Page 61

262.

(Table: Workers and Output) Use Table: Workers and Output. After graduation, you

achieve your dream of opening an art shop that specializes in selling mud statues. You

pay $10 per day on a loan from your uncle, regardless of how much you produce. You

also pay $10 per day to each of the workers who you hire to make the mud statues. The

variable cost of producing 43 statues is:

A)

$10.

B)

$20.

C)

$40.

D)

$43.

263.

(Table: Workers and Output) Use Table: Workers and Output. After graduation, you

achieve your dream of opening an art shop that specializes in selling mud statues. You

pay $10 per day on a loan from your uncle, regardless of how much you produce. You

also pay $10 per day to each of the workers who you hire to make the mud statues. The

total cost of producing 43 statues is:

A)

$10.

B)

$20.

C)

$40.

D)

$50.

264.

(Table: Workers and Output) Use Table: Workers and Output. After graduation, you

achieve your dream of opening an art shop that specializes in selling mud statues. You

pay $10 per day on a loan from your uncle, regardless of how much you produce. You

also pay $10 per day to each of the workers who you hire to make the mud statues. The

variable cost of producing 48 statues is:

A)

$50.

B)

$48.

C)

$20.

D)

$10.

265.

(Table: Workers and Output) Use Table: Workers and Output. After graduation, you

achieve your dream of opening an art shop that specializes in selling mud statues. You

pay $10 per day on a loan from your uncle, regardless of how much you produce. You

also pay $10 per day to each of the workers who you hire to make the mud statues. The

total cost of producing 48 statues is:

A)

$240.

B)

$60.

C)

$50.

D)

$10.

266.

(Table: Workers and Output) Use Table: Workers and Output. After graduation, you

achieve your dream of opening an art shop that specializes in selling mud statues. You

pay $10 per day on a loan from your uncle, regardless of how much you produce. You

also pay $10 per day to each of the workers who you hire to make the mud statues. How

many workers should you hire to minimize your marginal cost?

A)

two

B)

three

C)

four

D)

five

267.

(Table: Output and Costs) Use Table: Output and Costs. When output increases from 1

to 2, marginal cost equals:

A)

$13.

B)

$10.

C)

$8.

D)

$17.

268.

(Table: Output and Costs) Use Table: Output and Costs. When output is 4, total variable

cost equals:

A)

$48.

B)

$38.

C)

$58.

D)

$28.

269.

(Table: Output and Costs) Use Table: Output and Costs. When output is 3, average total

cost equals:

A)

$13.

B)

$10.

C)

$8.

D)

$17.

Page 63

Use the following to answer questions 270-273:

270.

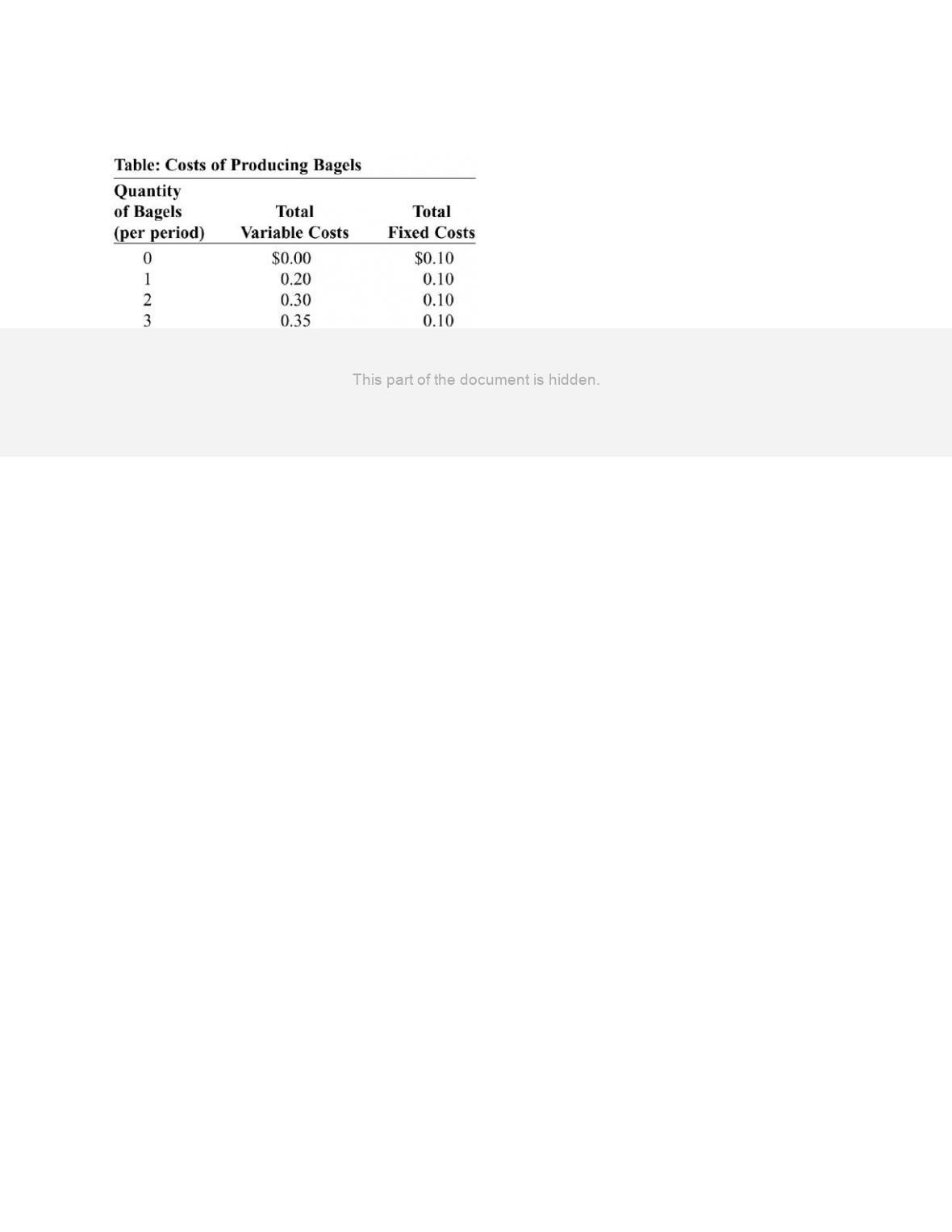

(Table: Costs of Producing Bagels) Use Table: Cost of Producing Bagels. The total cost

of producing 6 bagels is:

A)

$0.10.

B)

$0.20.

C)

$0.80.

D)

$0.90.

271.

(Table: Costs of Producing Bagels) Use Table: Cost of Producing Bagels. The marginal

cost of producing the sixth bagel is:

A)

$0.10.

B)

$0.15.

C)

$0.20.

D)

$0.80.

272.

(Table: Costs of Producing Bagels) Use Table: Cost of Producing Bagels. Marginal cost

reaches its minimum value for the _____ bagel.

A)

first

B)

third

C)

fourth

D)

fifth

Page 64

273.

(Table: Costs of Producing Bagels) Use Table: Cost of Producing Bagels. Average total

cost reaches its minimum value for the _____ bagel.

A)

first

B)

third

C)

fourth

D)

fifth

274.

(Table: Costs of Producing Bagels) Use Table: Cost of Producing Bagels. The average

total cost of producing 6 bagels is:

A)

$0.10.

B)

$0.15.

C)

$0.20.

D)

$0.80.

275.

(Table: Costs of Producing Bagels) Use Table: Cost of Producing Bagels. The total cost

of producing 2 bagels is:

A)

$0.10.

B)

$0.20.

C)

$0.40.

D)

$0.50.

276.

(Table: Costs of Producing Bagels) Use Table: Cost of Producing Bagels. The average

total cost of producing 2 bagels is:

A)

$0.05.

B)

$0.10.

C)

$0.20.

D)

$0.40.

277.

(Table: Costs of Producing Bagels) Use Table: Cost of Producing Bagels. The marginal

cost of producing the second bagel is:

A)

$0.05.

B)

$0.10.

C)

$0.30.

D)

$0.40.

Page 65

Use the following to answer questions 278-292:

278.

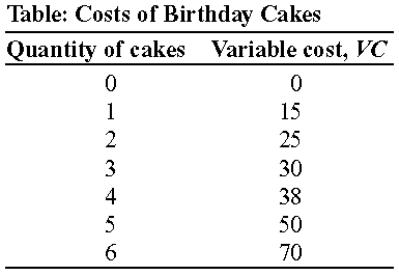

(Table: Costs of Birthday Cakes) Use Table: Costs of Birthday Cakes. Assume that

fixed costs are $10. What is the average variable cost of 2 cakes?

A)

$40.00

B)

$35.00

C)

$25.00

D)

$12.50

279.

(Table: Costs of Birthday Cakes) Use Table: Costs of Birthday Cakes. Assume that

fixed costs are $10. What is the average fixed cost of 2 cakes?

A)

$5

B)

$10

C)

$25

D)

$30

280.

(Table: Costs of Birthday Cakes) Use Table: Costs of Birthday Cakes. Assume that

fixed costs are $10. What is the average total cost of 2 cakes?

A)

$35.00

B)

$25.00

C)

$17.50

D)

$12.50

281.

(Table: Costs of Birthday Cakes) Use Table: Costs of Birthday Cakes. Assume that

fixed costs are $10. What is the marginal cost of the second cake?

A)

$5

B)

$10

C)

$25

D)

$35

Page 66

282.

(Table: Costs of Birthday Cakes) Use Table: Costs of Birthday Cakes. Assume that

fixed costs are $10. What is the average variable cost of 4 cakes?

A)

$38.00

B)

$10.00

C)

$9.50

D)

$8.00

283.

(Table: Costs of Birthday Cakes) Use Table: Costs of Birthday Cakes. Assume that

fixed costs are $10. What is the average fixed cost of 4 cakes?

A)

$48.00

B)

$10.00

C)

$5.00

D)

$2.50

284.

(Table: Costs of Birthday Cakes) Use Table: Costs of Birthday Cakes. Assume that

fixed costs are $10. What is the average total cost of 4 cakes?

A)

$35.00

B)

$25.00

C)

$9.50

D)

$12.00

285.

(Table: Costs of Birthday Cakes) Use Table: Costs of Birthday Cakes. Assume that

fixed costs are $10. What is the marginal cost of the fourth cake?

A)

$8

B)

$10

C)

$25

D)

$35

286.

(Table: Costs of Birthday Cakes) Use Table: Costs of Birthday Cakes. Assume that

fixed costs are $10. What is the average variable cost of 5 cakes?

A)

$300

B)

$250

C)

$50

D)

$10

Page 67

287.

(Table: Costs of Birthday Cakes) Use Table: Costs of Birthday Cakes. Assume that

fixed costs are $10. What is the average fixed cost of 5 cakes?

A)

$1

B)

$2

C)

$5

D)

$10

288.

(Table: Costs of Birthday Cakes) Use Table: Costs of Birthday Cakes. Assume that

fixed costs are $10. What is the average total cost of 5 cakes?

A)

$110

B)

$60

C)

$12

D)

$2

289.

(Table: Costs of Birthday Cakes) Use Table: Costs of Birthday Cakes. Assume that

fixed costs are $10. What is the marginal cost of the fifth cake?

A)

$2

B)

$10

C)

$12

D)

$20

290.

(Table: Costs of Birthday Cakes) Use Table: Costs of Birthday Cakes. Assume that

fixed costs are $10. The point of diminishing returns begins when output exceeds:

A)

2.

B)

3.

C)

4.

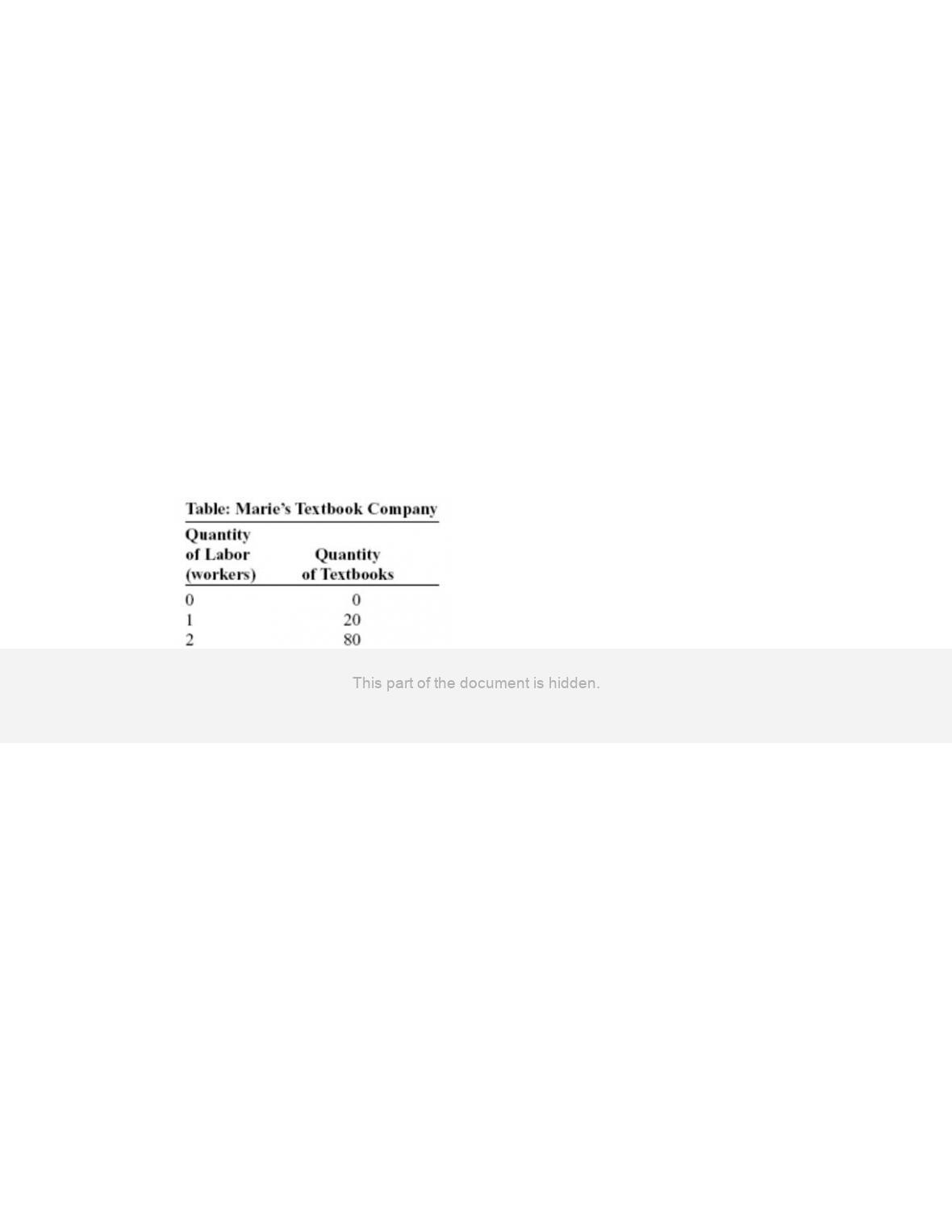

D)

5.

291.

(Table: Costs of Birthday Cakes) Use Table: Costs of Birthday Cakes. Assume that

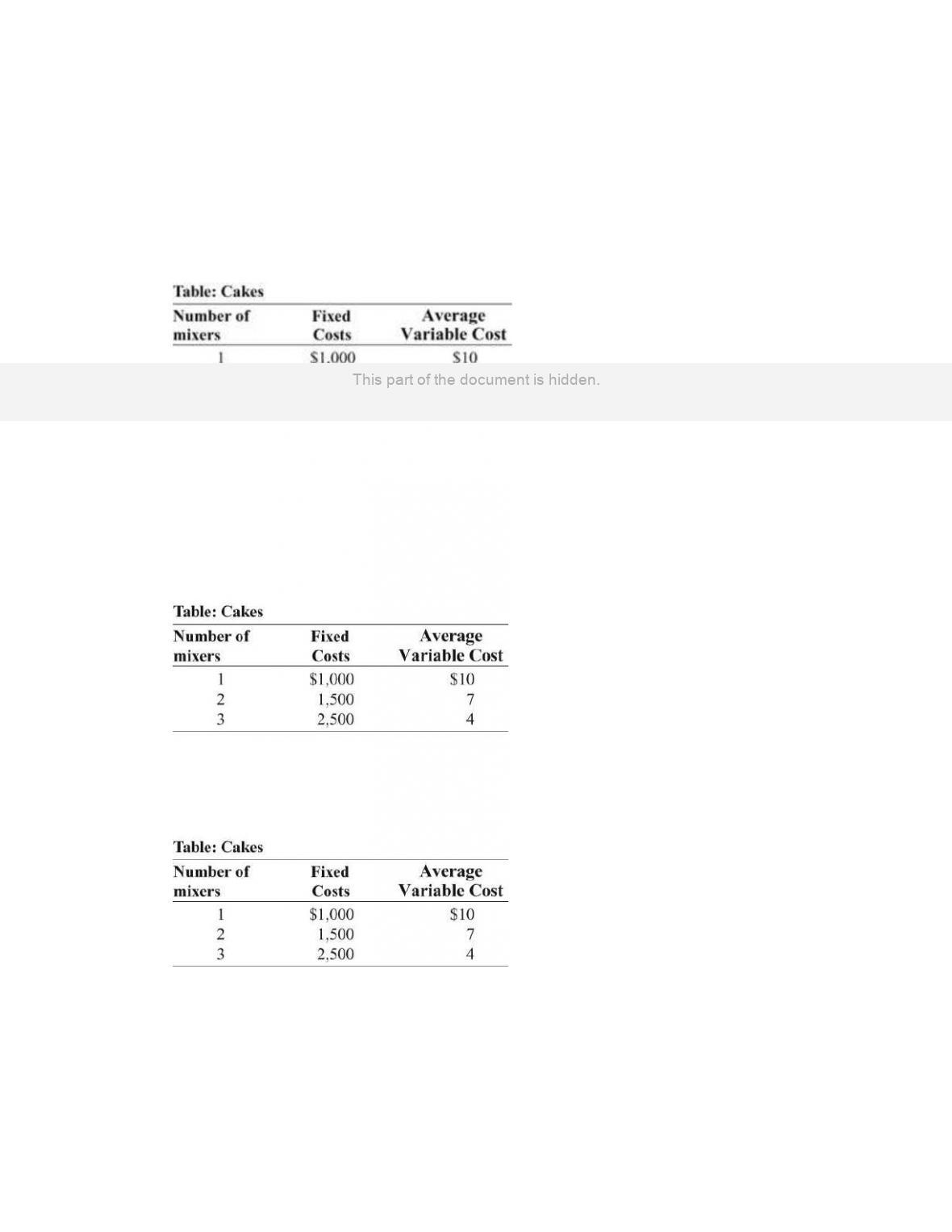

fixed costs are $10. The minimum average variable cost occurs at output of:

A)

2.

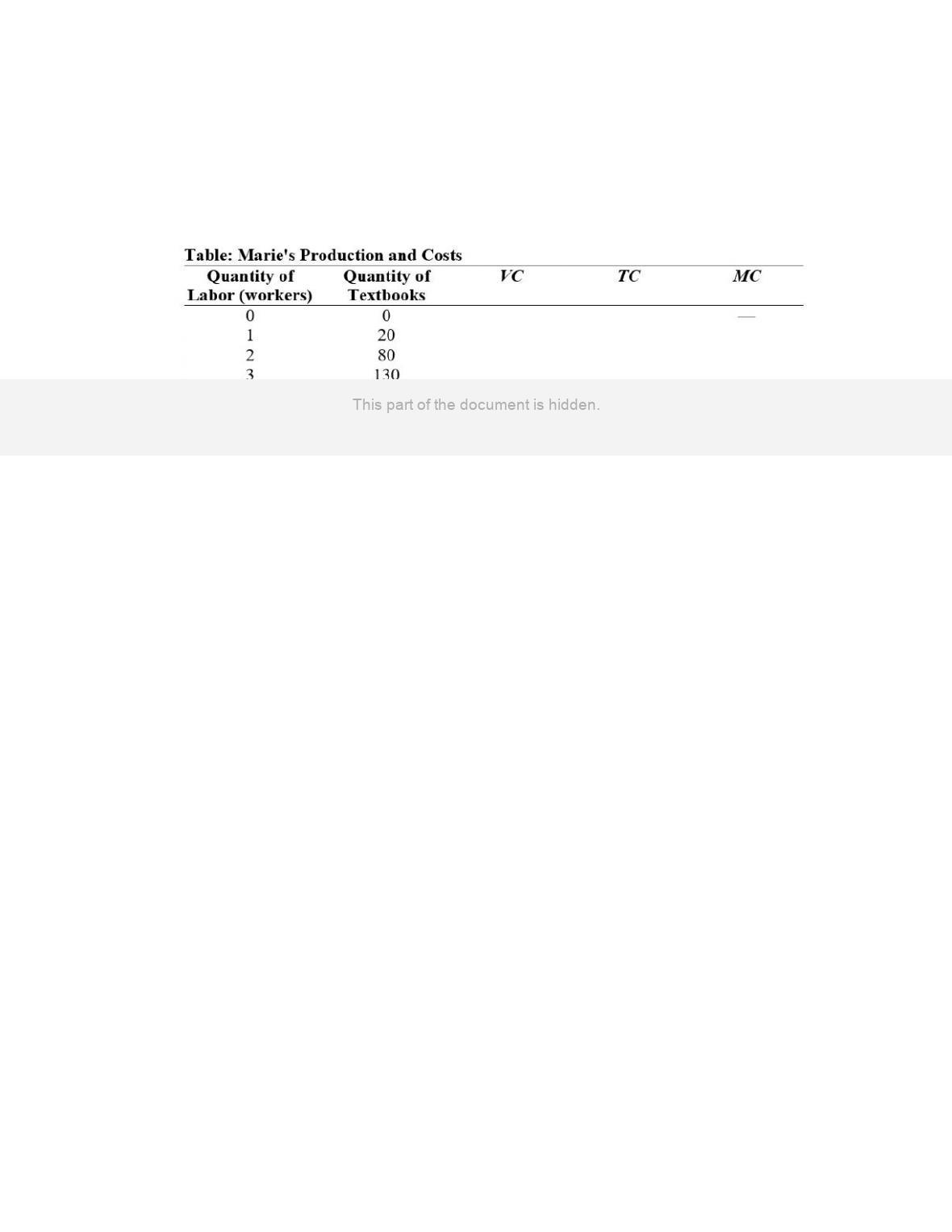

B)

3.

C)

4.

D)

5.

Page 68

292.

(Table: Costs of Birthday Cakes) Use Table: Costs of Birthday Cakes. Assume that

fixed costs are $10. The minimum average total cost occurs at output of:

A)

6.

B)

5.

C)

3.

D)

2.

293.

Farmers in the United States grow about three times as much wheat per acre as do

farmers in Western Europe.

A)

True

B)

False

294.

Scott operates a business that takes people on boat tours in Crystal River, Florida. The

amount of fuel Scott uses each day is a variable input.

A)

True

B)

False

295.

In the long run, every input available to a manufacturer is a fixed input.

A)

True

B)

False

296.

Joan adds one more employee to her construction company. The additional output

produced by this employee represents the average product of this employee.

A)

True

B)

False

297.

The total product curve for the Wallmark Greeting Card Company shows how the

quantity of output depends on the quantity of the variable input for a given amount of

the fixed inputs.

A)

True

B)

False

298.

The slope of the total product curve is equal to the average product of labor.

A)

True

B)

False

Page 69

299.

As more labor is added to a fixed amount of capital, eventually the marginal product of

labor decreases.

A)

True

B)

False

300.

When returns are diminishing, the marginal cost curve is upward-sloping.

A)

True

B)

False

301.

As a firm increases production in the short run, the marginal cost of output increases

because the marginal product of the variable input decreases.

A)

True

B)

False

302.

The short-run average total cost curve is U-shaped because at low output levels the

spreading effect of falling average fixed costs dominates the diminishing returns effect,

while at high output levels the reverse is true.

A)

True

B)

False

303.

In the short run, and with nonzero fixed costs, the average total cost curve always lies

above the average variable cost curve.

A)

True

B)

False

304.

If the average total cost curve and the average variable cost curve are both U-shaped,

and fixed costs are nonzero, then the minimum point of the average total cost curve

must lie above the minimum point of the average variable cost curve.

A)

True

B)

False

305.

If average total cost is declining, marginal cost cannot be increasing.

A)

True

B)

False

Page 70

306.

In the short run, if marginal cost is higher than average total cost, producing an extra

unit of output must raise average total cost.

A)

True

B)

False

307.

In the short run, the average total cost curve reaches its minimum point at a lower level

of output than the short-run marginal cost curve reaches its minimum.

A)

True

B)

False

308.

In some complex production processes, such as nuclear power plants, some inputs have

to be treated as being fixed even in the long run.

A)

True

B)

False

309.

In the long run, some of a firm’s costs are fixed, while others are variable.

A)

True

B)

False

310.

Firms choose their level of fixed cost in the long run based on the amount of output that

they expect to produce.

A)

True

B)

False

311.

When a firm adds physical capital, its fixed cost will decrease in the short run.

A)

True

B)

False

312.

When a firm adds physical capital, labor will become more productive in the short run.

A)

True

B)

False

313.

When a firm adds physical capital, its variable cost will decrease in the long run.

A)

True

B)

False

Page 71

314.

The long run is the period during which fixed costs do not change.

A)

True

B)

False

315.

In the long run, when a firm adds physical capital, workers become more productive, so

variable costs increase.

A)

True

B)

False

316.

The long-run average total cost curve shows the relationship between output and the

average total cost when fixed cost has been chosen to minimize average total cost for

each level of output.

A)

True

B)

False

317.

The long-run average total cost curve shows the relationship between output and the

average total cost when variable cost has been chosen to minimize average total cost for

each level of output.

A)

True

B)

False

318.

A firm always operates at some point on its long-run average total cost curve in both the

long run and the short run.

A)

True

B)

False

319.

If output increases, a firm will move along its short-run average total cost curve in the

short run until it has time to adjust its fixed cost.

A)

True

B)

False

320.

The long-run average cost curve is tangent to a series of short-run average fixed cost

curves.

A)

True

B)

False

Page 72

321.

The long-run average cost curve is tangent to a series of short-run average total cost

curves.

A)

True

B)

False

322.

If a firm has to increase output suddenly to meet an increase in demand, its average total

cost will increase in the short run until it has time to add physical capital.

A)

True

B)

False

323.

If a firm has to increase output suddenly to meet an increase in demand, its average total

cost will decrease in the short run until it has time to add physical capital.

A)

True

B)

False

324.

When a firm has to increase its output, average total costs will increase in the short run

and then decrease in the long run, after the firm has time to add physical capital.

A)

True

B)

False

325.

When a firm has to increase its output, average total costs will decrease in the short run

and then increase in the long run after the firm has time to add physical capital.

A)

True

B)

False

326.

Scale is the size of a firm’s operations.

A)

True

B)

False

327.

When the long-run average total cost curve is downward-sloping as output increases, the

firm has diseconomies of scale.

A)

True

B)

False

328.

When long-run average total cost is constant as output increases, the firm has constant

returns to scale.

A)

True

B)

False

Page 73

329.

When the long-run average total cost curve is upward sloping as output increases, the

firm has diseconomies of scale.

A)

True

B)

False

330.

Economies of scale are often the result of increased specialization, which can occur

when output levels increase.

A)

True

B)

False

331.

Economies of scale most often occur in industries whose initial fixed cost of plant and

equipment is low.

A)

True

B)

False

332.

A production function that is characterized by economies of scale will not be subject to

diminishing returns.

A)

True

B)

False

333.

Diminishing returns are one explanation for diseconomies of scale.

A)

True

B)

False

334.

If a firm builds a larger plant and increases output and if its long-run average total cost

does not change, the firm has constant returns to scale.

A)

True

B)

False

335.

The advantage of specialization in production is one of the primary reasons for

decreasing returns to scale.

A)

True

B)

False

336.

In the short run, why is it believed that the total product curve increases at a decreasing

rate when more labor is added to the production function?

Page 74

337.

Some people say, “There are too many cooks in the kitchen,” to describe any chaotic

scene where nothing gets done. Relate this phrase to short-run production functions.

338.

Suppose a short-run production function always increases at a constant rate of three

units of output for every additional worker added. What does this imply about the

marginal product of labor? Is this realistic? Explain.

339.

It is time to pay the bills. You pay the rent, the basic cable bill, the electricity bill, and

your grocery bill. Which of these are good examples of fixed costs, and which are

variable costs? Explain your reasoning.

340.

(Table: Marie’s Textbook Company) Use Table: Marie’s Textbook Company. Marie has

fixed costs of $500 per month and hires workers for $2,000 each per month. With as

much precision as possible, calculate the following:

A) total cost of production when four workers are employed

B) the output level that produces the lowest average total cost

C) the price that Marie must charge to break even on the production of 130

textbooks

341.

Describe the shape of the AFC curve when fixed costs are nonzero and explain why it

takes this shape. Can AFC ever intersect the x-axis in such cases?

342.

Consider the statement, “When the marginal cost is rising, the average total cost must

also be rising.” Is this statement true or false? Explain your reasoning.

343.

A firm employs capital as a fixed input and labor as a variable input in the short run. If

the cost of capital falls, what will happen to the AVC, ATC, and MC curves? Explain.

Page 75

344.

(Table: Cakes) Use Table: Cakes. Pat is opening a bakery to make and sell special

birthday cakes. Her estimated fixed and average variable costs if she purchases 1, 2, or 3

mixers are shown in the table. Assume that average variable costs do not vary with the

quantity of output. Suppose that Pat is producing 100 cakes with 1 mixer, but she has a

sudden increase in demand, so she begins to produce 200 cakes. Explain how her

average total cost will change in the short run and in the long run.

345.

(Table: Cakes) Use Table: Cakes. Pat is opening a bakery to make and sell special

birthday cakes. Her estimated fixed and average variable costs if she purchases 1, 2, or 3

mixers are shown in the table. Assume that average variable costs do not vary with the

quantity of output. Suppose that Pat is producing 200 cakes with two mixers, but she has

a sudden increase in demand, so she begins to produce 400 cakes. Explain how her

average total cost will change in the short run and in the long run.

346.

What are some factors that contribute to a firm achieving increasing returns to scale (or

economies of scale) in the long run?

Page 76

347.

(Table: Marie’s Production and Costs) Use Table: Marie’s Production and Costs. Marie

has fixed costs of $500 per month and hires workers for $2,000 each per month. Some

of Marie’s monthly production and cost information is in the accompanying table.

Calculate the missing information and complete the table.

348.

The production function provides information about:

A)

a firm’s profit level.

B)

the transformation of inputs into output.

C)

the location of the firm’s production.

D)

a firm’s market structure.

349.

The level of inputs a firm employs will determine a firm’s:

A)

ability to produce output.

B)

elasticity of demand.

C)

stock price.

D)

location of production.

Page 77

350.

(Table: Tonya’s Production Function for Apples) Use Table: Tonya’s Production

Function for Apples. Tonya is operating:

A)

in the long run.

B)

in the short run.

C)

in a very expensive location.

D)

at a loss.

351.

(Table: Tonya’s Production Function for Apples) Use Table: Tonya’s Production

Function for Apples. In the short run, Tonya’s fixed input(s) is/are:

A)

land.

B)

labor.

C)

land and labor.

D)

neither land nor labor.