Page 1

Name: __________________________ Date: _____________

1.

In an oligopoly:

A)

there are many sellers.

B)

there are no barriers to entry.

C)

firms recognize their interdependence.

D)

total surplus is maximized.

2.

The MOST important source of oligopoly in an industry is:

A)

economies of scale.

B)

government regulation.

C)

technological inferiority.

D)

ownership of plentiful resources.

3.

An industry that is dominated by a few firms, each of which recognizes that its own

choices can affect the choices of its rivals and vice versa, is:

A)

a monopoly.

B)

an oligopoly.

C)

characterized by monopolistic competition.

D)

characterized by perfect competition.

4.

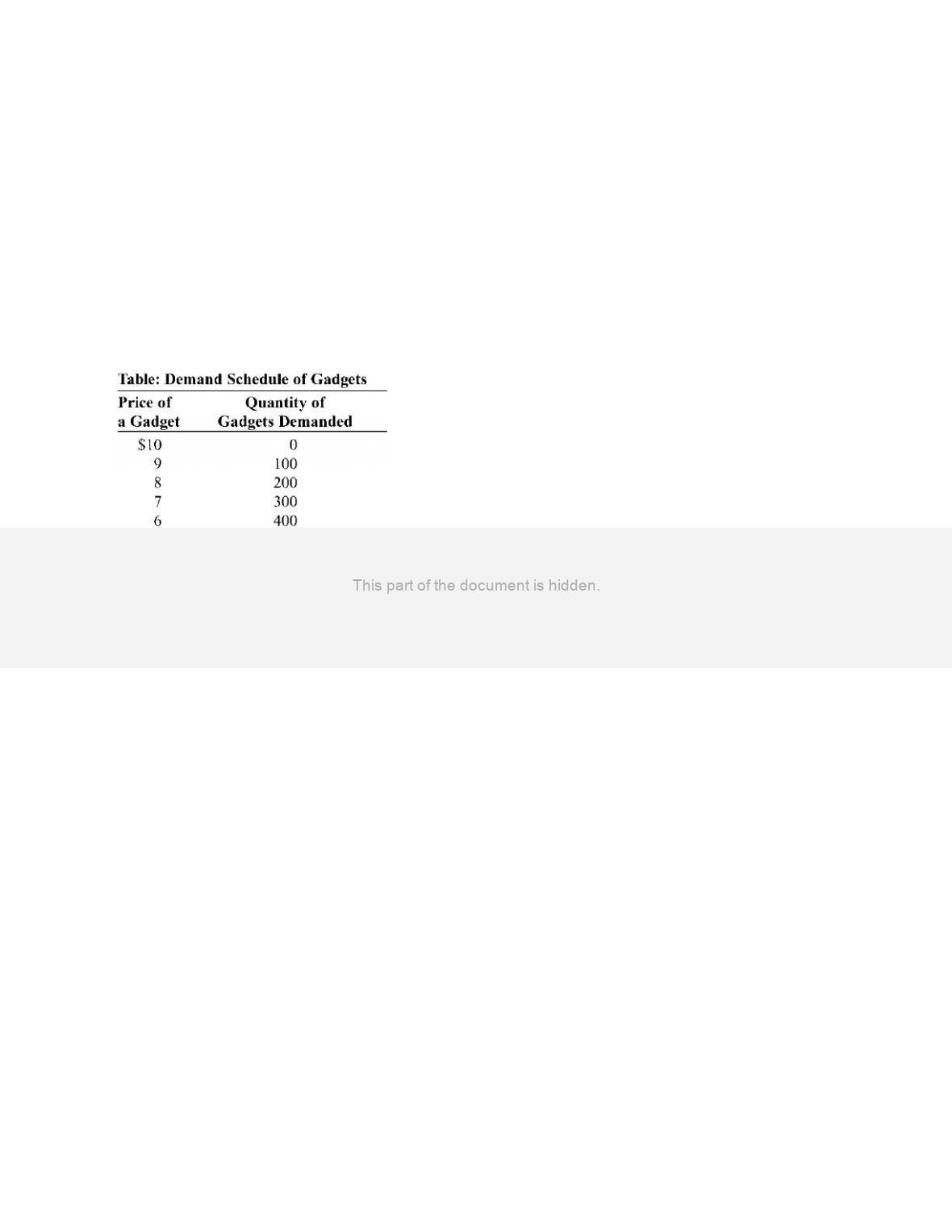

Oligopoly is a market structure that is characterized by a _____ number of _____ firms

producing _____ products.

A)

small; interdependent; identical or differentiated

B)

small; independent; identical or differentiated

C)

large; relatively small independent; differentiated

D)

large; relatively small independent; identical

5.

To be called an oligopoly, an industry must have:

A)

independence in decision making.

B)

a horizontal demand curve.

C)

a small number of interdependent firms.

D)

relatively easy entry and exit.

6.

Oligopoly is a market structure characterized by:

A)

independence in decision making.

B)

interdependence: each firm’s decision affects the profit of the other firms.

C)

substantial diseconomies of scale.

D)

a large number of small firms.

Page 2

7.

The market structure characterized by a few interdependent firms and barriers to entry is

called:

A)

monopolistic competition.

B)

perfect competition.

C)

oligopoly.

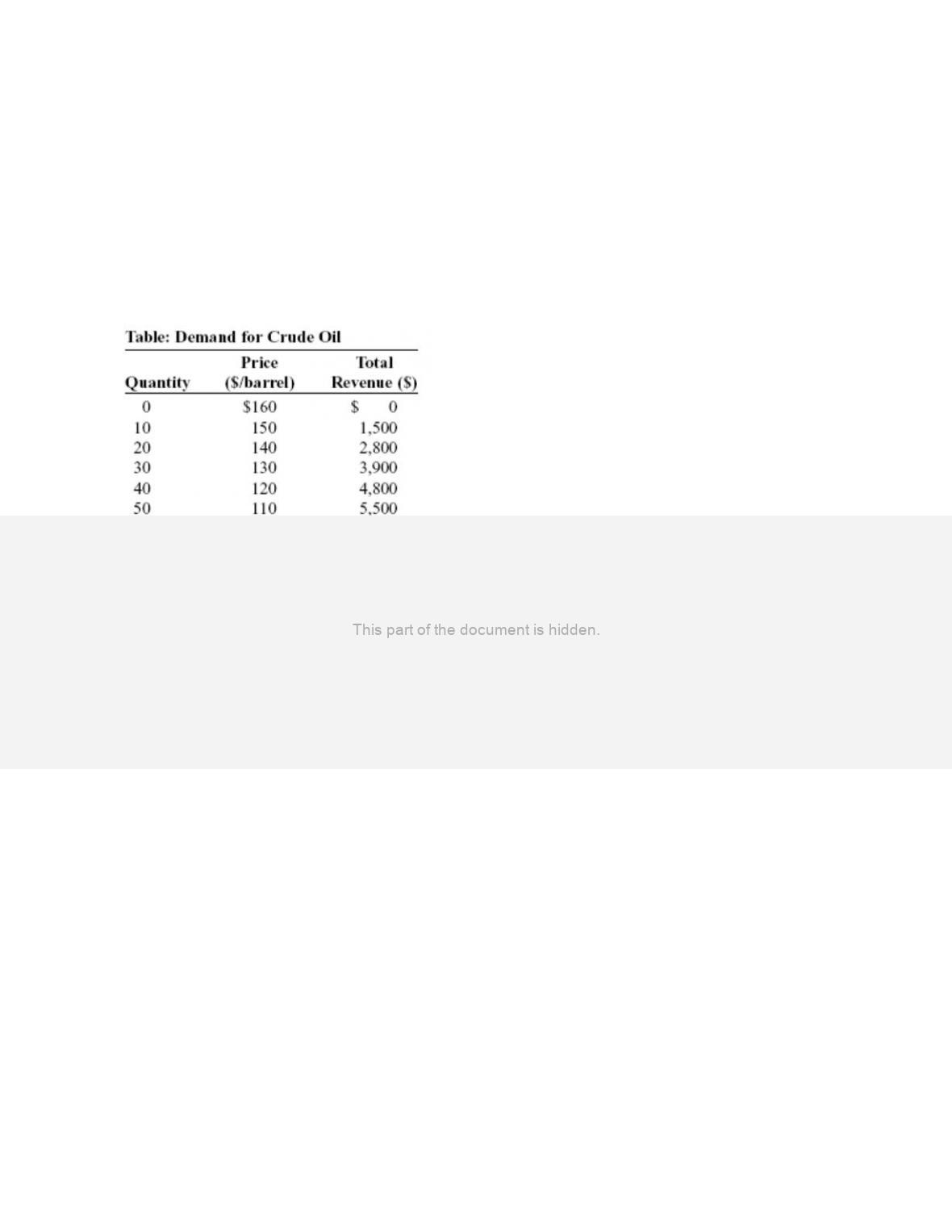

D)

monopoly.

8.

In oligopoly, a firm must realize that:

A)

what it does has no effect on the other firms in the industry.

B)

its behavior will be ignored by other firms in the industry.

C)

another major firm may dominate choices in the industry, and it will have to

behave accordingly.

D)

collusion was made legal in 2004.

9.

A firm that is in an oligopoly knows that its _____ affect its _____ and that the _____ of

its rivals will affect it.

A)

actions; rivals; reactions

B)

price changes; total revenue in a positive way; reactions

C)

actions rarely; rivals; actions

D)

price increases; total revenue in the long run only; large but not small price changes

10.

The market structure that is characterized by only a small number of producers is:

A)

oligopoly.

B)

perfect competition.

C)

monopoly.

D)

monopolistic competition.

11.

Which scenarios BEST describes an oligopolistic industry?

A)

A single cable company serves customers in a small town.

B)

Thousands of soybean farmers sell their output in a global commodities market.

C)

Coca-Cola and Pepsi sell most of the soft drinks consumed around the world.

D)

A college has one bookstore selling textbooks to students.

12.

To calculate the Herfindahl–Hirschman index (HHI), one must _____ market share(s) of

_____ in the industry.

A)

sum the; the four largest firms

B)

sum the; all of the firms

C)

divide the; the largest firm by the sum of the four largest firms

D)

sum the squared; all of the firms

Page 3

13.

An industry is dominated by a few firms. Each of these firms acknowledges that its own

choices affect the choices of its rivals. Each firm also recognizes that its rivals’ choices

affect the decisions it makes. This industry is an example of:

A)

a monopoly.

B)

an oligopoly.

C)

monopolistic competition.

D)

perfect competition.

14.

Oligopoly is a market structure that is characterized by a _____ number of _____ firms

that produce _____ products.

A)

large; relatively small and independent; identical

B)

small; independent; identical or differentiated

C)

large; relatively small and independent; differentiated

D)

small; interdependent; identical or differentiated

15.

An industry characterized by a few interdependent firms and by barriers to entry is

called:

A)

perfect competition.

B)

monopolistic competition.

C)

monopoly.

D)

oligopoly.

16.

The sum of the squared market shares of each firm in an industry is the:

A)

concentration ratio.

B)

employment rate.

C)

Herfindahl–Hirschman index.

D)

market number.

17.

A monopoly will have a Herfindahl–Hirschman index equal to:

A)

1.

B)

100.

C)

1,000.

D)

10,000.

Page 4

18.

Which Herfindahl–Hirschman index is MOST likely to indicate a perfectly competitive

market?

A)

100

B)

1,800

C)

10,000

D)

100,000

19.

The Herfindahl–Hirschman index is a measure of concentration found by:

A)

squaring the percentage market share of each firm in the industry.

B)

squaring the percentage market share of each firm in the industry and then

summing the squared market shares.

C)

summing the percentage market shares of each firm in the industry.

D)

squaring the sums of the concentration ratios found in an industry survey of the

largest four and largest eight firms.

20.

The largest Herfindahl–Hirschman index possible is _____, and the industry is a(n)

_____.

A)

10; monopoly

B)

10,000; monopoly

C)

100,000; monopoly

D)

100,000; oligopoly

21.

The Herfindahl–Hirschman index equals _____ when _____ have/has _____% of the

market.

A)

10,000; four firms each; 25

B)

5,000; three firms each; 33

C)

5,000; two firms each; 50

D)

100,000; one firm; 100

22.

Large barriers to entry in the gas station business explain why the two only gas stations

in a small town:

A)

can earn an economic profit in the long run.

B)

must produce at the minimum average total cost in the long run.

C)

have no fixed costs in the long run.

D)

must produce a level of output such that MR = MC to maximize their profit.

Page 5

23.

An industry with only two firms is generally called:

A)

a monopoly.

B)

monopolistic competition.

C)

a duopoly.

D)

perfect competition.

24.

A duopoly is an industry that consists of:

A)

a single firm.

B)

two firms.

C)

three or more firms.

D)

a large number of small firms.

25.

An industry that consists of two firms is:

A)

a duopoly.

B)

a monopoly.

C)

a monopsony.

D)

monopolistic competition.

26.

_____ occurs when the only two firms in an industry agree to fix the price at a given

level.

A)

Collusion

B)

The ability to satisfy demand

C)

Price extortion

D)

Price leadership

27.

An extreme case of oligopoly in which firms collude to raise joint profits is known as a:

A)

duopoly.

B)

cartel.

C)

dominant producer.

D)

price war.

28.

If there are two gas stations in a very small town, then the gas station business there is

probably BEST characterized as:

A)

perfectly competitive.

B)

monopolistically competitive.

C)

monopolistic.

D)

oligopolistic.

Page 6

29.

Collusive agreements are typically difficult for cartels to maintain because each firm can

increase profits by:

A)

producing more than the quantity that maximizes joint profits.

B)

producing less than the quantity that maximizes joint profits.

C)

charging more than the price that maximizes joint cartel profits.

D)

advertising less than will maximize joint cartel profits.

30.

The owners of the gas stations in a town are trying to set up a cartel that will raise the

price of gasoline. Which scenario will INCREASE the chances that the cartel will fail

because of cheating by the owners?

A)

All of the gas stations face the same costs.

B)

There are only a few gas stations.

C)

The gas stations are producing as much as they can.

D)

The gas stations vary in terms of the services that they provide.

31.

In an oligopoly market, collusion between firms usually leads to higher profits than does

noncooperative behavior. However, formal, overt collusion doesn’t usually occur in the

United States because:

I. it is illegal.

II. there is an incentive for each firm to cheat on a collusive agreement.

III. an oligopolistic firm will typically prefer lower profits for itself if the only way to

make higher collective profits in the industry is to improve the profit position of its

rivals.

A)

I only

B)

II only

C)

I and II

D)

II and III

32.

Gary’s Gas and Frank’s Fuel are the only two providers of gasoline in their small town.

Gary and Frank decide to form a cartel to raise the price of gasoline. The total industry

profits are highest when _____ cheat(s) on the agreement, and Gary’s profits are highest

when _____.

A)

neither firm; neither firm cheats on the agreement

B)

neither firm; Gary cheats but Frank does not

C)

both firms; Gary cheats but Frank does not

D)

both Gary and Frank; both Gary and Frank cheat

Page 7

33.

In which situation does overt collusion take place?

A)

Smaller firms in an industry have an unspoken agreement to charge the same price

as the largest firm.

B)

Firms in an industry agree openly on price and output, and they jointly make other

decisions aimed at achieving monopoly profits.

C)

Competition among a large number of small firms generates similar but slightly

different prices.

D)

Competition among a large number of small firms generates a stable market price.

Use the following to answer questions 34-60:

34.

(Table: Demand Schedule of Gadgets) Use Table: Demand Schedule of Gadgets. The

market for gadgets consists of two producers, Margaret and Ray. Each firm can produce

gadgets with no marginal cost or fixed cost. If these two producers formed a cartel and

acted to maximize total industry profits, total industry output would be _____, and the

price would be _____.

A)

1,000; $10

B)

100; $9

C)

400; $6

D)

500; $5

Page 8

35.

(Table: Demand Schedule of Gadgets) Use Table: Demand Schedule of Gadgets. The

market for gadgets consists of two producers, Margaret and Ray. Each firm can produce

gadgets with no marginal cost or fixed cost. If these two producers formed a cartel and

acted to maximize total industry profits, total industry profit would be:

A)

$10,000.

B)

$5,000.

C)

$2,500.

D)

$1,250.

36.

(Table: Demand Schedule of Gadgets) Use Table: Demand Schedule of Gadgets. The

market for gadgets consists of two producers, Margaret and Ray. Each firm can produce

gadgets with no marginal cost or fixed cost. If these two producers formed a cartel, split

the production of output equally, and acted to maximize total industry profits, each

firm’s output would be _____, and each firm’s profit would be _____.

A)

500; $2,500

B)

250; $1,250

C)

1,000; $500

D)

1,000; $10,000

37.

(Table: Demand Schedule of Gadgets) Use Table: Demand Schedule of Gadgets. The

market for gadgets consists of two producers, Margaret and Ray. Each firm can produce

gadgets with no marginal cost or fixed cost. Suppose that these two producers have

formed a cartel and are maximizing total industry profits and splitting the production of

output evenly between themselves. If Margaret decides to cheat on the agreement and

sell 100 more gadgets, how many gadgets will she sell?

A)

0

B)

250

C)

350

D)

600

38.

(Table: Demand Schedule of Gadgets) Use Table: Demand Schedule of Gadgets. The

market for gadgets consists of two producers, Margaret and Ray. Each firm can produce

gadgets with no marginal cost or fixed cost. Suppose that these two producers have

formed a cartel, agreed to split production of output evenly, and are maximizing total

industry profits. If Margaret decides to cheat on the agreement and sell 100 more

gadgets, the market price of gadgets will be:

A)

$4.

B)

$5.

C)

$6.

D)

$7.

Page 9

39.

(Table: Demand Schedule of Gadgets) Use Table: Demand Schedule of Gadgets. The

market for gadgets consists of two producers, Margaret and Ray. Each firm can produce

gadgets with no marginal cost or fixed cost. Suppose that these two producers have

formed a cartel, agreed to split production of output evenly, and are maximizing total

industry profits. If Margaret decides to cheat on the agreement and sell 100 more

gadgets, Margaret’s profit will be _____, and Ray’s profit will be _____.

A)

$1,250; $1,250

B)

$500; $500

C)

$1,400; $1,000

D)

$1,000; $1,400

40.

(Table: Demand Schedule of Gadgets) Use Table: Demand Schedule of Gadgets. The

market for gadgets consists of two producers, Margaret and Ray. Each firm can produce

gadgets with no marginal cost or fixed cost. Suppose that these two producers have

formed a cartel, agreed to split production of output evenly, and are maximizing total

industry profits. If Margaret decides to cheat on the agreement and sell 100 more

gadgets, Margaret’s quantity effect will be a(n) _____ in profit of _____.

A)

decrease; $250

B)

increase; $150

C)

increase; $400

D)

decrease; $400

41.

(Table: Demand Schedule of Gadgets) Use Table: Demand Schedule of Gadgets. The

market for gadgets consists of two producers, Margaret and Ray. Each firm can produce

gadgets with no marginal cost or fixed cost. Suppose that these two producers have

formed a cartel, agreed to split production of output evenly, and are maximizing total

industry profits. If Margaret decides to cheat on the agreement and sell 100 more

gadgets, Margaret’s price effect will be a(n) _____ in profit of _____.

A)

decrease; $400

B)

increase; $400

C)

increase; $250

D)

decrease; $250

Page 10

42.

(Table: Demand Schedule of Gadgets) Use Table: Demand Schedule of Gadgets. The

market for gadgets consists of two producers, Margaret and Ray. Each firm can produce

gadgets with no marginal cost or fixed cost. Suppose that these two producers have

formed a cartel, agreed to split production of output evenly, and are maximizing total

industry profits. If Margaret decides to cheat on the agreement and sell 100 more

gadgets but Ray continues to sell 250 gadgets, Ray’s profits will be:

A)

$1,400.

B)

$1,250.

C)

$1,000.

D)

$400.

43.

(Table: Demand Schedule of Gadgets) Use Table: Demand Schedule of Gadgets. The

market for gadgets consists of two producers, Margaret and Ray. Each firm can produce

gadgets with no marginal cost or fixed cost. If industry output is 350 gadgets produced

by Margaret and 250 gadgets produced by Ray and if Ray decides to increase output by

an additional 100 gadgets, industry output will be:

A)

700.

B)

600.

C)

500.

D)

400.

44.

(Table: Demand Schedule of Gadgets) Use Table: Demand Schedule of Gadgets. The

market for gadgets consists of two producers, Margaret and Ray. Each firm can produce

gadgets with no marginal cost or fixed cost. If industry output is 350 gadgets produced

by Margaret and 250 gadgets produced by Ray and if Ray decides to increase output by

an additional 100 gadgets, industry price will be:

A)

$3.

B)

$2.

C)

$1.

D)

$0.

45.

(Table: Demand Schedule of Gadgets) Use Table: Demand Schedule of Gadgets. The

market for gadgets consists of two producers, Margaret and Ray. Each firm can produce

gadgets with no marginal cost or fixed cost. If industry output is 350 gadgets produced

by Margaret and 250 gadgets produced by Ray and if Ray decides to increase output by

an additional 100 gadgets, Margaret’s profit will be _____, and Ray’s profit will be

_____.

A)

$1,750; $1,250

B)

$1,250; $1,250

C)

$1,400; $1,000

D)

$1,050; $1,050

Page 11

46.

(Table: Demand Schedule of Gadgets) Use Table: Demand Schedule of Gadgets. The

market for gadgets consists of two producers, Margaret and Ray. Each firm can produce

gadgets with no marginal cost or fixed cost. If industry output is 700, each firm’s profits

will be _____ than they would be at the output of 500, which maximizes industry profit.

A)

$150 less

B)

$150 more

C)

$200 more

D)

$200 less

47.

(Table: Demand Schedule of Gadgets) Use Table: Demand Schedule of Gadgets. The

market for gadgets consists of two producers, Margaret and Ray. Each firm can produce

gadgets with no marginal cost or fixed cost. Suppose that these two producers have

formed a cartel, agreed to split production of output evenly, and are maximizing total

industry profits. Total industry output would be _____ gadgets.

A)

10

B)

5

C)

50

D)

500

48.

(Table: Demand Schedule of Gadgets) Use Table: Demand Schedule of Gadgets. The

market for gadgets consists of two producers, Margaret and Ray. Each firm can produce

gadgets at a marginal cost of $2 and no fixed cost. If these two producers formed a

cartel, agreed to split production of output evenly, and acted to maximize total industry

profits, total industry output would be _____, and the price would be _____.

A)

1,000; $10

B)

100; $9

C)

400; $6

D)

500; $5

49.

(Table: Demand Schedule of Gadgets) Use Table: Demand Schedule of Gadgets. The

market for gadgets consists of two producers, Margaret and Ray. Each firm can produce

gadgets at a marginal cost of $2 and no fixed cost. If these two producers formed a

cartel, agreed to split production of output evenly, and acted to maximize total industry

profits, total industry profit would be:

A)

$10,000.

B)

$5,000.

C)

$2,500.

D)

$1,600.

50.

(Table: Demand Schedule of Gadgets) Use Table: Demand Schedule of Gadgets. The

market for gadgets consists of two producers, Margaret and Ray. Each firm can produce

gadgets at a marginal cost of $2 and no fixed cost. Suppose that these two producers

have formed a cartel, agreed to split production of output evenly, and are maximizing

total industry profits. Each firm’s output would be _____, and each firm’s profit would

be _____.

A)

500; $2,500

B)

200; $800

C)

1,000; $500

D)

1,000; $10,000

51.

(Table: Demand Schedule of Gadgets) Use Table: Demand Schedule of Gadgets. The

market for gadgets consists of two producers, Margaret and Ray. Each firm can produce

gadgets at a marginal cost of $2 and no fixed cost. Suppose that these two producers

have formed a cartel, agreed to split production of output evenly, and are maximizing

total industry profits. If Margaret decides to cheat on the agreement and sell 100 more

gadgets, how many gadgets will Margaret sell?

A)

500

B)

200

C)

300

D)

600

52.

(Table: Demand Schedule of Gadgets) Use Table: Demand Schedule of Gadgets. The

market for gadgets consists of two producers, Margaret and Ray. Each firm can produce

gadgets at a marginal cost of $2 and no fixed cost. Suppose that these two producers

have formed a cartel, agreed to split production of output evenly, and are maximizing

total industry profits. If Margaret decides to cheat on the agreement and sell 100 more

gadgets, the market price of gadgets will be:

A)

$4.

B)

$5.

C)

$6.

D)

$7.

53.

(Table: Demand Schedule of Gadgets) Use Table: Demand Schedule of Gadgets. The

market for gadgets consists of two producers, Margaret and Ray. Each firm can produce

gadgets at a marginal cost of $2 and no fixed cost. Suppose that these two producers

have formed a cartel, agreed to split production of output evenly, and are maximizing

total industry profits. If Margaret decides to cheat on the agreement and sell 100 more

gadgets, Margaret’s profit will be _____, and Ray’s profit will be _____.

A)

$1500; $1,000

B)

$900; $600

C)

$1,400; $1,000

D)

$1,000; $1,400

54.

(Table: Demand Schedule of Gadgets) Use Table: Demand Schedule of Gadgets. The

market for gadgets consists of two producers, Margaret and Ray. Each firm can produce

gadgets at a marginal cost of $2 and no fixed cost. Suppose that these two producers

have formed a cartel, agreed to split production of output evenly, and are maximizing

total industry profits. If Margaret decides to cheat on the agreement and sell 100 more

gadgets, Margaret’s quantity effect will be a(n) _____ in profit of _____.

A)

decrease; $100

B)

increase; $100

C)

increase; $300

D)

decrease; $300

55.

(Table: Demand Schedule of Gadgets) Use Table: Demand Schedule of Gadgets. The

market for gadgets consists of two producers, Margaret and Ray. Each firm can produce

gadgets at a marginal cost of $2 and no fixed cost. Suppose that these two producers

have formed a cartel, agreed to split production of output evenly, and are maximizing

total industry profits. If Margaret decides to cheat on the agreement and sell 100 more

gadgets, Margaret’s price effect will be a(n) _____ in profit of _____.

A)

decrease; $400

B)

increase; $400

C)

increase; $200

D)

decrease; $200

56.

(Table: Demand Schedule of Gadgets) Use Table: Demand Schedule of Gadgets. The

market for gadgets consists of two producers, Margaret and Ray. Each firm can produce

gadgets at a marginal cost of $2 and no fixed cost. Suppose that these two producers

have formed a cartel, agreed to split production of output evenly, and are maximizing

total industry profits. If Margaret decides to cheat on the agreement and sell 100 more

gadgets but Ray continues to sell 200 gadgets, Ray’s profits will be:

A)

$1,400.

B)

$1,250.

C)

$600.

D)

$400.

57.

(Table: Demand Schedule of Gadgets) Use Table: Demand Schedule of Gadgets. The

market for gadgets consists of two producers, Margaret and Ray. Each firm can produce

gadgets at a marginal cost of $2 and no fixed cost. If industry output is 300 gadgets

produced by Margaret and 200 gadgets produced by Ray and if Ray decides to increase

output by an additional 100 gadgets, industry output will be:

A)

700.

B)

600.

C)

500.

D)

400.

58.

(Table: Demand Schedule of Gadgets) Use Table: Demand Schedule of Gadgets. The

market for gadgets consists of two producers, Margaret and Ray. Each firm can produce

gadgets at a marginal cost of $2 and no fixed cost. If industry output is 300 gadgets

produced by Margaret and 200 gadgets produced by Ray and if Ray decides to increase

output by an additional 100 gadgets, industry price will be:

A)

$4.

B)

$3.

C)

$2.

D)

$1.

59.

(Table: Demand Schedule of Gadgets) Use Table: Demand Schedule of Gadgets. The

market for gadgets consists of two producers, Margaret and Ray. Each firm can produce

gadgets at a marginal cost of $2 and no fixed cost. If industry output is 300 gadgets

produced by Margaret and 200 gadgets produced by Ray and if Ray decides to increase

output by an additional 100 gadgets, Margaret’s profit will be _____, and Ray’s profit

will be _____.

A)

$1,750; $1,250

B)

$1,250; $1,250

C)

$1,400; $1,000

D)

$600; $600

Page 15

60.

(Table: Demand Schedule of Gadgets) Use Table: Demand Schedule of Gadgets. The

market for gadgets consists of two producers, Margaret and Ray. Each firm can produce

gadgets at a marginal cost of $2 and no fixed cost. If the industry were actually perfectly

competitive, the output would be _____ gadgets, and the price would be _____.

A)

0; $10

B)

500; $5

C)

600; $4

D)

800; $2

Use the following to answer questions 61-71:

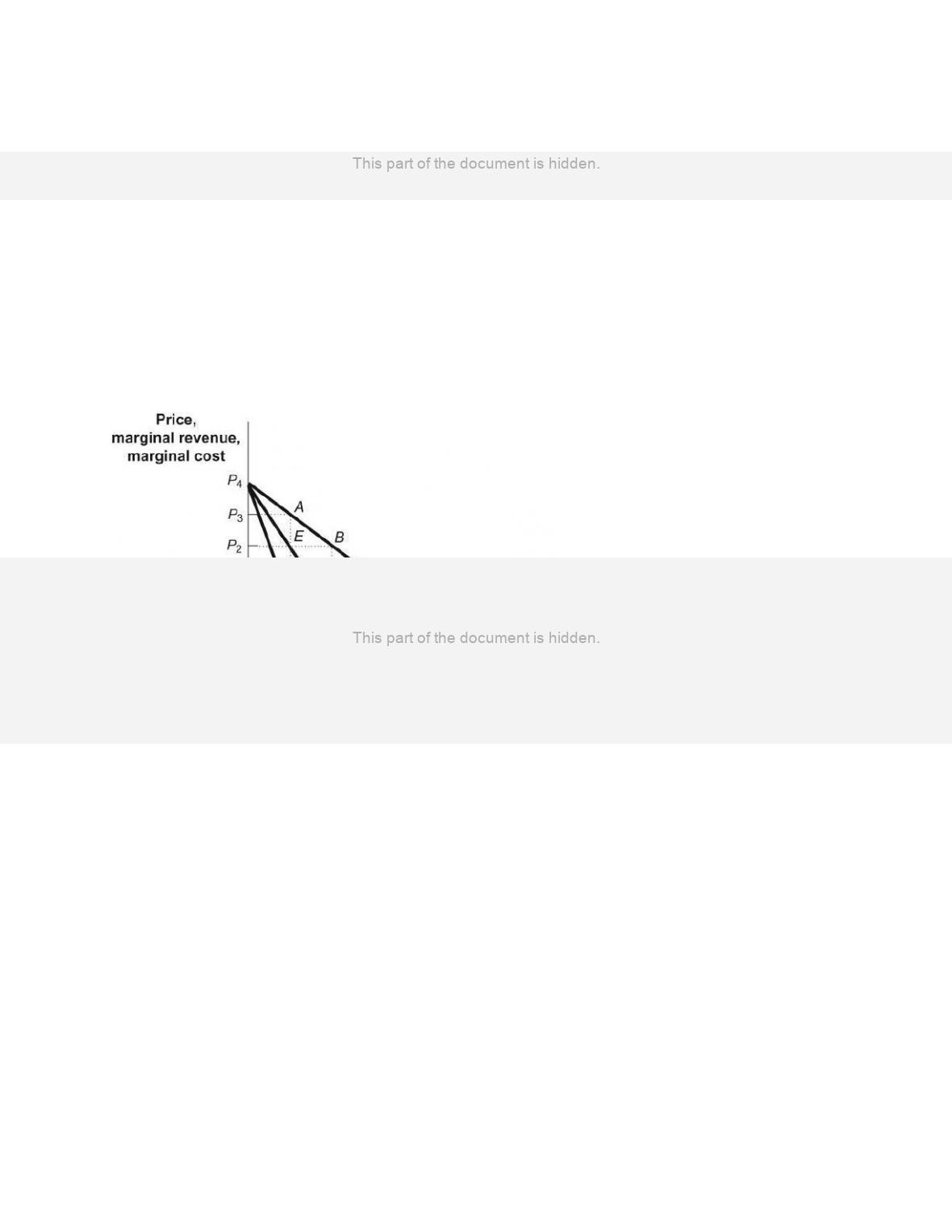

Figure: Monopoly Profits in Duopoly

61.

(Figure: Monopoly Profits in Duopoly) Use Figure: Monopoly Profits in Duopoly. If

there were two firms in this industry, they could engage in _____ and reap monopoly

profits.

A)

game theory

B)

the prisoners’ dilemma

C)

collusive behavior

D)

measuring the four-firm concentration ratio

Page 16

62.

(Figure: Monopoly Profits in Duopoly) Use Figure: Monopoly Profits in Duopoly.

Suppose there are two firms in this industry. Each firm faces an identical demand curve,

D1, and the market demand curve is D2. The figure illustrates how firms can reap

monopoly profits, even in an industry with:

A)

free entry and exit.

B)

two firms.

C)

monopolistic competition.

D)

a four-firm concentration ratio of 50.

63.

(Figure: Monopoly Profits in Duopoly) Use Figure: Monopoly Profits in Duopoly. The

figure shows how an industry consisting of two firms that face identical demand curves

(D1) can collude to increase profits. Which assumption is NOT a part of the analysis

illustrated by the model?

A)

The two firms are identical.

B)

The two firms sell identical products.

C)

While the firms face the same MC curves, their respective TC curves have unequal

slopes.

D)

Each firm has a horizontal marginal cost curve.

64.

(Figure: Monopoly Profits in Duopoly) Use Figure: Monopoly Profits in Duopoly. The

figure shows how an industry consisting of two firms that face identical demand curves

(D1) can collude to increase profits. The market demand curve is D2. Which assumption

is part of the analysis illustrated by the model?

A)

The two firms have identical marginal cost but different average total cost.

B)

The two firms sell differentiated products.

C)

The MR curve is not relevant to either firm’s choices.

D)

The firms can act as a cartel and maximize their combined economic profit.

65.

(Figure: Monopoly Profits in Duopoly) Use Figure: Monopoly Profits in Duopoly. The

figure shows how an industry consisting of two firms that face identical demand curves

(D1) can collude to increase profits. The market demand curve is D2. If the firms collude

to share the market demand equally, then each firm will act as if its demand curve is

given by:

A)

D1.

B)

D2.

C)

MR1.

D)

2 × D1.

Page 17

66.

(Figure: Monopoly Profits in Duopoly) Use Figure: Monopoly Profits in Duopoly. The

figure shows how an industry consisting of two firms that face identical demand curves

(D1) can collude to increase profits. If the firms collude to share the market demand

equally, then each firm will act as if its marginal revenue curve is given by:

A)

MR1.

B)

2 × MR1.

C)

MR2.

D)

MC.

67.

(Figure: Monopoly Profits in Duopoly) Use Figure: Monopoly Profits in Duopoly. The

figure shows how an industry consisting of two firms that face identical demand curves

(D1) can collude to increase profits. If the firms collude to share the market demand

equally, then each firm will act as if its demand curve is given by _____, while the

market demand curve is given by _____.

A)

D1; MR2

B)

D2; D1

C)

D1; D2

D)

MR1; MR2

68.

(Figure: Monopoly Profits in Duopoly) Use Figure: Monopoly Profits in Duopoly.

Given the duopoly industry illustrated in the figure, if each firm acted on the belief that

it faced demand curve D2 and acted without consideration of the other, each firm would

attempt to maximize economic profits by producing quantity _____ and setting price

equal to _____.

A)

Q4; P1

B)

Q4; P2

C)

Q1; P4

D)

Q2; P2

69.

(Figure: Monopoly Profits in Oligopoly) Use Figure: Monopoly Profits in Duopoly.

Firms in the duopoly industry illustrated in the figure have zero fixed costs. The market

demand curve is D2. If the two firms colluded to maximize their combined economic

profits, they would set the market price at _____, and combined economic profits of the

firms would be _____.

A)

P1; given by the area of the rectangle 0P1CQ4

B)

P1; zero

C)

P3; given by the area of the rectangle 0P3AQ1

D)

P2; given by the area of the rectangle P1P2BG

Page 18

70.

(Figure: Monopoly Profits in Duopoly) Use Figure: Monopoly Profits in Duopoly. The

efficient solution in the figure is found where price is _____ and quantity is _____.

A)

P1; Q4

B)

P2; Q2

C)

P2; Q1

D)

P3; Q1

71.

(Figure: Monopoly Profits in Duopoly) Use Figure: Monopoly Profits in Duopoly. If the

two firms in the figure colluded to split production evenly and to maximize their joint

profits, the market price they set would be _____, and each firm’s economic profit

would be _____. (Assume that the market demand curve is D2.)

A)

P2; given by the area of the rectangle bounded by P1P2EF = FEBG

B)

P1; P1P3AF

C)

P3; given by the area of the rectangle bounded by 0P3AQ1

D)

P2; given by the area of the rectangle bounded by P1P2BG

Use the following to answer questions 72-73:

Figure: Collusion

72.

(Figure: Collusion) Use Figure: Collusion. The quantity of output produced by the

industry with collusion is shown by:

A)

Q.

B)

R.

C)

S.

D)

T.

Page 19

73.

(Figure: Collusion) Use Figure: Collusion. The price charged by the industry with

collusion is shown by:

A)

W.

B)

X.

C)

Y.

D)

Z.

Use the following to answer questions 74-83:

74.

(Table: Demand for Crude Oil) Use Table: Demand for Crude Oil. Assume that the

crude oil industry is a duopoly and the marginal cost of producing crude oil is zero. If

the two firms collude to share the market equally, the price of crude oil will be _____,

firm 1 will produce _____ barrels, firm 2 will produce _____ barrels, and each firm will

earn revenue equal to _____.

A)

$80; 80; 80; $6,400

B)

$80; 40; 40; $3,200

C)

$60; 50; 50; $3,000

D)

$40; 60; 60; $2,400

Page 20

75.

(Table: Demand for Crude Oil) Use Table: Demand for Crude Oil. The marginal cost of

producing crude oil is zero. If the crude oil industry is a monopoly, the price of crude oil

will be _____, the total quantity of crude oil produced by the monopoly will be _____

barrels, and the monopoly will earn revenue equal to _____.

A)

$80; 80; $6,400

B)

$80; 80; $0

C)

$160; 0; $0

D)

$60; 100; $6,000

76.

(Table: Demand for Crude Oil) Use Table: Demand for Crude Oil. Assume that the

crude oil industry is a duopoly and the marginal cost of producing crude oil is zero.

Suppose that the two firms are maximizing industry profit and splitting the profit

evenly. If firm 1 decides to cheat and increase production by 10 more barrels, total

industry output will be _____ barrels.

A)

160

B)

100

C)

90

D)

80

77.

(Table: Demand for Crude Oil) Use Table: Demand for Crude Oil. Assume that the

crude oil industry is a duopoly and the marginal cost of producing crude oil is zero.

Suppose that the two firms are maximizing industry profit and splitting the profit

evenly. If firm 1 decides to cheat and increase production by 10 more barrels, the price

of crude oil will be:

A)

$0.

B)

$70.

C)

$80.

D)

$160.

78.

(Table: Demand for Crude Oil) Use Table: Demand for Crude Oil. Assume that the

crude oil industry is a duopoly and the marginal and fixed cost of producing crude oil

equals zero. Suppose that the two firms are maximizing industry profit and splitting the

profit evenly. If firm 1 decides to cheat and increase production by 10 more barrels, it

will earn profits of:

A)

$6,400.

B)

$6,300.

C)

$3,500.

D)

$2,800.