Real Estate Finance & Investments, 16e (Brueggeman)

Chapter 16 Financing Project Development

1) One of the risks of project development is “project risks,” which are the result of unexpected

changes in general market conditions affecting the supply and demand for space.

2) In general, developers must get a construction loan before they can line up permanent (long-

term) financing that will be used once the project is complete and being operated with tenants.

3) A bullet loan is a construction loan that, in effect, becomes permanent financing when

construction is complete.

4) Holdbacks are used by construction lenders to be sure that a developer has met all of his or her

obligations before all of the funds from the construction loan are given to the developer.

5) The demand for retail space should be examined in terms of the characteristics of the tenant’s

demand in a given market.

6) Construction loans provide the money to construct a building and are usually provided by life

insurance companies or pensions funds.

7) Permanent loans generally provide the money to pay off the construction loan in segments, as

the work progresses.

8) Commitments for construction financing are usually contingent on commitments for

permanent financing.

9) Permanent financing commitments usually allow the lender to approve major leases.

10) Lenders typically finance the development of a project as a percentage of completed

appraised value, including the price of the site.

11) Even after obtaining permanent financing, a developer still maintains the right to alter a

project’s design or the level of expenditures.

12) Generally, as the cost of a site increases, so do the quality and the density of the

improvements constructed on it.

13) Loans made under the assumption that markets will turn around are referred to as spec loans.

14) A standby commitment differs from a permanent take-out commitment in that neither party

really expects the standby commitment to be used by the developer.

15) A permanent take-out commitment is:

A) A way to increase NOI for projects with large debt service obligations

B) An agreement by a lender to provide permanent financing for a property once construction is

complete, provided all of the contingencies have been met.

C) Another term for a construction loan

D) The same thing as an acquisition and development loan

16) Which of the following is one reason that construction lenders typically prefer the cost

approach to valuation over the income approach?

A) The cost approach provides a more conservative estimate of value

B) The cost approach provides a more optimistic estimate of value

C) The cost approach is a good indication of the expected value of an income-producing property

once construction is complete and it has been leased-up

D) The cost approach is a better estimate of actual market value of the project

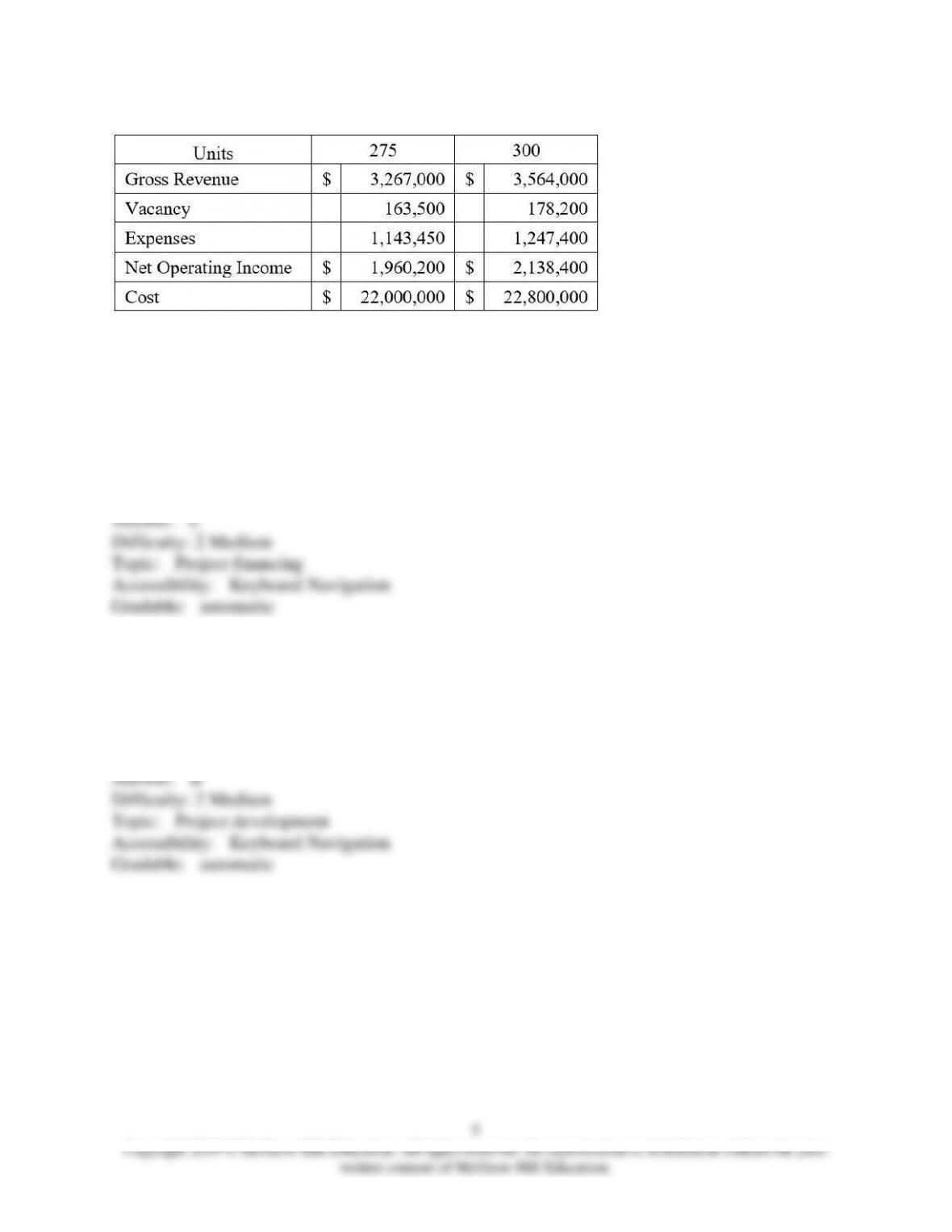

17)

Consider the table above. An investor-developer demands a return of at least 9 percent on cost.

Which of the following statements is TRUE based on the information above?

A) Neither project produces a sufficient expected return

B) The 275 unit project produces a sufficient return, but the 300 unit project does not

C) The 300 unit project produces a sufficient return, but the 275 unit project does not

D) Both projects produce sufficient return, but the 275 unit project produces a higher return than

the 300 unit project

18) Which of the following is the usual progression for a real estate development project?

A) Land acquisition, completion, management, sale, construction

B) Land acquisition, construction, completion, management, sale

C) Land acquisition, construction, completion, sale, management

D) Land acquisition, management, construction, completion, sale

19) Which of the following is a “soft cost” of construction?

A) The cost of the architectural drawings

B) The cost of pouring the foundation

C) The cost of erecting the building

D) The cost of finishing the interior space

20) Permanent funding commitments usually contain many funding contingencies. Which of the

following typically is NOT one of those contingencies?

A) Approval of all prospective leases

B) Approval of design changes or building material substitution

C) Provisions for gap financing

D) Minimum rent-up requirements

21) Mini-perm loans usually refer to financing:

A) At local coffers

B) For the lease-up period

C) For construction and all subsequent periods

D) For construction, lease-up, and one or two subsequent years

22) The MOST common method of distributing funds provided by a construction loan is a:

A) Single lump sum of money at the closing of the loan

B) Single lump sum of money at the end of the construction project to reimburse the developer

for the project’s expenses and profit

C) Series of payments throughout the construction project to reimburse the developer for costs

incurred since the previous payment

D) Series of payments throughout the construction project to reimburse the developer for

anticipated expenses in the upcoming period

23) In comparison to permanent financing, the rates and rate variability for a construction loan

would be:

Interest Rate

Interest Rate Variability

(A)

High

Steady

(B)

High

Fluctuating

(C)

Low

Steady

(D)

Low

Fluctuating

A) Option A

B) Option B

C) Option C

D) Option D

24) Interest on a construction loan is usually paid:

A) Up front at the beginning of the loan

B) Periodically over the life of the loan

C) In quarterly installments over the life of the loan

D) At the end of the loan

25) Besides an estimate of costs, a construction loan submission package includes many other

components. Which of the following is NOT one of those components?

A) Two years of prior tax returns

B) Current financial statements

C) Pro Forma Operating Statements

D) Ratio and Sensitivity Analysis

26) In the context of a lease, percentage rents generally indicate that:

A) The tenant will pay a proportionate amount of rent for his space in comparison to the total net

rentable area

B) In addition to a base rent, the lessor will receive a percentage of the tenant’s cash flow above

some break even point

C) The tenant will pay a rent that is a certain percentage of the national average

D) None of the above

27) Why would a developer be willing to manage a completed project even after it has been

sold?

A) The developer knows the project better than other management companies and, therefore,

could manage the property more efficiently

B) The developer could profit from the lucrative management fees being charged by

management companies

C) Knowledge of the tenant’s needs and the current leasing market might give the developer

better insight with respect to future developments

D) All of the above

28) Which of the following is NOT one of the development strategies that may be used by

developers?

A) Selling and leasing back the land for the development

B) Owning and managing the real estate after sale

C) Selling the real estate after lease-up phase

D) Developing the real estate for lease in master-planned development

29) Which of the following is FALSE regarding a construction loan?

A) It usually has a lower rate than does permanent financing

B) It is also known as an interim

C) Hard costs can usually be financed

D) The entire land cost cannot usually be financed

30) Which of the following common contingencies is NOT usually included with a permanent

financing agreement?

A) Completion date for construction phase

B) Minimum rent-up requirements

C) Materials used in construction phase

D) Cleanliness of work area

31) What term applies to third-party financing that is used between funds advanced by the

permanent lender and funds needed to repay the construction loan?

A) Interim loan

B) Mini-perm financing

C) Gap financing

D) Partial financing

32) Developers usually hold back about ________ percent of each progress payment.

A) 1

B) 10

C) 25

D) 75

33) ADL lenders recognize that too much of what may lead to significant overbuilding and an

excess supply of space in a local market?

A) Speculative, closed-ended construction lending

B) Speculative, open-ended construction lending

C) Planned, closed-ended construction lending

D) Planned, open-ended construction lending

34) When commercial banks consider construction loans their analysis is generally based on

which of the following:

A) Hard costs, soft costs

B) Hard costs, soft costs, site location

C) Hard costs, soft costs, appraised value

D) Hard costs, site location

35) In determining whether a project is commercially viable given the prevailing market rents,

land prices, and construction and financing costs, a developer would be likely to conduct a(an):

A) Feasibility analysis

B) Submarket analysis

C) Economic analysis

D) Multivariate analysis