Page 21

103.

Suppose that a fall in commodity prices causes a supply shock. The short-run Phillips

curve will:

A)

shift down.

B)

show a movement along the same curve.

C)

not be affected at all.

D)

shift up.

104.

The negative relationship between the inflation rate and the unemployment rate is

known as the _____curve.

A)

short-run Phillips

B)

short-run aggregate supply

C)

long-run Phillips

D)

aggregate demand

105.

If the short-run Phillips curve has shifted upward, the _____ curve has shifted to the

_____.

A)

AD; right

B)

AD; left

C)

SRAS; right

D)

SRAS; left

106.

If the short-run Phillips curve has shifted downward, the _____ curve has shifted to the

_____.

A)

SRAS; left

B)

SRAS; right

C)

AD; left

D)

AD; right

107.

If there has been a downward movement along the fixed short-run Phillips curve, the

_____ curve has shifted to the _____.

A)

AD; left

B)

AD; right

C)

SRAS; left

D)

SRAS; right

Page 22

108.

If there has been an upward movement along the fixed short-run Phillips curve, the

_____ curve has shifted to the _____.

A)

SRAS; left

B)

SRAS; right

C)

AD; left

D)

AD; right

Use the following to answer questions 109-111:

109.

(Figure: AD–AS Model and the Short-Run Phillips Curve) Refer to Figure: AD–AS

Model and the Short-Run Phillips Curve. If the central bank increases the money supply

so that aggregate demand shifts from AD1 to AD2, then real GDP will increase by:

A)

zero.

B)

2%.

C)

4%.

D)

6%.

110.

(Figure: AD–AS Model and the Short-Run Phillips Curve) Refer to Figure: AD–AS

Model and the Short-Run Phillips Curve. If the central bank decreases the money supply

so that aggregate demand shifts from AD2 to AD1, then the unemployment rate will be:

A)

zero.

B)

2%.

C)

4%.

D)

6%.

Page 23

111.

(Figure: AD–AS Model and the Short-Run Phillips Curve) Refer to Figure: AD–AS

Model and the Short-Run Phillips Curve. If the central bank increases the money supply

so that aggregate demand shifts from AD1 to AD2, then the inflation rate will be:

A)

zero.

B)

2%.

C)

4%.

D)

6%.

112.

An increase in the expected rate of inflation:

A)

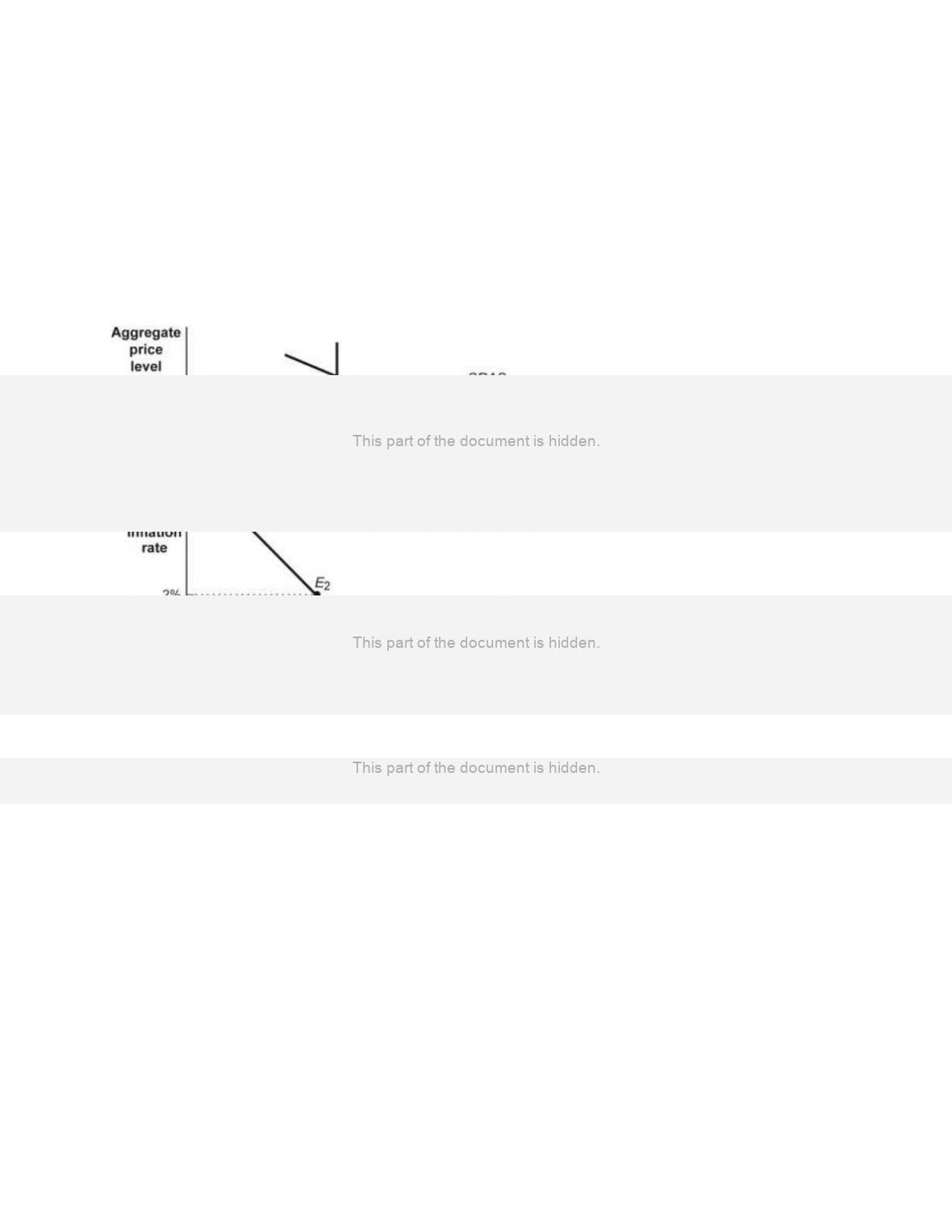

shifts the short-run Phillips curve down.

B)

shifts the short-run Phillips curve up.

C)

moves the economy along the short-run Phillips curve to higher rates of inflation.

D)

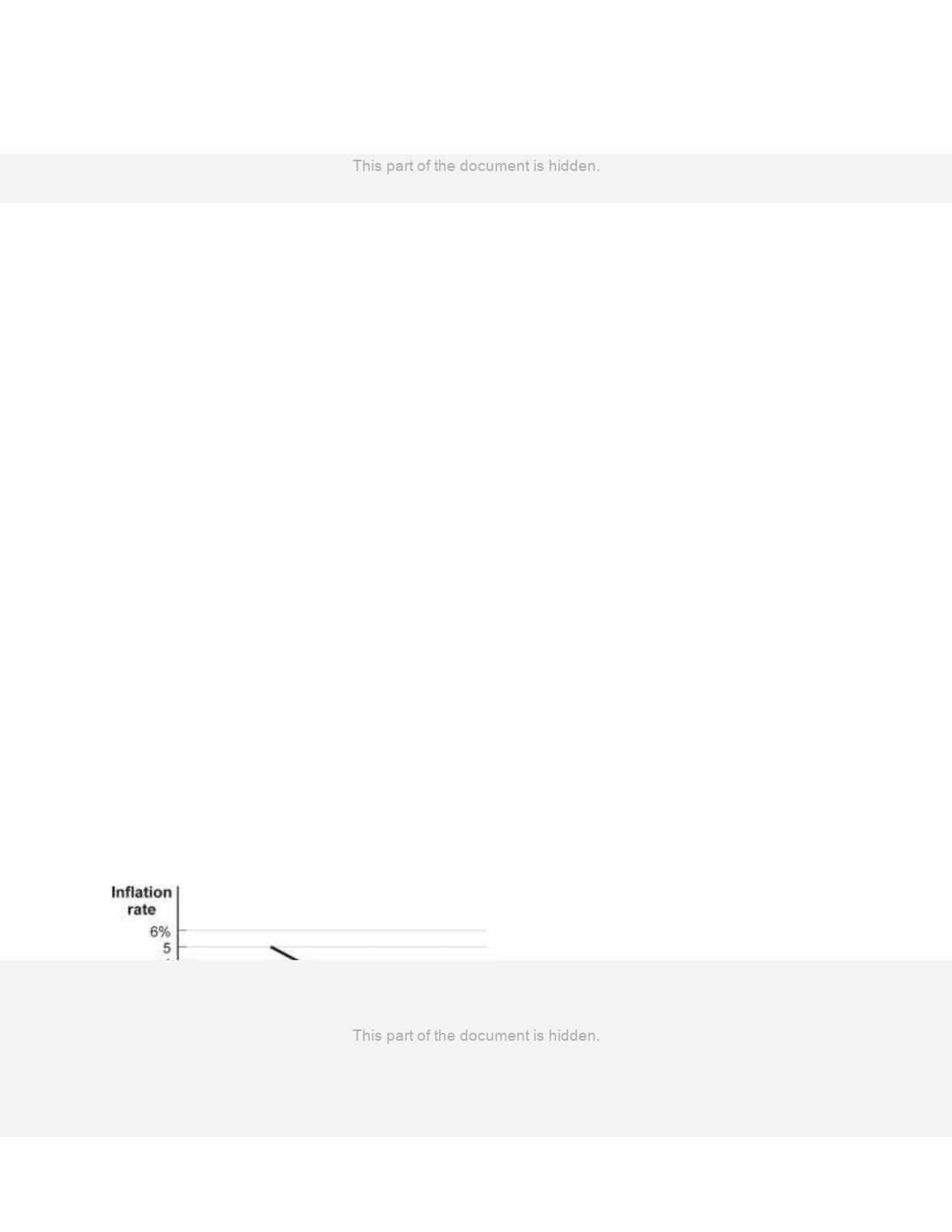

moves the economy along the short-run Phillips curve to higher rates on

unemployment.

113.

If workers expect a lower rate of inflation, the short-run Phillips curve will:

A)

remain constant, but there will be a movement down the curve.

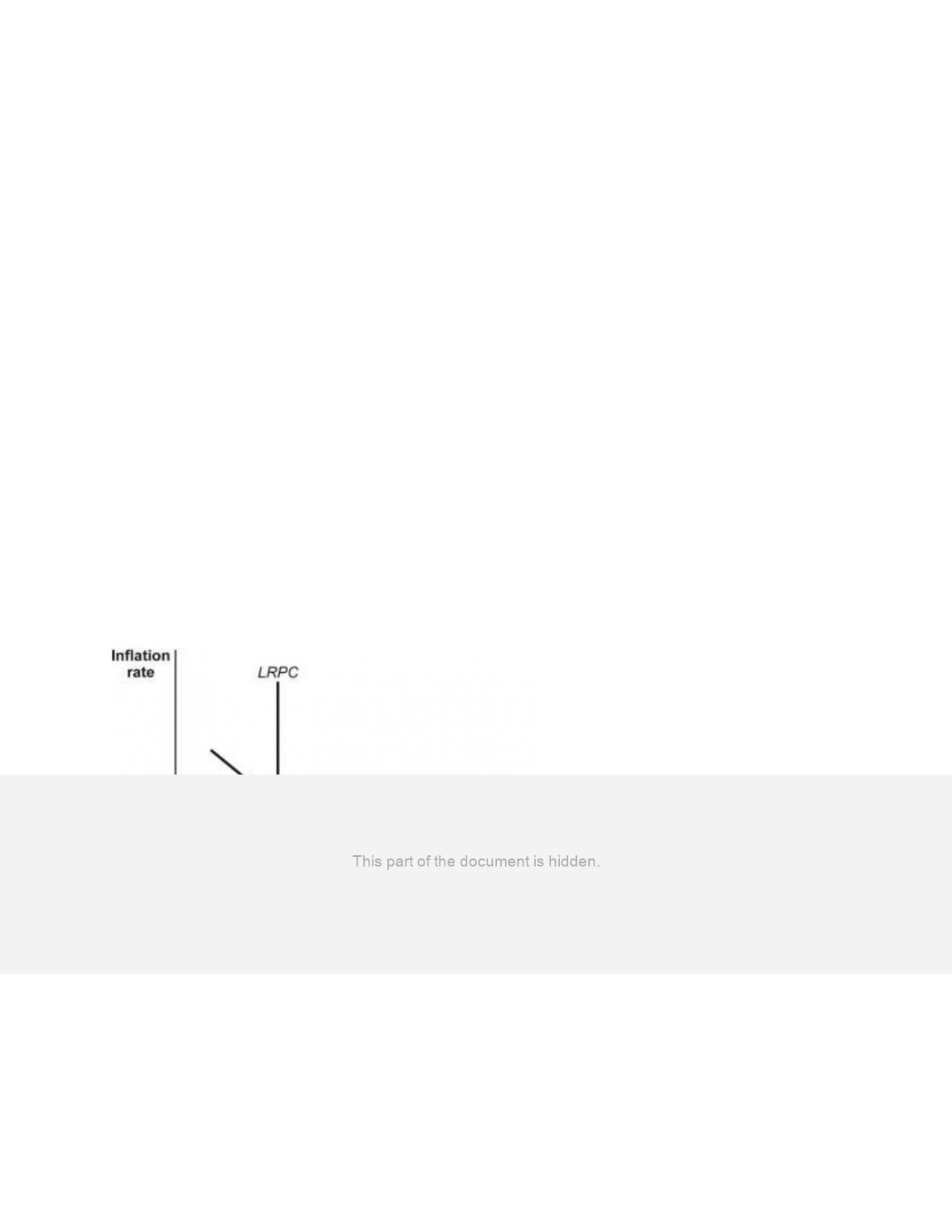

B)

be unaffected.

C)

shift up.

D)

shift down.

114.

Expectations of a higher inflation rate shift the short-run aggregate supply curve to the

_____, changing the trade-off between inflation and unemployment. As a result, the

short-run Phillips curve shifts _____.

A)

left; down

B)

right; up

C)

left; up

D)

right; down

Use the following to answer questions 115-116:

115.

(Figure: Expected Inflation and the Short-Run Phillips Curve) SRPC0 is the Phillips

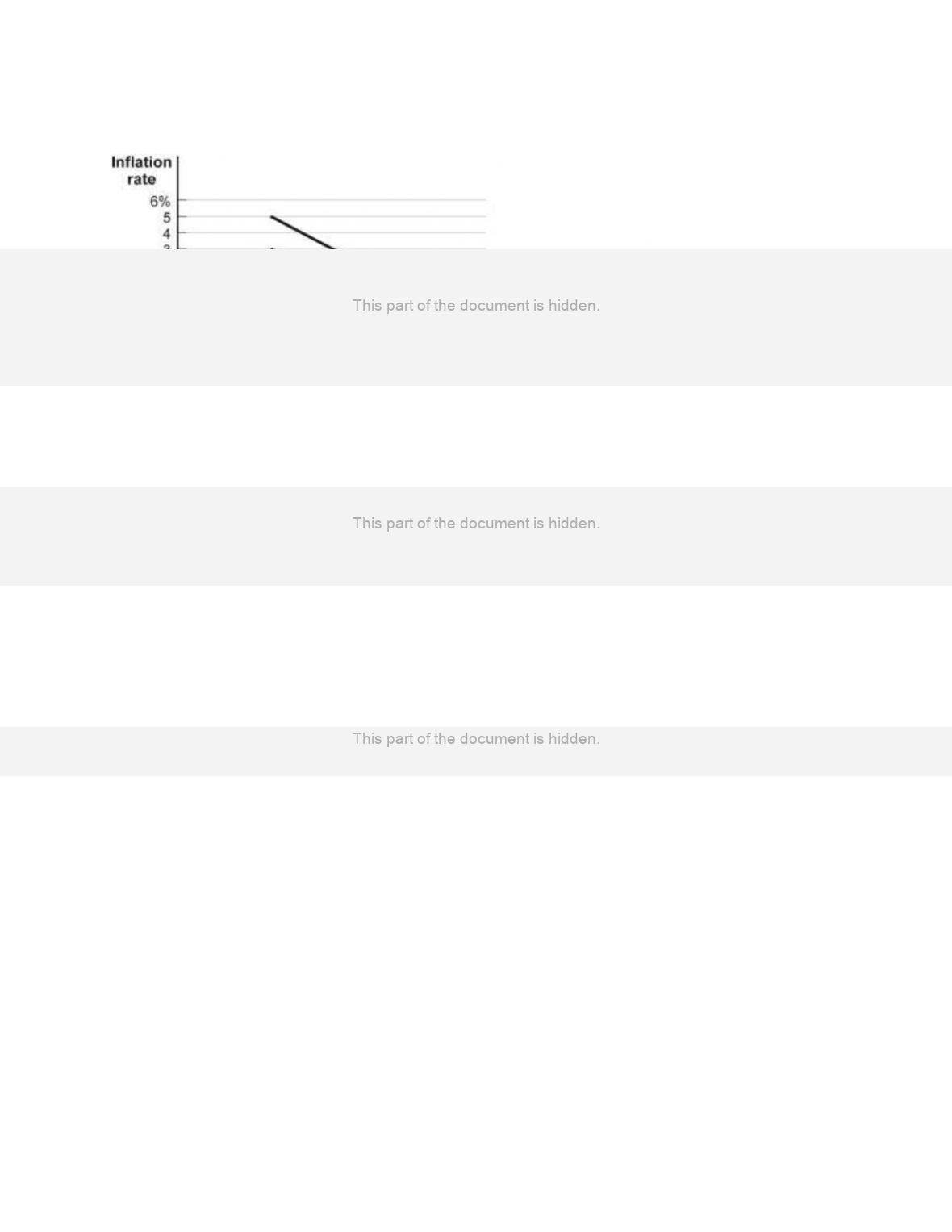

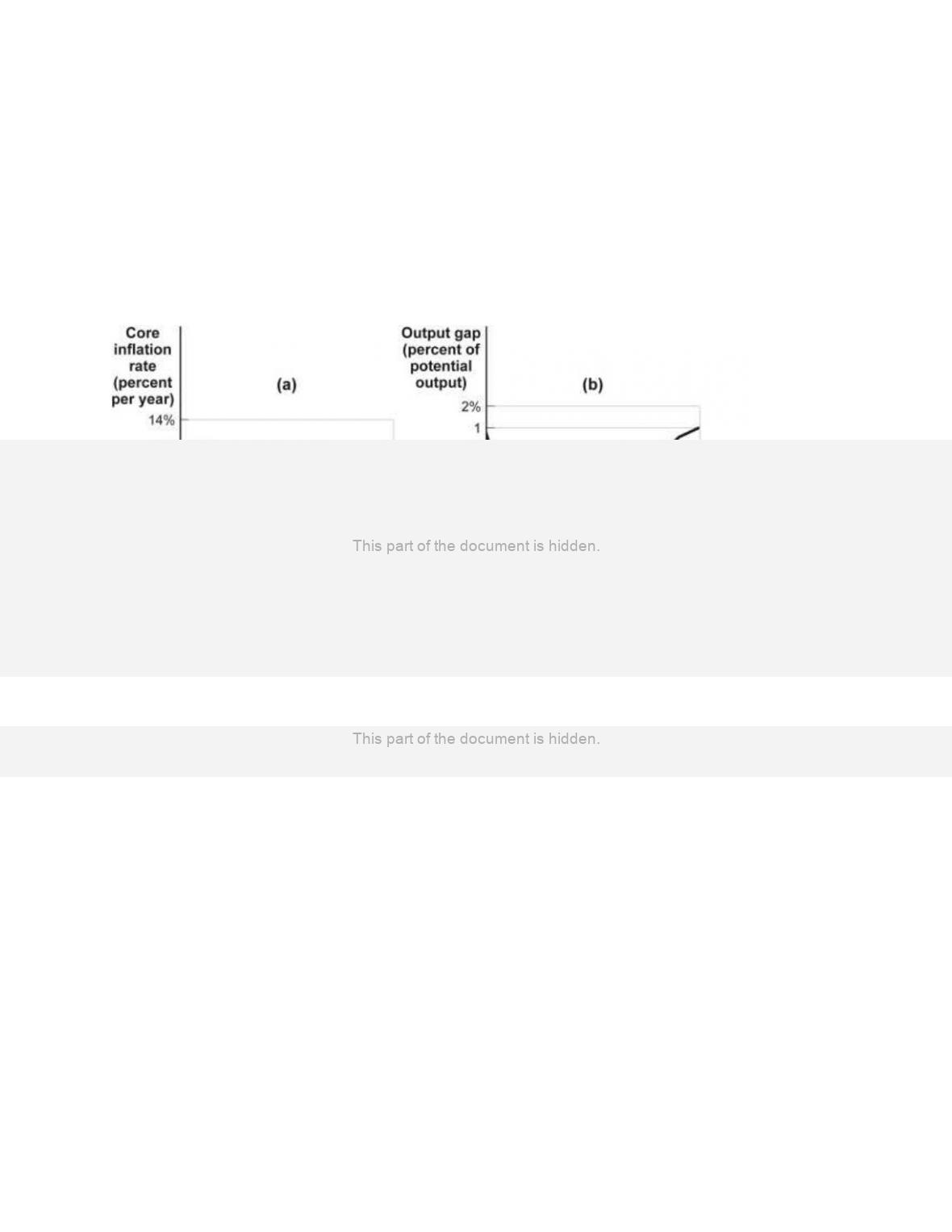

curve with an expected inflation rate of zero; SRPC2 is the Phillips curve with an

expected inflation rate of 2%.

Refer to Figure: Expected Inflation and the Short-Run Phillips Curve. Suppose that this

economy has an unemployment rate of 6%, no inflation, and no expectation of inflation.

If the central bank increases the money supply such that aggregate demand shifts to the

right and unemployment falls to 4%, then inflation will:

A)

fall to –2%.

B)

not change.

C)

rise to 2%.

D)

rise to 4%.

116.

(Figure: Expected Inflation and the Short-Run Phillips Curve) SRPC0 is the Phillips

curve with an expected inflation rate of zero; SRPC2 is the Phillips curve with an

expected inflation rate of 2%.

Refer to Figure: Expected Inflation and the Short-Run Phillips Curve. Suppose that this

economy has an unemployment rate of 6%, no inflation, and no expectation of inflation.

If the central bank decreases the money supply such that aggregate demand shifts to the

left and unemployment rises to 8%, then inflation will:

A)

fall to –2%.

B)

not change.

C)

rise to 2%.

D)

rise to 4%.

117.

(Figure: Expected Inflation and the Short-Run Phillips Curve) SRPC0 is the Phillips

curve with an expected inflation rate of zero; SRPC2 is the Phillips curve with an

expected inflation rate of 2%.

Refer to Figure: Expected Inflation and the Short-Run Phillips Curve. Suppose that this

economy has an unemployment rate of 6%, inflation of 2%, and an expectation of 2%

inflation. If the central bank increases the money supply such that aggregate demand

shifts to the right and unemployment falls to 4%, then inflation will:

A)

fall to –2%.

B)

not change.

C)

rise to 2%.

D)

rise to 4%.

Use the following to answer question 118:

118.

(Figure: Expected Inflation and the Short-Run Phillips Curve) SRPC0 is the Phillips

curve with an expected inflation rate of zero; SRPC2 is the Phillips curve with an

expected inflation rate of 2%.

Refer to Figure: Expected Inflation and the Short-Run Phillips Curve. Suppose that this

economy has an unemployment rate of 6%, inflation of 2%, and an expectation of 2%

future inflation. If the central bank decreases the money supply such that aggregate

demand shifts to the left and unemployment rises to 8%, then inflation will:

A)

fall to zero.

B)

not change.

C)

rise to 2%.

D)

rise to 4%.

119.

Suppose that commodity prices across the economy begin to fall and consumers and

firms begin to expect a lower rate of inflation. The SRAS curve will shift to the _____,

and the short-run Phillips curve will shift _____.

A)

left; downward

B)

right; downward

C)

left; upward

D)

right; upward

120.

An increase in expected inflation will affect the short-run Phillips curve:

A)

by shifting it downward; the actual rate of inflation at any given unemployment

rate will fall by the same amount.

B)

by shifting it upward; the actual rate of inflation at any given unemployment rate

will also be higher when the expected inflation rate is higher.

C)

by moving along the same curve, where it equals the actual rate of inflation.

D)

only if the economy is at the nonaccelerating inflation rate of unemployment.

Page 26

121.

The long-run Phillips curve is:

A)

the same as the short-run Phillips curve.

B)

negatively sloped, showing an inverse relationship between unemployment and

inflation.

C)

vertical at the nonaccelerating inflation rate of unemployment (NAIRU).

D)

unrelated to the NAIRU.

122.

Which shape accurately portrays the long-run Phillips curve?

A)

a horizontal curve

B)

a vertical curve

C)

an upward-sloping curve

D)

a downward-sloping curve

123.

A long-run Phillips curve has a(n) _____ slope because _____.

A)

negative; there is a positive relationship between the output gap and the

nonaccelerating inflation rate of unemployment (NAIRU)

B)

infinite; any unemployment rate below the NAIRU leads to ever-accelerating

inflation

C)

zero; there is a positive relationship between expected inflation and unemployment

D)

positive; any unemployment rate above the NAIRU leads to ever-accelerating

inflation

124.

As a consequence of the existence of a nonaccelerating inflation rate of unemployment:

A)

cyclical unemployment can never be zero.

B)

there is no short-run trade-off between unemployment and inflation.

C)

money is neutral.

D)

there is no long-run trade-off between unemployment and inflation.

125.

If the natural rate of unemployment _____, the nonaccelerating inflation rate of

unemployment _____, and the long-run Phillips curve shifts to the left.

A)

falls; falls

B)

rises; rises

C)

falls; rises

D)

rises; falls

Page 27

126.

When workers and firms become aware of a rise in the general price level:

A)

they will not do anything, because they know they are powerless to counter any

economic changes.

B)

they will incorporate higher prices into their expectations.

C)

firms with sticky prices will ultimately adjust their prices downward.

D)

they will agree to renegotiate wage contracts downward.

127.

In the long run, when the actual inflation rate gets embedded in people’s expectation:

A)

the trade-off between inflation and unemployment becomes even stronger.

B)

it is possible to achieve lower unemployment in the long run by accepting higher

inflation.

C)

there is no longer a trade-off between inflation and unemployment.

D)

actual inflation at any unemployment rate is always higher than expected inflation.

128.

The NAIRU is:

A)

the inflation rate at which the unemployment rate does not change over time.

B)

a trade-off between unemployment and inflation.

C)

the unemployment rate at which inflation does not change over time.

D)

a rate at which it is possible to achieve lower unemployment by accepting higher

inflation.

129.

The long-run Phillips curve shows the relationship between:

A)

potential aggregate output and the natural rate of unemployment at a given rate of

expected inflation.

B)

expected inflation and actual inflation after the expectation becomes embedded in

people’s minds.

C)

the aggregate output and the aggregate price level at a given rate of expected

inflation.

D)

unemployment and inflation after expectations of inflation have had time to adjust

to experience.

130.

The long-run Phillips curve is:

A)

vertical at an unemployment rate equal to the nonaccelerating inflation rate of

unemployment (NAIRU).

B)

horizontal at inflation rate equal to NAIRU.

C)

upward sloping, showing that there is no trade-off between unemployment and

inflation.

D)

downward sloping, showing that there is a trade-off between unemployment and

inflation.

Page 28

131.

The long-run Phillips curve is vertical at the nonaccelerating inflation rate of

unemployment (NAIRU) because an unemployment rate _____ the NAIRU will lead to

_____ inflation.

A)

below; ever-accelerating

B)

equal to; zero

C)

above; ever-accelerating

D)

below; ever-decelerating

Use the following to answer question 132:

132.

(Table: Combinations of Unemployment and Inflation) Refer to Table: Combinations of

Unemployment and Inflation. Which combination could lie on the same long-run

Phillips curve?

A)

W and Z

B)

W and Y

C)

X and Z

D)

X and Y

133.

Which statement accurately describes disinflation?

A)

It must be accompanied by a decline in the price level.

B)

The inflation rate rises at a higher rate.

C)

It is a reduction of the inflation.

D)

It is a gradual reduction in the price level over time.

134.

To bring disinflation to an economy, policy makers must:

A)

slow down labor productivity growth.

B)

increase the money supply to release the economy from the liquidity trap.

C)

keep unemployment below its natural rate for an extended period.

D)

announce and commit to a credible policy of disinflation.

Page 29

135.

If the Fed reduces the inflation rate from 5% to 3%, it is:

A)

following a policy rule.

B)

engaging in disinflation.

C)

increasing employment.

D)

raising economic growth.

136.

Disinflation means a decrease in:

A)

prices.

B)

the rate of inflation.

C)

aggregate supply.

D)

the money supply.

137.

The cost of disinflation is the:

A)

leftward shift in aggregate supply.

B)

decrease in prices.

C)

loss of real GDP in the process.

D)

loss of international markets when prices change.

138.

Disinflation is costly to the economy if _____ is forced on the economy, _____, and

_____.

A)

deflation; employment decreases; aggregate output falls

B)

increasing inflation; unemployment decreases; aggregate price level increases

C)

stagflation; unemployment increases; inflation increases

D)

a recession; unemployment increases; aggregate output falls

139.

Reduction of inflation that is embedded in expectations is called:

A)

disinflation.

B)

deflation.

C)

hyperinflation.

D)

the natural rate of inflation.

140.

Core inflation excludes the price of:

A)

new cars.

B)

luxury items, such as fur coats.

C)

houses.

D)

energy and food.

Page 30

141.

Analysis of the Phillips curve reveals that a _____ in unemployment, like that of the

early 1980s, is needed to break the cycle of inflationary expectations.

A)

permanent increase

B)

permanent decrease

C)

temporary increase

D)

temporary decrease

Use the following to answer question 142:

142.

(Figure: The Great Disinflation) Refer to Figure: The Great Disinflation. In the early

1980s, the inflation rate was beaten down by the Federal Reserve’s tight monetary

policy. In the short run this policy led to a _____ level of actual output and a _____ rate

of unemployment.

A)

high; high

B)

low; high

C)

low; low

D)

high; low

143.

The U.S. government reports a core inflation rate that excludes _____ and _____ prices

to remove the volatility of those two sectors from inflation estimates.

A)

housing; automobile

B)

steel; housing

C)

energy; food

D)

gasoline; housing

Page 31

144.

The measure used by the Fed that excludes food and energy prices is the:

A)

consumer price index.

B)

wholesale price index.

C)

core inflation rate.

D)

federal funds rate.

145.

The measure that the Fed regards as the best guide to underlying inflation is the:

A)

consumer price index.

B)

wholesale price index.

C)

core inflation rate.

D)

federal funds rate.

146.

Deflation:

A)

hurts borrowers and helps lenders.

B)

helps borrowers and hurts lenders.

C)

unlike inflation, affects neither borrowers nor lenders.

D)

affects only lenders.

147.

Deflation:

A)

can cause increases in output.

B)

can cause budget surpluses.

C)

can cause decreases in output.

D)

will not affect output.

148.

The problem of debt deflation deepens during an economic slump because:

A)

borrowers have to reduce spending to pay off debts.

B)

the Fisher effect raises the nominal interest rate during deflation.

C)

lenders have to reduce spending to accommodate higher returns from loans.

D)

the zero bound on the nominal interest rate is broken.

149.

Debt deflation is the _____ in aggregate _____ caused by deflation.

A)

increase; supply

B)

reduction; supply

C)

increase; demand

D)

reduction; demand

Page 32

150.

In debt deflation, deflation raises the cost of existing debt by increasing the value of

money needed to pay it off, leading to a(n) _____ in aggregate _____.

A)

increase; supply

B)

reduction; supply

C)

increase; demand

D)

reduction; demand

151.

Irving Fisher described debt deflation as:

A)

increasing aggregate demand and improving the economic downturn, leading to

less deflation.

B)

reducing aggregate demand and worsening the economic downturn, leading to

further deflation.

C)

reducing the debt obligation of borrowers as they become better off under

deflation.

D)

hurting lenders by reducing the value of their loans and lowering the interest rate

on loan.

152.

Irving Fisher argued that deflation is MOST likely to:

A)

expand the economy because the cost of goods has fallen.

B)

increase aggregate supply.

C)

increase aggregate demand.

D)

decrease aggregate demand.

153.

Who gains when there is unexpected deflation?

A)

real-asset owners

B)

borrowers

C)

lenders

D)

real-asset owners, borrowers, and lenders

154.

Who loses when there is unexpected deflation?

A)

nominal-asset holders

B)

borrowers

C)

lenders

D)

nominal-asset holders, borrowers, and lenders

155.

Deflation leads to winners and losers; for example:

A)

mortgage holders lose, but banks awaiting mortgage payments benefit.

B)

landlords lose, but people paying rent gain.

C)

savings account holders lose, but the banks gain.

D)

bond and stock holders lose, but the brokerage company gains.

Page 33

156.

During periods of deflation _____ will be hurt and _____ will be helped.

A)

firms; borrowers

B)

borrowers; lenders

C)

consumers; firms

D)

home buyers; home sellers

157.

When economists state that there is a zero bound on nominal interest rates, they mean

that the:

A)

real interest rate cannot go below zero.

B)

nominal interest rate cannot go below zero.

C)

real interest rate can very well be negative.

D)

nominal interest rate can always go below zero.

158.

The inability to use monetary policy because the nominal rate of interest cannot fall

below zero is called:

A)

liquidity preference.

B)

money neutrality.

C)

liquidity trap.

D)

money illusion.

159.

If the economy is in a liquidity trap, monetary policy is _____ and fiscal policy is

_____.

A)

effective; effective

B)

ineffective; ineffective

C)

effective; ineffective

D)

ineffective; effective

160.

There is a zero bound to:

A)

the real money supply.

B)

nominal interest rates.

C)

potential output.

D)

real money demand.

161.

Liquidity traps are most likely to occur when the:

A)

economy is going through a recovery.

B)

economy is expanding rapidly.

C)

public expects inflation.

D)

public expects deflation.

Page 34

162.

Expecting the inflation rate to be 3%, Tony decides to put his savings in a 12-month

certificate of deposit yielding a fixed 6% interest rate. If the actual inflation rate is

_____, it can be argued that _____ is/are worse off.

A)

above 3%; the bank issuing the certificate

B)

exactly 6%; both the bank and Tony

C)

below 3%; Tony

D)

below 3%; the bank issuing the certificate

163.

Expecting the inflation rate to be 3%, Adrianna decides to put her savings in bonds

yielding a fixed 5% interest rate over a year. If the actual inflation rate is _____, it can

be argued that _____ is/are better off.

A)

below 3%; Adrianna

B)

exactly 5%; both the bond issuer and Adrianna

C)

above 3%; Adrianna

D)

below 3%; the bond issuer

164.

In a liquidity trap:

A)

using expansionary monetary policy is not effective because the real interest rate is

negative.

B)

aggregate demand falls because consumers do not have enough liquidity to

consume.

C)

using expansionary monetary policy is not effective because the nominal interest

rate is irreducible.

D)

lenders are trapped by large loans with declining rates of return.

165.

A liquidity trap results from:

A)

the inflation tax.

B)

expansionary fiscal policy.

C)

the Fisher effect.

D)

the zero bound of the nominal interest rate.

166.

If there is too much deflation:

A)

people will switch from money to real assets.

B)

the nominal interest rate will be constrained by the zero interest rate bound.

C)

lenders will be harmed.

D)

aggregate demand will increase.

Page 35

167.

The liquidity trap is NOT associated with:

A)

a large reduction in the demand for loanable funds.

B)

the nominal interest rate falling to zero.

C)

monetary policy becoming ineffective.

D)

fiscal policy becoming ineffective.

168.

To avoid falling into a liquidity trap, most central banks:

A)

seek a positive but small inflation rate rather than zero inflation.

B)

target inflation rather than the money supply.

C)

conduct open-market operations to change the money supply instead of changing

the discount rate.

D)

aim at a target of zero inflation so that inflation expectations are zero too.

169.

When Fed officials worried about the possibility of “Japanification” in the United

States, it meant that they were worried that the U.S. economy would:

A)

grow faster than the economy of Japan after World War II.

B)

accumulate large trade surpluses, like Japan.

C)

fall into a period of hyperinflation.

D)

fall into a deflationary trap.

Use the following to answer questions 170-173: