Real Estate Finance & Investments, 16e (Brueggeman)

Chapter 22 Real Estate Investment Performance and Portfolio Considerations

1) It is difficult to compare the investment performance of real estate with stocks and bonds

because when investment properties do sell, the sale price is generally not publicly available.

2) The NCREIF index measures the investment performance of real estate by using actual sale

prices.

3) Much like the securities markets, there is a large, centralized collection of real estate

transactions and operating income data.

4) The NCREIF Property Index includes property value increases or decreases only when

properties are sold since the sale price is the only true measure of market value.

5) Both levered and unlevered properties are included in the NCREIF Property Index.

6) An investor in a mortgage REIT is basically buying equity shares of an entity whose assets are

mainly mortgages.

7) When used to evaluate the performance of an investment, the geometric mean is considered to

be superior to the arithmetic mean.

8) When comparing investment alternatives, the standard deviation is deemed to be a measure of

risk.

9) The optimal portfolio is obtained by combining a group of securities which, by themselves,

offer the highest returns with the lowest risk.

11) If two securities have the same positive mean returns and they are perfectly, negatively

correlated, an investor in such securities will earn a positive return with zero risk.

12) In comparison to investment portfolios comprised entirely of corporate stocks and bonds,

portfolios which include some form of real estate investment tend to offer higher returns for each

level of risk.

13) The sources of data for real estate performance evaluation are security prices for REIT shares

and the value of individual properties that are owned by pension plan sponsors.

14) The holding period return and geometric mean return calculations will yield the same result

for holding periods longer than two years.

4

Copyright 2019 © McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

15) Consider an investment held over three years with a return of +20 percent in the first

year, −25 percent in the second year, and +20 percent in the third year. What is the

arithmetic mean return on the investment?

A) −2.6%

B) +2.6%

C) +5.0%

D) +8.0%

Answer: C

Difficulty: 1 Easy

Topic: Performance evaluation

Accessibility: Keyboard Navigation

Gradable: automatic

16) Consider an investment held over three years with a return of +20 percent in the first

year, −25 percent in the second year, and +20 percent in the third year. What is the

geometric mean return on the investment?

A) −2.6%

B) +2.6%

C) +5.0%

D) +8.0%

Answer: B

Difficulty: 2 Medium

Topic: Performance evaluation

Accessibility: Keyboard Navigation

Gradable: automatic

17) What statistical concept do many portfolio managers use to represent risk when considering

investment performance?

A) The standard deviation of returns

B) The difference, or “spread,” between the highest value over the holding period and the lowest

value over the holding period

C) The geometric mean return

D) The coefficient of variation

18) Why does including REITs in a portfolio containing S&P 500 securities produce

diversification benefits?

A) Real estate investment returns are highly correlated with returns for stocks

B) Real estate investment returns are not highly correlated with returns for stocks

C) Real estate investment returns are not subject to federal income taxes

D) Real estate investment returns do not change much from year to year

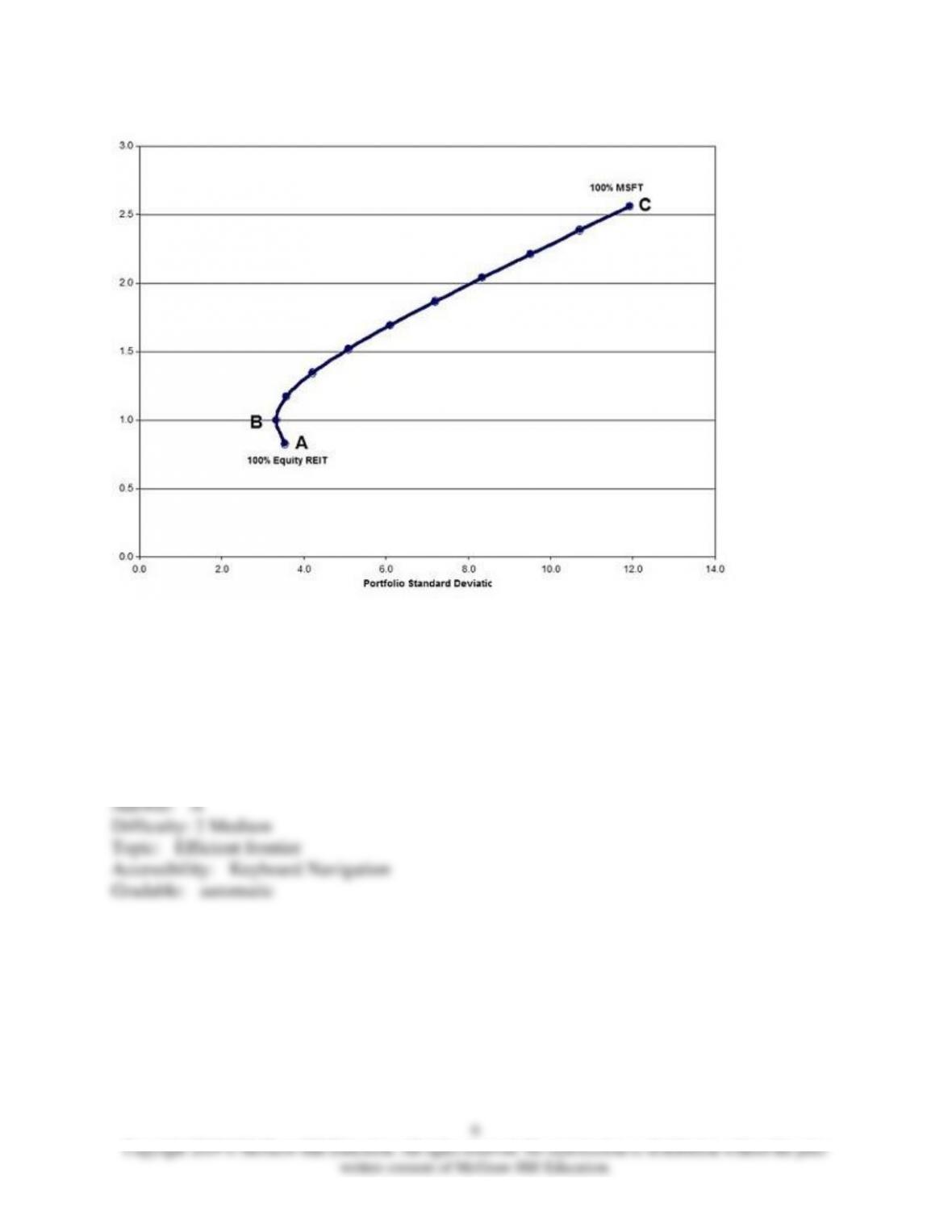

19)

Assume you have a choice between investing in either an equity REIT or Microsoft stock

(MSFT) or a combination of the two. Which point in the figure above is NOT on the efficient

portfolio frontier?

A) A

B) B

C) C

D) All points are on the efficient portfolio frontier

20) The data sources used to produce investment returns on investment properties include the:

A) National Association of Real Estate Professionals (NAREP)

B) National Association of Real Estate Investment Trusts (NAREIT)

C) National Board of Realtors (NBR)

D) All of the above

21) The NCREIF Property Index can be characterized by each of the following EXCEPT:

A) The index includes only properties with no outstanding mortgage debt

B) The information used in compiling the index is contributed by members of the NCREIF

C) The index reflects payments to both property managers and portfolio asset managers

D) All of the above are true

22) On January 1st, an investor purchases security A for $105. Over the next four months,

dividends totaling $15 were paid on security A. On March 31st, security A was sold for $120.

What is the holding period return for security A?

A) 0.0%

B) 14.3%

C) 25.0%

D) 28.6%

23) Geometric mean returns are:

A) Simple averages of holding period returns

B) Expressed as compound rates of interest

C) More applicable when no specific time interval is considered to be any more important than

another

D) Widely used in statistical studies spanning very long periods of time

24) Regarding real estate investments, risk that is associated with the type of property and its

location, design, lease structure, and so on can be thought of as:

A) Marketability risk

B) Liquidity risk

C) Business risk

D) Interest rate risk

25) The coefficient of variation, also known as the risk-to-reward ratio, is defined as:

A) The standard deviation of returns divided by the mean return

B) The variance of return multiplied by the mean return

C) The variance of returns divided by the standard deviation of returns

D) None of the above

26) Which of the following provides a measure of the extent to which returns tend to move

together or have no relationships?

A) The coefficient of determination

B) The variance

C) The coefficient of variation

D) The coefficient of correlation

27) If the returns of two securities are compared over time and there appears to be no

relationship between their movements, what is the likely value of their coefficient of correlation?

A) +1

B) −1

C) 0

D) +∞ (infinity)

28) Assume a portfolio is comprised of two securities, A and B, whose standard deviations are

0.0412 and 0.0721, respectively. If their covariance is 0.002, what is their coefficient of

correlation?

A) 0.005

B) 0.115

C) 0.673

D) 1.485

29) The optimal combination of securities that provides the greatest amount of return for each

level of risk is known as:

A) The expected frontier

B) The economic frontier

C) The efficient frontier

D) None of the above

30) The unit of measure that is used by portfolio managers to measure returns for individual

securities on a periodic basis is the:

A) Return on investment (ROI)

B) Holding period return (HPR)

C) Geometric mean return

D) Arithmetic mean return

31) The variability on an asset’s returns represents:

A) Flexibility

B) Profitability

C) Risk

D) Default

32) One would see the greatest amount of diversification from two securities that are:

A) Positively correlated

B) Negatively correlated

C) Not correlated

D) Perfectly correlated

33) Which of the following is a major property category associated with the NCREIF Index:

A) Apartment complexes

B) Office buildings

C) Hotels

D) All of the above