Page 1

Name: __________________________ Date: _____________

1.

Money is anything that:

A)

serves as a medium of exchange for goods and services.

B)

can be converted to silver with relatively little loss in value.

C)

can be converted to gold with relatively little loss in value.

D)

is traded in the stock market.

2.

Money is:

A)

paper money and coins but not checks.

B)

currency and stocks.

C)

anything that can easily be used to buy goods and services.

D)

paper money but not coins.

3.

An economy that lacks a medium of exchange must use a(n) _____ system.

A)

anarchist

B)

barter

C)

communist

D)

expanding

4.

Which asset is the MOST liquid?

A)

a $50 bill

B)

a $50 gift certificate

C)

100 shares of stock

D)

an economics textbook

5.

Which combination of assets is considered to be money?

A)

currency in circulation, checkable bank deposits, and credit cards

B)

currency in circulation, checkable bank deposits, and traveler’s checks

C)

currency in circulation and in bank vaults, checkable bank deposits, and traveler’s

checks

D)

currency in circulation and in bank vaults, checkable bank deposits, and credit

cards

6.

Which asset would NOT fit the economist’s definition of money?

A)

currency

B)

checkable bank deposits

C)

coins

D)

bonds

Page 2

7.

Which asset is the MOST liquid?

A)

checkable bank deposits

B)

currency

C)

stocks

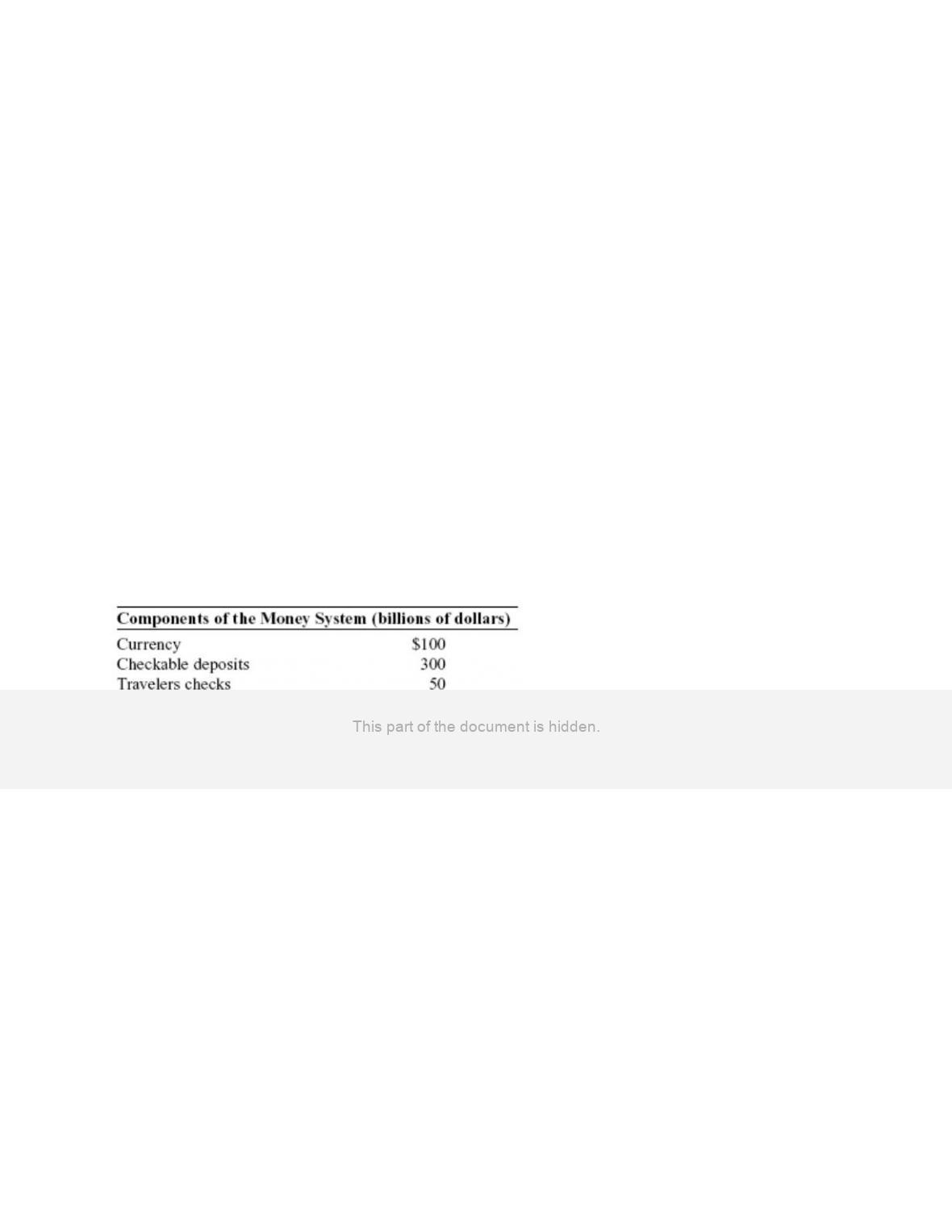

D)

money market mutual funds

8.

Which asset is one that most people would consider money?

A)

a house

B)

shares of stock in a company

C)

a checking account balance

D)

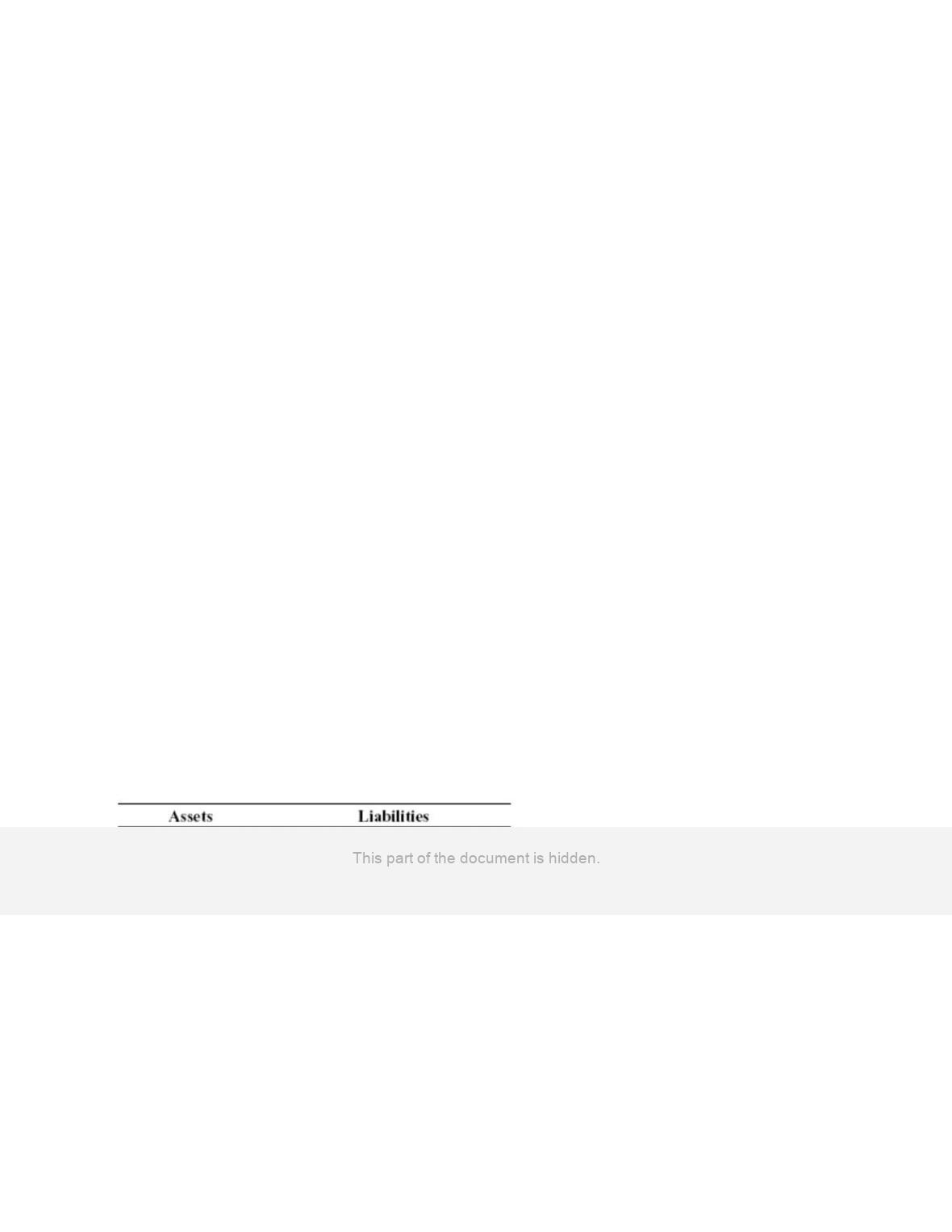

a car

9.

Money is any asset that:

A)

the government says is money.

B)

can easily be used to purchase goods and services.

C)

has a positive value.

D)

the government says is money and that has a positive value.

10.

Which asset is money?

A)

a $20 bill

B)

a work of art

C)

a baseball signed by a famous player

D)

shares of stock in a profitable company

11.

Which asset is considered to be money?

A)

stock

B)

bonds

C)

credit cards

D)

checkable bank deposits

12.

The double coincidence of wants problem can be solved by:

A)

more resources.

B)

more production.

C)

money.

D)

economic growth.

Page 3

13.

An example of a double coincidence of wants is:

A)

a car mechanic who wants a TV finding an owner of an electronics store who

wants a car repaired.

B)

a car dealer who wants a TV finding an electronics store owner who wants money.

C)

an electronics store owner who wants car repairs finding a car mechanic who wants

money.

D)

a car dealer who wants a new employee finding a car mechanic who wants money.

14.

The narrowest definition of money does NOT include:

A)

currency in the vault at the bank.

B)

traveler’s checks.

C)

currency in circulation.

D)

checkable bank deposits.

15.

Currency in circulation is cash:

I. held by the public.

II. in the vaults of commercial banks.

III. in the vault of the Federal Reserve.

A)

I only

B)

II only

C)

III only

D)

I, II, and III

16.

Which example is NOT a role of money?

A)

measure of wealth

B)

medium of exchange

C)

unit of account

D)

store of value

17.

When you are using money to purchase a new car, money is serving as a:

A)

store of value.

B)

medium of exchange.

C)

unit of account.

D)

double coincidence of wants.

Page 4

18.

Suppose a group of people decided to set up their own economic system with cartons of

milk serving as money. If we decided to use this “liquid asset” as our medium of

exchange and all prices were measured in cartons of milk, milk would still not be a good

form of money mainly because it would not be a good:

A)

medium of exchange.

B)

unit of account.

C)

store of value.

D)

near-money.

19.

“Tuition at State University this year is $8,000.” Which function of money does this

statement best illustrate?

A)

store of value

B)

medium of exchange

C)

unit of account

D)

means of deferred payment

20.

Which statement is NOT considered one of the three chief characteristics of money?

A)

It serves as a medium of exchange.

B)

It acts as a store of value.

C)

It is a highly illiquid asset.

D)

It is a unit of account.

21.

Money used to buy groceries is a:

A)

medium of exchange.

B)

reserve of wealth.

C)

unit of account.

D)

store of value.

22.

The medium-of-exchange function means that money is used:

A)

as the common denominator of prices.

B)

as the common denominator of future payments.

C)

to pay for goods and services.

D)

to accumulate purchasing power.

23.

Money used to buy a ticket to a football game is functioning primarily as a:

A)

medium of exchange.

B)

store of value.

C)

unit of account.

D)

standard of deferred payment.

Page 5

24.

The functions of money are:

A)

expander of economic activity, medium of exchange, and store of value.

B)

medium of exchange, store of value, and factor of production.

C)

store of value, medium of exchange, and determinant of investment.

D)

store of value, unit of account, and medium of exchange.

25.

When a person makes price comparisons among products, money is being used mainly

as a(n):

A)

unit of account.

B)

expander of economic activity.

C)

medium of exchange.

D)

checkable deposit.

26.

When you buy a ticket to the rodeo, you are using money as mainly a(n):

A)

expander of economic activity.

B)

store of value.

C)

factor of production.

D)

medium of exchange.

27.

When you discover money in your coat that you put there last winter, you unexpectedly

find you were using money primarily as a(n):

A)

medium of exchange.

B)

expander of economic activity.

C)

factor of production.

D)

store of value.

28.

When we keep part of our wealth in a savings account, money is playing the role mainly

of:

A)

medium of exchange.

B)

unit of account.

C)

barter.

D)

store of value.

29.

When we put a price on a meal, money is playing the role primarily of:

A)

medium of exchange.

B)

unit of account.

C)

barter token.

D)

store of value.

Page 6

30.

When people purchase downloaded music, they are using money primarily as a:

A)

medium of exchange.

B)

store of value.

C)

unit of account.

D)

store of account.

31.

The store-of-value function of money is:

A)

necessary and distinctive.

B)

not necessary but distinctive.

C)

necessary but not distinctive.

D)

not necessary and not distinctive.

32.

When you or your parents pay the tuition at college, money is being used mainly as a:

A)

unit of account.

B)

store of value.

C)

medium of exchange.

D)

unit of account, a store of value, and a medium of exchange.

33.

When you are looking at a car’s price to decide whether you can afford it, you are using

money primarily as a:

A)

unit of account.

B)

store of value.

C)

medium of exchange.

D)

medium of exchange and a unit of account.

34.

When, in The Wealth of Nations, Adam Smith wrote of “a sort of waggon-way through

the air,” he was referring to:

A)

the invisible hand.

B)

the forces of competition.

C)

mass transit systems of the future.

D)

paper money.

35.

Commodity-backed money is:

A)

a medium of exchange with no intrinsic value.

B)

equivalent to commodity money.

C)

a medium of exchange with alternative economic uses.

D)

gold and silver coins used for exchange.

Page 7

36.

When countries replaced gold and silver coins with paper money exchangeable for

certain amounts of precious metals, the monetary system evolved from using _____

money to using _____ money.

A)

commodity; fiat

B)

commodity-backed; fiat

C)

commodity; commodity-backed

D)

fiat; commodity-backed

37.

Commodity money is:

A)

whatever the government has decreed is money.

B)

a good used as a medium of exchange that has other uses.

C)

money used for commodity futures trading.

D)

whatever people accept as money.

38.

Money that has value apart from its use as money is:

A)

fiat money.

B)

currency.

C)

convertible paper money.

D)

commodity money.

39.

Money that the government has ordered to be accepted as money is:

A)

fiat money.

B)

not usable in international transactions.

C)

convertible paper money.

D)

commodity money.

40.

Money that some authority, generally a government, has ordered to be accepted as a

medium of exchange is called _____ money.

A)

fiat

B)

intrinsic

C)

bank-created

D)

debt

41.

Currency in the United States today is _____ money.

A)

fiat

B)

intrinsic

C)

commodity

D)

commodity-backed

Page 8

42.

Money whose value derives entirely from its official status as a means of exchange is

known as:

A)

commodity money.

B)

commodity-backed money.

C)

fiat money.

D)

bank reserves.

43.

The U.S. dollar is an example of:

A)

commodity-backed money.

B)

fiat money.

C)

commodity money.

D)

near-money.

44.

The U.S. dollar is defined as:

A)

fiat money, because it was established as money by an act of law.

B)

faith money, because we trust the government to defend its value.

C)

commodity-backed money, because it is convertible to gold.

D)

commodity money, because it is widely used to buy commodities.

45.

Fiat money:

A)

is currency from Italy.

B)

can include currency backed by gold but not by silver.

C)

is currency backed by the gold in Fort Knox.

D)

has advantages over commodity-backed money.

46.

The U.S. dollar in your pocket today is BEST described as:

A)

commodity money.

B)

near-money.

C)

fiat money.

D)

commodity-backed money.

47.

A share of stock is considered:

A)

an asset for the owner of the stock.

B)

part of M2.

C)

a liability for the owner of the stock.

D)

part of the money supply.

Page 9

48.

A bond is considered:

A)

an asset for the owner and is not part of the money supply.

B)

M1.

C)

M2.

D)

a liability for the owner and is part of the money supply.

49.

The primary difference between M1 and M2 is that:

A)

the dollar amount of M1 is much larger than the dollar amount of M2.

B)

M1 includes checkable deposits, but M2 does not.

C)

M2 includes checkable deposits, but M1 does not.

D)

M2 includes savings deposits and time deposits, but M1 does not.

50.

Suppose you find a $50 bill that you put in a coat pocket last winter. If you deposit it in

your checking account:

A)

M1 increases by $50.

B)

M2 increases by $50.

C)

M1 and M2 both increase by $50.

D)

there is no change in M1 or M2.

51.

If you transfer $1,000 from your savings account to your checking account:

A)

M1 decreases by $1,000, and M2 increases by $1,000.

B)

M1 increases by $1,000, and M2 decreases by $1,000.

C)

M1 and M2 don’t change.

D)

M1 increases by $1,000, but M2 doesn’t change.

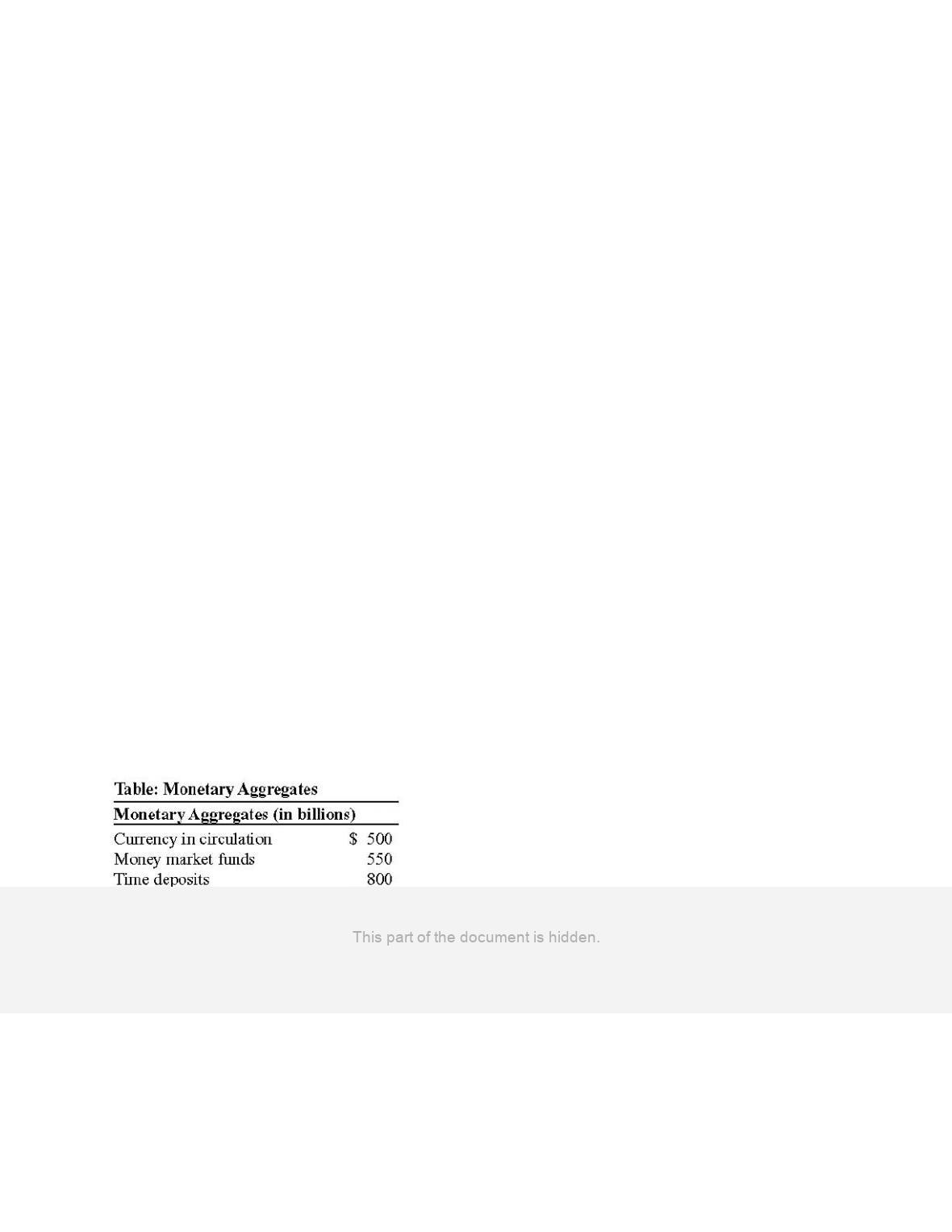

Use the following to answer questions 52-53:

Page 10

52.

(Table: Monetary Aggregates) Refer to Table: Monetary Aggregates. The value of M1

is:

A)

$880 billion.

B)

$895 billion.

C)

$2,005 billion.

D)

$920 billion.

53.

(Table: Monetary Aggregates) Refer to Table: Monetary Aggregates. The value of M2

is:

A)

$2,805 billion.

B)

$3,340 billion.

C)

$3,355 billion.

D)

$2,005 billion.

54.

Suppose that Ronny decides to withdraw all of the cash from his checking account and

open a single time deposit account at the same bank. As a result of this transaction:

A)

M2 falls but M1 remains unchanged.

B)

M1 and M2 both fall.

C)

M1 and M2 both remain unchanged.

D)

M1 falls but M2 remains unchanged.

55.

Which asset is NOT included in M1?

A)

savings deposits

B)

checkable bank deposits

C)

currency

D)

traveler’s checks

56.

If monetary aggregates were ranked from most liquid to least liquid, the order would be:

A)

M1 and M2.

B)

stocks and bonds, M2, and M1.

C)

M2, private equity investments, and M1.

D)

gold, M1, and M2.

57.

Which statement is TRUE?

A)

M2 includes the gold stock but not M1.

B)

M2 includes M1.

C)

The gold stock backs M2 but not M1.

D)

M1 includes M2 but not the gold stock.

Page 11

58.

Saving deposits are counted in:

A)

M1 but not in M2.

B)

vault cash but not in M2.

C)

M2 but not in M1.

D)

M1, M2, and the gold stock.

59.

The LARGEST monetary aggregate is:

A)

M1, because it contains all of the currency in circulation.

B)

M2, because it contains currency in circulation, all bank deposits, other deposits,

and deposit-like assets.

C)

the reserves in the vaults of Federal Reserve banks, because they are the money

multiplier.

D)

the total volume of stocks and bonds, because they store most of the national

wealth.

60.

Which asset is near-money?

A)

a traveler’s check

B)

a credit card

C)

a debit card

D)

a savings account

61.

Which financial asset belongs to M2 but not to M1?

A)

a savings account

B)

a checkable deposit

C)

currency

D)

traveler’s checks

62.

When a waiter deposits his cash tips in his savings account:

A)

M2 increases.

B)

M1 decreases.

C)

M2 decreases.

D)

M3 increases.

63.

Included in M1 are:

A)

checkable bank deposits.

B)

savings deposits.

C)

U.S. Treasury bills.

D)

demand deposits, savings deposits, and U.S. Treasury bills.

Page 12

64.

Included in M2 is/are:

A)

currency in circulation only.

B)

money market funds only.

C)

traveler’s checks only.

D)

currency in circulation, money market funds, and traveler’s checks.

65.

If the currency in circulation is $100 million, checkable bank deposits are $500 million,

savings deposits are $300 million, and traveler’s checks are $10 million, then M1 is:

A)

$100 million.

B)

$410 million.

C)

$610 million.

D)

$900 million.

66.

Suppose you transfer $500 from your checking account to your savings account. With

this transaction, M1 _____ and M2_____.

A)

increases; stays the same

B)

stays the same; increases

C)

decreases; increases

D)

decreases; stays the same

67.

Suppose you transfer $500 from your savings account to your checking account. With

this transaction, M1 _____ and M2 _____.

A)

increases; decreases

B)

increases; stays the same

C)

decreases; decreases

D)

stays the same; decreases

68.

Which asset is part of M1?

A)

short-term certificates of deposit

B)

shares of corporate stock

C)

currency in a bank’s vault

D)

checkable bank deposits

69.

Which asset is part of M1?

A)

long-term certificates of deposit

B)

corporate bonds

C)

currency in a person’s purse

D)

money market fund account balances

Page 13

70.

Which asset is part of M1?

A)

gold

B)

shares of corporate stock

C)

currency in a bank’s vault

D)

traveler’s checks

71.

M1 consists of:

A)

currency only.

B)

currency and checkable bank deposits only.

C)

currency in circulation and checkable bank deposits only.

D)

currency in circulation, checkable bank deposits, and traveler’s checks only.

72.

The Federal Reserve reports on two main monetary aggregates:

A)

M2 and total debt.

B)

M1 and currency held by banks.

C)

M1 and M2.

D)

M1 and total stock purchases.

Use the following to answer question 73:

73.

(Table: Components of the Money System) Refer to Table: Components of the Money

Supply. The money supply measured by M1 is:

A)

$325 billion.

B)

$450 billion.

C)

$1,425 billion.

D)

$1,875 billion.

Page 14

74.

Currency, checkable deposits, and traveler’s checks are about _____% of M1.

A)

10

B)

55

C)

75

D)

100

75.

Near-moneys are:

A)

paper money.

B)

fiat money.

C)

highly liquid financial assets.

D)

any financial assets.

76.

Prior to the Civil War:

A)

the U.S. government issued paper money but only in small quantities.

B)

the U.S. government did not allow banks to issue private money.

C)

the U.S. government did not issue paper money.

D)

all private money issued by banks was of equal value.

77.

After 1873, the U.S. government:

A)

stopped redeeming greenbacks for gold.

B)

guaranteed the value of a dollar in terms of gold.

C)

guaranteed the value of a dollar in terms of gold or silver.

D)

stopped the use of commodity-backed money.

78.

Which asset was used as money by European settlers in the American colonies before

the Revolutionary War?

I. dixies

II. tobacco

III. paper money issued by the newly established Federal Reserve

A)

I only

B)

II only

C)

III only

D)

I, II, and III

79.

In the nineteenth century, before the Civil War, most commodity-backed money in the

United States was:

A)

issued by the Treasury Department.

B)

issued by the Federal Reserve and redeemable for gold coins.

C)

issued by private banks and redeemable for silver coins.

D)

borrowed from banks in Europe.

Page 15

80.

Banks don’t lend out all of the funds deposited because:

A)

it would not be profitable.

B)

they have to satisfy any depositor who wants to withdraw funds.

C)

they have to reduce their liquidity position.

D)

they have to make more money on interest-bearing deposits.

81.

Bank reserves are:

A)

the fraction of deposits kept in gold with the Federal Reserve.

B)

the deposits lent to finance illiquid investments.

C)

the fraction of deposits kept in the form of very liquid assets.

D)

gold kept in the bank’s vault.

82.

Banks can lend money because:

A)

they have so much to lend.

B)

they know not everyone wants their deposits back at the same time.

C)

there is a high demand for commodity money.

D)

they don’t know how much cash they have in their vault.

83.

The reserve ratio is the:

A)

bank’s holdings of gold.

B)

government’s holdings of gold at Fort Knox.

C)

fraction of deposits that banks hold in their vaults plus their deposits at the Federal

Reserve.

D)

ratio of gold to the paper money in the economy.

Use the following to answer questions 84-85:

84.

(Table: Balance Sheet) Refer to Table: Balance Sheet. If the reserve ratio is 25%,

deposits are:

A)

$5,000.

B)

$15,000.

C)

$60,000.

D)

$80,000.

Page 16

85.

(Table: Balance Sheet) Refer to Table: Balance Sheet. If the reserve ratio is 25%, loans

are:

A)

$5,000.

B)

$15,000.

C)

$60,000.

D)

$80,000.

86.

The reserve ratio is the fraction of its:

A)

deposits that a bank holds as reserves.

B)

loans that a bank is required to hold as reserves.

C)

loans that a bank holds as reserves.

D)

assets that a bank is required to hold as reserves.

87.

Among the assets of a bank are:

A)

customers’ deposits.

B)

loans.

C)

customers’ borrowings.

D)

deposits and loans.

88.

Among the liabilities of banks are:

A)

customers’ deposits.

B)

loans.

C)

reserves.

D)

loans and reserves.

89.

If a bank has deposits of $100,000, loans of $75,000, cash on hand of $10,000, and

$15,000 on deposit at the Federal Reserve, then its reserve ratio is:

A)

5%.

B)

10%.

C)

12.5%.

D)

25%.

90.

Bank reserves are:

A)

the money in bank vaults only.

B)

the amount of cash that a bank must hold to pay FDIC insurance premiums.

C)

the currency held at bank vaults plus bank deposits at the Federal Reserve.

D)

the entire amount of checkable bank deposits.

Page 17

91.

A reserve ratio is the:

A)

proportion of cash and security reserves the bank holds.

B)

fraction of deposits that the bank is required to hold as reserves.

C)

loan-to-deposit ratio in the bank’s balance sheet.

D)

money belonging to the bank’s largest depositors.

92.

Reserve requirements:

A)

set the maximum amount of reserves a bank must hold.

B)

set the minimum amount of reserves a bank must hold.

C)

are established by Congress.

D)

are set by the American Bankers Association.

93.

The reserve ratio is defined as the ratio of:

A)

bank assets to bank liabilities.

B)

bank assets to bank reserves.

C)

customers’ bank deposits to bank assets.

D)

bank reserves to customers’ checkable bank deposits.

94.

Banks are illiquid because:

A)

their deposits are less liquid than their loans.

B)

their loans are less liquid than their deposits.

C)

their assets are greater than their liabilities.

D)

their liabilities are greater than their assets.

95.

Which of the following about bank runs is false?

A)

They may start as a result of a rumor that a bank is in financial trouble.

B)

Many banks’ depositors try to withdraw their funds because they fear a bank

failure.

C)

Bank runs typically happen only to small banks with few financial assets.

D)

Bank runs often lead to a loss of faith in other banks, causing additional bank runs.

96.

A bank run can break a bank because:

A)

borrowers default on their loans, and the bank’s assets become worthless.

B)

banks cannot quickly convert illiquid loans to liquid assets without facing a large

financial loss.

C)

depositors’ panic spreads to borrowers, who want to take additional loans from the

bank.

D)

the bank’s reserves kept with the Federal Reserve are in the form of illiquid U.S.

Treasury bonds.

Page 18

97.

Bank runs in the United States during the 1930s damaged the economy because:

A)

capital requirements prevented bank managers from taking additional lending risks.

B)

the reserve ratio was set too high.

C)

the Federal Reserve system did not exist at the time.

D)

the loss of confidence at one bank quickly extended to other banks.

98.

A bank run occurs when:

A)

too many people are trying to borrow more at one time.

B)

many bank depositors are trying to withdraw their funds from the bank.

C)

interest rates start to increase.

D)

interest rates are higher than inflation rates.

99.

A major problem with bank runs is that they:

A)

spread to other banks.

B)

cause inflation because the money moves so fast.

C)

drive down interest rates.

D)

drive down both inflation and interest rates.

100.

The government has almost eliminated the possibility of bank runs by instituting

protective measures. Which example is NOT such a measure?

A)

capital requirements

B)

reserve requirements

C)

loan guarantees

D)

deposit insurance

101.

The guarantee by the FDIC to reimburse bank customers up to $250,000 per deposit in

the event of bank problems is called:

A)

fractional reserve banking.

B)

reserve requirements.

C)

discount rate.

D)

deposit insurance.

102.

Probably the most important feature of deposit insurance is that it:

A)

is paid for by the federal government.

B)

costs so little to buy the policies to keep your money safe.

C)

protects the economy against bank runs.

D)

ensures that banks will always make a profit.

Page 19

103.

Which factor is NOT one of the main features designed to protect depositors and the

economy against bank runs?

A)

deposit insurance

B)

capital requirements

C)

reserve requirements

D)

interest rate ceilings on checkable deposits

104.

Which example of bank regulations is NOT designed to prevent bank runs?

A)

reserve requirements

B)

deposit insurance

C)

the federal funds rate

D)

capital requirements

105.

Capital requirements for banks do NOT serve the purpose of:

A)

reducing a bank owner’s incentive for excessive risk taking.

B)

offsetting the change in incentives caused by deposit insurance.

C)

putting to use the excess of a bank’s assets over its deposits and other liabilities.

D)

reducing deposits.

106.

If a bank has assets of $100 million, according to practice, its liabilities should NOT

exceed:

A)

$7 million.

B)

$70 million.

C)

$93 million.

D)

$107 million.

107.

Which entity acts to protect depositors from a bank run by insuring all deposits up to

$250,000?

A)

the FDIC

B)

the Department of Justice

C)

the Federal Reserve

D)

the Office of Management and Budget

108.

The existence of banks:

A)

results in the money supply being larger than the amount of currency in circulation.

B)

inhibits the creation of money.

C)

makes the money supply equal to the amount of currency in circulation.

D)

results in the money supply being less than the amount of currency in circulation.

Page 20

109.

Banks create money when they:

A)

make loans.

B)

take deposits.

C)

hold excess reserves.

D)

pay withdrawals to depositors.

110.

What would be the immediate effect if an individual made a $9,000 cash deposit in a

bank?

A)

The money supply would rise by $9,000.

B)

The money supply would fall by $9,000.

C)

The money supply would not be affected.

D)

The money supply would fall but by less than the $9,000 deposit.

111.

Suppose that the reserve ratio is 20%. If Sam deposits $500 in his checking account, his

bank can increase loans by:

A)

$500.

B)

$2,500.

C)

$100.

D)

$400.

112.

Suppose that the reserve ratio is 20%. If Holly deposits $1,000 of cash in her checking

account and her bank lends $600 to Freda, the money supply:

A)

remains the same.

B)

decreases by $1,000.

C)

decreases by $600.

D)

increases by $600.

113.

Suppose that a bank does NOT hold excess reserves and the reserve ratio is 20%. If

Molly deposits $1,000 of cash in her checking account and the bank lends $600 to

Freda, the bank can lend an additional:

A)

$400.

B)

$200.

C)

$1,000.

D)

$5,000.