65) You run a regression for a stock’s return on a market index and find the following Excel

output:

Multiple R

0.35

R-Square

0.12

Adjusted R-Square

0.02

Standard Error

38.45

Observations

12

Coefficients

Standard Error

t-Stat

p-Value

Intercept

4.05

15.44

0.26

0.80

Market

1.32

0.97

1.36

0.10

The characteristic line for this stock is Rstock = ________ + ________ Rmarket.

A) .35; .12

B) 4.05; 1.32

C) 15.44; .97

D) .26; 1.36

66) You run a regression for a stock’s return on a market index and find the following Excel

output:

Multiple R

0.35

R-Square

0.12

Adjusted R-Square

0.02

Standard Error

38.45

Observations

12

Coefficients

Standard Error

t-Stat

p-Value

Intercept

4.05

15.44

0.26

0.80

Market

1.32

0.97

1.36

0.10

________ % of the variance is explained by this regression.

A) 12

B) 35

C) 4.05

D) 80

67) You run a regression for a stock’s return on a market index and find the following Excel

output:

Multiple R

0.35

R-Square

0.12

Adjusted R-Square

0.02

Standard Error

38.45

Observations

12

Coefficients

Standard Error

t-Stat

p-Value

Intercept

4.05

15.44

0.26

0.80

Market

1.32

0.97

1.36

0.10

The stock is ________ riskier than the typical stock.

A) 32%

B) 15.44%

C) 12%

D) 38%

68) Decreasing the number of stocks in a portfolio from 50 to 10 would likely ________.

A) increase the systematic risk of the portfolio

B) increase the unsystematic risk of the portfolio

C) increase the return of the portfolio

D) decrease the variation in returns the investor faces in any one year

69) If you want to know the portfolio standard deviation for a three-stock portfolio, you will

have to ________.

A) calculate two covariances and one trivariance

B) calculate only two covariances

C) calculate three covariances

D) average the variances of the individual stocks

70) Which of the following correlation coefficients will produce the least diversification benefit?

A) -.6

B) -.3

C) 0

D) .8

71) Which of the following correlation coefficients will produce the most diversification

benefits?

A) -.6

B) -.9

C) 0

D) .4

72) What is the most likely correlation coefficient between a stock-index mutual fund and the

S&P 500?

A) -1

B) 0

C) 1

D) .5

73) Investing in two assets with a correlation coefficient of -.5 will reduce what kind of risk?

A) market risk

B) nondiversifiable risk

C) systematic risk

D) unique risk

74) Investing in two assets with a correlation coefficient of 1 will reduce which kind of risk?

A) market risk

B) unique risk

C) unsystematic risk

D) none of these options (With a correlation of 1, no risk will be reduced.)

75) A portfolio of stocks fluctuates when the Treasury yields change. Since this risk cannot be

eliminated through diversification, it is called ________.

A) firm-specific risk

B) systematic risk

C) unique risk

D) none of the options

76) As you lengthen the time horizon of your investment period and decide to invest for multiple

years, you will find that:

I. The average risk per year may be smaller over longer investment horizons.

II. The overall risk of your investment will compound over time.

III. Your overall risk on the investment will fall.

A) I only

B) I and II only

C) III only

D) I, II, and III

77) You are considering adding a new security to your portfolio. To decide whether you should

add the security, you need to know the security’s:

I. Expected return

II. Standard deviation

III. Correlation with your portfolio

A) I only

B) I and II only

C) I and III only

D) I, II, and III

78) Which of the following is a correct expression concerning the formula for the standard

deviation of returns of a two-asset portfolio where the correlation coefficient is positive?

A) σ2rp < (W12σ12 + W22σ22)

B) σ2rp = (W12σ12 + W22σ22)

C) σ2rp = (W12σ12 – W22σ22)

D) σ2rp > (W12σ12 + W22σ22)

79) What is the standard deviation of a portfolio of two stocks given the following data: Stock A

has a standard deviation of 18%. Stock B has a standard deviation of 14%. The portfolio contains

40% of stock A, and the correlation coefficient between the two stocks is -.23.

A) 9.7%

B) 12.2%

C) 14%

D) 15.6%

80) What is the standard deviation of a portfolio of two stocks given the following data: Stock A

has a standard deviation of 30%. Stock B has a standard deviation of 18%. The portfolio contains

60% of stock A, and the correlation coefficient between the two stocks is -1.

A) 0%

B) 10.8%

C) 18%

D) 24%

81) The expected return of a portfolio is 8.9%, and the risk-free rate is 3.5%. If the portfolio

standard deviation is 12%, what is the reward-to-variability ratio of the portfolio?

A) 0

B) .45

C) .74

D) 1.35

82) A project has a 60% chance of doubling your investment in 1 year and a 40% chance of

losing half your money. What is the standard deviation of this investment?

A) 25%

B) 50%

C) 62%

D) 73%

83) A project has a 50% chance of doubling your investment in 1 year and a 50% chance of

losing half your money. What is the expected return on this investment project?

A) 0%

B) 25%

C) 50%

D) 75%

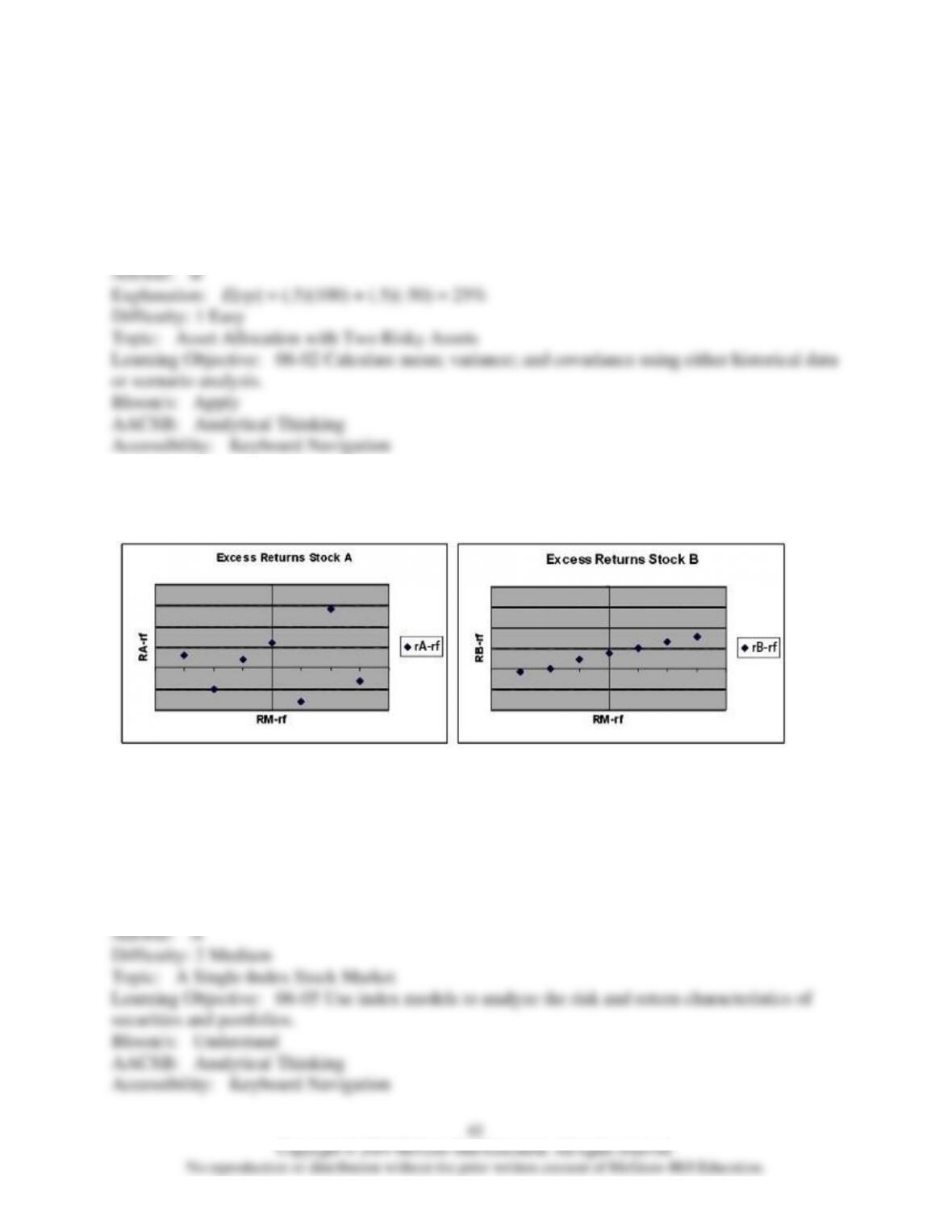

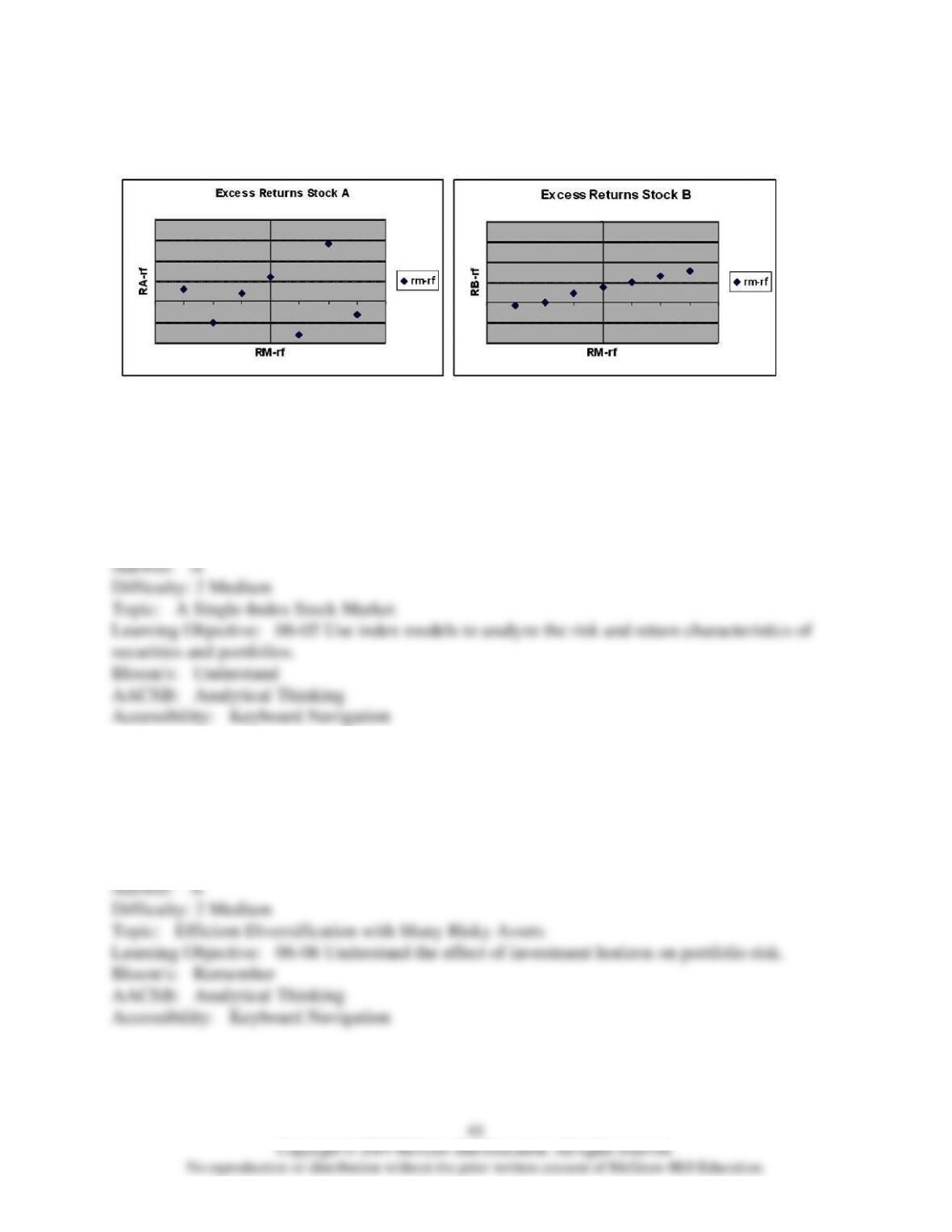

84) The figures below show plots of monthly excess returns for two stocks plotted against excess

returns for a market index.

Which stock is likely to further reduce risk for an investor currently holding her portfolio in a

well-diversified portfolio of common stock?

A) Stock A

B) Stock B

C) There is no difference between A or B.

D) The answer cannot be determined from the information given.

85) The figures below show plots of monthly excess returns for two stocks plotted against excess

returns for a market index.

Which stock is riskier to a nondiversified investor who puts all his money in only one of these

stocks?

A) Stock A is riskier.

B) Stock B is riskier.

C) Both stocks are equally risky.

D) The answer cannot be determined from the information given.

86) The efficient frontier represents a set of portfolios that

A) maximize expected return for a given level of risk.

B) minimize expected return for a given level of risk.

C) maximize risk for a given level of return.

D) None of the options.

87) The portfolio with the lowest standard deviation for any risk premium is called the_______.

A) CAL portfolio

B) efficient frontier portfolio

C) global minimum variance portfolio

D) optimal risky portfolio

88) Lear Corp. has an expected excess return of 8% next year. Assume Lear’s beta is 1.43. If the

economy booms and the stock market beats expectations by 5%, what was Lear’s actual excess

return?

A) 7.15%

B) 13%

C) 15.15%

D) 18.59 %

89) The plot of a security’s excess return relative to the market’s excess return is called the

________.

A) efficient frontier

B) security characteristic line

C) capital allocation line

D) capital market line