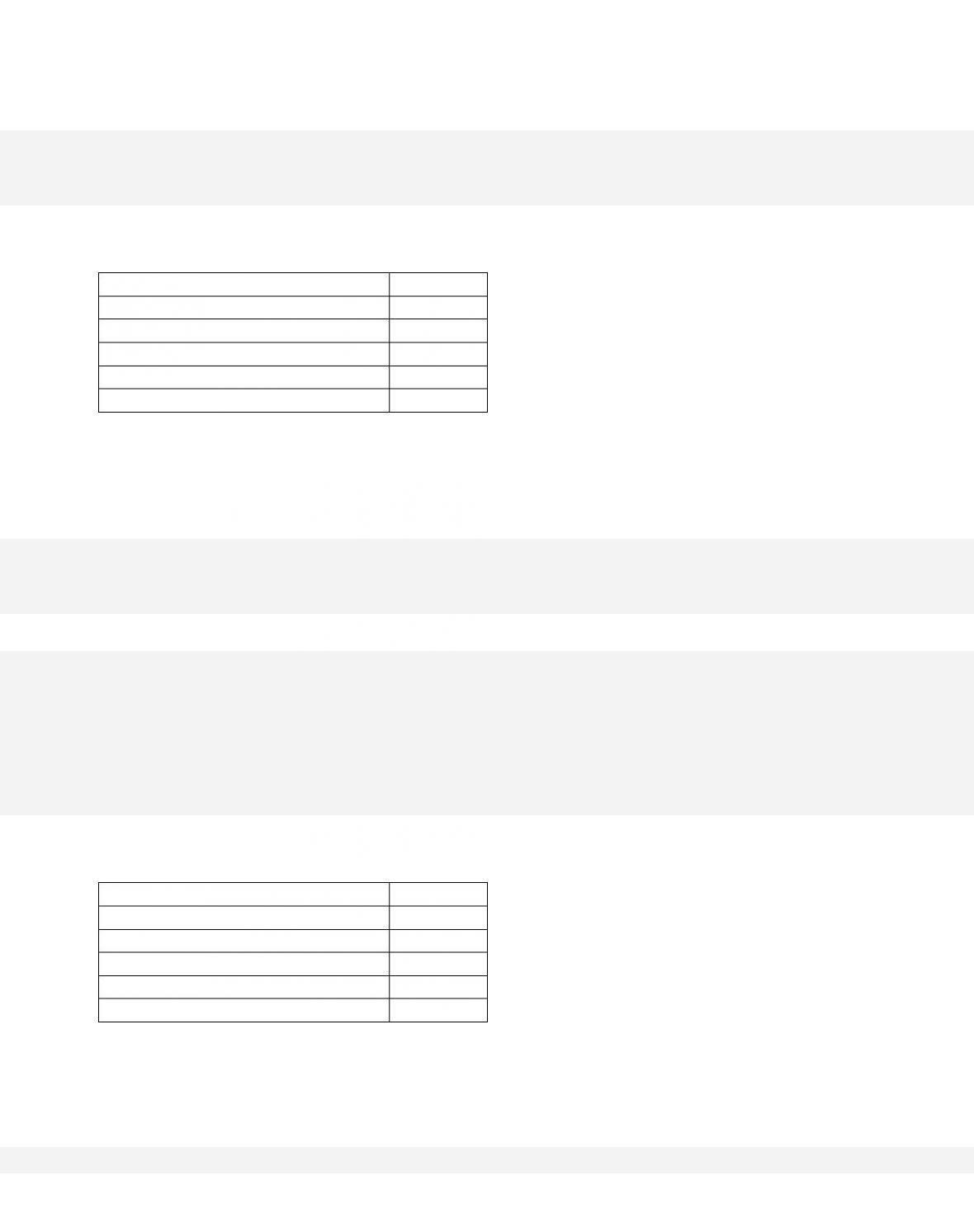

10

$40,000

$10,000

20

40,000

10,000

25

40,000

10,000

30

40,000

10,000

The accompanying table gives data for a commercial bank or thrift. If the legal reserve

ratio falls from 25 percent to 10 percent, excess reserves of this single bank will

92. If actual reserves in the banking system are $8,000, checkable deposits are $70,000,

and the legal reserve ratio is 10 percent, then excess reserves are

93.

If actual reserves in the banking system are $40,000, excess reserves are $10,000, and

checkable deposits are $240,000, then the legal reserve requirement is

35–42

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

B. 12.5 percent.

C. 20 percent.

D.

5 percent.

94. If actual reserves in the banking system are $50,000, excess reserves are $5,000, and

checkable deposits are $225,000, then the monetary multiplier is

95.

If the monetary authorities want to reduce the monetary multiplier, they should

35–43

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

Topic: The Monetary Multiplier

96.

If the reserve ratio is 100 percent, the value of the monetary multiplier is

97. The greater the required reserve ratio, the

98. Money is destroyed when

35–44

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

Learning Objective: 35-03 Describe how a bank can create money.

Learning Objective: 35-04 Describe the multiple expansion of loans and money by the entire

banking system.

Test Bank: I

Topic: Money-Creating Transactions of a Commercial Bank

T o p i c : The Banking System: Multiple-Deposit Expansion

99. When a bank loan is repaid, the supply of money

100.

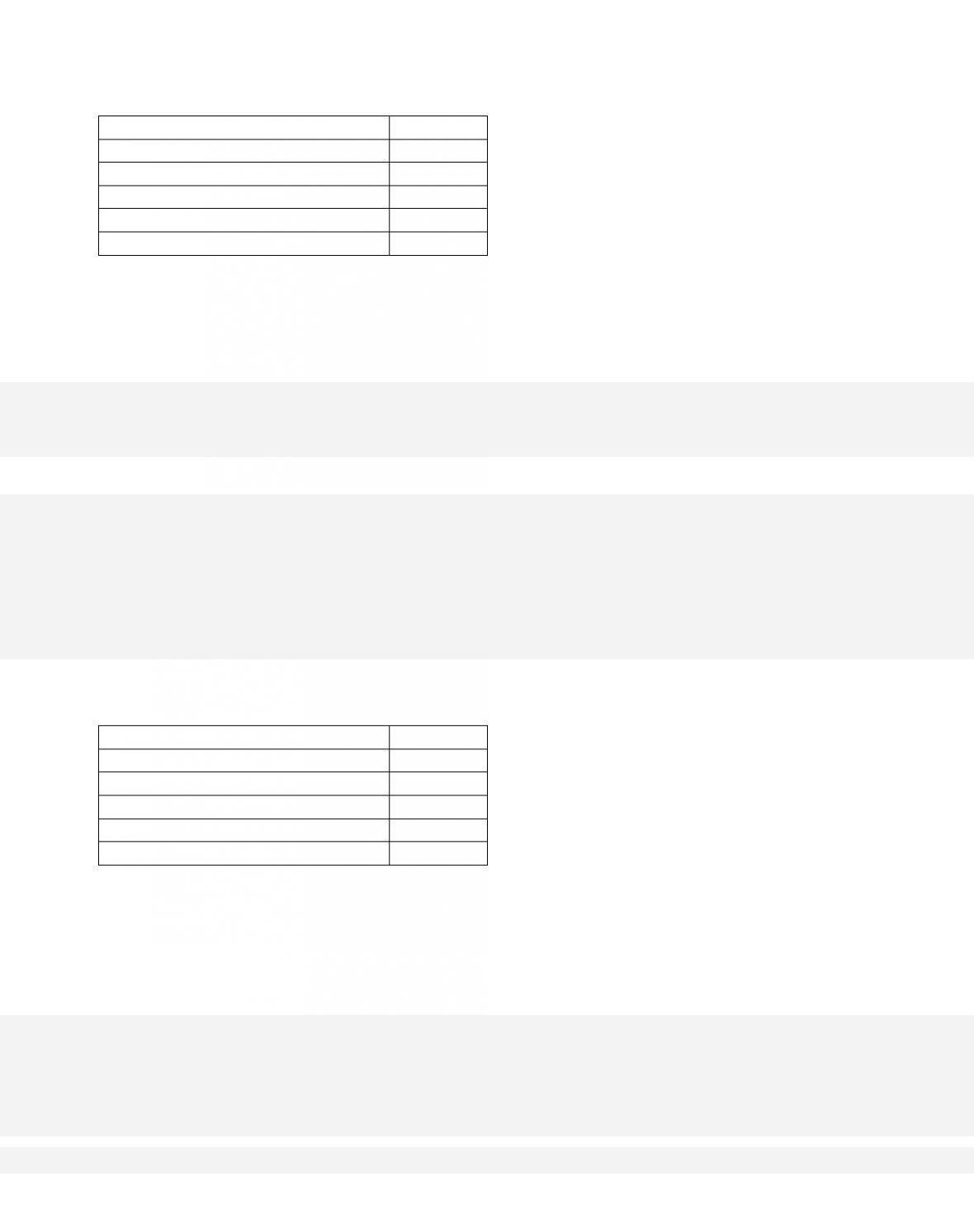

Reserves

$100

Checkable Deposits

1,000

Loans (to customers)

300

Property

400

Securities (owned)

300

Stock Shares

100

Refer to the accompanying table of information for the Moolah Bank. Assume that the

listed amounts constitute this bank‘s complete set of accounts. Moolah’s

35–45

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

between a banks actual reserves and its required reserves.

Test Bank: I

Topic: A Single Commercial Bank

Type: Table

101.

Reserves

$100

Checkable Deposits

1,000

Loans (to customers)

300

Property

400

Securities (owned)

300

Stock Shares

100

Refer to the accompanying table of information for the Moolah Bank. Assume that the listed

amounts constitute this bank’s complete set of accounts. Moolah’s

102.

Reserves

$100

Checkable Deposits

1,000

Loans (to customers)

300

Property

400

Securities (owned)

300

Stock Shares

100

Refer to the accompanying table of information for the Moolah Bank. Assume that the

listed amounts constitute this bank‘s complete set of accounts. Moolah’s

35–46

103.

Reserves

$100

Checkable Deposits

1,000

Loans (to customers)

300

Property

400

Securities (owned)

300

Stock Shares

100

Refer to the accompanying table of information for the Moolah Bank. If Moolah Bank is legally

“loaned up,” the reserve requirement must be

104.

Reserves

$100

Checkable Deposits

1,000

Loans (to customers)

300

Property

400

Securities (owned)

300

Stock Shares

100

Refer to the accompanying table of information for the Moolah Bank. If Moolah Bank is legally

“loaned up,” the banking system’s monetary multiplier must be

105.

Reserves

$100

Checkable Deposits

1,000

Loans (to customers)

300

Property

400

Securities (owned)

300

Stock Shares

100

Refer to the accompanying table of information for the Moolah Bank, and assume that Moolah

bank is “loaned up.” If it receives a $100 deposit of currency, it could safely expand its loans

by

35–48

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

AACSB: Knowledge Application

Blooms: Understand

D i f f i c u l t y : 02 Medium

Learning Objective: 35-03 Describe how a bank can create money.

Test Bank: I

Topic: Money-Creating Transactions of a Commercial Bank

Type: Table

106.

Reserves

$100

Checkable Deposits

1,000

Loans (to customers)

300

Property

400

Securities (owned)

300

Stock Shares

100

Refer to the accompanying table of information for the Moolah Bank, and assume that

Moolah Bank is “loaned up.” If it receives a $100 deposit of currency, the banking system

of which Moolah is a part could expand loans by

107. (Last Word) The term “leverage” refers to

35–49

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

Blooms: Understand

D i f f i c u l t y : 02 Medium

Learning Objective: 35-04 Describe the multiple expansion of loans and money by the entire

banking system.

Test Bank: I

Topic: The Banking System: Multiple-Deposit Expansion

108.

(Last Word) The greater the leverage in the financial system, all else equal,

109.

(Last Word) Suppose Balin has $100 to invest in an opportunity that returns, for every $100

invested, $120 if it goes well but only $80 if it goes poorly. If leverage allows Balin to borrow

$90 for every $10 he invests, what are his rates of profit and loss, respectively, if he

borrows the full amount to invest in the opportunity?

110. (Last Word) Leverage in the financial system

35–50

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

A. magnifies profits but reduces losses.

B. magnifies both profits and losses.

C. reduces profits but magnifies losses.

D.

reduces both profits and losses.

AACSB: Knowledge Application

A c c e s s i b i l i t y : Keyboard Navigation

Blooms: Understand

D i f f i c u l t y : 02 Medium

Learning Objective: 35-04 Describe the multiple expansion of loans and money by the entire

banking system.

Test Bank: I

Topic: The Banking System: Multiple-Deposit Expansion

True / False Questions

111. Excess reserves are the amount by which required reserves exceed actual reserves.

112.

Actual reserves equal required reserves plus excess reserves.

113. Commercial bank reserves are an asset to commercial banks but a liability to the

Federal Reserve Bank holding them.

114. Balance sheets always balance because reserves must always equal liabilities plus

net worth.

115.

Loans made to customers are a liability on a bank‘s balance sheet.

116. Checkable deposits are a liability on a bank‘s balance sheet.

35–52

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

AACSB: Knowledge Application

A c c e s s i b i l i t y : Keyboard Navigation

Blooms: Understand

D i f f i c u l t y : 02 Medium

Learning Objective: 35–02 Explain the basics of a banks balance sheet and the distinction

between a banks actual reserves and its required reserves.

Test Bank: I

Topic: A Single Commercial Bank

117.

The supply of money increases when the public buys government securities from

commercial banks.

118. Commercial banks increase the supply of money when they purchase either personal

IOUs or government bonds from businesses and households.

119.

When commercial banks retire outstanding loans, the supply of money is increased.

35–53

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

Test Bank: I

Topic: Money-Creating Transactions of a Commercial Bank

120. Commercial banks monetize claims when they sell securities to Federal Reserve

Banks.

121. The banking system can lend by a multiple of its excess reserves because lending

does not result in a loss of reserves to the banking system as a whole.

122.

The monetary multiplier and the spending multiplier are two ways of referring to the same

concept.

123. In an uncontrolled or unregulated system, commercial bank lending will tend to

intensify the business cycle.

124. An individual bank can safely lend out a multiple of its excess reserves, but the

banking system can safely lend out only an amount equal to the excess reserves in the

banking system.

125. If the reserve requirement is 20 percent, the monetary multiplier will be 4.

126.

The higher the reserve requirement, the lower is the monetary multiplier.

Multiple Choice Questions

127. Fractional reserve banking refers to a system where banks

128.

The fractional reserve system of banking started when goldsmiths began

35–56

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

Test Bank: II

Topic: The Fractional Reserve System

129.

What is one significant consequence of fractional reserve banking?

130.

What is one significant characteristic of fractional reserve banking?

131. A bank’s net worth is equal to its

35–57

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

Blooms: Understand

D i f f i c u l t y : 02 Medium

Learning Objective: 35–02 Explain the basics of a banks balance sheet and the distinction

between a banks actual reserves and its required reserves.

Test Bank: II

Topic: A Single Commercial Bank

132.

A bank’s net worth is the

133. A bank owns a 10-story office building. In the bank’s balance sheet, this would be

listed as part of

134.

A bank has $2 million in checkable deposits. In the bank’s balance sheet, this would be part

of

35–58

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

B. liabilities.

C.

capital stock.

D.

net worth.

135.

The claims of creditors of a bank against the bank’s assets are called

136. Which of the following are liabilities to a bank?

137. One major component of money supply M1 is part of a bank‘s

138.

A checkable deposit at a commercial bank is a(n)

139. Cash held by a bank in its vault is a part of the bank‘s

35–60

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

Learning Objective: 35–02 Explain the basics of a banks balance sheet and the distinction

between a banks actual reserves and its required reserves.

Test Bank: II

Topic: A Single Commercial Bank

140.

When a bank sells capital stock (equity shares) in return for cash,

141.

When cash is deposited in a checkable-deposit account at a bank, there is

142. When cash is withdrawn from a checkable-deposit account at a bank,