Real Estate Finance & Investments, 16e (Brueggeman)

Chapter 21 Real Estate Investment Trusts (REITs)

1) At least 95 percent of the value of a REIT’s assets must consist of real estate assets, cash, and

government securities.

2) Funds from operation (FFO), is calculated by adding back depreciation and amortization and

other non-cash deductions to earnings.

3) A mortgage REIT is a REIT that primarily invests in mortgages rather than equity ownership.

4) The U.S. is the only country that allows REITs (or similar investments).

5) Mortgage REITs use debt financing to increase their capital bases.

6) REITs are required to pay out 90 percent of their earnings as dividends.

7) The difference between EPS (earnings per share) and FFO (funds from operations) is the

interest deduction.

8) Usually ground leases are for relatively short periods of time.

9) REITs can sometimes capitalize rather than lease certain expenditures to increase FFO.

10) Because REITs are corporations, they are subject to double taxation.

11) A REIT must have at least 200 shareholders.

12) A portion of a REIT’s dividend may be a non-taxable return of capital.

13) Real estate assets, cash, and government securities must represent at least 75% of REIT

assets.

14) REITs must be passive investments with external advisors.

15) A blended capitalization rate is an average of the capitalization rates that would be used for

the individual properties in a portfolio if each was being valued separately.

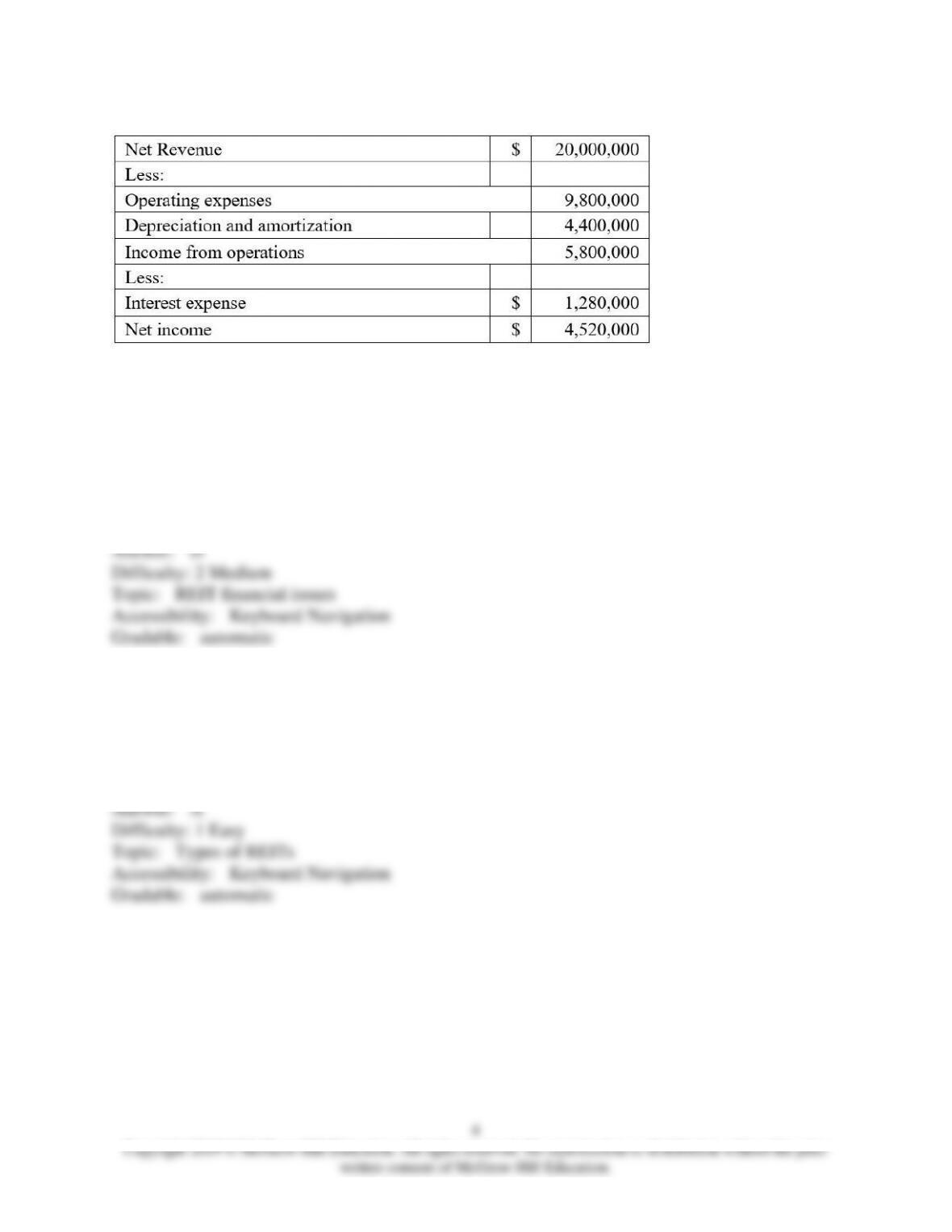

16)

Consider the financial statements for a REIT, given above. Price multiples for comparable REITs

are about 10 times current funds from operation (FFO). What price does this suggest for the

REIT’s shares if 1,000,000 shares are issued?

A) $4.52 per share

B) $45.20 per share

C) $8.92 per share

D) $89.20 per share

17) The most common type of REITs in today’s market are:

A) Equity trusts

B) Mortgage trusts

C) Hybrid trusts

D) Partnership trusts

18) Which of the following regarding private (unlisted) REITs is TRUE?

A) Unlisted REITs are less expensive than listed REITs

B) Unlisted REITs are less liquid than listed REITS

C) Unlisted REITs are more subject to short-term market price volatility than listed REITS

D) “List or liquidate” provisions in unlisted REITs make such REITs less risky than listed

REITS

19) A REIT has an NOI of $15 per share and currently pays a dividend of $10 per share. The

dividend is projected to increase by 4 percent by next year and continue to increase by 4 percent

per year thereafter. Assuming that the blended cap rate is 9.75 percent and the required rate of

return is 10.5 percent, what value would the Gordon Dividend Discount Model provide?

A) $60.15

B) $71.89

C) $153.85

D) $160.00

20) A REIT has an NOI of $15 per share and currently pays a dividend of $10 per share. The

dividend is projected to increase by 4 percent by next year and continue to increase by 4 percent

per year thereafter. Assuming that the blended cap rate is 9.75 percent and the required rate of

return is 10.5 percent, what would the net asset value (NAV) of the REIT be?

A) $60.15

B) $71.89

C) $153.85

D) $160.00

21) Which of the following is NOT a current type of REIT?

A) Mortgage trust

B) Equity trust

C) Hybrid trust

D) Neither Mortgage trust nor Hybrid trust

22) Hybrid REITs, which are no longer tracked by NAREIT, are comprised of what primary

classifications of REITs?

A) UPREITs, mortgage

B) Mortgage, equity, retail

C) Mortgage, equity

D) Healthcare, retail, office

23) A REIT with 100 shares outstanding earns $1,000 in rent and incurs operating expenses of

$400. In addition, the REIT owns property with an historic cost of $6,000 and depreciates it over

a 15 year period using straight-line depreciation. What are the funds from operations per share

and the earnings per share for this REIT?

A) $4 and $3, respectively

B) $4 and $2, respectively

C) $6 and $2, respectively

D) $6 and $3, respectively

24) A REIT with 100 shares outstanding earns $1,000 in rent and incurs operating expenses of

$400. In addition, the REIT owns property with an historic cost of $6,000 and depreciates it over

a 15 year period using straight-line depreciation. At the very least, what dividend payment must

it make to maintain its tax exempt status?

A) $1.80/share

B) $2.00/share

C) $3.60/share

D) $5.40/share

25) An investor pays $63.00 per share for stock in a given REIT. The REIT declares a dividend

of $4.00 per share and has an EPS of $2.37. Considering the recovery of capital (ROC), what is

the new cost basis of the stock acquired by the investor?

A) $60.63

B) $61.37

C) $63.00

D) $64.63

26) Which of the following is NOT a requirement of REITs?

A) A REIT must have at least 100 stockholders

B) Not more than 50% of a REIT’s shares can be owned by five or fewer shareholders

C) At least 90% of a REIT’s income must be distributed to shareholders

D) All of the above are REIT requirements

27) Which of the following REIT types is organized to acquire the specific property or properties

described in its prospectus?

A) A property trust

B) A mixed trust

C) A purchasing trust

D) An exchange trust

28) Which of the following REIT types is NOT likely to own real property?

A) Hybrid REIT

B) Mortgage REIT

C) Equity REIT

D) All of the above

29) Which of the following is likely to occur upon the sale of a REIT-owned property?

A) If a capital gain is realized, the REIT can retain the gain for future investment and be taxed at

the appropriate corporate capital gains tax rate

B) If a capital gain is realized, the REIT can retain the gain for future investment and be taxed at

the shareholder’s capital gains tax rate

C) If a capital gain is realized, the REIT can distribute the gain as a dividend to shareholders who

will realize it as dividend income for individual tax reporting purposes

D) If a capital loss is realized, the loss can be passed through to individual investors

30) The funds from operations (FFO) for a REIT is roughly equal to:

A) NOI less interest deductions

B) Earnings before tax plus noncash expenses

C) NOI plus interest deductions

D) Earnings per share plus capital gains

31) Once an entity has been terminated as a REIT, the entity cannot make a new election to be

taxed as a REIT until ________ years after the termination.

A) 2

B) 3

C) 4

D) 5

32) The difference between EPS (earnings per share) and FFO (funds from operations) is:

A) Irrelevant

B) Determined by growth of the company

C) Due to depreciation and amortization

D) Due to the number of shares outstanding

33) REIT dividends are considered ________ income and thus do not qualify as passive income

to offset passive losses.

A) Portfolio

B) Operating

C) Trading

D) Outside professional

34) Recovery of capital (ROC) results in:

A) An increase in the dividend available to the investor

B) An increase in the value of the stock

C) A reduction in the cost basis of acquired stock

D) A reduction in losses on the stock

35) The growth of the REIT industry in the early 1970s was mainly attributed to which of the

following?

A) Mortgage trust loans were less regulated than bank loans

B) Increased interest rates

C) Declined performance of other investments

D) Increased value of real property throughout the country

36) Which of the following represents the space that is currently being rented to paying tenants?

A) Leased space

B) Occupied space

C) Ground space

D) REIT space

37) An arrangement in which a REIT collects a stream of rents from a building owner, then

makes a lower, and sometimes fixed, payment to the landowner:

A) Fixed investment

B) REIT spreading

C) Spread investing

D) Renewal option