Page 76

Use the following to answer question 326:

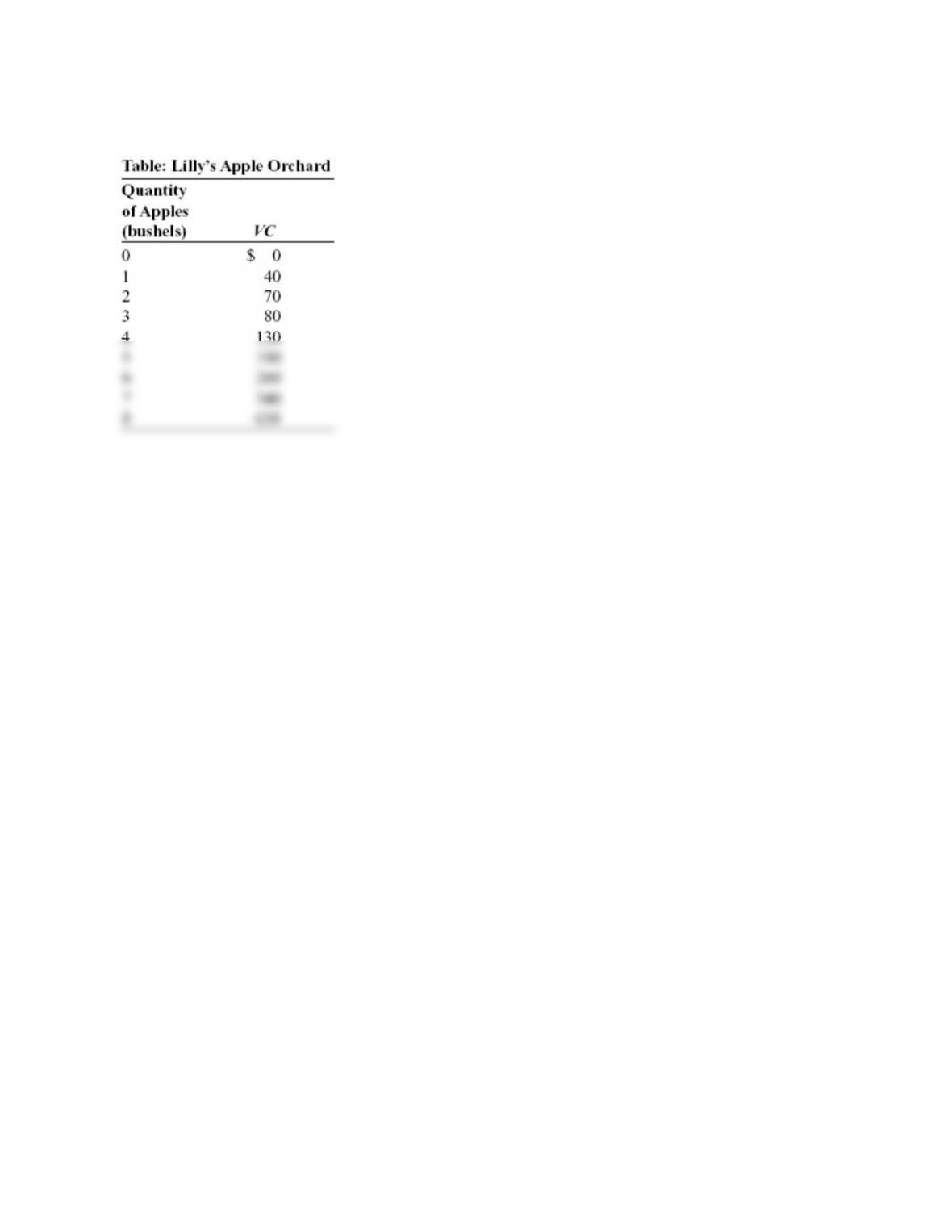

326.

(Table: Lilly’s Apple Orchard) Use Table: Lilly’s Apple Orchard. Lilly is the

price-taking owner of an apple orchard. Her orchard has fixed costs of $30. If the price

of a bushel of apples is $80, how many bushels will Lilly produce? Is this a long-run

equilibrium? If not, what will be the price of a bushel of apples in the long run? Show

your work.

327.

In a perfectly competitive market, _____ are price takers.

A)

only consumers

B)

only producers

C)

both producers and consumers

D)

neither producers nor consumers

328.

Perfectly competitive industries are characterized by:

A)

few sellers and many buyers.

B)

consumers who can differentiate between products.

C)

standardized goods.

D)

a few producers who make up most of the market share of the industry.

329.

In perfect competition, _____ are _____, and _____ are price takers.

A)

all goods; standardized; all market participants

B)

some goods; standardized; consumers but not producers

C)

all goods; differentiated; producers but not consumers

D)

some goods; differentiated; consumers but not producers

Page 77

330.

When a firm produces at an output level at which MR = MC, it is operating at the _____

level.

A)

shut-down

B)

break-even

C)

optimal-output

D)

minimum-cost

331.

The addition to the total revenue from selling one more unit of the good is:

A)

less than the market price.

B)

average profit.

C)

marginal cost.

D)

marginal revenue.

332.

Ashley, who makes knitted caps, determines that her marginal cost of knitting one more

cap is $10. A consumer offers her $12 for one more knitted cap. Ashley will:

A)

not sell the additional cap since she does not know what her total costs will be.

B)

sell the additional cap since the marginal revenue is greater than the marginal cost

for the unit.

C)

realize that her production is not profitable and shut down her business.

D)

offer to sell 20 additional caps since it must be profitable.

333.

Tony runs Read Economic Reports. If Tony finds that the cost of completing an

additional report is $100 and someone offers him $125 to complete this additional

report, Tony should:

A)

not complete the additional report since he will incur a loss.

B)

complete the additional report only if the person buys two additional reports.

C)

complete the additional report.

D)

not complete the additional report since his additional cost is more than his

additional revenue.

334.

Firms will make a profit in the long run or short run if the price is:

A)

equal to marginal revenue.

B)

greater than ATC.

C)

less than MC.

D)

greater than AVC.

Page 78

335.

If a firm’s economic profits are equal to zero, its accounting profits are MOST likely:

A)

less than zero.

B)

positive.

C)

less than fixed costs.

D)

equal to zero.

336.

A firm produces at the output level at which its average total costs are minimized. At

this output level, its average total costs are NOT equal to:

A)

price.

B)

MC.

C)

MR.

D)

AVC.

337.

Maximizing profits also means that a firm is attempting to:

A)

make as much output as possible.

B)

change the market price.

C)

produce at the output level where the difference between total revenue and total

cost is the greatest.

D)

produce below its break-even price.

338.

In the short run, a firm will continue to sell its product as long as:

A)

it is making a positive profit.

B)

the price is greater than average total costs.

C)

the price is greater than average variable costs.

D)

its marginal cost is increasing.

339.

In the short run, a firm will produce as long as the price is GREATER than its:

A)

ATC.

B)

MC.

C)

MR.

D)

AVC.

340.

In the short run, fixed costs:

A)

are an important feature in a firm’s decision to produce or not produce.

B)

have no impact on a firm’s profit level.

C)

do not exist.

D)

remain constant.

Page 79

341.

A perfectly competitive firm will produce:

A)

whenever it can.

B)

mostly in the long run and only if price is greater than AFC.

C)

with a loss in the short run if its price is greater than AVC but less than ATC.

D)

only when it earns profits in the short run.

342.

In the short run, for a perfectly competitive firm, the portion of the MC curve at or

above the shut-down price is also its:

A)

individual short-run supply curve.

B)

ATC curve.

C)

AVC curve.

D)

individual demand curve.

343.

Hank operates a perfectly competitive firm in the long run. For several periods, the

market price has been $20, and his break-even price is $22. Given the chance to change

his fixed costs, Hank should:

A)

stay in the industry since he can cover his fixed costs.

B)

seriously consider exiting the industry since he is consistently making economic

losses.

C)

stay in the industry since he is a perfect competitor and must take the price as

given.

D)

wait for the short-run period.

Use the following to answer questions 344-345:

Page 80

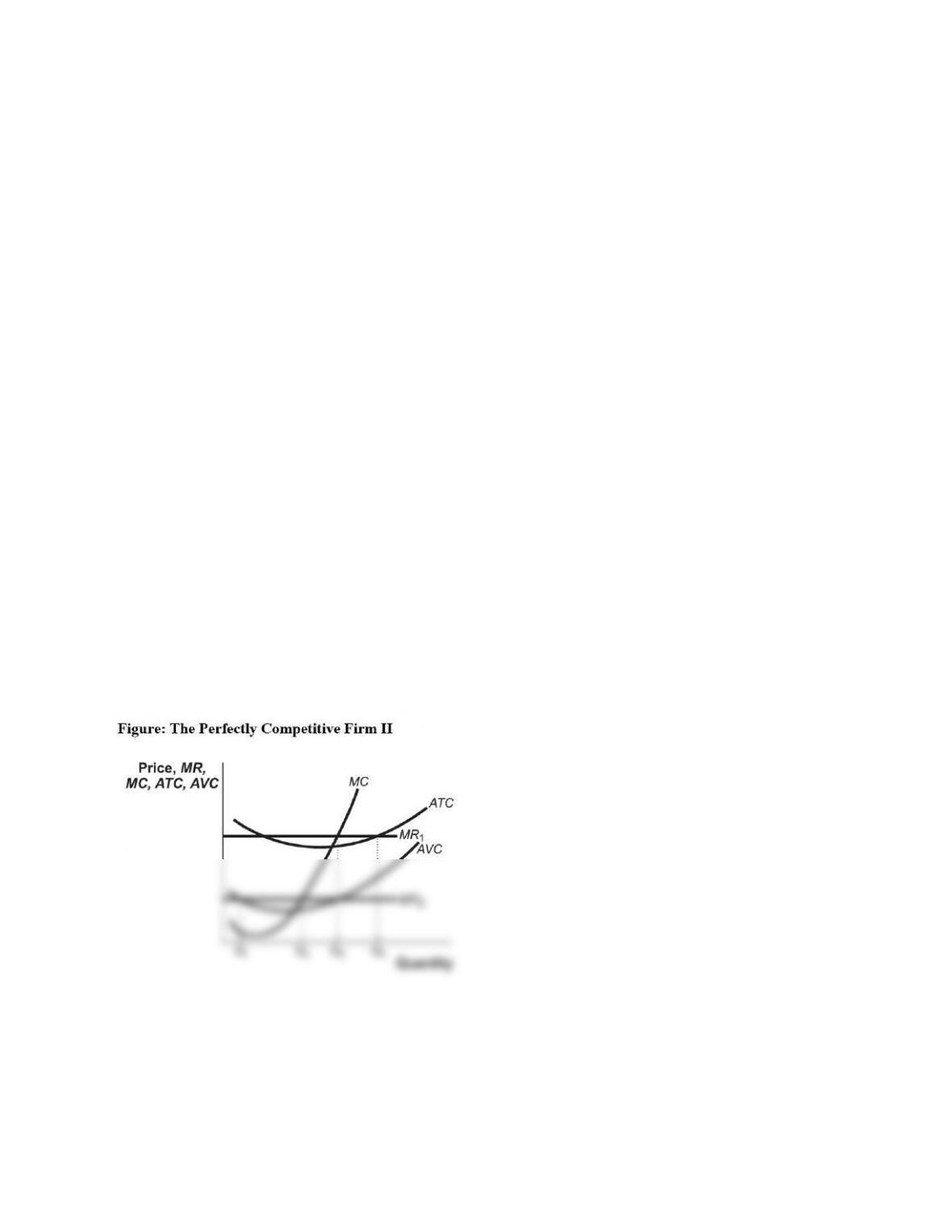

344.

(Figure: The Perfectly Competitive Firm II) Use Figure: The Perfectly Competitive

Firm II. If this firm’s MR curve is MR1, the firm will maximize profit by producing

_____ units of output, and its economic profit will be _____.

A)

Q1; positive

B)

Q2; negative

C)

Q3; positive

D)

Q4; negative

345.

(Figure: The Perfectly Competitive Firm II) Use Figure: The Perfectly Competitive

Firm II. If this firm’s MR curve is MR2, then this firm’s optimal output is _____ units of

output and its economic profit will be _____.

A)

Q1; positive

B)

Q2; negative

C)

Q3; positive

D)

Q4; negative

346.

The horizontal sum of individual firms’ MC curves (specifically the portions above

AVC) is the:

A)

short-run industry demand curve.

B)

short-run industry supply curve.

C)

long-run fixed cost curve.

D)

long-run average variable cost curve.

347.

A perfectly competitive industry has 10 firms, each with an MC curve that can be

expressed as MC = 5q, where q is the level of output for each firm. Which equation

would describe the industry supply curve, where Q is the market quantity and P is the

market price?

A)

P = Q

B)

P = 0.5Q

C)

P = 2Q

D)

P = 5Q

348.

In the long run, each firm in a perfectly competitive industry will:

A)

earn only enough to cover the opportunity costs of all resources used in production.

B)

produce where MR is greater than MC.

C)

differentiate its goods.

D)

increase its price.

Page 81

349.

If the long-run market supply curve for a perfectly competitive market is horizontal,

then this industry exhibits _____ costs.

A)

constant

B)

decreasing

C)

increasing

D)

an absence of marginal

350.

In a perfectly competitive market, tastes and preferences lead to an increase in the

demand for the good. Holding everything else constant, this will lead to an increase in

price that will result in _____ in the short run, which will in turn _____, which will

_____.

A)

positive economic profits; attract new firms; reduce the price

B)

economic losses; attract new firms; reduce the price

C)

positive economic profits; lead some firms to leave the industry; further increase

the price

D)

economic losses; lead some firms to leave the industry; further increase the price

351.

A perfectly competitive industry with constant costs initially operates in long-run

equilibrium. When demand increases:

A)

in the short run, prices and profits will be higher, but in the long run, price will fall

back to its original level and firms will again earn zero economic profit.

B)

prices and profits will be higher than before the demand increase in both the long

run and the short run.

C)

in the short run, prices and profits will fall, but in the long run, price will rise back

to its initial level, as will profits.

D)

prices and profits will be lower than before the demand increase in both the long

run and the short run.

352.

A perfectly competitive industry with constant costs initially operates in long-run

equilibrium. When demand increases, in the long run and the short run:

A)

positive economic profits will result for all firms.

B)

higher prices will result.

C)

output will increase.

D)

negative economic profits will result for some firms.

353.

In the long run, all of the firms in a perfectly competitive industry will:

A)

produce at an output level at which average total cost equals marginal cost.

B)

earn an economic profit greater than zero.

C)

exit the industry if price is greater than average total cost.

D)

produce an output level at which price is greater than average total cost.

Page 82

354.

Bob runs a pedicure business in a perfectly competitive industry. He knows that he will

break even if the price of pedicures is $15 but that he will have to shut down if the price

is $11 or lower. If the market demand in the industry is P = 30 – (0.2)Q and the market

supply is P = (0.2)Q, in the short run, Bob will:

A)

shut down since he cannot cover any of his variable costs.

B)

produce but make zero economic profit.

C)

produce with a loss since he is operating below his break-even level.

D)

shut down, although he is making a positive economic profit.

Answer Key

Page 84

45.

B

46.

A

47.

B

48.

A

49.

D

50.

B

51.

B

52.

B

53.

A

54.

A

55.

B

56.

B

57.

A

58.

C

59.

B

60.

A

61.

D

62.

D

63.

A

64.

D

65.

B

66.

A

67.

B

68.

B

69.

D

70.

B

71.

A

72.

B

73.

A

74.

B

75.

A

76.

D

77.

C

78.

A

79.

A

80.

A

81.

B

82.

A

83.

C

84.

D

85.

D

86.

A

87.

C

88.

D

89.

B

90.

B

Page 85

91.

C

92.

B

93.

C

94.

D

95.

A

96.

B

97.

B

98.

C

99.

D

100.

A

101.

A

102.

D

103.

A

104.

B

105.

D

106.

C

107.

B

108.

C

109.

B

110.

D

111.

B

112.

D

113.

B

114.

D

115.

B

116.

B

117.

B

118.

B

119.

A

120.

B

121.

C

122.

A

123.

D

124.

C

125.

B

126.

C

127.

D

128.

C

129.

A

130.

D

131.

B

132.

C

133.

B

134.

B

135.

A

136.

D

Page 86

137.

B

138.

B

139.

C

140.

A

141.

C

142.

B

143.

D

144.

C

145.

C

146.

B

147.

C

148.

A

149.

D

150.

A

151.

B

152.

B

153.

C

154.

A

155.

D

156.

C

157.

D

158.

D

159.

C

160.

A

161.

D

162.

D

163.

B

164.

B

165.

C

166.

B

167.

A

168.

A

169.

B

170.

C

171.

B

172.

D

173.

A

174.

D

175.

C

176.

B

177.

C

178.

C

179.

B

180.

D

181.

C

182.

A

Page 87

183.

A

184.

B

185.

A

186.

B

187.

A

188.

A

189.

C

190.

B

191.

A

192.

C

193.

A

194.

C

195.

A

196.

A

197.

B

198.

B

199.

C

200.

A

201.

C

202.

A

203.

A

204.

D

205.

D

206.

B

207.

A

208.

B

209.

D

210.

D

211.

B

212.

B

213.

D

214.

C

215.

B

216.

D

217.

C

218.

C

219.

D

220.

B

221.

A

222.

D

223.

C

224.

C

225.

B

226.

C

227.

A

228.

A

Page 88

229.

B

230.

C

231.

A

232.

D

233.

C

234.

B

235.

A

236.

C

237.

C

238.

C

239.

A

240.

B

241.

C

242.

B

243.

D

244.

C

245.

D

246.

A

247.

B

248.

D

249.

B

250.

D

251.

C

252.

A

253.

A

254.

D

255.

C

256.

D

257.

C

258.

C

259.

D

260.

D

261.

B

262.

A

263.

A

264.

C

265.

D

266.

B

267.

D

268.

A

269.

B

270.

C

271.

C

272.

C

273.

D

274.

C

Page 89

275.

D

276.

C

277.

A

278.

C

279.

B

280.

D

281.

B

282.

A

283.

D

284.

A

285.

B

286.

C

287.

D

288.

C

289.

D

290.

B

291.

B

292.

A

293.

A

294.

A

295.

A

296.

B

297.

B

298.

A

299.

A

300.

B

301.

A

302.

A

303.

A

304.

A

305.

B

306.

B

307.

A

308.

B

309.

B

310.

B

311.

A

312.

B

313.

A

314.

A

315.

316.

317.

318.

319.

320.

Page 90

321.

322.

323.

324.

325.

326.

327.

C

328.

C

329.

A

330.

C

331.

D

332.

B

333.

C

334.

B

335.

B

336.

D

337.

C

338.

C

339.

D

340.

D

341.

C

342.

A

343.

B

344.

C

345.

B

346.

B

347.

B

348.

A

349.

A

350.

A

351.

A

352.

C

353.

A

354.

B