Page 1

Name: __________________________ Date: _____________

1.

A _____ is an organization that produces goods or services for sale.

A)

production function

B)

firm

C)

variable input

D)

fixed input

2.

In the short run:

A)

all inputs are fixed.

B)

all inputs are variable.

C)

some inputs are fixed and some inputs are variable.

D)

all costs are variable.

3.

The _____ is the increase in output that is produced when a firm hires an additional

worker.

A)

average product

B)

total product

C)

marginal product

D)

marginal cost

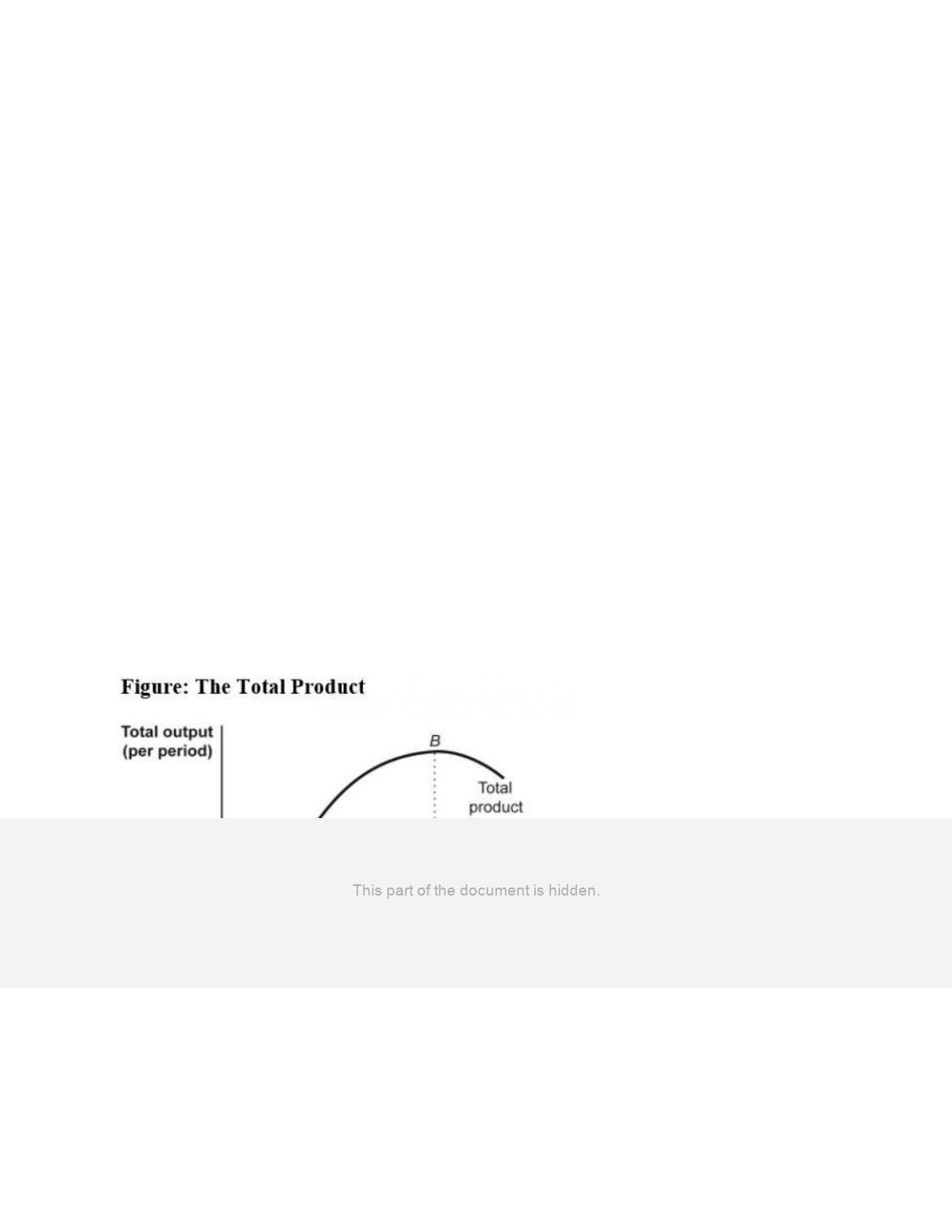

4.

Lauren has 11 people working in her tangerine grove. The marginal product of the

eleventh worker is 13 bushels of tangerines. If she hires a twelfth worker, the marginal

product of that worker will be _____ bushels.

A)

14

B)

15

C)

12

D)

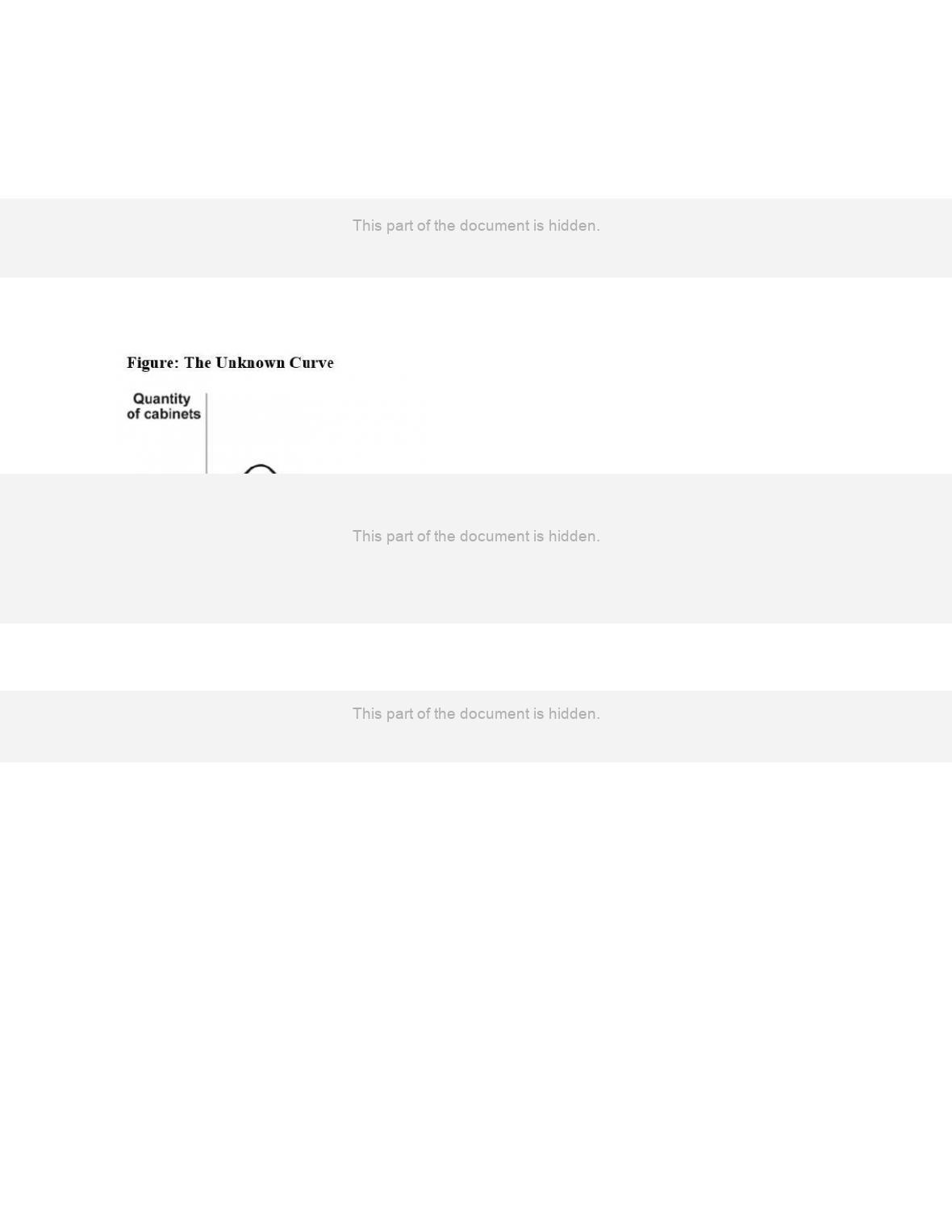

The answer cannot be determined with the information available.

5.

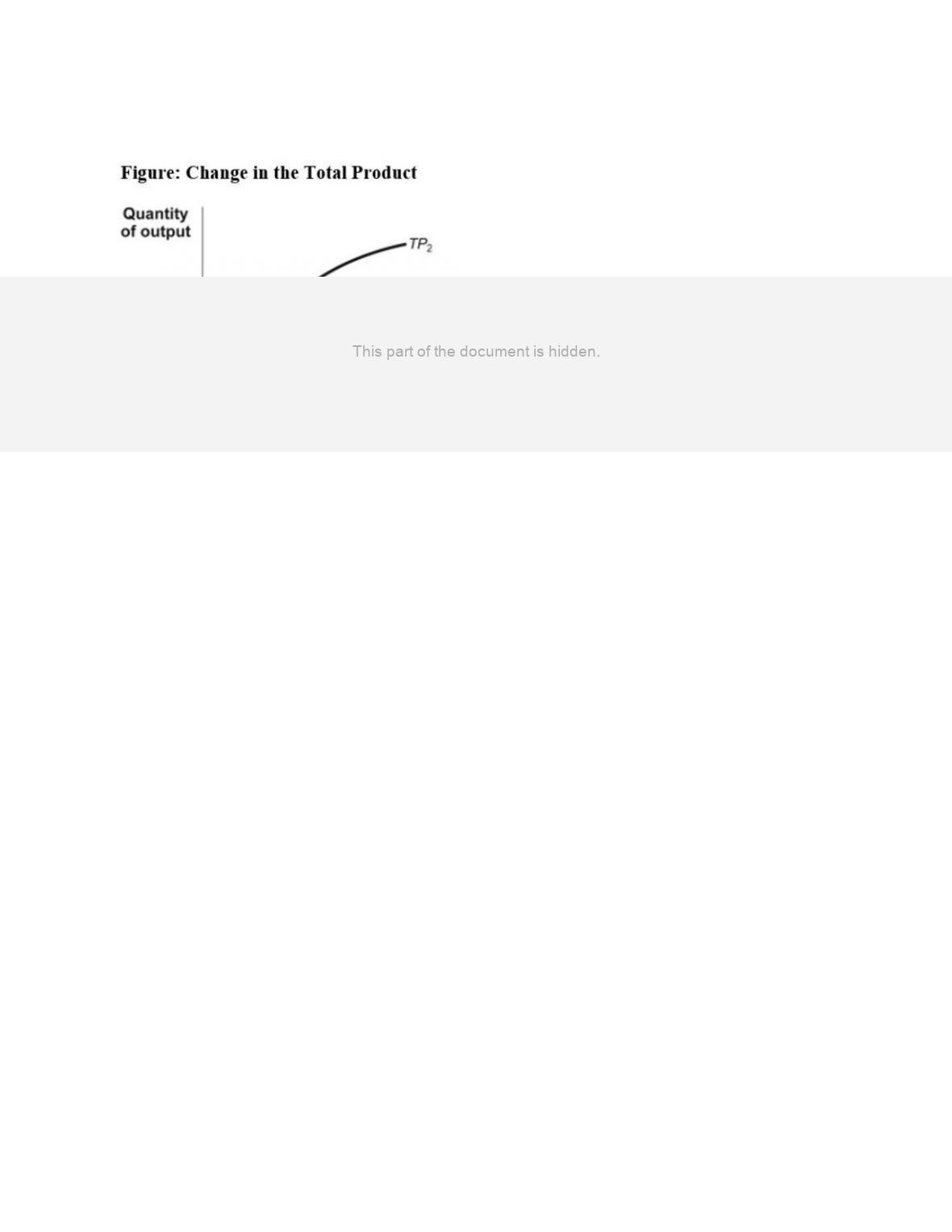

The total product curve:

A)

shows the relation between output and the quantity of a variable input for varying

levels of the fixed input.

B)

will become flatter as output increases if there are diminishing returns to the

variable input.

C)

will be downward sloping if there are diminishing returns to the variable input.

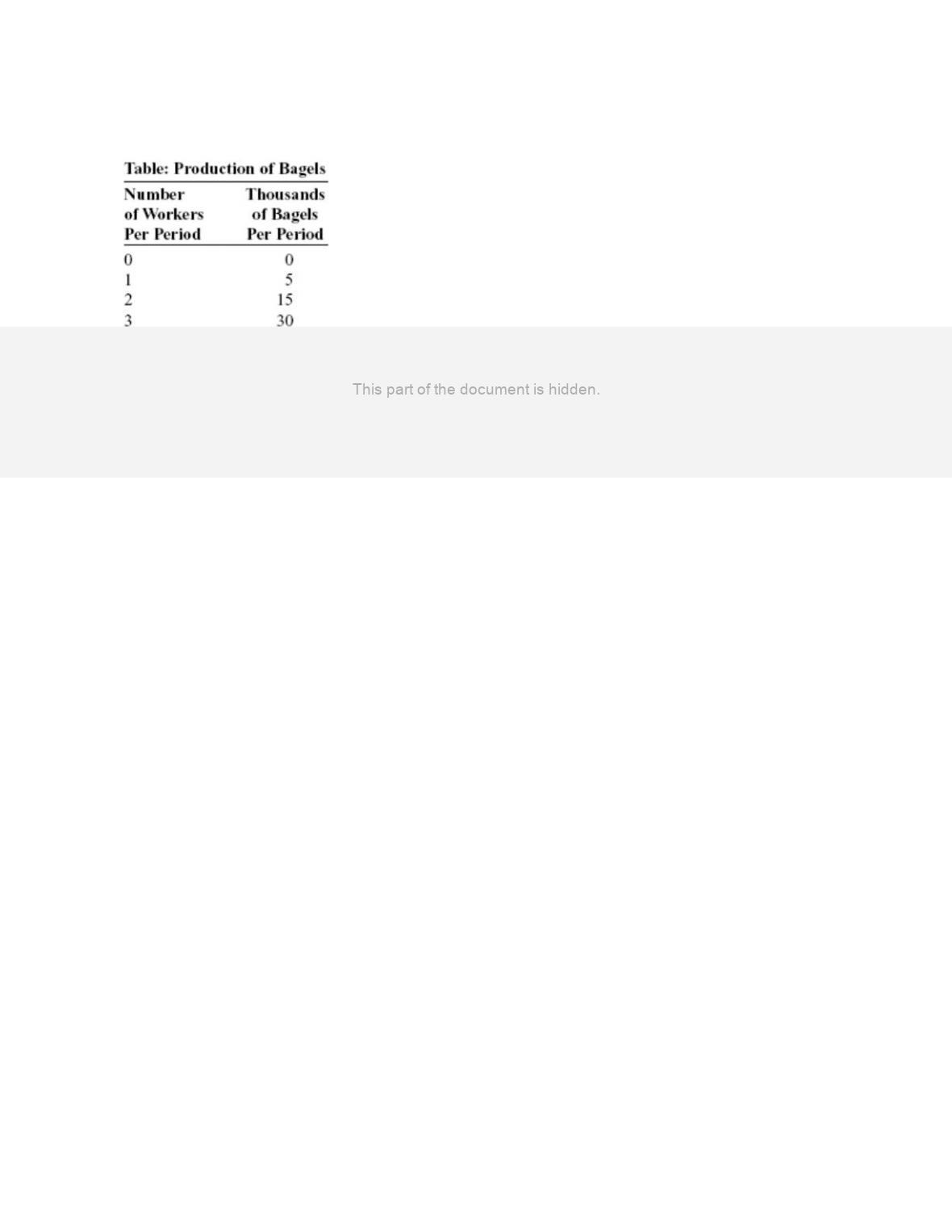

D)

will become horizontal when the marginal product of the variable input is constant.

Page 2

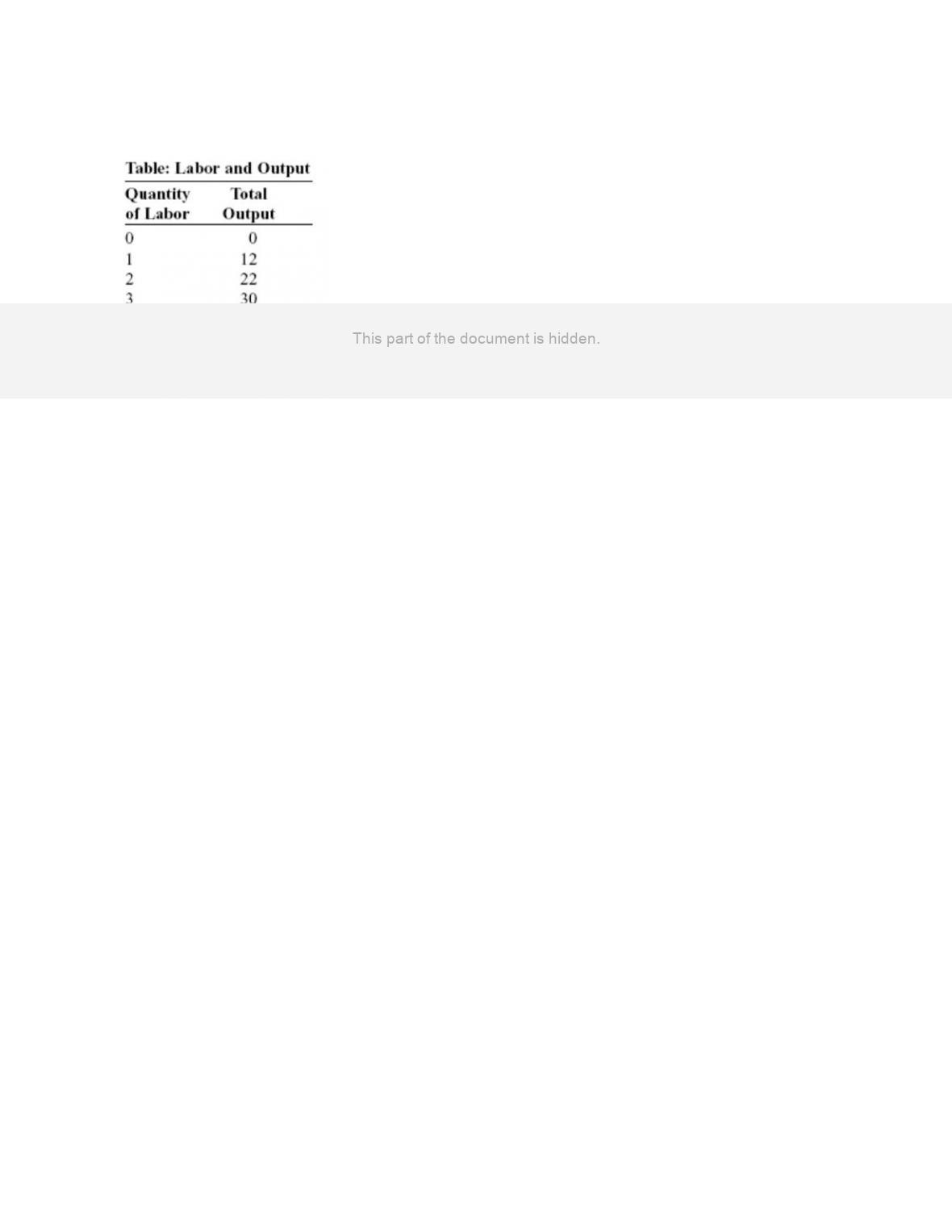

Use the following to answer questions 6-7:

6.

(Table: Labor and Output) Use Table: Labor and Output. The marginal product of the

fifth worker is:

A)

8.

B)

4.

C)

3.

D)

40.

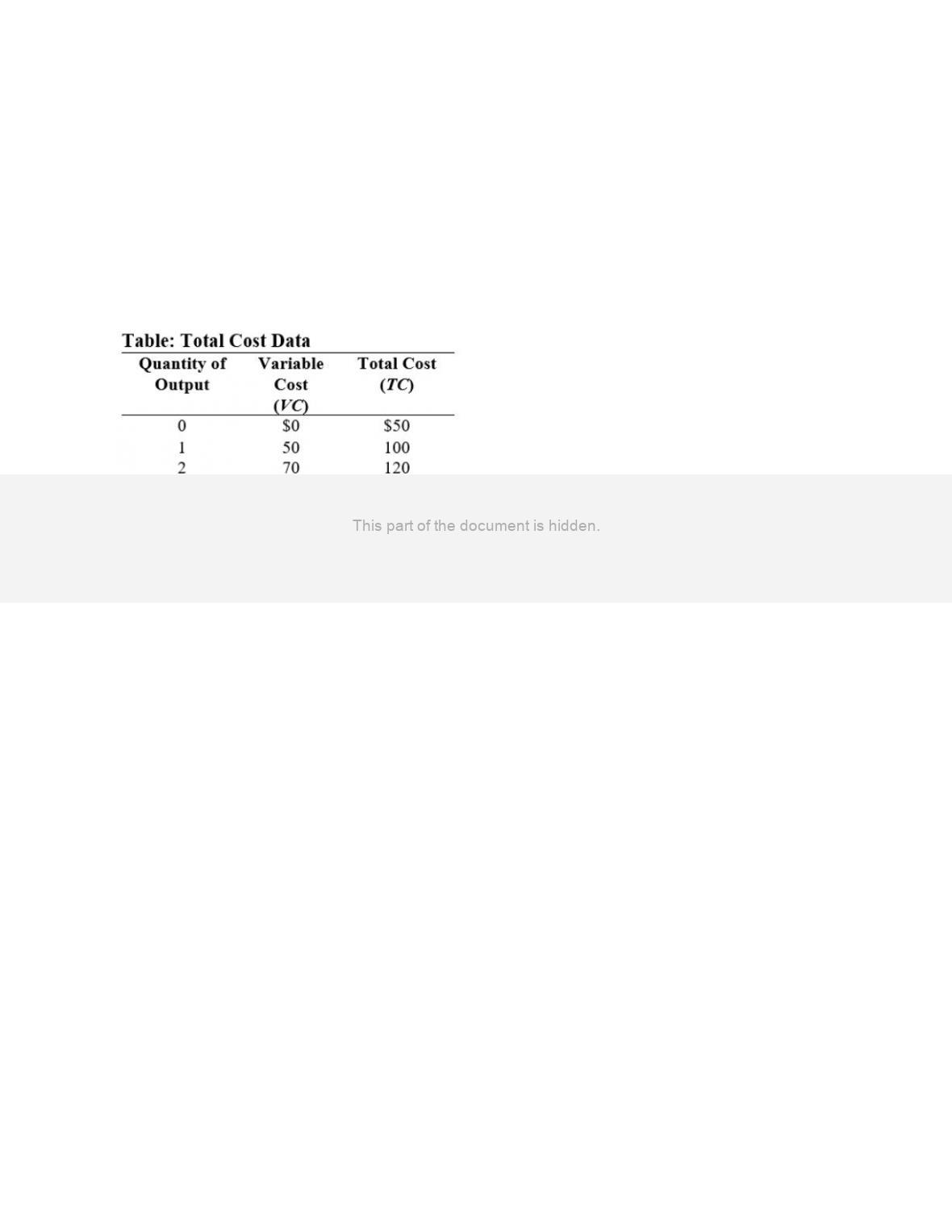

7.

(Table: Labor and Output) Use Table: Labor and Output. The marginal product of the

fourth worker is:

A)

9.

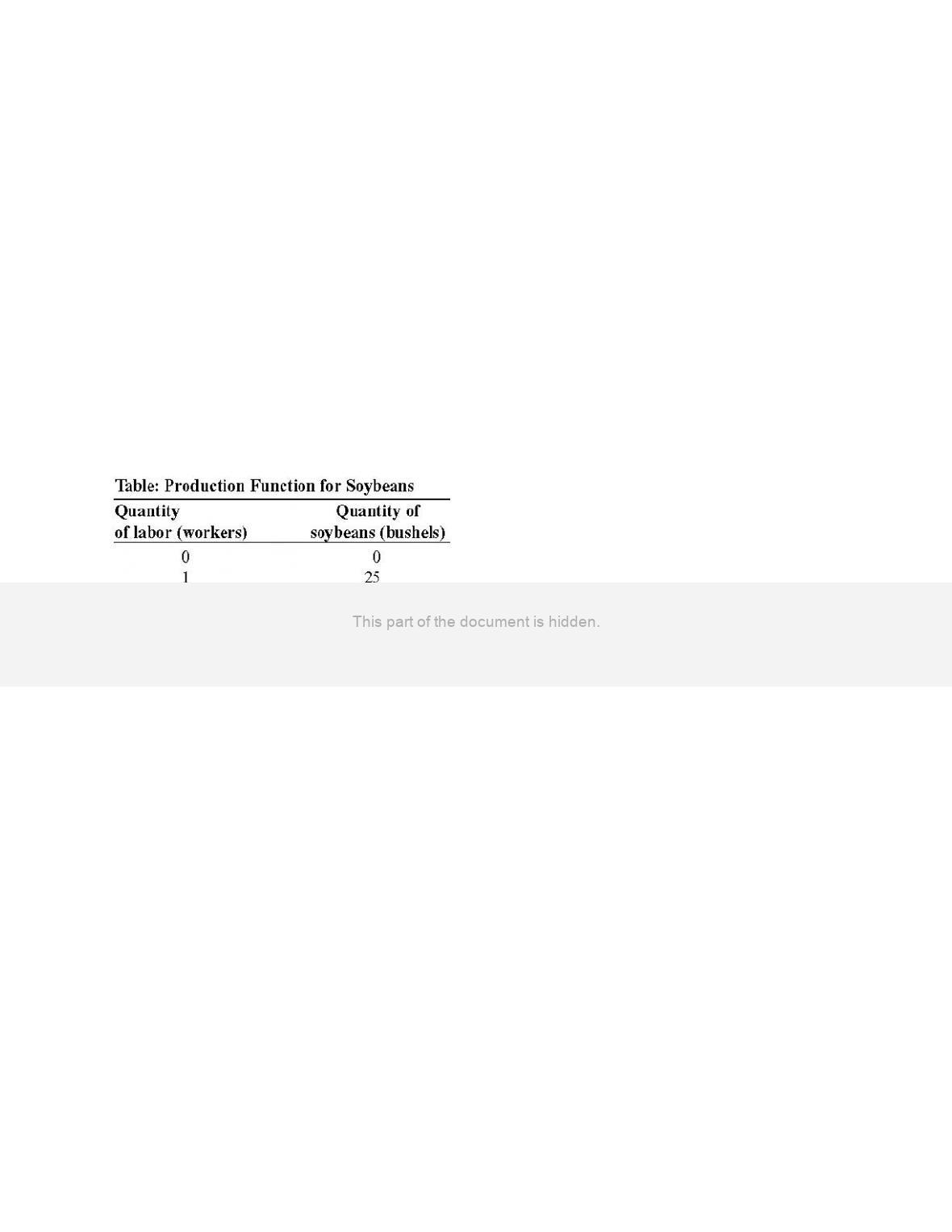

B)

36.

C)

10.

D)

6.

8.

The term diminishing returns refers to a:

A)

falling interest rate that can be expected as one’s investment in a single asset

increases.

B)

reduction in profits caused by increasing output beyond the optimal point.

C)

decrease in total output due to the firm hiring uneducated workers.

D)

decrease in the extra output due to the use of an additional unit of a variable input

when all other inputs are held constant.

Page 3

9.

The idea of diminishing returns to an input in production suggests that, if a local college

adds more custodians, the marginal product of labor for the custodial staff will:

A)

increase at an increasing rate.

B)

increase at a decreasing rate.

C)

decrease.

D)

not change.

10.

Diminishing returns to an input occur:

A)

when all inputs are fixed.

B)

when some inputs are fixed and some are variable.

C)

when all inputs are variable.

D)

only when there are no fixed inputs.

11.

If two firms are identical in all respects except that one has more of the fixed input

capital than another, the total product curve for the firm with more capital:

A)

must equal the total product curve for the firm with less capital.

B)

will lie above the total product curve for the firm with less capital.

C)

will lie below the total product curve for the firm with less capital.

D)

will show no diminishing marginal returns.

12.

If two firms are identical in all respects except that one has more of the fixed input

capital than another, the marginal product curve for the firm with more capital:

A)

must equal the marginal product curve for the firm with less capital.

B)

will lie above the marginal product curve for the firm with less capital.

C)

will lie below the total marginal curve for the firm with less capital.

D)

will show no diminishing marginal returns.

Page 4

Use the following to answer questions 13-15:

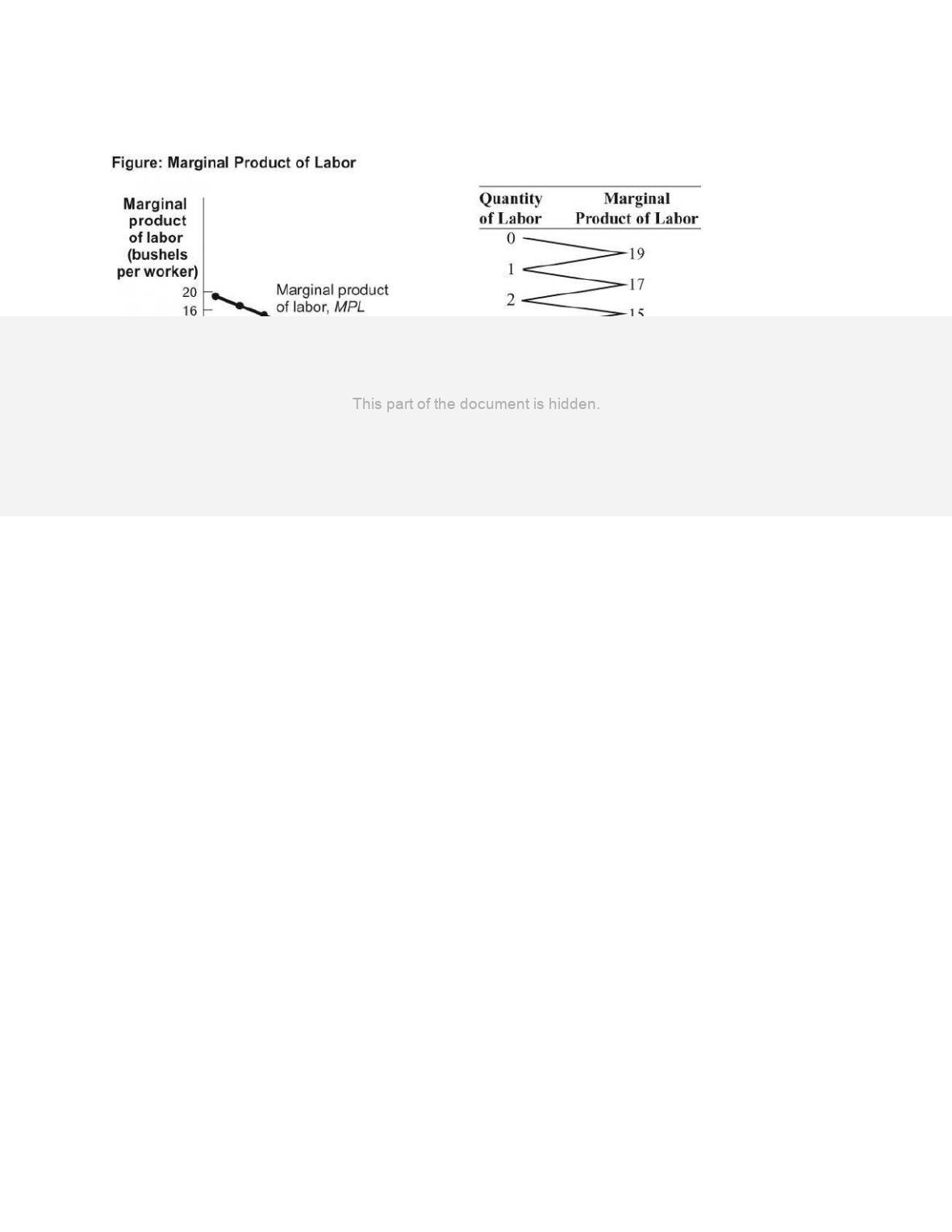

13.

(Figure: Marginal Product of Labor) Use Figure: The Marginal Product of Labor. The

total product for three workers is _____ bushels.

A)

51

B)

45

C)

39

D)

15

14.

(Figure: Marginal Product of Labor) Use Figure: The Marginal Product of Labor. The

total product of labor for five workers is _____ bushels.

A)

11

B)

45

C)

55

D)

75

15.

(Figure: Marginal Product of Labor) Use Figure: The Marginal Product of Labor. The

total product of labor for eight workers is _____ bushels.

A)

40

B)

35

C)

96

D)

75

Page 5

16.

In economics, the short run is defined as:

A)

less than 1 year.

B)

less than 6 months.

C)

the period in which some inputs are considered to be fixed in quantity.

D)

the period in which some inputs are fixed, but it cannot exceed 1 year.

17.

In economics, the short run is:

A)

less than 1 week.

B)

less than 1 month.

C)

enough time to vary output but not plant capacity.

D)

enough time to change all inputs to production.

18.

An input whose quantity can be changed in the short run is a(n) _____ input.

A)

marginal

B)

fixed

C)

incremental

D)

variable

19.

An input whose quantity CANNOT be changed in the short run is:

A)

marginal.

B)

fixed.

C)

incremental.

D)

variable.

20.

A fixed input is one:

A)

that only exists in nature, and there is only so much of it.

B)

that can be used for one thing only.

C)

that can never produce more or less in any period.

D)

whose quantity cannot be changed in the short run.

21.

The long run is a planning period:

A)

over which a firm can consider all inputs as variable.

B)

of at least five years.

C)

of more than six months.

D)

of six months to five years.

Page 6

22.

In the long run:

A)

all inputs are fixed.

B)

inputs are neither variable nor fixed.

C)

at least one input is variable and one input is fixed.

D)

all inputs are variable.

23.

The _____ curve shows the absolute quantities of output that can be obtained from

different quantities of a variable input, assuming other inputs are fixed.

A)

total input

B)

marginal input

C)

total product

D)

average total quantity

24.

A total product curve indicates the relationship between _____ when all other inputs are

fixed.

A)

a variable input and price

B)

a variable input and variable cost

C)

a variable input and output

D)

output and price

25.

The marginal product of labor is the:

A)

change in labor divided by the change in total product.

B)

slope of the total product of labor curve.

C)

change in average product divided by the change in the quantity of labor.

D)

change in output that occurs when capital increases by one unit.

26.

A farm can produce 1,000 bushels of wheat per year with two workers and 1,300

bushels of wheat per year with three workers. The marginal product of the third worker

is _____ bushels.

A)

100

B)

300

C)

1,300

D)

2,300

Page 7

27.

When Caroline’s dress factory hires two workers, the total product is 50 dresses. When

she hires three workers, total product is 60, and when she hires four workers, total

product is 65. The slope of the marginal product curve between two and four workers

hired is:

A)

positive.

B)

zero.

C)

infinite.

D)

negative.

28.

When Caroline’s dress factory hires two workers, the total product is 50 dresses. When

she hires three workers, total product is 60, and when she hires four workers, total

product is 75. The slope of the marginal product curve between two and four workers

hired is:

A)

positive.

B)

negative.

C)

infinite.

D)

zero.

29.

When Caroline’s dress factory hires two workers, the total product is 50 dresses. When

she hires three workers, total product is 48, and when she hires four workers, total

product is 45. The marginal product of the third and fourth workers is:

A)

increasing and positive.

B)

increasing and negative.

C)

decreasing and positive.

D)

decreasing and negative.

Use the following to answer questions 30-32:

Page 8

30.

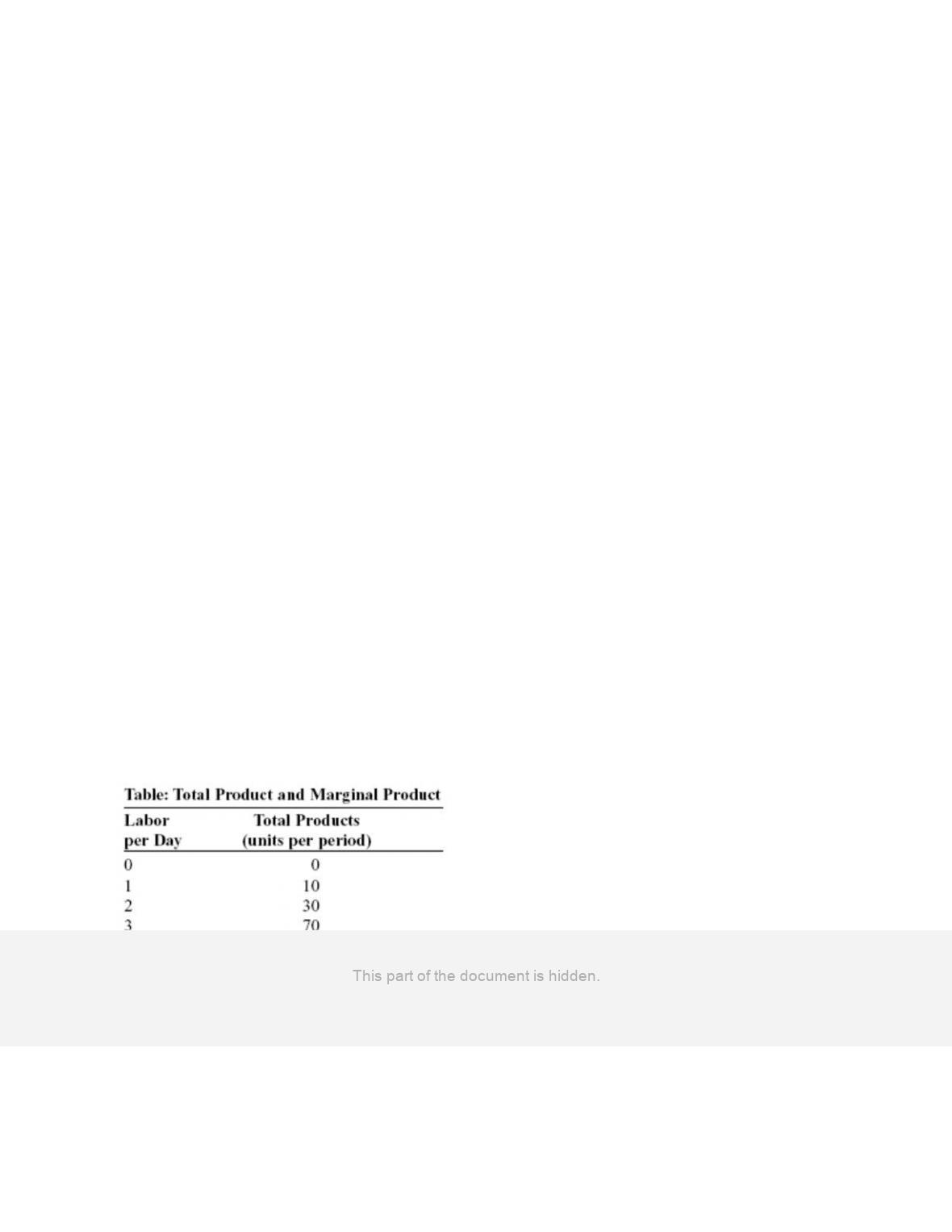

(Table: Total Product and Marginal Product) Use Table: Total Product and Marginal

Product. The marginal product of the second worker is _____ units per period.

A)

10

B)

15

C)

20

D)

30

31.

(Table: Total Product and Marginal Product) Use Table: Total Product and Marginal

Product. The marginal product of the fourth worker is _____ units per period.

A)

20

B)

22.5

C)

50

D)

90

32.

(Table: Total Product and Marginal Product) Use Table: Total Product and Marginal

Product. Negative marginal returns begin when the _____ worker is added.

A)

fifth

B)

sixth

C)

seventh

D)

eighth

Use the following to answer questions 33-39:

Page 9

33.

(Figure: The Total Product) Use Figure: The Total Product. Between points A and B the

marginal product of labor is:

A)

increasing.

B)

zero.

C)

decreasing.

D)

infinite.

34.

(Figure: The Total Product) Use Figure: The Total Product. Labor added from L1 and up

to L2 is:

A)

subject to diminishing marginal returns.

B)

adding to total product at an increasing rate.

C)

adding nothing to total product.

D)

adding to total product at a constant rate.

35.

(Figure: The Total Product) Use Figure: The Total Product. As labor is hired between L1

and L2, the total product is _____ and the marginal product is _____.

A)

increasing; positive

B)

decreasing; zero

C)

increasing; negative

D)

increasing; zero

36.

(Figure: The Total Product) Use Figure: The Total Product. For hiring labor between

zero and L1, the:

A)

marginal product of labor is increasing.

B)

marginal product of labor is decreasing.

C)

total product is increasing at a diminishing rate.

D)

total product is decreasing.

37.

(Figure: The Total Product) Use Figure: The Total Product. After hiring L2 labor and

producing at point B on the total product curve, hiring more labor beyond L2 would

cause the:

A)

marginal product of labor to rise.

B)

marginal product of labor to be negative.

C)

total product to be negative.

D)

total product to be zero.

Page 10

38.

(Figure: The Total Product) Use Figure: The Total Product. When L2 labor is hired, the

total product is at a _____ and the marginal product of labor is _____.

A)

minimum; zero

B)

maximum; zero

C)

maximum; positive

D)

minimum; positive but falling

39.

(Figure: The Total Product) Use Figure: The Total Product. If the firm hires more than

L2 labor, the total product will _____ because the marginal product of labor is _____.

A)

decrease; positive

B)

increase; positive

C)

decrease; negative

D)

increase; negative

40.

When an additional unit of a variable input adds less to total product than the previous

unit, the firm has:

A)

increasing returns.

B)

diminishing marginal returns.

C)

diminishing total returns.

D)

diminishing marginal returns and diminishing total returns.

41.

Diminishing marginal returns occur when:

A)

each additional unit of a variable factor adds more to total output than the previous

unit.

B)

each additional unit of a variable factor adds less to total output than the previous

unit.

C)

the marginal product of a variable factor is increasing at a decreasing rate.

D)

total product decreases.

42.

You own a deli. Which input of production is MOST likely fixed at your deli?

A)

the dining room

B)

the bread used to make sandwiches

C)

the tomato sauce used to make soups

D)

the employees

Page 11

43.

You own a deli. Which decision is most likely to be made in the LONG run at your

deli?

A)

You order more breadsticks.

B)

You order more soft drinks for next week.

C)

You renovate the second floor of your building to increase the size of the dining

room.

D)

You advertise for part-time workers.

Use the following to answer question 44:

44.

(Figure: The Unknown Curve) Use Figure: The Unknown Curve. You are a

cabinetmaker. You employ several workers to produce kitchen and bathroom cabinets.

Your summer intern has drawn a graph showing a relationship between the number of

cabinetmakers you employ and the number of cabinets produced. Unfortunately, your

intern has failed to identify this curve. It is likely to be the _____ curve.

A)

total cost

B)

total product

C)

marginal product

D)

total variable cost

Page 12

Use the following to answer question 45:

45. (Table: Production of Cabinets) Use Table: The Production of Cabinets. After the _____

worker, the firm begins to have diminishing returns to labor.

A) first

B) second

C) third

D) seventh

Ans: B

Refer To: Ref 11-6 Table: Production of Cabinets

bloomslevel: Applying

45.

(Table: Production of Cabinets) Use Table: The Production of Cabinets. If each

cabinetmaker could be hired at no cost, how many workers would your firm employ?

A)

two

B)

six

C)

seven

D)

eight

Page 13

Use the following to answer questions 46-47:

46.

(Figure: Change in the Total Product) Use Figure: Change in the Total Product. Which

choice is a likely cause of the shift in production function from TP1 to TP2?

A)

Workers in the firm are less productive on average.

B)

The firm employed more of a variable input in the short run.

C)

Available technology has decreased.

D)

The firm employed more of a fixed input in the long run.

47.

(Figure: Change in the Total Product) Use Figure: Change in the Total Product. As

indicated by the change in a production function from TP1 to TP2, the marginal product

of labor curve has:

A)

shifted upward.

B)

shifted downward.

C)

not moved.

D)

become inverted.

48.

A factor of production whose quantity can be changed in the SHORT run is a(n) _____

factor of production.

A)

marginal

B)

fixed

C)

incremental

D)

variable

Page 14

49.

A factor of production whose quantity CANNOT be changed in the short run is a(n)

_____ factor of production.

A)

marginal

B)

fixed

C)

incremental

D)

variable

50.

Think about running a restaurant. It is likely the case that:

A)

cooks and hosts are variable resources.

B)

a building is a variable resource in the short run.

C)

cheese and other wholesale food items are fixed resources in the short run.

D)

valet parking staff are a fixed resource in the long run.

51.

As defined in the text, the long run is a planning period:

A)

in which a firm can adjust all resources.

B)

that is at least five years long.

C)

during which the firm must increase sales to stay in business.

D)

in which variable resources become fixed.

52.

A planning period during which all of a firm’s resources are variable is the _____ run.

A)

long

B)

fixed

C)

short

D)

nominal

53.

In the long run:

A)

the firm has time to change the level of all inputs.

B)

inputs are neither variable nor fixed.

C)

at least one input is free.

D)

all inputs are more expensive.

54.

The long run is:

A)

long enough to vary the quantities of all factors of production.

B)

long enough to vary all factors of production except for the amount of capital

available.

C)

more than one month.

D)

at least one year.

Page 15

Use the following to answer questions 55-57:

55.

(Table: Production of Bagels) Use Table: Production of Bagels. The marginal product of

the third worker is _____ bagels.

A)

9,000

B)

10,000

C)

12,000

D)

15,000

56.

(Table: Production of Bagels) Use Table: Production of Bagels. The marginal product of

the fifth worker is _____ bagels.

A)

5,000

B)

9,000

C)

10,000

D)

12,000

57.

(Table: Production of Bagels) Use Table: Production of Bagels. Diminishing marginal

returns begin with the addition of the _____ worker.

A)

third

B)

fourth

C)

fifth

D)

sixth

Page 16

58.

“Diminishing marginal returns” means that:

A)

each additional unit of an input will decrease output.

B)

each additional unit of an input will increase output, but by smaller and smaller

amounts as inputs increase.

C)

each additional unit of an input will increase output, but by larger and larger

amounts as inputs increase.

D)

the firm is maximizing profit.

59.

Assuming that all other factors of production are held constant, marginal product is the

change in _____ output resulting from a one-unit change in _____.

A)

total; a variable input

B)

total; a fixed input

C)

total; total product

D)

per unit; a fixed input

60.

The marginal product of labor is the change in _____ divided by the change in _____.

A)

labor; total product

B)

total output; the quantity of labor

C)

average output; the quantity of labor

D)

total costs; the quantity of labor

61.

A farm can produce 1,000 bushels of wheat per year with two workers, 1,300 bushels of

wheat per year with three workers, and 1500 bushels of wheat per year with four

workers. The marginal product of the fifth worker is _____ bushels.

A)

250

B)

300

C)

1500

D)

less then 200

62.

The marginal product of labor is NOT:

A)

the change in output resulting from a one-unit change in labor.

B)

the slope of the total product curve.

C)

positive at some levels of input and possibly negative at others.

D)

total product divided by total labor.

Page 17

63.

Suppose that hiring one, two, three, or four workers at a diaper factory generates total

outputs of 200, 350, 450, or 500 diapers, respectively. The marginal product of the

second worker is:

A)

50.

B)

100.

C)

150.

D)

200.

64.

Suppose that when a coal-mining firm hires one, two, three, four, or five workers, the

corresponding total outputs are 10, 15, 19, 22, or 24 tons of coal, respectively. The

marginal product of the third worker is _____ tons of coal.

A)

3

B)

4

C)

15

D)

19

65.

When a firm has diminishing marginal returns:

A)

its output is falling.

B)

marginal product is falling but is likely to still be positive.

C)

total product falls because marginal product is falling and positive.

D)

marginal product is always negative.

66.

The long run refers to the time period when:

A)

a fixed input exists.

B)

all inputs are variable.

C)

marginal costs are decreasing.

D)

diminishing returns raise marginal cost.

67.

In the short run, the costs associated with variable inputs are _____, and the costs

associated with _____ inputs are _____.

A)

variable; fixed; fixed

B)

fixed; fixed; variable

C)

variable; fixed; variable

D)

fixed; fixed; fixed

68.

Which cost concept is CORRECTLY defined?

A)

MC = TC/FC

B)

ATC = VC + FC

C)

ATC = AVC + AFC

D)

TC = AVC + AFC

Page 18

69.

A cost that does NOT depend on the quantity of output produced is:

A)

marginal.

B)

fixed.

C)

variable.

D)

average.

Use the following to answer questions 70-71:

70.

(Table: Total Cost Data) Use Table: Total Cost Data. What is the fixed cost for this

bicycle firm?

A)

$40

B)

$50

C)

$100

D)

$70

71.

(Table: Total Cost Data) Use Table: Total Cost Data. What is the total variable cost for

this bicycle firm when the firm produces 5 bicycles?

A)

$50

B)

$240

C)

$60

D)

$190

72.

The total cost curve for shows how _____ cost depends on the quantity of _____.

A)

total; fixed inputs

B)

average; variable inputs

C)

total; output

D)

marginal; output

Page 19

73.

A fixed cost:

A)

will exist only in the long run.

B)

depends on the level of output.

C)

is positive, even if the firm doesn’t produce any output in the short run.

D)

decreases until the point of diminishing returns is reached.

74.

The sum of fixed and variable costs is _____ cost.

A)

total

B)

marginal

C)

variable

D)

average

Use the following to answer questions 75-83:

75.

(Table: Production Function for Soybeans) Use Table: Production Function for

Soybeans. Assume that the fixed input, capital, is 10 acres of land and a tractor, which

have a combined cost of $150 per day. The cost of labor is $100 per worker per day.

The fixed cost of producing 25 bushels of soybeans is:

A)

$50.

B)

$100.

C)

$150.

D)

$250.

Page 20

76.

(Table: Production Function for Soybeans) Use Table: Production Function for

Soybeans. Assume that the fixed input, capital, is 10 acres of land and a tractor, which

have a combined cost of $150 per day. The cost of labor is $100 per worker per day.

The variable cost of producing 25 bushels of soybeans is:

A)

$50.

B)

$100.

C)

$150.

D)

$250.

77.

(Table: Production Function for Soybeans) Use Table: Production Function for

Soybeans. Assume that the fixed input, capital, is 10 acres of land and a tractor, which

have a combined cost of $150 per day. The cost of labor is $100 per worker per day.

The total cost of producing 25 bushels of soybeans is:

A)

$50.

B)

$100.

C)

$150.

D)

$250.

78.

(Table: Production Function for Soybeans) Use Table: Production Function for

Soybeans. Assume that the fixed input, capital, is 10 acres of land and a tractor, which

have a combined cost of $150 per day. The cost of labor is $100 per worker per day.

The variable cost of producing 45 bushels of soybeans is:

A)

$100.

B)

$200.

C)

$350.

D)

$4,500.

79.

(Table: Production Function for Soybeans) Use Table: Production Function for

Soybeans. Assume that the fixed input, capital, is 10 acres of land and a tractor, which

have a combined cost of $150 per day. The cost of labor is $100 per worker per day.

The total cost of producing 45 bushels of soybeans is:

A)

$100.

B)

$200.

C)

$350.

D)

$4,500.