Page 21

Use the following to answer questions 102-108:

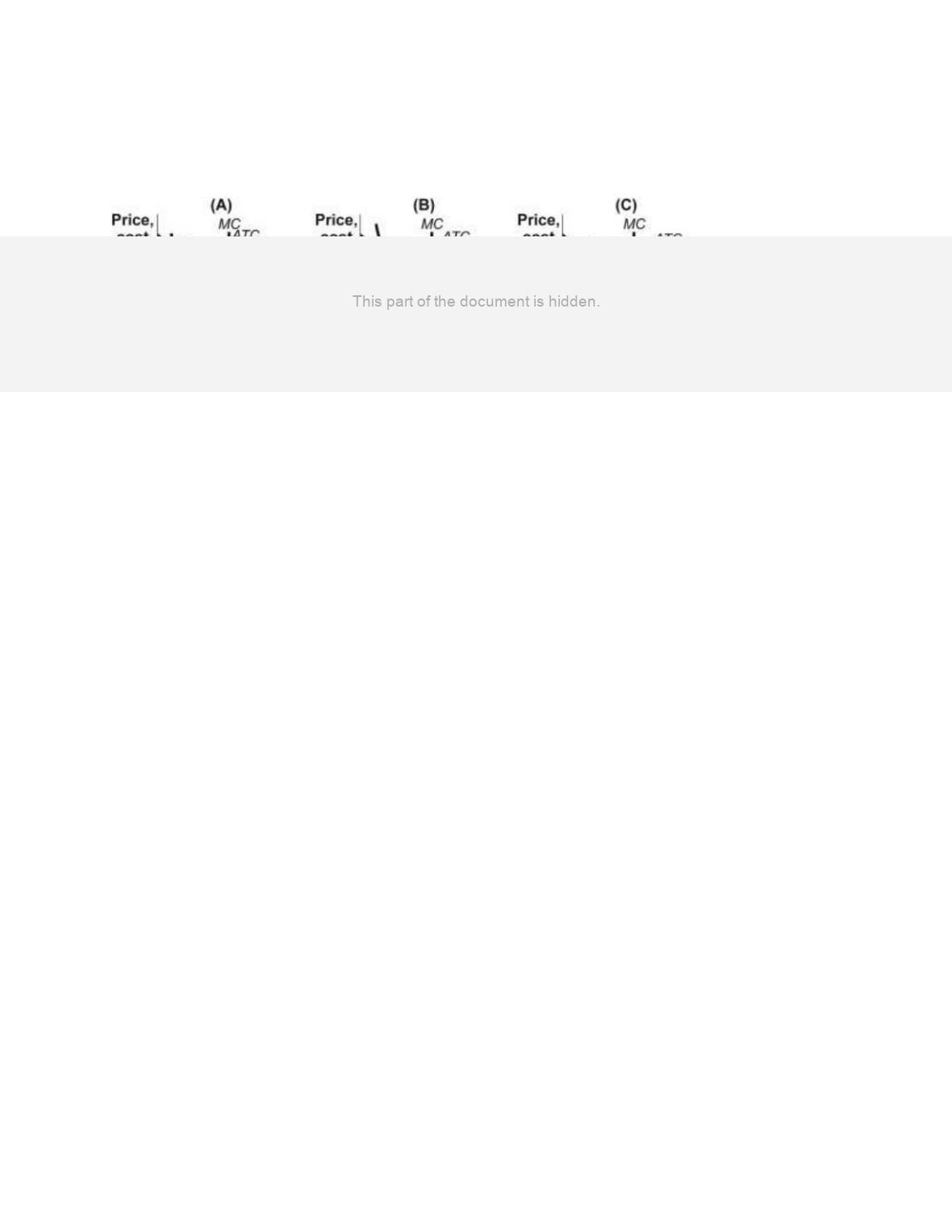

Figure: Profits in Monopolistic Competition

102.

(Figure: Profits in Monopolistic Competition) Use Figure: Profits in Monopolistic

Competition. In panel (A) of the figure, the profit-maximizing quantity of output is

determined by the intersection at point:

A)

G.

B)

F.

C)

H.

D)

C.

103.

(Figure: Profits in Monopolistic Competition) Use Figure: Profits in Monopolistic

Competition. In panel (B) of the figure, the profit-maximizing quantity of output is

determined by the intersection at point:

A)

J.

B)

K.

C)

L.

D)

M.

104.

(Figure: Profits in Monopolistic Competition) Use Figure: Profits in Monopolistic

Competition. In panel (C) of the figure, the profit-maximizing quantity of output is

determined by the intersection at point:

A)

P.

B)

S.

C)

R.

D)

Q.

Page 22

105.

(Figure: Profits in Monopolistic Competition) Use Figure: Profits in Monopolistic

Competition. A positive economic profit is earned if the profit-maximizing price is

_____ in panel _____.

A)

E; (B)

B)

B; (A)

C)

A; (A)

D)

N; (C)

106.

(Figure: Profits in Monopolistic Competition) Use Figure: Profits in Monopolistic

Competition. A zero economic profit is earned if the profit-maximizing price is _____ in

panel _____.

A)

A; (A)

B)

B; (A)

C)

N; (C)

D)

E; (B)

107.

(Figure: Profits in Monopolistic Competition) Use Figure: Profits in Monopolistic

Competition. A negative economic profit (or economic loss) is earned if the

profit-maximizing price is _____ in panel _____.

A)

E; (B)

B)

B; (A)

C)

N; (C)

D)

O; (C)

108.

(Figure: Profits in Monopolistic Competition) Use Figure: Profits in Monopolistic

Competition. A long-run equilibrium is illustrated at the profit-maximizing price _____

in panel _____.

A)

A; (A)

B)

E; (B)

C)

B; (A)

D)

N; (C)

Page 23

Use the following to answer questions 109-114:

Figure: The Restaurant Market

109.

(Figure: The Restaurant Market) Use Figure: The Restaurant Market. The figure shows

curves facing a typical restaurant. Assume that many firms, differentiated products, and

easy entry and exit characterize the restaurant industry. The restaurant shown here will

maximize profits at quantity:

A)

Q1.

B)

Q2.

C)

Q3.

D)

Not enough information is given to answer the question.

110.

(Figure: The Restaurant Market) Use Figure: The Restaurant Market. The figure shows

curves facing a typical restaurant. Assume that many firms, differentiated products, and

easy entry and exit characterize the restaurant market. For the restaurant shown here, the

profit-maximizing price is:

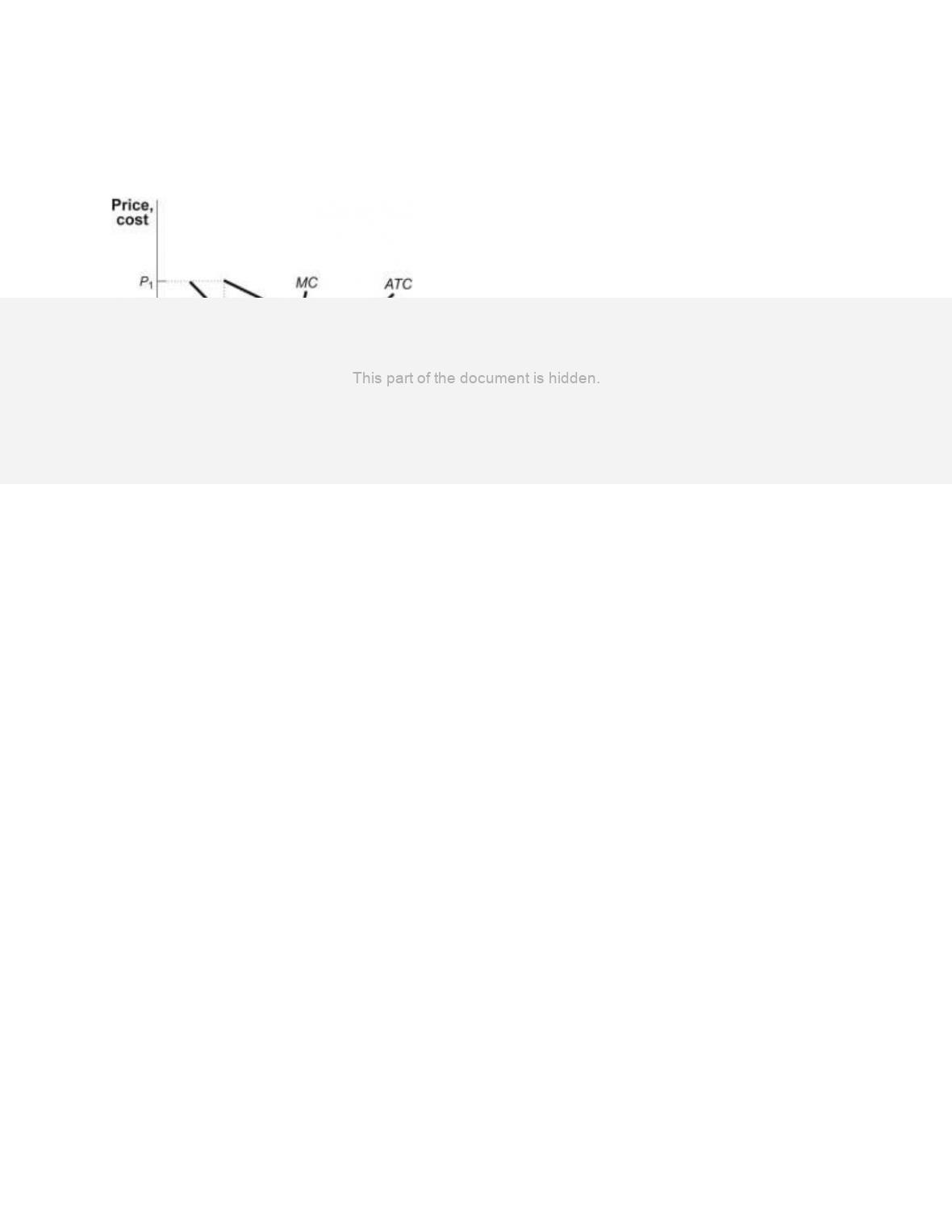

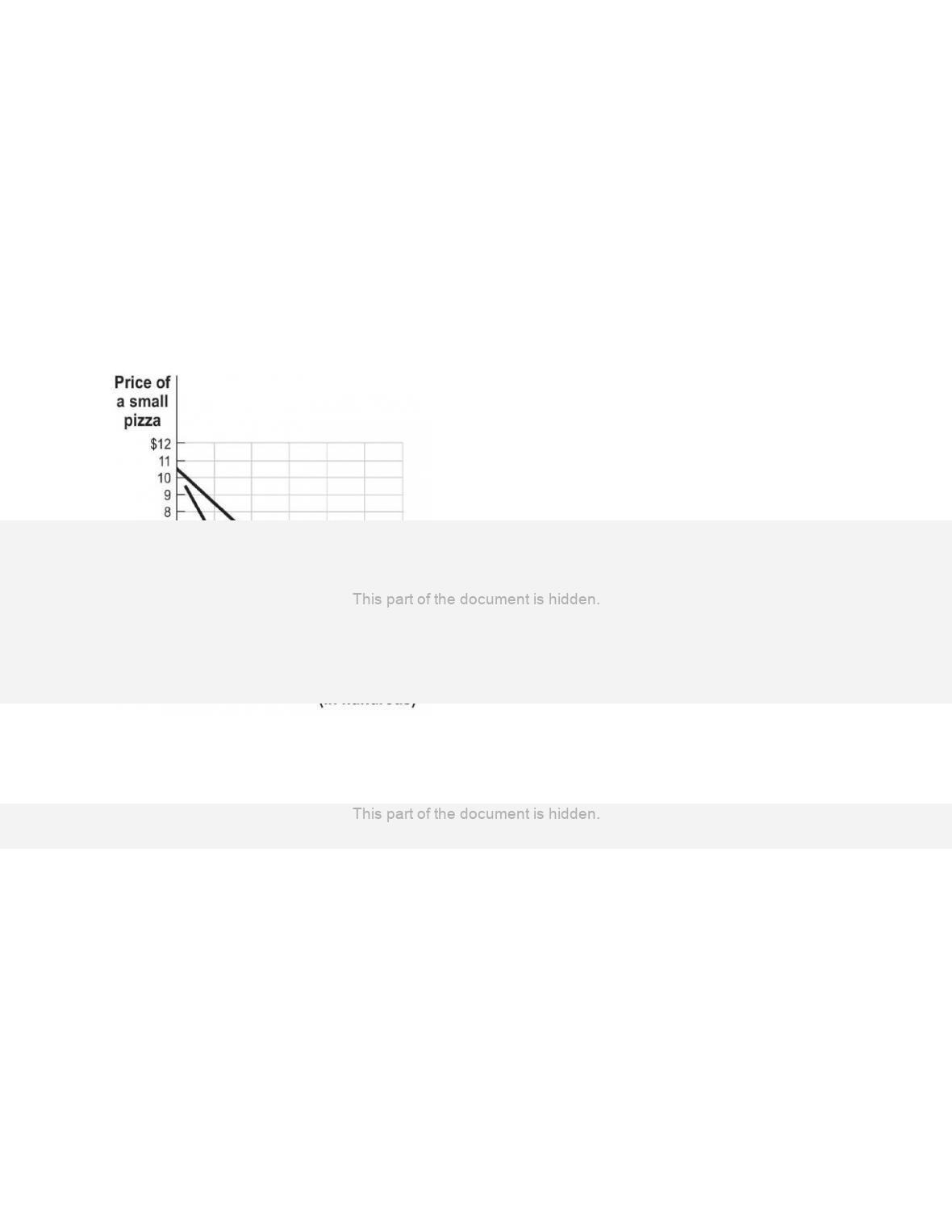

A)

P1.

B)

P2.

C)

P3.

D)

Not enough information is given to answer the question.

Page 24

111.

(Figure: The Restaurant Market) Use Figure: The Restaurant Market. The figure shows

curves facing a typical restaurant. Assume that many firms, differentiated products, and

easy entry and exit characterize the restaurant market. For the restaurant shown here, the

profit per unit is represented by the vertical distance between the points:

A)

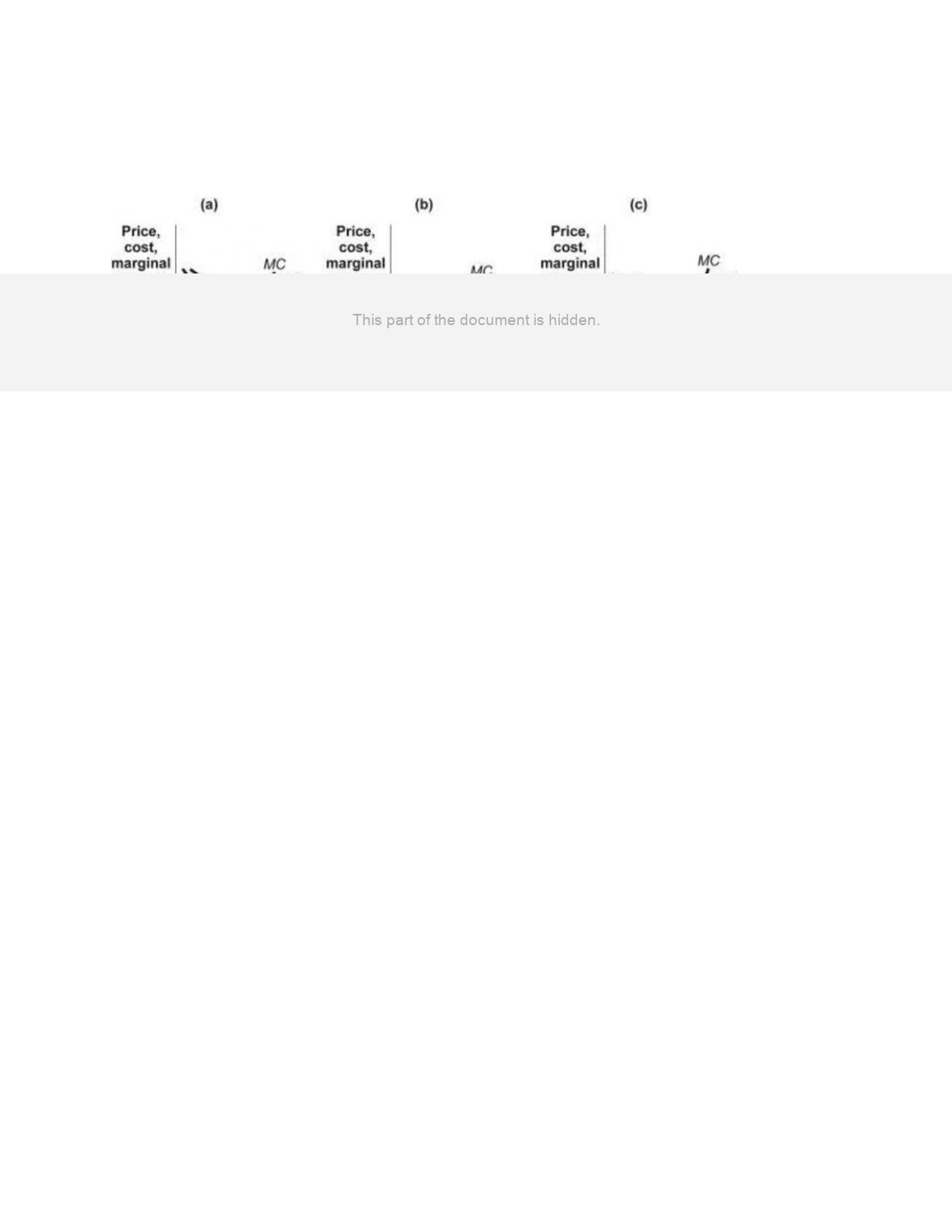

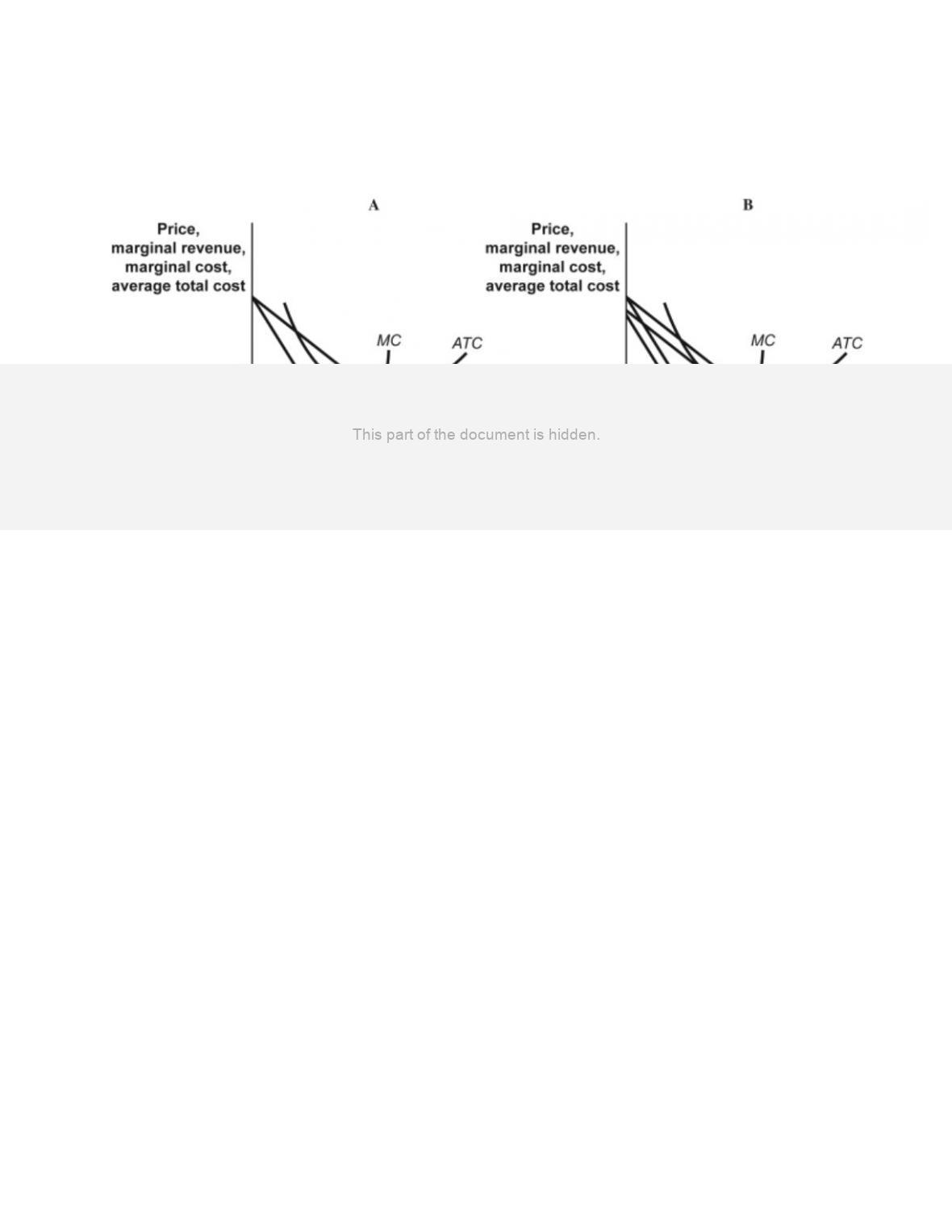

a and e.

B)

f and d.

C)

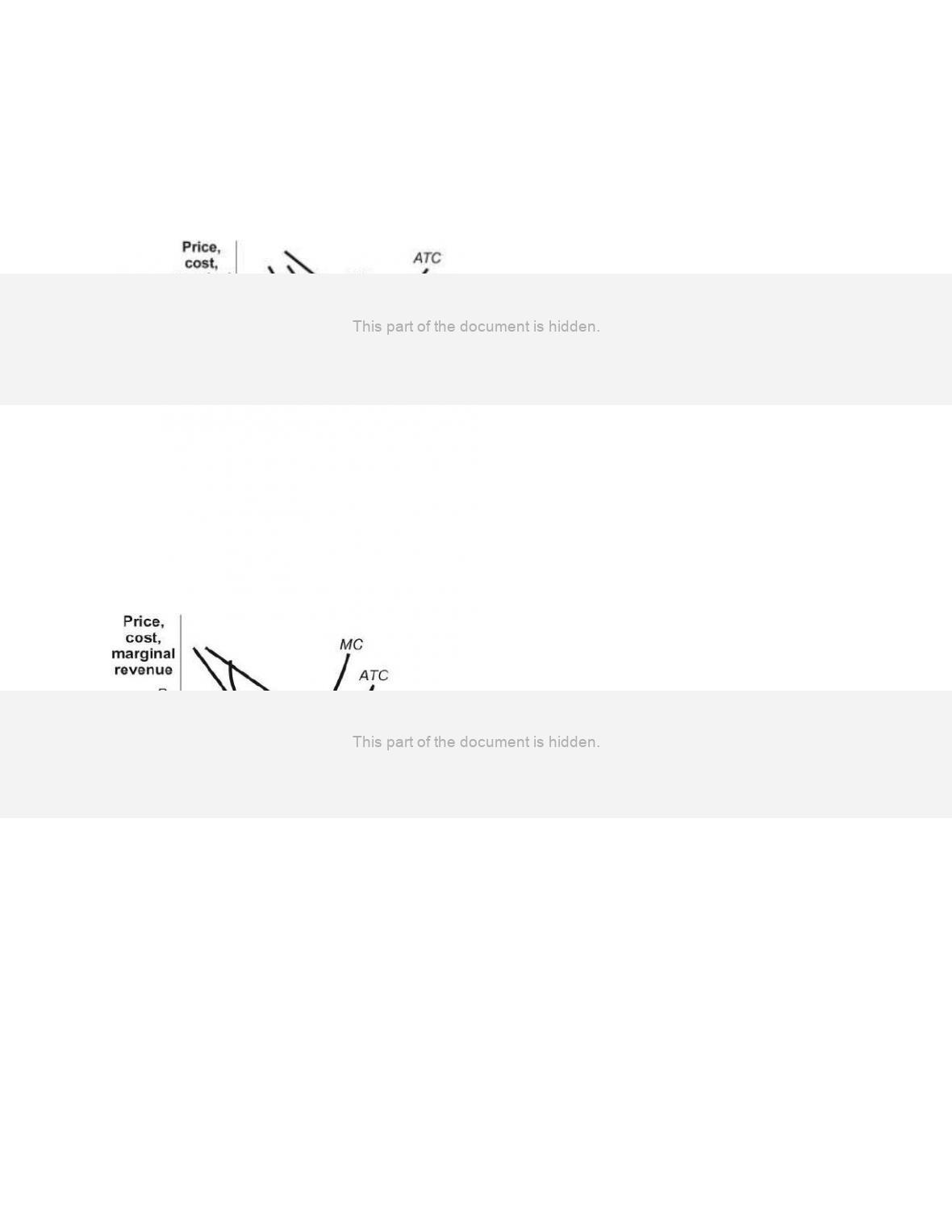

b and f.

D)

b and d.

112.

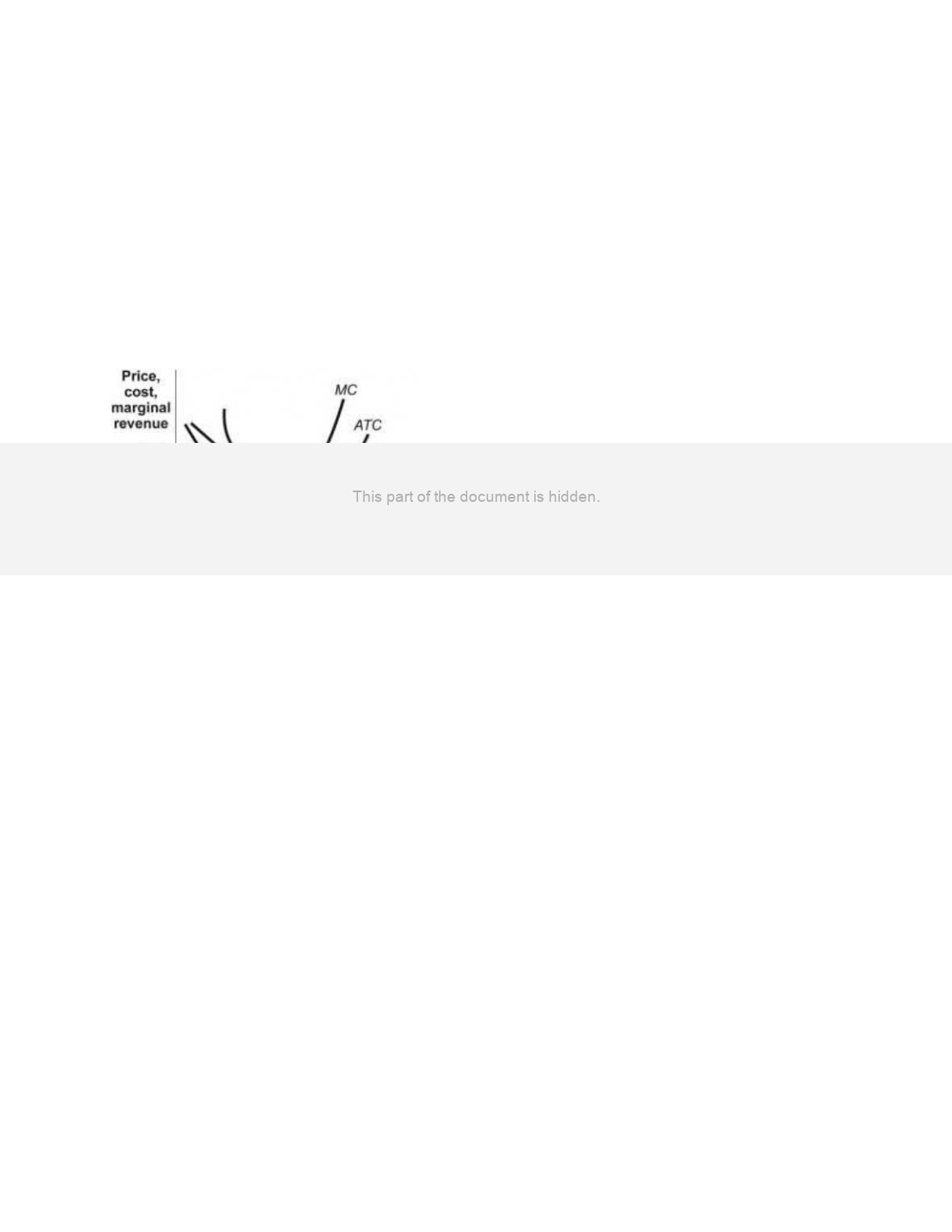

(Figure: The Restaurant Market) Use Figure: The Restaurant Market. The figure shows

curves facing a typical restaurant. Assume that many firms, differentiated products, and

easy entry and exit characterize the restaurant market. If the restaurant shown here were

to raise its price above the profit-maximizing price, its total revenue would:

A)

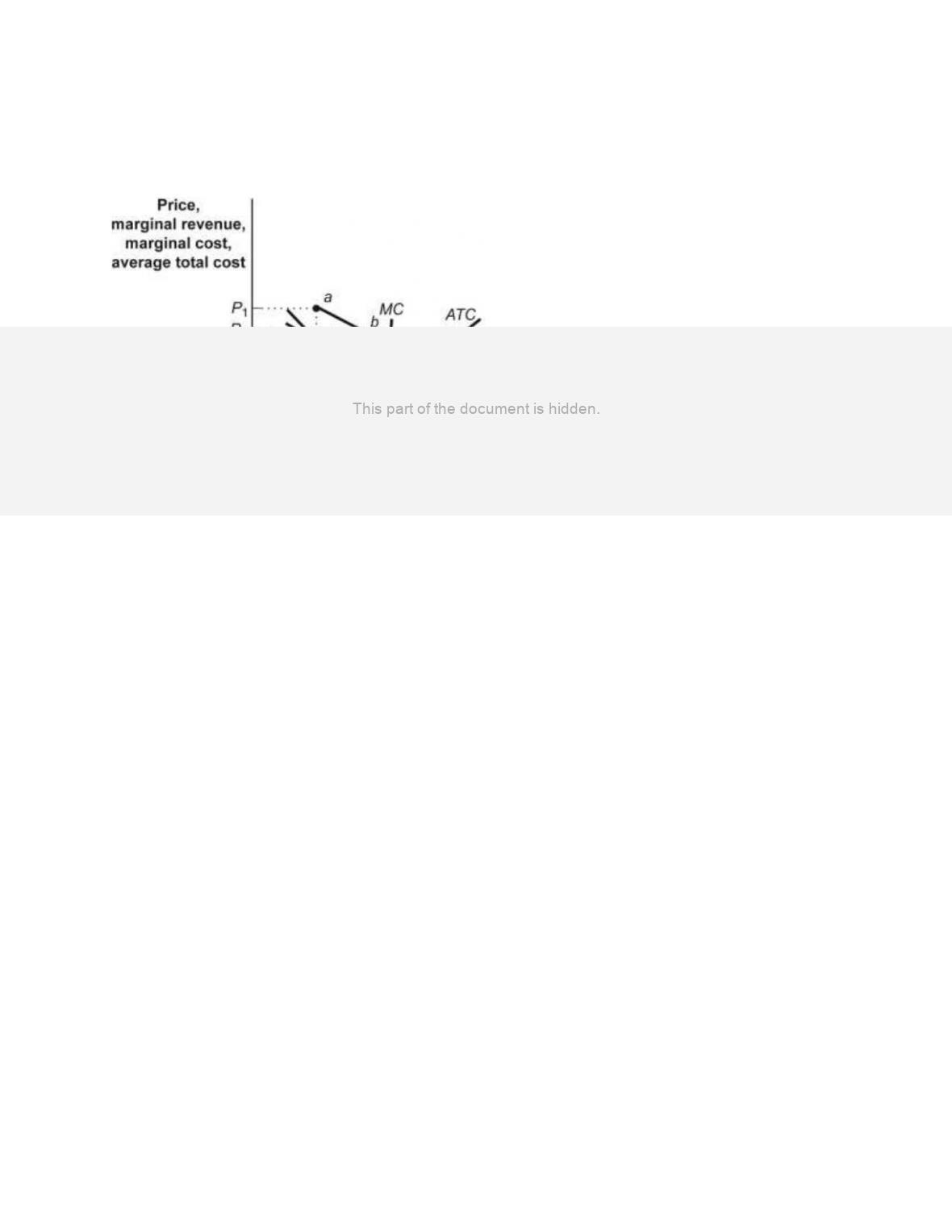

decrease.

B)

increase.

C)

not change.

D)

Not enough information is given to answer the question.

113.

(Figure: The Restaurant Market) Use Figure: The Restaurant Market. The figure shows

curves facing a typical restaurant. Assume that many firms, differentiated products, and

easy entry and exit characterize the market. In the long run:

A)

restaurants will leave the market.

B)

restaurants will enter the market.

C)

restaurants will neither enter nor exit the market.

D)

Not enough information is given to answer the question.

114.

(Figure: The Restaurant Market) Use Figure: The Restaurant Market. The figure shows

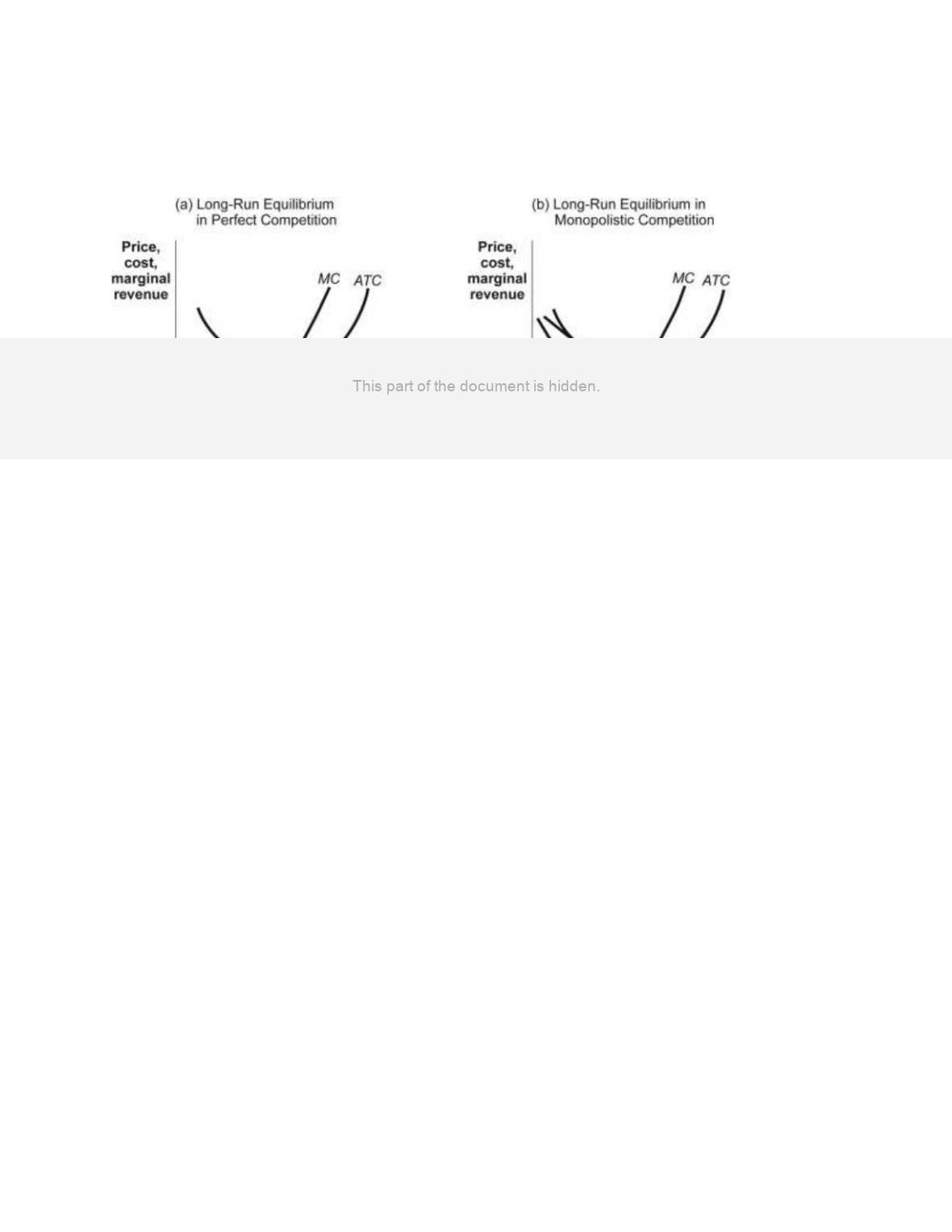

curves facing a typical restaurant. Assume that many firms, differentiated products, and

easy entry and exit characterize the restaurant market. In long-run equilibrium, the

economic profit earned by the typical restaurant in the community will be:

A)

negative.

B)

zero.

C)

equal to the level shown in the figure.

D)

Not enough information is given to answer the question.

Page 25

115.

The model of monopolistic competition characterizes a city’s market for plumbing

services. Suppose that the market is initially in long-run equilibrium, and then overall

demand for plumbing services increases. In the short run, the price for plumbing

services will _____ and total output in the market will _____.

A)

fall; fall

B)

not change; not change

C)

rise; rise

D)

rise; fall

Page 26

Use the following to answer questions 116-120:

Figure: The Market for Gas Stations

116. (Figure: The Market for Gas Stations) Use Figure: The Market for Gas Stations.

Assume that the market for gas stations is characterized by many firms, differentiated

products, easy entry, and easy exit. The typical gas station will maximize profits at a

quantity of:

A) Q1.

B) Q2.

C) Q3.

D) Not enough information is given to answer the question.

Ans: B

Refer To: Ref 15-5 Figure: The Market for Gas Stations

bloomslevel: Applying

chaptername: Chapter 15

levelofdifficulty: Moderate

questiontype: Multiple Choice

sequence: 15116

topic: Comprehensive: Understanding Monopolistic Competition

Page 27

116.

(Figure: The Market for Gas Stations) Use Figure: The Market for Gas Stations. Assume

that the market for gas stations is characterized by many firms, differentiated products,

easy entry, and easy exit. For the typical gas station, the profit-maximizing price would

be:

A)

P1.

B)

P2.

C)

P3.

D)

Not enough information is given to answer the question.

117.

(Figure: The Market for Gas Stations) Use Figure: The Market for Gas Stations. The

figure shows curves facing a typical gas station in a large town. The market is

characterized by many firms, differentiated products, easy entry, and easy exit. If the

gas station shown here were to raise its price above the profit-maximizing price, the

outcome would be _____ in total revenue.

A)

a reduction

B)

an increase

C)

no change

D)

Not enough information is given to answer the question.

118.

(Figure: The Market for Gas Stations) Use Figure: The Market for Gas Stations. The

figure shows curves facing a typical gas station in a large town. The market is

characterized by many firms, differentiated products, easy entry, and easy exit. If the

gas station here is typical, then in the long run, we would expect to observe:

A)

a few gas stations leaving the market.

B)

new gas stations entering the market.

C)

neither entry nor exit.

D)

many gas stations leaving the market.

119.

(Figure: The Market for Gas Stations) Use Figure: The Market for Gas Stations. The

figure shows curves facing a typical gas station in a large town. The market is

characterized by many firms, differentiated products, easy entry, and easy exit. If the

gas station here is typical, prices charged by firms in the market are likely to:

A)

fall in the long run.

B)

rise in the long run.

C)

remain unchanged.

D)

rise dramatically in the long run.

Page 28

120.

(Figure: The Market for Gas Stations) Use Figure: The Market for Gas Stations. This

market is characterized by many firms, differentiated products, easy entry, and easy exit.

In long-run equilibrium, the economic profit earned by the typical gas station will be:

A)

equal to the level shown in the figure.

B)

negative.

C)

zero.

D)

Not enough information is given to answer the question.

121.

The model of monopolistic competition characterizes the market for plumbing services.

This market is initially in long-run equilibrium, but then there is an increase in the

market demand for plumbing services. We expect that in the long run, the economic

profits of typical firms will be:

A)

typical of those earned by monopoly firms.

B)

negative.

C)

zero.

D)

positive but less than the level typically earned by monopoly firms.

122.

General Snacks is a typical firm in a market characterized by monopolistic competition.

Initially, the market is in long-run equilibrium, and then there is an increase in the

market demand for snacks. In the short run the price of snacks will _____ and the

market output of snacks will _____.

A)

fall; fall

B)

remain unchanged; remain unchanged

C)

rise; fall.

D)

rise; rise

123.

General Snacks is a typical firm in a market characterized by the model of monopolistic

competition. Initially, the market is initially in long-run equilibrium, and then there is an

increase in the market demand for snacks. We expect that:

A)

in the long run, new firms will enter the market.

B)

there will be a short-run increase in the number of firms, but in the long run, the

number of firms will return to the original level.

C)

firms will leave the market in the long run.

D)

firms will shut down, but they will not leave the industry in the long run.

Page 29

Use the following to answer questions 124-127:

Figure: Monopolistic Competition II

124.

(Figure: Monopolistic Competition II) Use Figure: Monopolistic Competition II.

Panel(s) _____ in the figure show(s) a monopolistic competitor earning a loss in the

short run.

A)

(a)

B)

(b)

C)

(c)

D)

(b) and (c)

125.

(Figure: Monopolistic Competition II) Use Figure: Monopolistic Competition II. Which

panel(s) in the figure show(s) a monopolistic competitor earning a profit in the short

run?

A)

panel (a) only

B)

panel (b) only

C)

panel (c) only

D)

panels (a) and (c)

126.

(Figure: Monopolistic Competition II) Use Figure: Monopolistic Competition II. Which

panel(s) in the figure show(s) a monopolistic competitor producing where price is

greater than marginal revenue?

A)

panel (a) only

B)

panel (b) only

C)

panel (c) only

D)

panels (a), (b), and (c)

Page 30

127.

(Figure: Monopolistic Competition II) Use Figure: Monopolistic Competition II. Which

panel(s) in the figure show(s) a monopolistic competitor in long-run equilibrium?

A)

panel (a) only

B)

panel (b) only

C)

panel (c) only

D)

panels (a), (b), and (c)

Use the following to answer questions 128-129:

Figure: Monopolistic Competition III

128.

(Figure: Monopolistic Competition III) Use Figure: Monopolistic Competition III. The

figure shows the demand, marginal revenue, marginal cost, and average total cost curves

for Pat’s Pizza Parlor, a monopolistic competitor in the food-to-go industry. Pat’s Pizza

Parlor’s profit at the profit-maximizing quantity will be:

A)

$0.

B)

$350.

C)

$700.

D)

$900.

129.

(Figure: Monopolistic Competition III) Use Figure: Monopolistic Competition III. The

figure shows the demand, marginal revenue, marginal cost, and average total cost curves

for Pat’s Pizza Parlor, a monopolistic competitor in the food-to-go industry. In the long

run, the demand curve for Pat’s Pizza Parlor will shift to the _____ as competitors _____

the market.

A)

right; enter

B)

right; leave

C)

left; enter

D)

left; leave

130.

Toby operates a small deli downtown. The deli industry is monopolistically competitive.

Toby is producing the quantity that minimizes his average total cost. Assuming that

Toby is maximizing profits, his:

A)

marginal cost is less than his average total cost.

B)

marginal cost is less than his marginal revenue.

C)

price equals his average total cost.

D)

price is more than his average total cost.

131.

Toby operates a small deli downtown. The deli industry is monopolistically competitive.

Toby, along with every other deli in town, is producing the quantity that minimizes

average total cost. Assuming the delis are maximizing profits, the:

A)

number of delis will eventually decrease.

B)

number of delis will eventually increase.

C)

delis’ prices equal their average total costs.

D)

delis have excess capacity.

Page 32

132.

(Figure: Monopolistic Competition IV) Use Figure: Monopolistic Competition IV. The

firm in the figure is producing at the output level that maximizes profits (minimizes

losses). The shaded rectangle represents the firm’s:

Figure: Monopolistic Competition IV

A)

profit.

B)

loss.

C)

fixed cost.

D)

variable cost.

Use the following to answer questions 133-134:

Figure: Monopolistic Competition V

133.

(Figure: Monopolistic Competition V) Use Figure: Monopolistic Competition V. The

figure illustrates a firm in the _____; in the _____, the demand and marginal revenue

curves will shift to the _____.

A)

short run; long run; right

B)

long run; short run; left

C)

short run; long run; left

D)

long run; short run; right

Page 33

134.

(Figure: Monopolistic Competition V) Use Figure: Monopolistic Competition V. In the

figure, in the long run firms will:

A)

enter this market until all firms earn zero economic profit.

B)

exit this market until all remaining firms earn zero profit.

C)

enter this market, leading to excess profit for all the firms.

D)

exit this market, leading to excess profit for all the remaining firms.

Use the following to answer questions 135-136:

Figure: Monopolistic Competition VI

135.

(Figure: Monopolistic Competition VI) Use Figure: Monopolistic Competition VI. The

figure illustrates a firm in the _____; in the _____, the demand and marginal revenue

curves will shift to the _____.

A)

short run; long run; right

B)

long run; short run; left

C)

short run; long run; left

D)

long run; short run; right

136.

(Figure: Monopolistic Competition VI) Use Figure: Monopolistic Competition VI. In

the figure, in the long run firms will:

A)

enter this market until all firms earn a zero economic profit.

B)

exit this market until all remaining firms earn a zero economic profit.

C)

enter this market, leading to excess profit for all of the firms.

D)

exit this market, leading to excess profit for all of the remaining firms.

Page 34

Use the following to answer questions 137-145:

Figure: Profit Maximization in Monopolistic Competition

137.

(Figure: Profit Maximization in Monopolistic Competition) Use Figure: Profit

Maximization in Monopolistic Competition. In panel (A) of the figure, the

profit-maximizing price and quantity are _____ and _____.

A)

S; M

B)

P; M

C)

P; Q

D)

T; Q

138.

(Figure: Profit Maximization in Monopolistic Competition) Use Figure: Profit

Maximization in Monopolistic Competition. A firm in monopolistic competition will

maximize profits by producing so that:

A)

P = MC.

B)

MR = MC.

C)

P = MR.

D)

P – ATC (i.e., economic profit per unit) is maximized.

139.

(Figure: Profit Maximization in Monopolistic Competition) Use Figure: Profit

Maximization in Monopolistic Competition. In the short run, a firm in monopolistic

competition may earn economic profits. The profits in panel (A) of the figure are:

A)

P – S.

B)

(P – S) × M.

C)

(P – S) × Q.

D)

(P – T) × Q.

Page 35

140.

(Figure: Profit Maximization in Monopolistic Competition) Use Figure: Profit

Maximization in Monopolistic Competition. If other firms see economic profits in the

industry, they will enter it, and the demand curve for firms already in the industry will

shift to the _____; in the long run, this will result in an economic profit _____ zero and

a price _____ ATC.

A)

right; equal to; equal to

B)

right; greater than; greater than

C)

left; less than; less than

D)

left; equal to; equal to

141.

(Figure: Profit Maximization in Monopolistic Competition) Use Figure: Profit

Maximization in Monopolistic Competition. In monopolistic competition, long-run

equilibrium is characterized by:

A)

P > MR.

B)

P < MR.

C)

P = MR.

D)

profit maximization, which occurs where P = MR = MC.

142.

(Figure: Profit Maximization in Monopolistic Competition) Use Figure: Profit

Maximization in Monopolistic Competition. In panel (A) of the figure, if the firm raises

its price above P, it will _____ customers.

A)

lose all of its

B)

still have some

C)

not lose any

D)

gain many new

143.

(Figure: Profit Maximization in Monopolistic Competition) Use Figure: Profit

Maximization in Monopolistic Competition. When the demand curve for a firm in

monopolistic competition shifts, the marginal revenue curve:

A)

must also shift.

B)

shifts in the opposite direction.

C)

will stay the same.

D)

will shift, but the profit-maximizing quantity will not change.

Page 36

144.

(Figure: Profit Maximization in Monopolistic Competition) Use Figure: Profit

Maximization in Monopolistic Competition. In panel (B) of the figure, the long-run

equilibrium will result in:

A)

no economic profits.

B)

no accounting profits.

C)

a tangency of the ATC curve with the MR curve.

D)

no economic profits and a tangency of the ATC curve with the MR curve.

145.

(Figure: Profit Maximization in Monopolistic Competition) Use Figure: Profit

Maximization in Monopolistic Competition. In panel (B) of the figure, the

profit-maximizing price is P2 and the ATC curve is tangent to the new demand curve.

The portion of the ATC that lies to the right of the tangency and continues down to the

intersection of MC with ATC indicates:

A)

that the firm is incurring an economic loss.

B)

that the firm is earning an economic profit.

C)

overutilization.

D)

excess capacity.

146.

A monopolistically competitive industry has some of the characteristics of perfect

competition, including:

A)

many firms making economic profit in the long run.

B)

easy entry and exit.

C)

identical products.

D)

easy entry and exit and identical products.

147.

Which statement is TRUE?

A)

For choosing the profit-maximizing quantity, the short-run decision-making

process of a firm in perfect competition is the same as that of a firm in

monopolistic competition since they produce so that P > MC.

B)

In the long run in perfect competition, economic profits equal zero, and in

monopolistic competition in the long run, economic profits are very large.

C)

In perfect competition, P = MC, and in monopolistic competition, MR = MC, but P

> MC and there is excess capacity.

D)

In both perfect competition and monopolistic competition, P equals minimum

average total cost in the long run.

Page 37

148.

The price in long-run equilibrium for a monopolistically competitive firm is _____ and

output is _____, compared with that of a perfectly competitive firm with an identical

production function and cost curves.

A)

higher; higher

B)

higher; lower

C)

lower; higher

D)

lower; lower

149.

The profit-maximizing rule, expressed as _____, is adhered to by firms operating in

_____ markets.

A)

MC > MR; monopolistically competitive but not perfectly competitive

B)

MC = MR; both monopolistically competitive and perfectly competitive

C)

MC > MR; perfectly competitive but not monopolistically competitive

D)

MC = MR; perfectly competitive but not monopolistically competitive

150.

The failure to produce enough to minimize average total cost is termed:

A)

economic profits.

B)

excess capacity.

C)

advertising.

D)

excess production.

151.

The main characteristic that distinguishes monopolistic competition from perfect

competition is:

A)

easy entry and exit.

B)

many firms.

C)

differentiated products.

D)

that in perfect competition, to maximize profits, a firm will produce where MR =

MC.

152.

Monopolistic competition in an industry results in:

A)

overutilization of plants.

B)

chronic excess capacity.

C)

less advertising than in perfect competition.

D)

lower prices than in perfect competition.

Page 38

153.

Long-run equilibrium in perfect competition and in monopolistic competition are similar

because in both models, firms _____ in the long run.

A)

produce at the minimum point of the average total cost curve

B)

set price equal to marginal cost

C)

make zero economic profits

D)

have excess capacity

154.

The broccoli market is perfectly competitive. This means that the price of broccoli is

_____ than if the market were monopolistically competitive, and total broccoli output in

the market is _____ than if it were monopolistically competitive.

A)

lower; higher

B)

lower; lower

C)

higher; lower

D)

higher; higher

155.

A monopolistically competitive firm has excess capacity in the long run. This means

that it:

A)

produces less than the output at which average total costs are minimized.

B)

produces less than the output at which price and marginal cost are equal.

C)

could produce more by moving to a larger plant.

D)

doesn’t maximize profits.

156.

The restaurant industry is characterized by excess capacity. This means that:

A)

restaurants are producing more than their profit-maximizing level.

B)

the profit-maximizing level is less than the level that minimizes average total costs.

C)

restaurants are producing less than their profit-maximizing level.

D)

the quantity of restaurant meals supplied exceeds the quantity of restaurant meals

demanded.

157.

Firms in the monopolistically competitive movie industry face excess capacity, which

means that there are _____ movies than the output at which _____ cost is minimized.

A)

fewer; marginal

B)

more; average total

C)

fewer; average total

D)

more; marginal

Page 39

Use the following to answer questions 158-160:

Figure: Comparing Long-Run Equilibriums

158.

(Figure: Comparing Long-Run Equilibriums) Use Figure: Comparing Long-Run

Equilibriums. Which statement is FALSE?

A)

The firm in panel (a) produces where price equals marginal cost and average total

cost.

B)

The firm in panel (b) produces where price equals marginal cost.

C)

The firm in panel (b) produces where price equals average total cost.

D)

The firm in panel (a) produces where price equals average total cost.

159.

(Figure: Comparing Long-Run Equilibriums) Use Figure: Comparing Long-Run

Equilibriums. Which statement is TRUE?

A)

Firms in the market structure shown in panel (a) cannot have profits in the long

run, but those in panel (b) can.

B)

Both panels show markets that have few interdependent firms.

C)

Both panels show markets that produce identical products.

D)

Both panels show markets that have many firms.

160.

(Figure: Comparing Long-Run Equilibriums) Use Figure: Comparing Long-Run

Equilibriums. Which statement is FALSE?

A)

Firms in panel (a) cannot have profits in the long run, but those in panel (b) can.

B)

Both panels show markets in which firms are covering all of their implicit and

explicit costs.

C)

Firms in the market shown in panel (a) produce identical products, whereas those

in panel (b) produce similar but differentiated products.

D)

Both firms show markets that have many firms.

Page 40

161.

Monopolistic competition in an industry will result in _____ because firms produce

_____.

A)

overutilization of plants; the minimum-cost output

B)

less advertising than in perfect competition; the minimum-cost output

C)

lower prices than in perfect competition; more than the minimum-cost output

D)

chronic excess capacity; less than the minimum-cost output

162.

When the profit-maximizing level of output is less than the output associated with the

minimum possible average total cost of production, a firm is said to have:

A)

economic profits.

B)

excess capacity.

C)

advertising.

D)

excess production.

163.

Which statement is TRUE?

A)

All markets should be oligopolies because that is the most efficient market

structure.

B)

Monopolistic competition results in excess capacity since, in the long run, the point

where MR = MC is to the right of the minimum of the ATC curve.

C)

In monopolistic competition, firms earn large economic profits in the long run.

D)

In monopolistic competition, firms earn zero economic profits in the long run.

164.

In contrast with perfect competition, in monopolistic competition:

A)

entry and exit are easy.

B)

there are many firms.

C)

products are differentiated.

D)

a firm will produce where MR = MC in order to maximize profits.

165.

Firm A and firm B have identical cost curves and operate in markets with similar market

demand curves. Firm A operates in perfect competition, and firm B operates in

monopolistic competition. In the long run, firm A will charge _____ and produce _____

than will firm B.

A)

less; less

B)

more; more

C)

more; less

D)

less; more