Real Estate Finance & Investments, 16e (Brueggeman)

Chapter 14 Disposition and Renovation of Income Properties

1) One factor an investor should consider when trying to decide whether to dispose of a property

he or she has owned for several years is the expected IRR for holding versus sale of the property.

2) Increasing rents tend to increase the marginal rate of return on a property.

3) A property should be sold when the marginal rate of return rises above the rate at which funds

can be reinvested.

4) One disadvantage of refinancing a property instead of selling the property is that taxes have to

be paid on funds received by additional borrowing, but no taxes would have to be paid if the

property is sold.

5) If capital gains tax must be paid, the opportunity cost of selling increases relative to the

opportunity costs of keeping the property.

6) When evaluating the incremental costs of borrowing, if the interest rate is higher on the larger

loan amount, the incremental cost of the additional funds borrowed tends to be lower than the

rate on the larger loan.

7) The benefits of equity buildup in a property are lessened over time because with an amortizing

mortgage, an investor will lose some tax benefits each year as the interest portion of the

payments decreases.

8) An investor purchased a property expecting to receive a 14% rate of return. However, the rate

of return on the property over a 5 year holding period turned out to be only 11.5%. Therefore, the

property should be sold.

9) Given the same expectations for future rents and expenses, a new buyer may earn a different

after-tax return than the current owner of the same property.

10) In general, equity buildup tends to lower the marginal rate of return of holding a property.

11) An investor calculates an incremental return of renovating a building of 14%. Other

properties provide a 12.5% overall rate of return to equity investors. Therefore, the property is a

good investment.

12) If a real estate tax law becomes more favorable, this generally benefits existing investors

over new investors.

13) The marginal rate of return on a property usually increases until the sale of the property.

Equity buildup should always be avoided if possible.

14) A property should be sold when the marginal rate of return falls below the rate at which

funds can be reinvested.

15) For refinancing to be profitable, the effective cost of the debt must be less than the unlevered

return on the projects being financed.

16) The investment foundation of a real estate investment is another name for the initial

investment.

17) If an investor is deciding whether to sell a property, his equity buildup in the existing

property should be considered as an opportunity cost.

18) The marginal rate of return for a property is:

A) The APR on an incremental amount of borrowing

B) The expected holding period return earned when the investor purchases the property

C) The return earned on subprime property relative to prime property

D) The return gained by holding the property for one additional year

19) Which of the following is NOT a typical benefit of renovating a property?

A) Increasing rents

B) Lowering vacancy

C) Increasing operating expenses

D) Increasing the future property value

20) Consider the information in the table below. What is the marginal rate of return for keeping

the property one additional year?

If sold today

If sold

next year

Sale price

$

2,500,000

$

2,650,000

Mortgage balance

1,000,000

900,000

Capital gain tax

112,500

135,000

Cash flow

$

1,387,000

$

1,615,000

NOI over next year

$

50,000

A) 16.4%

B) 20.0%

C) $50,000

D) $277,500

21) Consider the information in the table below. What is the rate of return the investor would

earn on the additional funds invested in renovating the property, assuming that the investor

would not borrow any additional funds?

After-tax cash flow from operations if renovated

$

75,000

After-tax cash flow from operations if not renovated

−

60,000

Incremental cash flow from operations

$

15,000

Sale proceeds if renovated

$

2,500,000

Sale proceeds if not renovated

2,250,000

Incremental cash flow from sale

$

250,000

Renovation costs

$

250,000

A) 6.0%

B) 106%

C) $15,000

D) $265,000

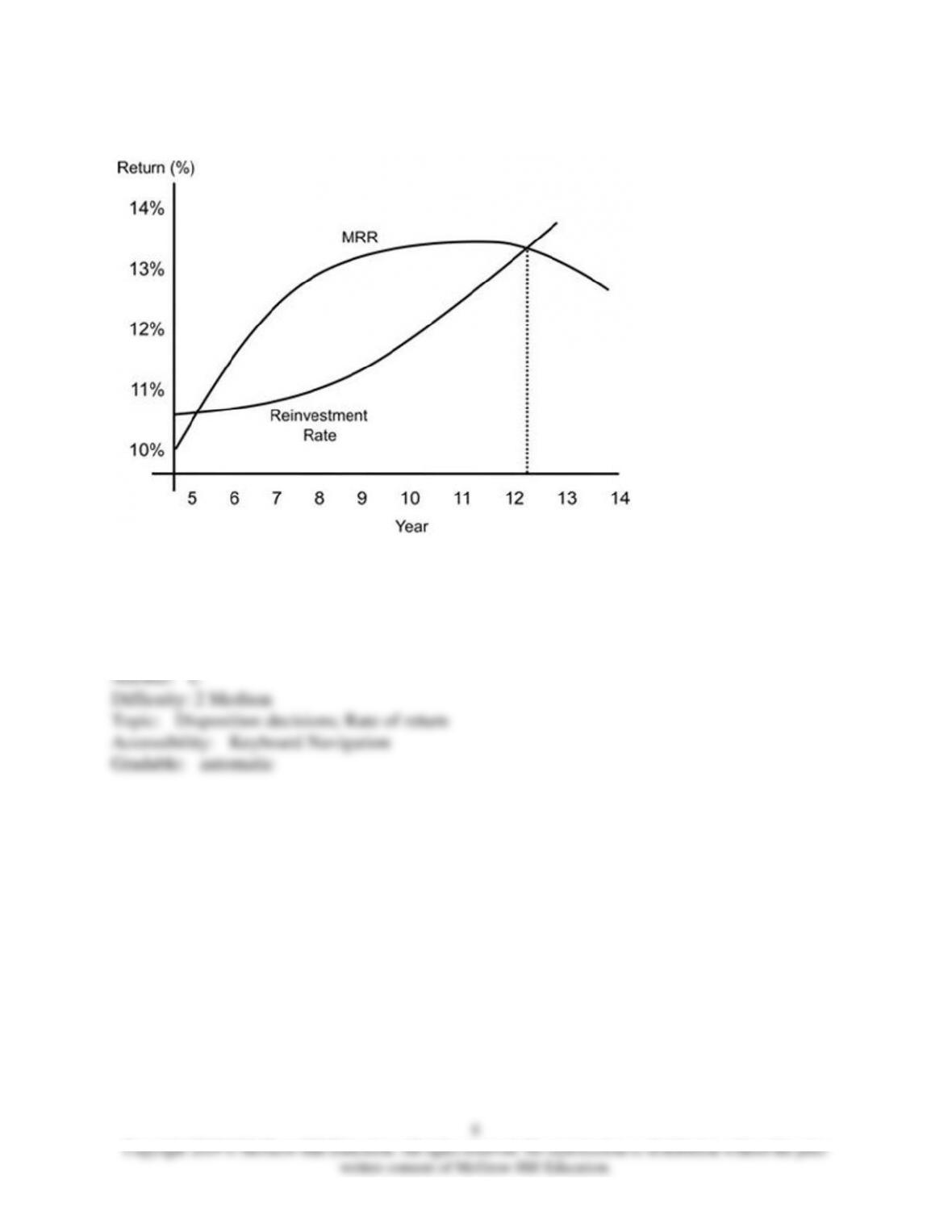

22) Consider the figure below. The dotted (vertical) line denotes the:

A) Incremental rate of return on additional borrowed funds

B) Marginal rate of return

C) Optimal holding period

D) Optimal yield

23) A property, if sold today, will provide the equity investor with $150,000 in cash flow after

taxes. If the property is held, the annual after-tax cash flow received by the investor will be as

follows: $18,000 for years 1 to 5, $24,000 for years 6 to 10. If held and sold in 10 years, the

property is expected to provide $180,000 in after-tax cash flow to the investor. What should the

investor do if she can receive a 14% rate of return by investing the sales proceeds today in a

different project?

A) Sell the property and invest proceeds in the second property

B) Do not sell the property

C) Renovate the property

D) Can’t tell without knowing the cash flow from the second property

24) A property could be sold today to provide an after-tax cash flow from sale of $800,000. The

current after-tax cash flow from operations is $20,000, which is expected to grow by 4% per

year. If sold next year, the property is expected to provide an after-tax cash flow of $824,000.

What is the marginal rate of return for holding the property for an additional year?

A) 5.6%

B) 2.6%

C) 3.1%

D) 9.3%

25) Which of the following factors would NOT be considered when an investor is trying to

decide whether to hold or sell a property at the end of year five?

A) After-tax operating income in year five

B) After-tax cash flow from the sale in year five

C) After-tax cash flow from the sale in the future

D) After-tax operating income after year five

26) A property worth $16 million can be refinanced with an 80% loan at 9.5% over 20 years. The

balance on the current loan is $12,148,566. Loan payments are $113,302 per month. The loan

balance in 10 years will be $8,396,769. If the property is expected to be sold in 10 years, what is

the incremental cost of refinancing?

A) 9.71%

B) 10.36%

C) 12.42%

D) 14.58%

27) An investor is considering renovating a building. The total cost of renovation is expected to

be $100,000, of which 75% can be borrowed. Given the after-tax cash flows to the equity

investor as showed below, what is the incremental return from renovating?

1

2

3

4

5

ATCF after renovation

9,200

10,000

12,000

14,000

316,000

ATCF-no renovation

10,000

10,200

10,440

10,680

160,900

A) 9.75%

B) 10.14%

C) 15.32%

D) 12.67%

28) Which of the following represents the formula for the annual marginal rate of return (MRR)

when trying to decide whether to hold or sell a property (ATCFS equals the after-tax cash flow

from sale and ATCFO equals the after-tax cash flow from operations)?

A) MRR = (ATCFS (year t + 1) + ATCFO (year t + 1) − ATCFS (year t) − ATCFO (year t) /

ATCFS (year t)

B) MRR = (ATCFS (year t + 1) − ATCFO (year t + 1) + ATCFS (year t)) / ATCFS (year t)

C) MRR = (ATCFS (year t + 1) + ATCFO (year t + 1) − ATCFS (year t)) / ATCFS (year t)

D) MRR = (ATCFS (year t + 1) + ATCFO (year t + 1) + ATCFS (year t)) / ATCFS (year t)

29) Which of the following would be considered when an investor is trying to decide whether or

not to renovate a property?

A) After-tax operating income before renovation

B) The difference between future operating income if renovated and if not renovated

C) After-tax cash flow from sale the year of renovation

D) The mortgage balance on the property the year before renovation

30) An investor is considering refinancing a property. The current mortgage has an interest rate

of 8.75% and a mortgage balance equal to 45% of the property value due to amortization of the

loan and some appreciation in value. However, the investor would like to refinance at an amount

equal to 75% of the property value. He has found out that the property can be refinanced at a

75% loan-to-value ratio for 9.5% interest over 15 years. What can be said about the incremental

cost of refinancing?

A) It will be higher than 9.5%

B) It will be less than 9.5%

C) It will be equal to 9.5%

D) Can’t tell without additional information

31) An investor purchased a building in 1982 when the building could be depreciated over 19

years. A new investor is interested in purchasing the building in 1992 when the depreciable life

according to tax laws is 31.5 years. Assuming both investors are in the same tax bracket and that

everything else is equal, what can be said about the after-tax cash flow received by the new

investor as compared to the after-tax cash flow that would be received by the original owner of

the building?

A) The new investor will have a higher after-tax cash flow because the depreciation expense will

be lower

B) The new investor will have a higher after-tax cash flow because the depreciation expense will

be higher

C) Both investors will have to use the 31.5 year depreciable life after 1986 so the after-tax cash

flow will be equal

D) The new investor will have a lower after-tax cash flow because the depreciation expense will

be lower

32) The marginal rate of return can be defined as the:

A) Return that results from holding the property for one additional year

B) IRR the year the internal rate of return starts to decrease from holding the property

C) Incremental return over a holding period resulting from renovating a property

D) Rate of return at which the net present value equals zero

33) Disposition when dealing with real estate means which of the following?

A) The way a property fits in with its surroundings

B) Refinancing the property

C) Improving property value

D) Sale of the property

34) The return calculated assuming the property is held for one additional year is referred to as

the:

A) After-tax cash flow from sale

B) Marginal rate of return

C) Reinvestment rate

D) None of the above

35) A property should be sold when which of the following occurs?

A) The marginal rate of return is rising but less than the reinvestment rate

B) The marginal rate of return is constant

C) The marginal rate of return is zero

D) The marginal rate of return is falling and becomes equal to the reinvestment rate

36) Which of the following is NOT a benefit of refinancing?

A) The investor can increase financial leverage

B) It is an alternative to sale of the property

C) Risk is decreased

D) No taxes have to be paid on funds received by additional borrowing

37) A property sale in which the buyer may make payments over time instead of paying the full

price at the time of purchase, is referred to as a(an):

A) Like kind sale

B) Carry over sale

C) Equivalent investment sale

D) Installment sale

38) In a real estate transaction, gross profit divided by the contact price is referred to as the:

A) Net profit

B) Operating profit

C) Profit ratio

D) Mortgage profit