets, then total producer

surplus for the five students is:

A)

$50.

B)

$74.

C)

$100.

D)

$276.

74.

(Table: Producer Surplus) Use Table: Producer Surplus. If the price of a ticket to see

The Nutty Nutcracker is $75 and there is no other market for tickets, the total producer

surplus for the five students is:

A)

$190.

B)

$139.

C)

$75.

D)

$40.

Page 22

75.

(Table: Producer Surplus) Use Table: Producer Surplus. If the tickets to The Nutty

Nutcracker are free and there is no other market for tickets, the total producer surplus

for the five students is:

A)

$276.

B)

$100.

C)

$74.

D)

$0.

76.

We can measure total producer surplus for good X as the:

A)

sum of the individual producer surpluses for all buyers of X.

B)

area below the supply curve for X and above the price of X.

C)

area bounded by the supply curve for X and the two axes.

D)

area between the demand curve for X and the supply curve for X.

77.

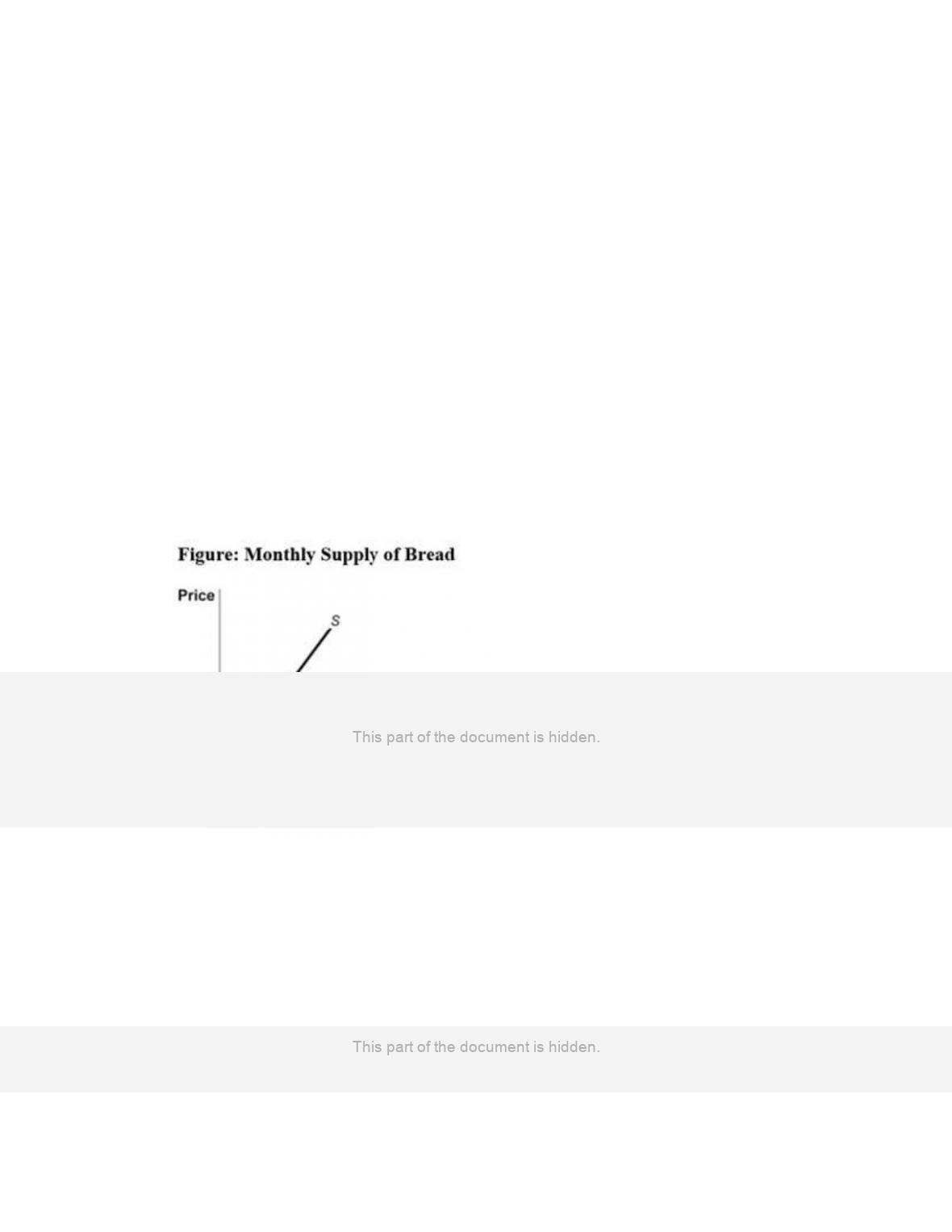

(Figure: Monthly Supply of Bread) The figure Monthly Supply of Bread represents the

monthly supply of bread at a local bakery. At $3 per loaf, the bakery produces 120

loaves per month. The producer surplus received by this bakery is equal to:

A)

$120.

B)

$60.

C)

$360.

D)

$180.

78.

Producer surplus for an individual seller is equal to the:

A)

price received for selling the good minus the cost of producing the good.

B)

cost of the good minus the willingness to pay for the good.

C)

willingness to pay for the good minus the price received for selling the good.

D)

cost of the good minus the price received for selling the good.

Page 23

79.

Maria wants to get rid of her bookshelf. She is willing to give it away, but her neighbor

offers to pay $30 for it. Maria takes a:

A)

consumer surplus gain.

B)

consumer surplus loss.

C)

producer surplus gain.

D)

producer surplus loss.

80.

Producer surplus is represented by the area _____ the supply curve and _____ the price

received by the seller.

A)

above; above

B)

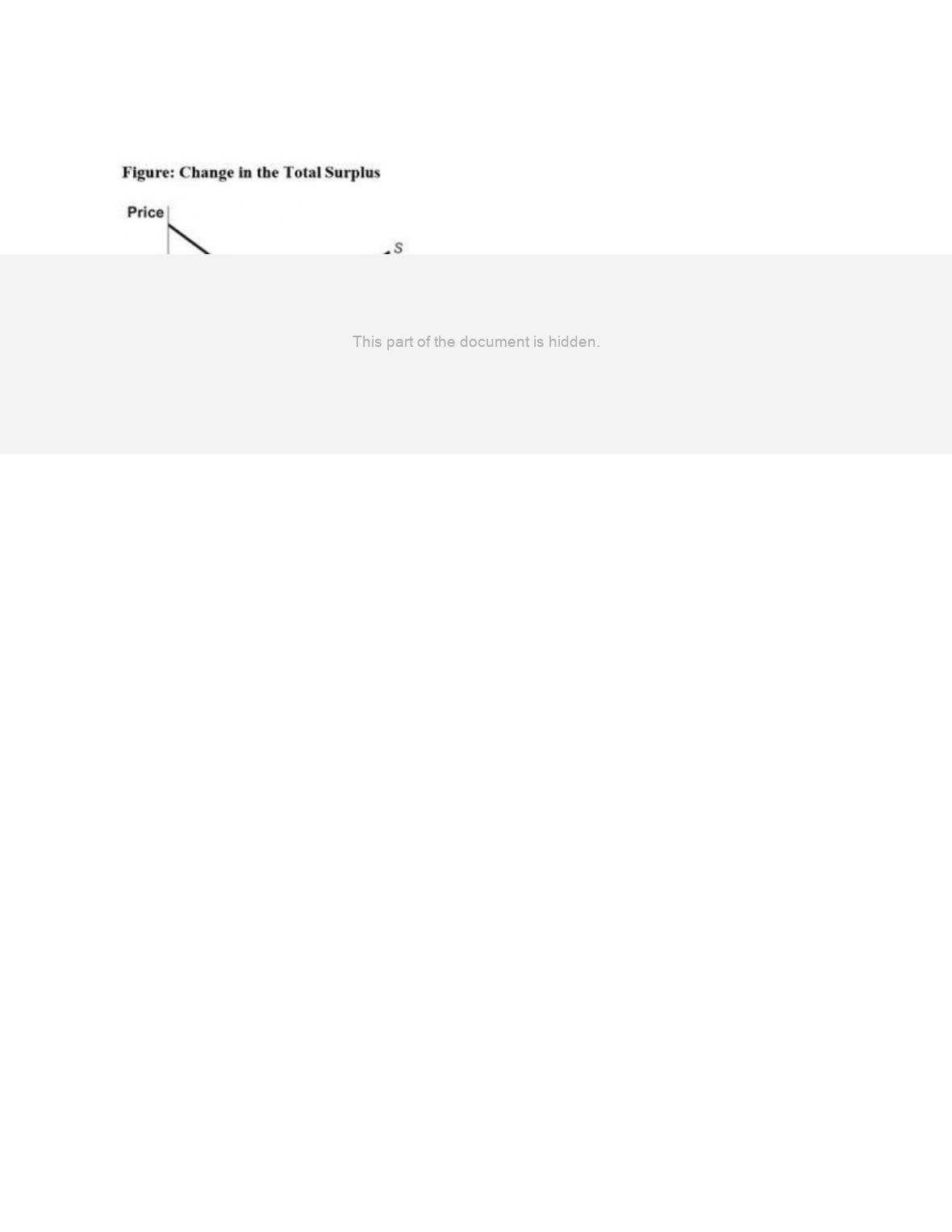

above; below

C)

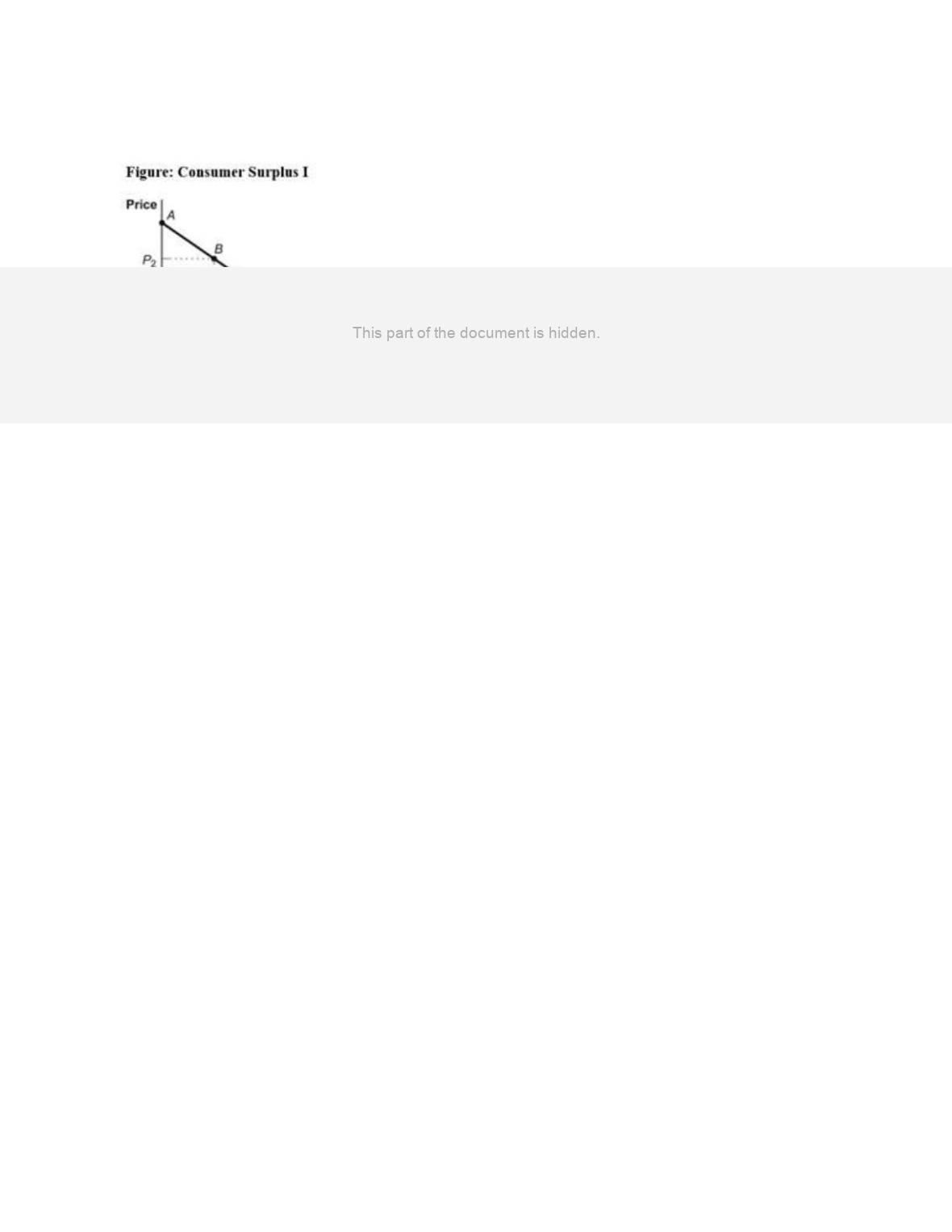

below; above

D)

below; below

81.

Mountain River Adventures offers whitewater rafting trips down the Colorado River. It

costs the firm $100 for the first raft trip per day, $120 for the second, $140 for the third,

and $160 for the fourth. If the market price for a raft trip is $150, Mountain River

Adventures will offer _____ trips per day and will have producer surplus equal to _____

per day.

A)

three; $90

B)

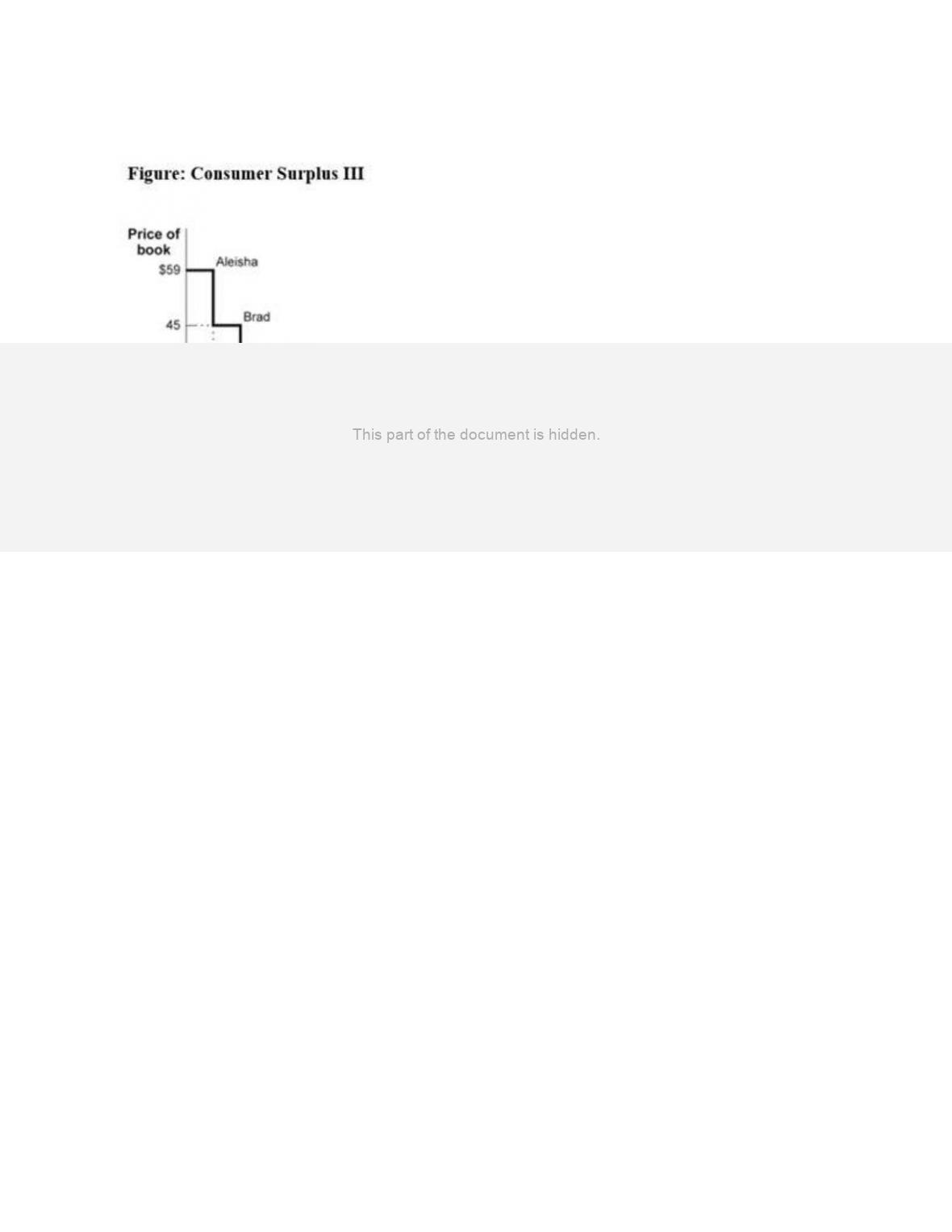

three; $10

C)

two; $220

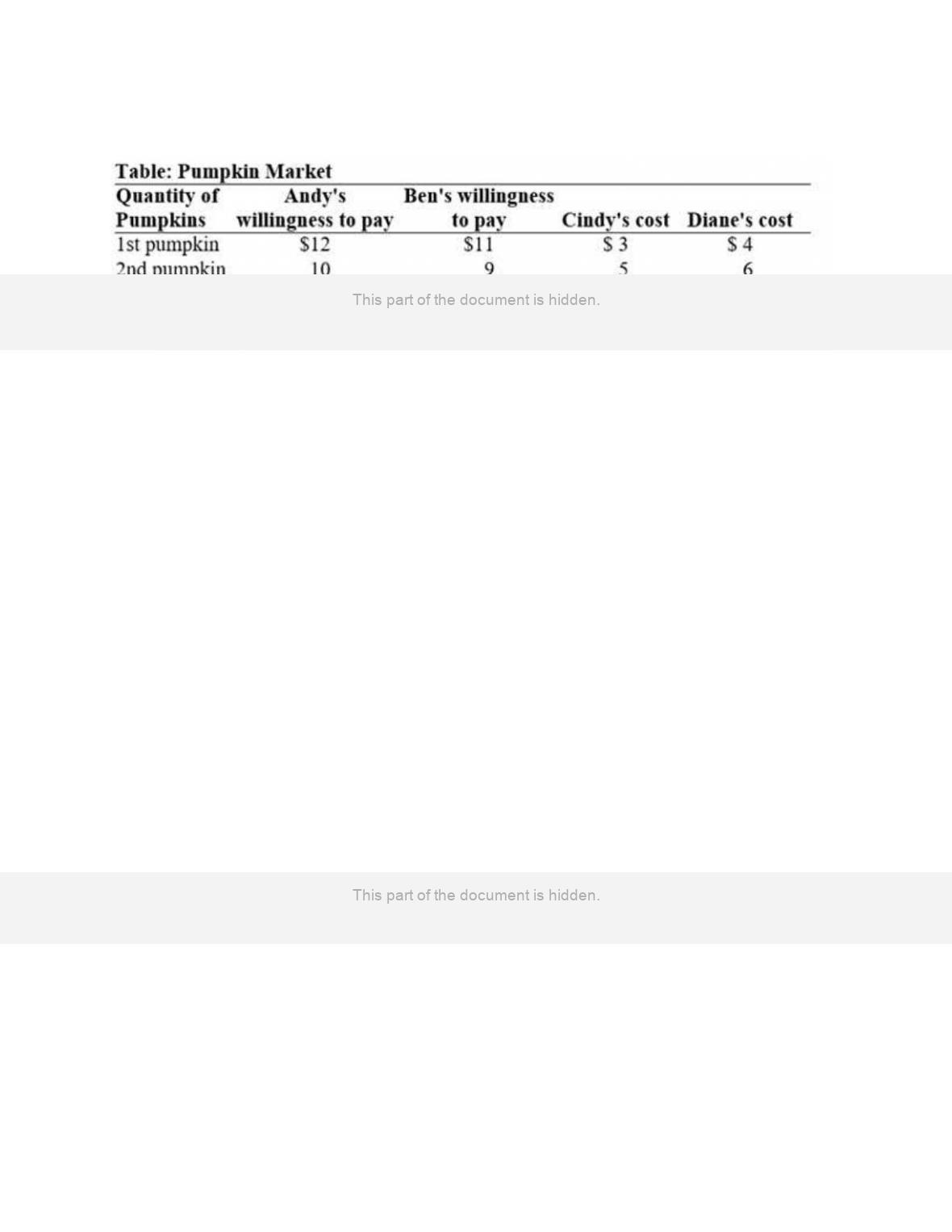

D)

four; $80

82.

Luis is willing to sell his pool table for no less than $600, but if he gets $840, the

producer surplus Luis receives is:

A)

$600.

B)

$840.

C)

$240.

D)

$1,440.

Page 24

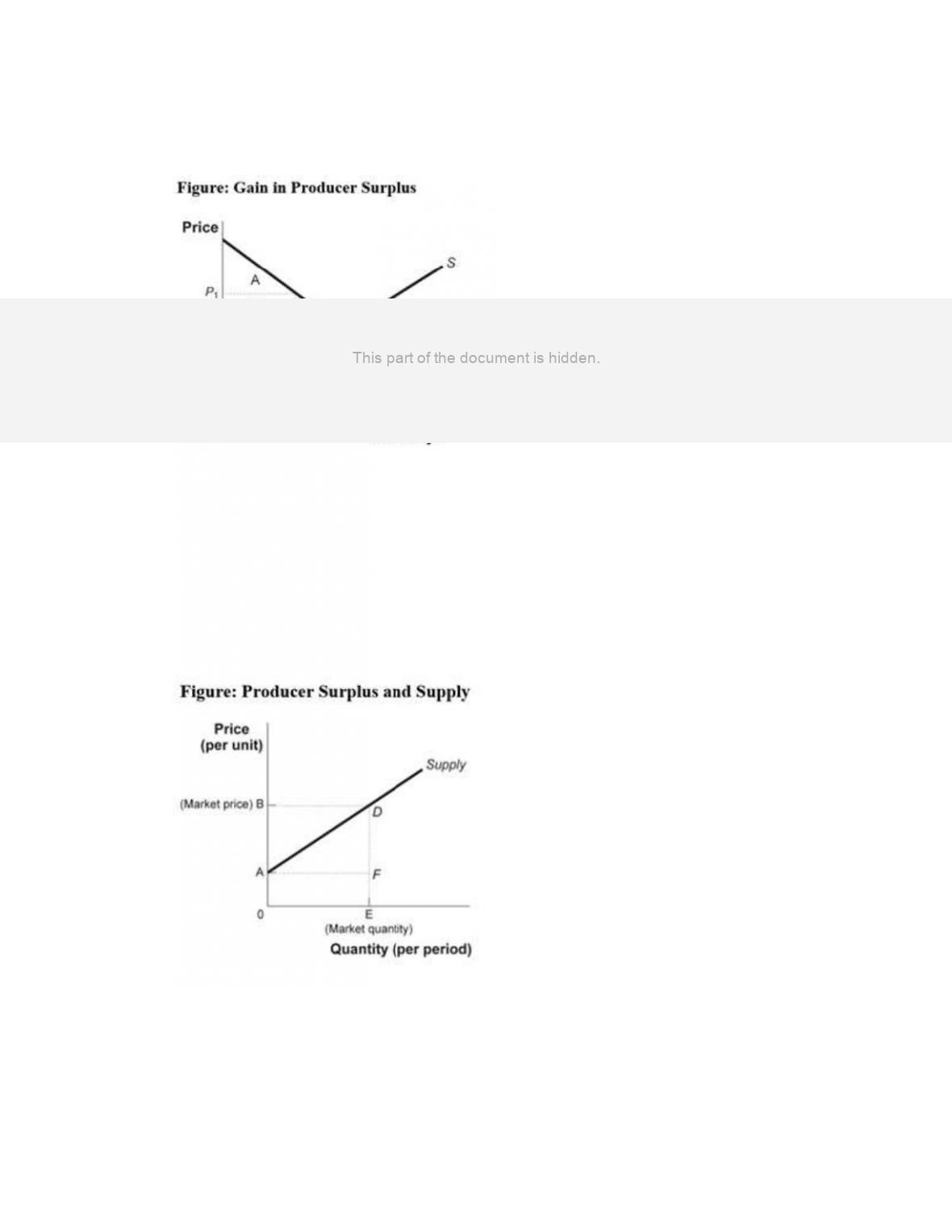

83.

(Figure: Gain in Producer Surplus) Look at the figure Gain in Producer Surplus. Which

areas represent producer surplus when the price is equal to P2?

A)

D, E, and F

B)

B and C

C)

D and E

D)

A, B, and C

84.

(Figure: Producer Surplus and Supply) Look at the figure Producer Surplus and Supply.

The difference between the total revenue received by sellers and their total cost is called

_____, which is depicted by area _____ if the amount sold is E.

A)

consumer surplus; ABD

B)

producer surplus; 0BDE

C)

profit; ABD

D)

producer surplus; ABD

Page 25

85.

Mountain River Adventures offers whitewater rafting trips down the Colorado River. It

costs the firm $100 for the first raft trip per day, $120 for the second, $140 for the third,

and $160 for the fourth. If the market price for a raft trip was $120 but has now

increased to $150, the gain in producer surplus is equal to:

A)

$20.

B)

$70.

C)

$80.

D)

$90.

86.

Along a given supply curve, an increase in the price of a good will:

A)

increase producer surplus.

B)

decrease producer surplus.

C)

increase consumer surplus.

D)

decrease producer surplus and increase consumer surplus.

87.

Assuming that the supply curve of cupcakes is upward-sloping and demand for

cupcakes decreases, there is a(n) _____ in _____ surplus.

A)

increase; producer

B)

increase; consumer

C)

increase; total

D)

decrease; producer

88.

Along the upward-sloping supply curve for brownies, a decrease in the price of

brownies will:

A)

increase producer surplus.

B)

decrease producer surplus.

C)

increase consumer surplus.

D)

increase producer surplus and consumer surplus.

89.

Peanut butter and jelly are complements in consumption. Assuming that the supply

curve of peanut butter is upward-sloping, if there is a decrease in the price of jelly,

producer surplus in the peanut butter market:

A)

will increase.

B)

will decrease.

C)

will not change.

D)

may change, but it is impossible to tell whether it will increase or decrease.

Page 26

90.

Equilibrium in the market for peanut butter is disturbed by an increase in the price of

peanuts. Assuming that the supply curve of peanut butter is upward-sloping, producer

surplus in the peanut butter market:

A)

will increase.

B)

will decrease.

C)

will not change.

D)

may change, but we cannot determine the change without more information.

91.

If the supply curve of ice cream is upward-sloping and demand for it decreases, there

will be _____ in producer surplus.

A)

an increase

B)

a decrease

C)

no change

D)

It’s impossible to tell what will happen to producer surplus.

92.

When a new medical report extols the health advantages of grapefruit, assuming an

upward-sloping supply curve, producer surplus in the grapefruit market:

A)

will increase.

B)

will decrease.

C)

will remain the same.

D)

may change, but we can’t tell how.

93.

Along a given upward-sloping supply curve, a decrease in the price of a good will

_____ producer surplus.

A)

increase

B)

decrease

C)

have no effect on

D)

It’s impossible to tell what will happen to producer surplus.

94.

If the price of a good rises along an upward-sloping supply curve, then producer

surplus:

A)

will increase.

B)

will decrease.

C)

will remain the same.

D)

may change, but we can’t tell how.

Page 27

95.

Along a given upward-sloping supply curve, a decrease in price will cause producer

surplus to:

A)

increase.

B)

decrease.

C)

stay the same.

D)

We cannot determine what producer surplus will do without information about the

demand curve.

96.

If the cost to download a song from the Internet falls from $0.99 to $0.50 along an

upward-sloping supply curve, producer surplus in the market for MP3 players is likely

to:

A)

increase.

B)

decrease.

C)

not change.

D)

We cannot determine what producer surplus will do without information about

consumer surplus.

97.

Total surplus is:

A)

the difference between price and the cost to the seller.

B)

the sum of consumer and producer surplus.

C)

equal to the area below the demand curve.

D)

always more for consumers than producers.

98.

Maximum total surplus in the market for chocolate occurs when:

A)

total net gain to producers is minimized.

B)

all consumers who value chocolate can buy chocolate.

C)

all producers can sell their chocolate.

D)

the market is in equilibrium.

99.

The total surplus in a market is the:

A)

excess supply due to a price above the equilibrium price.

B)

surplus that accrues when a good is not scarce, defined as the total amount (if any)

by which quantity supplied exceeds quantity demanded at a zero price.

C)

net benefit to consumers, defined as the excess of consumer surplus over producer

surplus.

D)

sum of consumer surplus and producer surplus.

Page 28

Use the following to answer question 100:

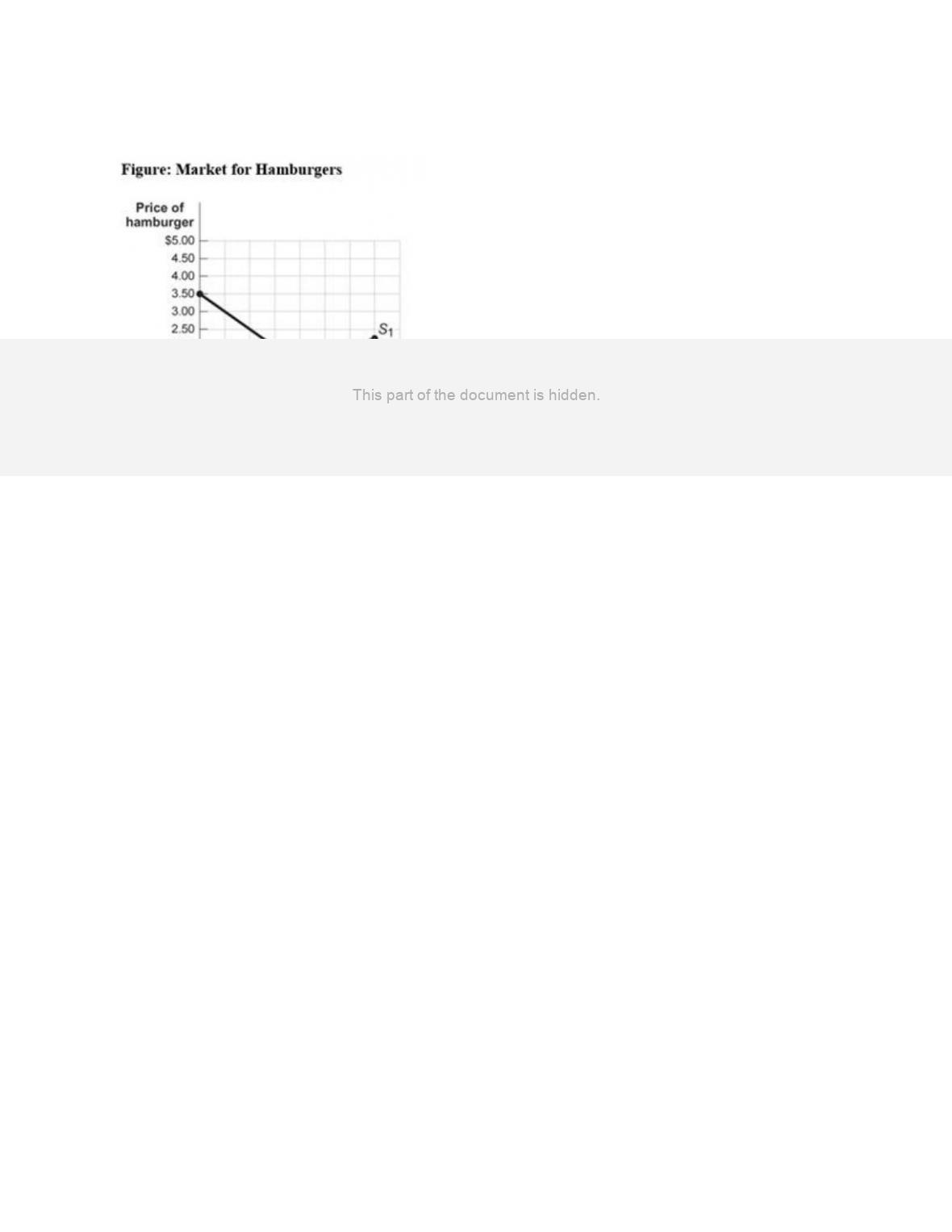

100.

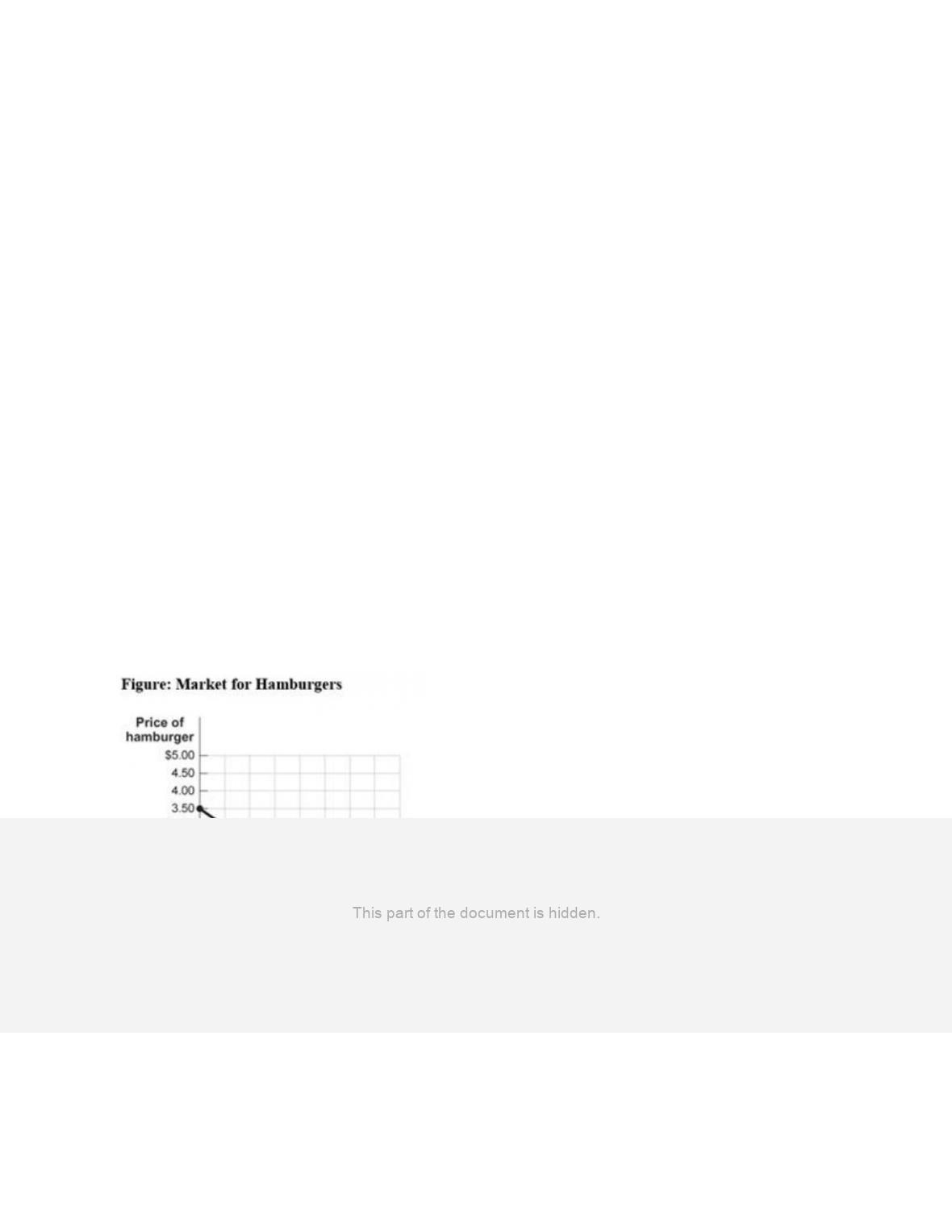

(Figure: The Market for Hamburgers) Look at the figure The Market for Hamburgers.

The maximum total surplus for the market is _____, and it occurs at a price equal to

_____.

A)

$550; $1.50

B)

$600; $1.50

C)

$1,050; $2

D)

Not enough information is provided to answer this question, since the maximum

total surplus could occur anywhere.

101.

Suppose you pay $10 to see Ryan Reynolds in his next movie. Suppose Mr. Reynolds

receives $31 million to work in this movie. This means that:

A)

you would have been better off being more self-reliant in the movie market.

B)

Ryan Reynolds received a producer surplus of $31 million.

C)

you received a consumer surplus of $10.

D)

you and Ryan Reynolds benefited from this transaction.

102.

Total surplus is:

A)

the sum of consumer and producer surplus.

B)

measured as the area between the supply and demand curves from their beginnings

to their ends.

C)

the total net gain to consumers from trading in the market.

D)

the total net gain to producers from trading in the market.

Page 29

103.

(Figure: The Market for Sandwiches) Look at the figure The Market for Sandwiches. At

the competitive price of $5, 10 sandwiches are sold. At this competitive price, consumer

surplus equals _____ and producer surplus equals _____.

A)

$50; $50

B)

$100; $50

C)

$50; $25

D)

$100; $25

104.

Alex is willing to buy the last ticket to the Billy Bragg concert for $15, while Jake is

willing to pay $25. Alex is first in line and buys a ticket for $15. He then resells his

ticket to Jake for $20. By reselling the ticket instead of going to the concert himself,

Alex caused:

A)

the sum of the consumer and producer surplus to increase.

B)

the sum of the consumer and producer surplus to decrease.

C)

a deadweight loss of $5.

D)

consumer surplus to decrease and producer surplus to increase.

105.

Suppose the equilibrium rent for apartments in Boston is $1,600. If the city of Boston

imposes a price ceiling of $1,200, there will be a(n):

A)

increase in producer surplus for each landlord.

B)

surplus of new apartments in Boston.

C)

increase in consumer surplus for Bostonians who can find apartments for $1,200.

D)

increase in total surplus.

Page 30

106.

When a market is in equilibrium and there is no outside intervention to change the

equilibrium price:

A)

total surplus is minimized.

B)

inefficiency is maximized.

C)

no mutually beneficial trades are missed.

D)

some mutually beneficial trades may be missed.

107.

If the market for grapefruit is in equilibrium without any outside intervention to change

the equilibrium price:

A)

total surplus is minimized.

B)

there is some deadweight loss.

C)

a few mutually beneficial trades are missed.

D)

consumer and producer surplus are maximized.

108.

A competitive market for cell phone chargers is in equilibrium. If the price temporarily

falls below the equilibrium price:

A)

producer surplus will rise.

B)

producer surplus will fall.

C)

the change in producer surplus is indeterminate.

D)

there will be no change in producer surplus.

109.

When a market is efficient:

A)

there is no way to make some people better off without making other people worse

off.

B)

consumers who value buying a good the least are the ones who can purchase the

good.

C)

producers whose willingness to accept a price above the market price can sell their

good.

D)

there are ways to make everyone better off.

110.

If the government intervened in the market by lowering the price of a good below the

equilibrium price, which scenario would NOT occur?

A)

Some consumers would receive an increase in consumer surplus.

B)

Producers would likely lose some producer surplus.

C)

The outcome would be efficient.

D)

Total surplus would be lower.

Page 31

111.

Which factor is key in the effectiveness of well-functioning markets?

A)

outcomes that are equitable for consumers and producers

B)

the role of the government to deliver economic signals to consumers and producers

C)

a significant degree of government intervention to maximize efficiency

D)

your right to use and dispose of your private property as you see fit

112.

Property rights are an important feature of an effective market because they:

A)

lead to the development of government control over prices.

B)

prevent harm to the environment from pollution.

C)

give owners of goods and services the right to use and dispose of those goods and

services as they choose.

D)

are the basis for an equitable tax system.

113.

The lack of property rights and inaccuracy of prices as economic signals often lead to:

A)

too much competition in markets.

B)

an increase in consumer surplus and a decrease in producer surplus.

C)

an increase in total surplus.

D)

market failure.

114.

Market failure refers to a situation in which:

A)

markets fail to reach a fair outcome.

B)

markets establish a high price for necessities.

C)

market-determined wages are not high enough to raise all workers above the

poverty line.

D)

markets fail to reach an efficient outcome.

115.

A factor that is NOT a possible reason for market failure is:

A)

firms having too much market power.

B)

externalities.

C)

public goods.

D)

extremely high prices for medical care.

116.

Assume that the supply curve for corn is upward-sloping. In the market for corn, a

primary input in the production of ethanol, total surplus _____ when the price of ethanol

increases.

A)

increases

B)

decreases

C)

does not change

D)

The answer cannot be determined without information about the supply curve.

Page 32

Use the following to answer questions 117-118:

117.

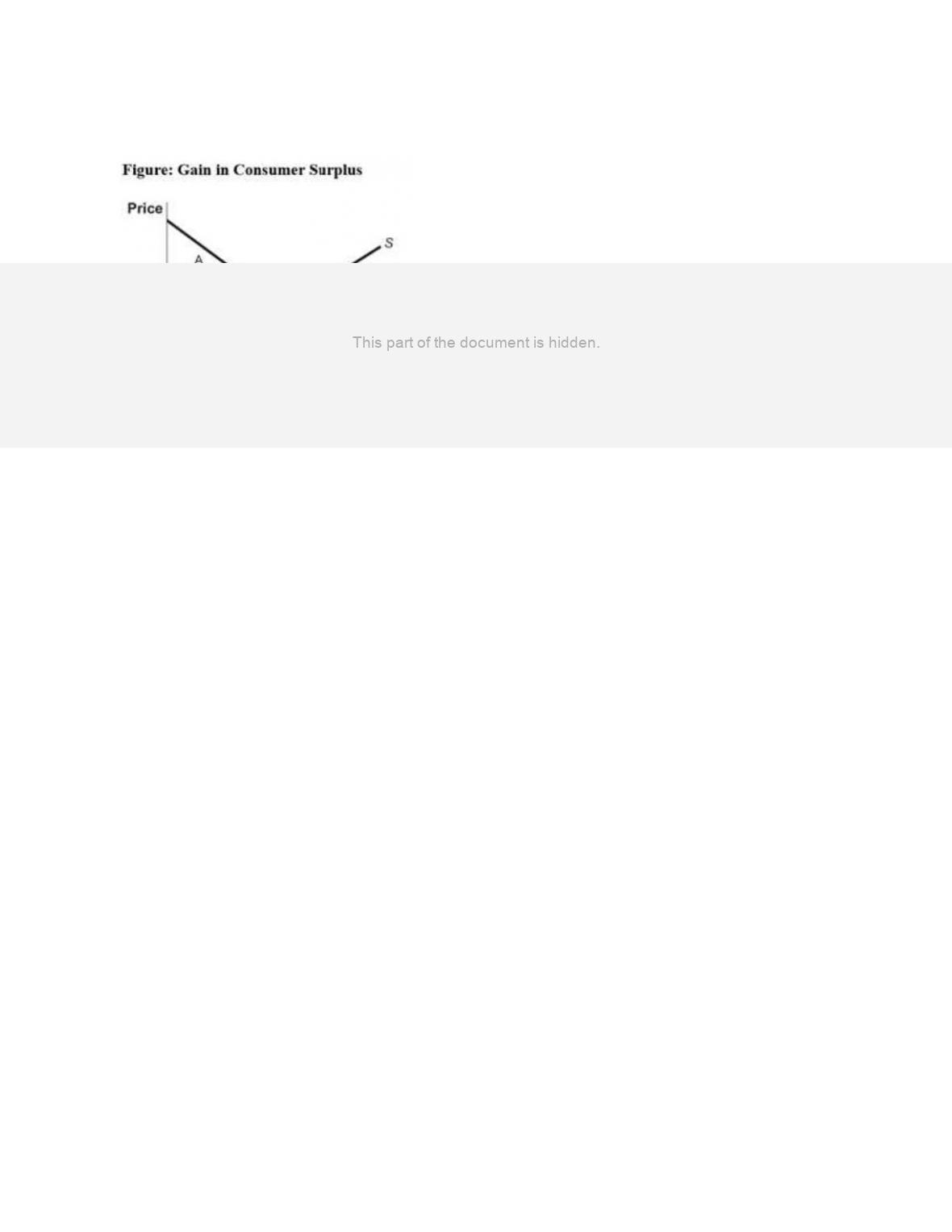

(Figure: Gain in Consumer Surplus) Look at the figure Gain in Consumer Surplus.

Identify the area or areas that represent the gain in consumer surplus to consumers

already participating in the market when the price falls from P1 to P2.

A)

A and B

B)

B

C)

B and C

D)

C

118.

(Figure: Gain in Consumer Surplus) Look at the figure Gain in Consumer Surplus.

Identify the area or areas that represent the total change in consumer surplus when the

price falls from P1 to P2.

A)

A and B

B)

B and C

C)

D and E

D)

A, B, and C

Page 33

Use the following to answer questions 119-120:

119.

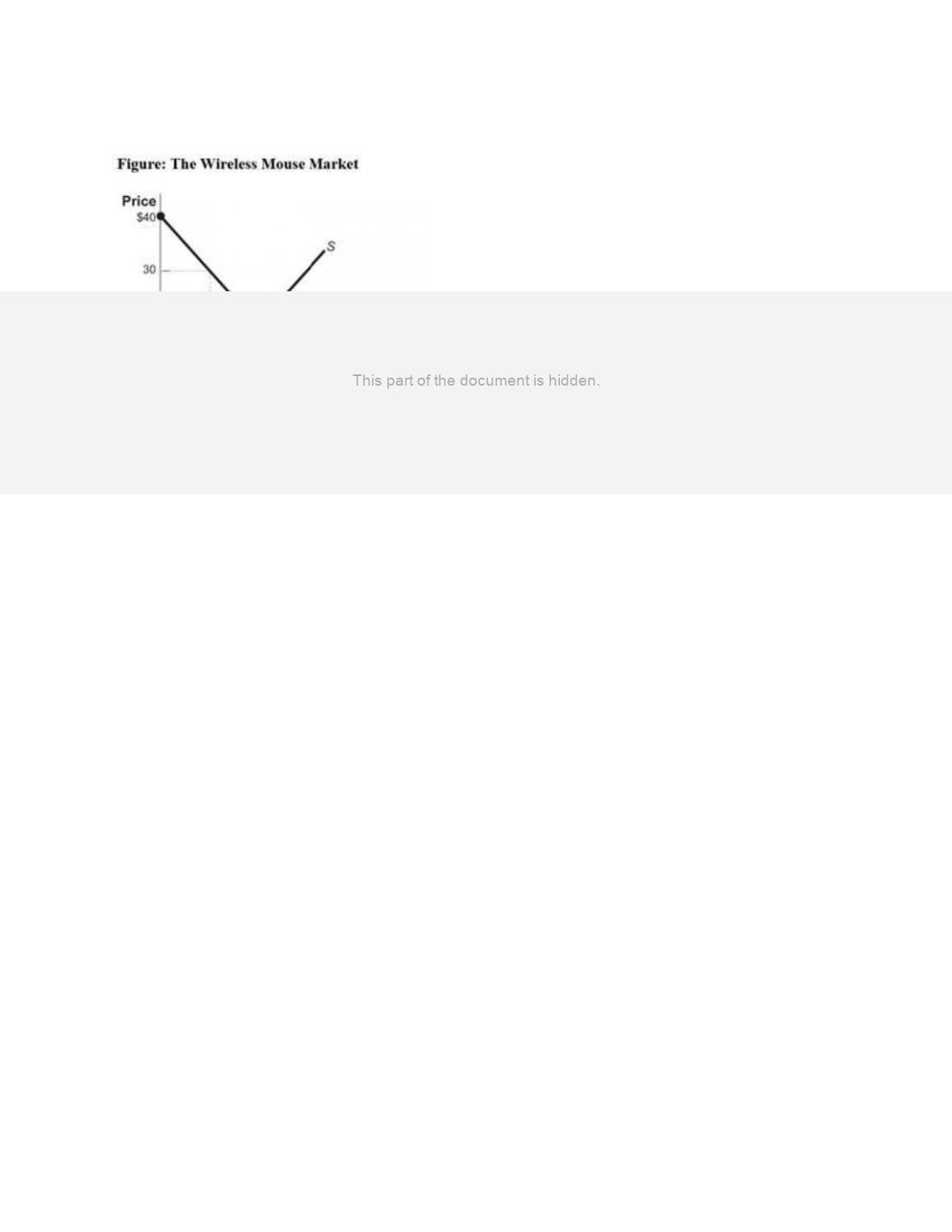

(Figure: Wireless Mouse Market) Look at the figure Wireless Mouse Market. Calculate

producer surplus when the market is in equilibrium.

A)

$4,000

B)

$2,000

C)

$8,000

D)

$1,000

120.

(Figure: Wireless Mouse Market) Look at the figure Wireless Mouse Market. Calculate

the change in producer surplus when the price increases from $10 to $15.

A)

$250

B)

$1,000

C)

$625

D)

$1,125

Page 34

Use the following to answer questions 121-122:

121.

(Figure: Change in Total Surplus) Look at the figure Change in Total Surplus. Which

areas represent the change in total surplus when the price falls from P1 to P2?

A)

A, B, and C

B)

B and C

C)

B, C, D, and E

D)

C and E

122.

(Figure: Change in Total Surplus) Look at the figure Change in Total Surplus. Which

areas represent the change in total surplus when the price falls from P2 to P3?

A)

A, B, and C

B)

B and C

C)

B, C, D, and E

D)

C and E

Page 35

Use the following to answer questions 123-127:

123.

(Figure: Consumer Surplus I) Look at the figure Consumer Surplus I. At a price of P1,

consumer surplus equals the area:

A)

ABP2.

B)

AFP1.

C)

AQ30.

D)

P1P2BF.

124.

(Figure: Consumer Surplus I) Look at the figure Consumer Surplus I. At a price of P2,

consumer surplus equals the area:

A)

ABP2.

B)

AFP1.

C)

AQ30.

D)

P1P2BF.

125.

(Figure: Consumer Surplus I) Look at the figure Consumer Surplus I. If the good is

being given away for free, consumer surplus equals the area:

A)

ABP2.

B)

AFP1.

C)

BGF.

D)

AQ30.

Page 36

126.

(Figure: Consumer Surplus I) Look at the figure Consumer Surplus I. If the price falls

from P2 to P1, consumer surplus increases by the area:

A)

ABP2.

B)

AFP1.

C)

BGF.

D)

P1P2BF.

127.

(Figure: Consumer Surplus I) Look at the figure Consumer Surplus I. If the price rises

from P1 to P2, consumer surplus decreases by the area:

A)

ABP2.

B)

AFP1.

C)

BGF.

D)

P1P2BF.

Use the following to answer questions 128-131:

128.

(Figure: Consumer Surplus II) Look at the figure Consumer Surplus II. If the price of

the good is $2, consumer surplus will equal:

A)

$30.

B)

$45.

C)

$60.

D)

$90.

Page 37

129.

(Figure: Consumer Surplus II) Look at the figure Consumer Surplus II. If the price of

the good is $4, consumer surplus will equal:

A)

$5.

B)

$10.

C)

$20.

D)

$40.

130.

(Figure: Consumer Surplus II) Look at the figure Consumer Surplus II. If the price of

the good increases from $3 to $4, consumer surplus will decrease by:

A)

$5.

B)

$10.

C)

$15.

D)

$20.

131.

(Figure: Consumer Surplus II) Look at the figure Consumer Surplus II. If the price of

the good decreases from $2 to $1, consumer surplus will increase by:

A)

$5.

B)

$10.

C)

$25.

D)

$35.

Use the following to answer questions 132-134:

Page 38

132.

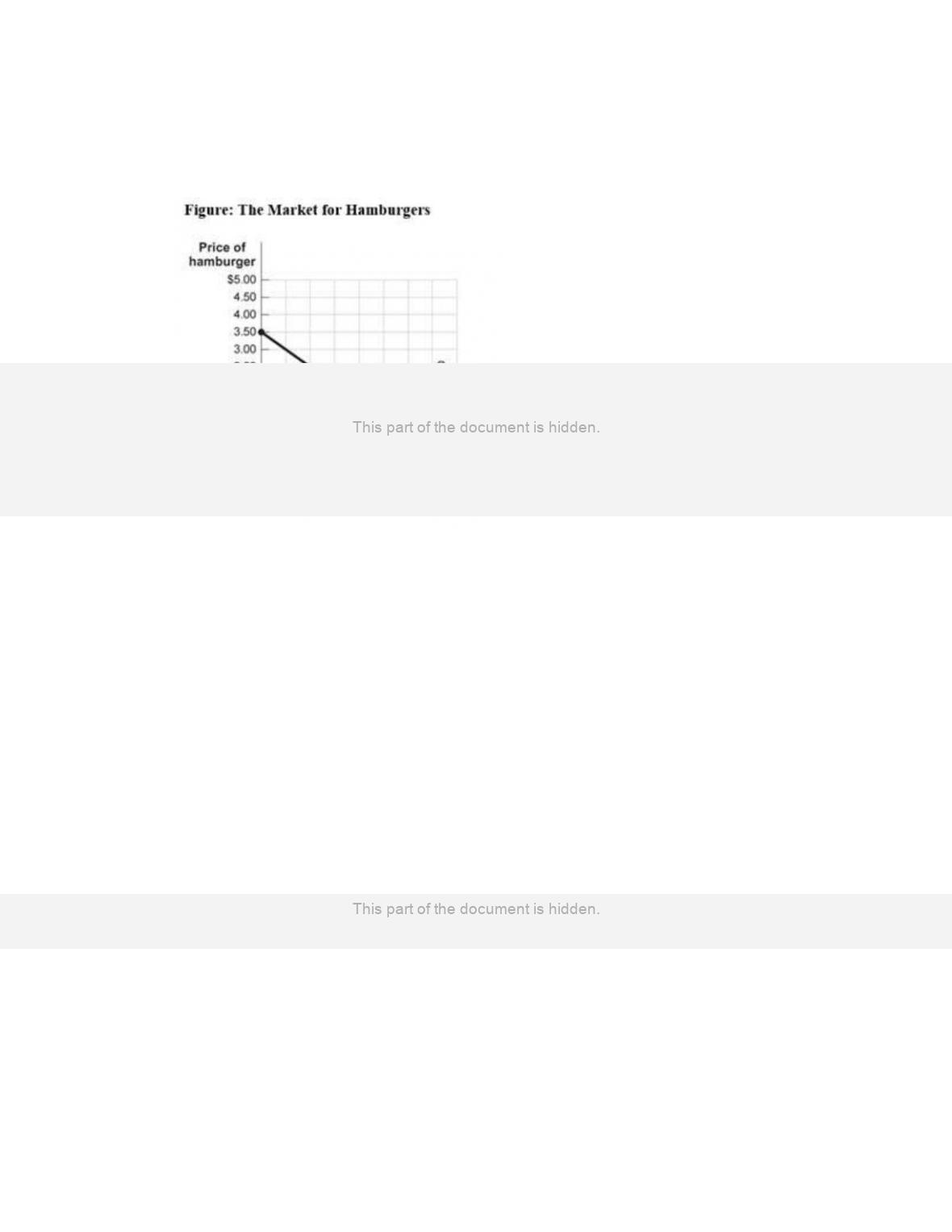

(Figure: The Market for Hamburgers) The figure The Market for Hamburgers shows the

weekly market for hamburgers in Tuscaloosa. If the price of a burger is $2, consumer

surplus will equal:

A)

$650.

B)

$400.

C)

$225.

D)

$450.

133.

(Figure: The Market for Hamburgers) The figure The Market for Hamburgers shows the

weekly market for hamburgers in Tuscaloosa. If 400 hamburgers are sold, consumer

surplus will equal:

A)

$650.

B)

$400.

C)

$225.

D)

$450.

134.

(Figure: The Market for Hamburgers) The figure The Market for Hamburgers shows the

weekly market for hamburgers in Tuscaloosa. If the price of a hamburger falls from

$2.00 to $1.50, the gain in consumer surplus to consumers who are persuaded to buy at

the lower price (and who were not buying when the price was $2.00) is equal to:

A)

$100.

B)

$75.

C)

$50.

D)

$25.

Page 39

Use the following to answer questions 135-137:

135.

(Figure: Consumer Surplus III) In the figure Consumer Surplus III, when the price falls

from $30 to $25, consumer surplus _____ for a total consumer surplus of _____.

A)

increases by $25; $74

B)

decreases by $15; $34

C)

increases by $15; $64

D)

increases by $5; $54

136.

(Figure: Consumer Surplus III) In the figure Consumer Surplus III, when the price rises

from $30 to $35, consumer surplus _____ for a total consumer surplus of _____.

A)

decreases by $15; $34

B)

increases by $15; $64

C)

increases by $25; $74

D)

decreases by $5; $44

137.

(Figure: Consumer Surplus III) In the figure Consumer Surplus III, total consumer

surplus is _____ when the price is $10.

A)

$50

B)

$59

C)

$124

D)

$144

Use the following to answer questions 138-150:

138.

(Table: Pumpkin Market) There are two consumers, Andy and Ben, in the market for

pumpkins. Their willingness to pay for each pumpkin is shown in the table Pumpkin

Market. There are two producers of pumpkins, Cindy and Diane, and their costs are also

shown. The equilibrium price for pumpkins is:

A)

$12.

B)

$10.

C)

$8.

D)

$6.

139.

(Table: Pumpkin Market) There are two consumers, Andy and Ben, in the market for

pumpkins. Their willingness to pay for each pumpkin is shown in the table Pumpkin

Market. There are two producers of pumpkins, Cindy and Diane, and their costs are also

shown. The equilibrium quantity of pumpkins is:

A)

two.

B)

three.

C)

four.

D)

five.

140.

(Table: Pumpkin Market) There are two consumers, Andy and Ben, in the market for

pumpkins. Their willingness to pay for each pumpkin is shown in the table Pumpkin

Market. There are two producers of pumpkins, Cindy and Diane, and their costs are also

shown. The equilibrium price for pumpkins is $8 and the equilibrium quantity is 5. At

the equilibrium price and quantity, Andy buys _____ pumpkins and his consumer

surplus is _____.

A)

four; $2

B)

three; $6

C)

two; $8

D)

one; $4