Refer to the accompanying graphs for a competitive market in the short run. What will happen to

the representative firm‘s economic profits as long-run market adjustments occur?

123. The long-run supply curve under pure competition is derived by observing what happens to

market price and quantity when market

124. The long-run supply curve under pure competition will be

11–62

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

Blooms: Understand

Diffi culty :

02 Medium

Learning Objective: 11–03 Explain the differences between constant-cost, increasing-cost, and

decreasing-cost industries.

Test Bank: II

Topic:

Long-Run Supply Curves

125. The long-run supply curve would be perfectly elastic when

126. The long-run supply curve for a purely competitive industry would be horizontal when

127. The long-run supply curve would be upward-sloping if

11–63

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

D. resource prices are set by the government.

128. The long-run market supply curve would be downward-sloping if the representative firms’

130. If there is a decrease in demand for a product in a purely competitive industry, it results in

an industry contraction that will end when the product price is

131. An industry where a change in the number of firms does not affect the prices of the

resources used in the industry will have a long-run supply curve that is

132. If the long-run supply curve is upward-sloping, it indicates that resource prices fall when

11–65

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

Learning Objective: 11–03 Explain the differences between constant-cost, increasing-cost, and

decreasing-cost industries.

Test Bank: II

Topic:

Long-Run Supply Curves

133. A long-run supply curve that is downward-sloping indicates that the firms‘ ATC curves

134. What happens in a decreasing-cost industry when some firms leave and the industry‘s output

contracts?

135. Assume a purely competitive decreasing-cost industry is initially in long-run equilibrium

but then there is a decrease in market demand for the product. After all economic adjustments to

this new situation have taken place, product price will be

11–66

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

C. higher, and total output will be higher.

D. lower, but total output will be higher.

136. Assume a purely competitive constant-cost industry is initially at long-run equilibrium.

Now suppose that a decrease in demand occurs. After all the long-run adjustments have been

completed, the new equilibrium price

137. Which statement is correct? The long-run supply curve for a purely competitive

11–67

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

Topic:

Long-Run Supply Curves

138. One explanation for the existence of an increasing-cost industry is that

140. An industry that has increasing returns to scale and fixed factor prices will have a long-run

supply curve that is

11–68

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

Blooms: Understand

Diffi culty :

02 Medium

Learning Objective: 11–03 Explain the differences between constant-cost, increasing-cost, and

decreasing-cost industries.

Test Bank: II

Topic:

Long-Run Supply Curves

141.

The provided graph represents a(n)

11–69

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

decreasing-cost industries.

Test Bank: II

Topic:

Long-Run Supply Curves

142.

The provided graph depicts long-run supply for

143.

The provided graph depicts a situation where, if the market demand for the product increases, the

prices of the resources used by the firms in the industry would

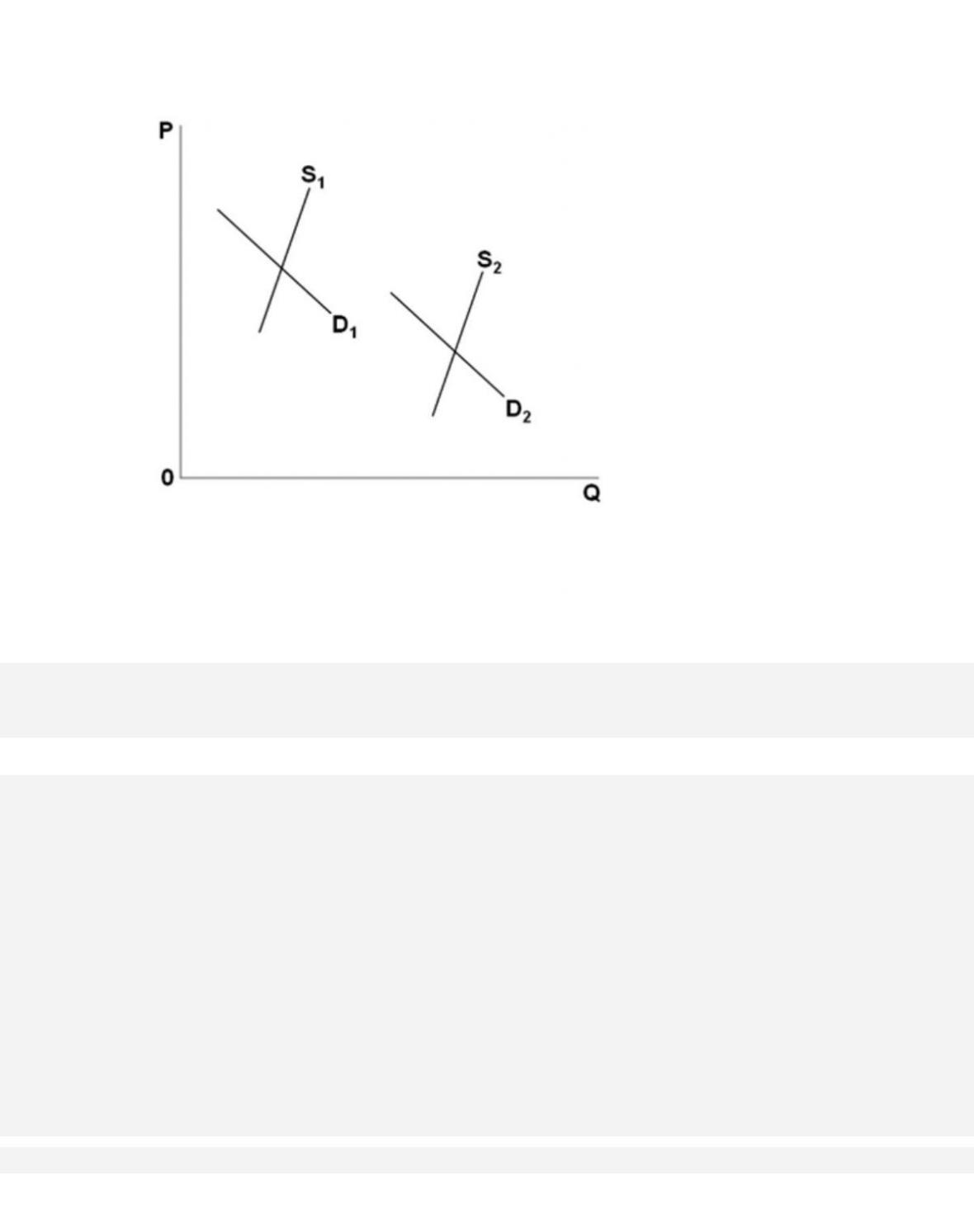

144.

The industry represented by the accompanying graph must be one where

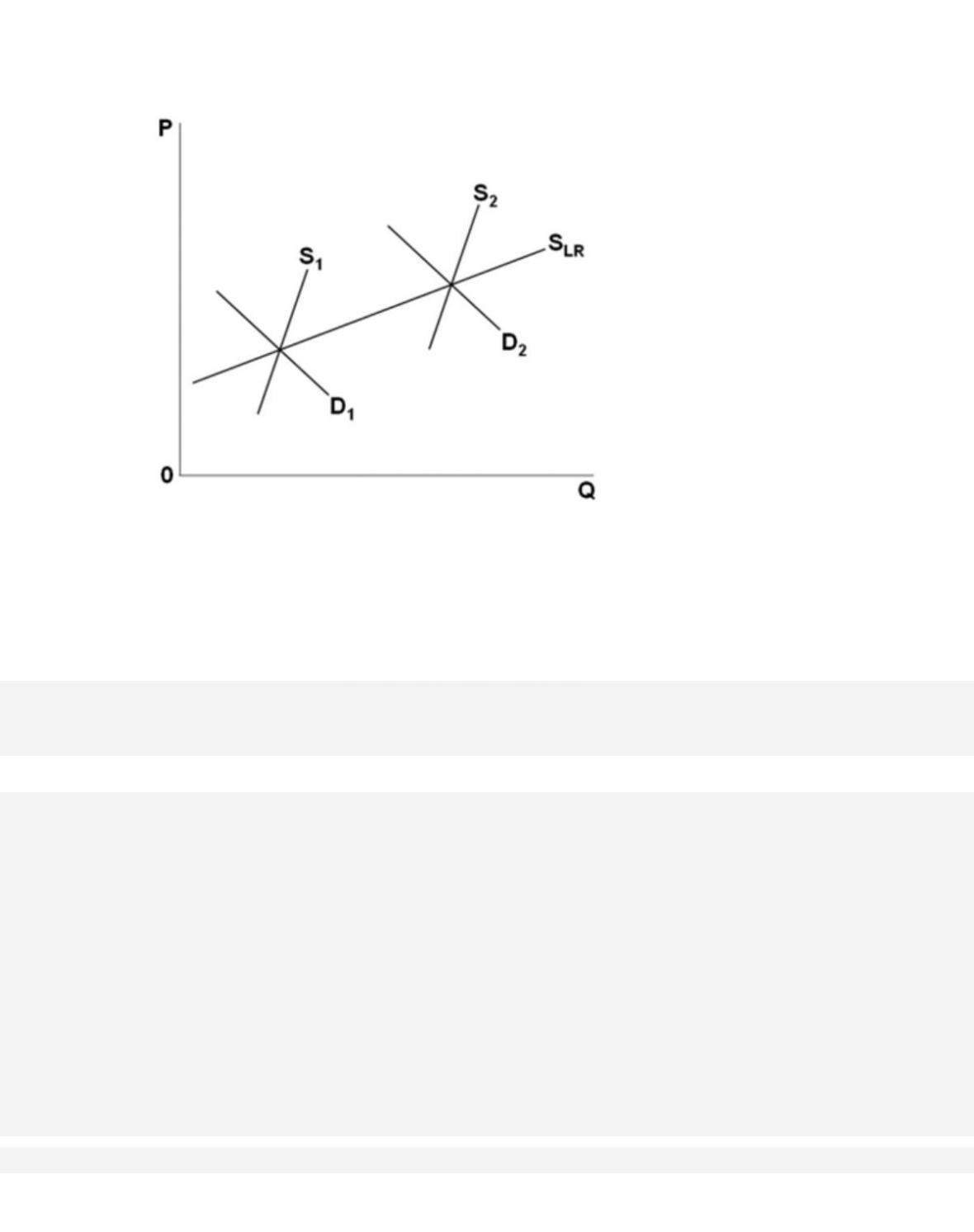

145.

The industry indicated by the accompanying graphs would be a(n)

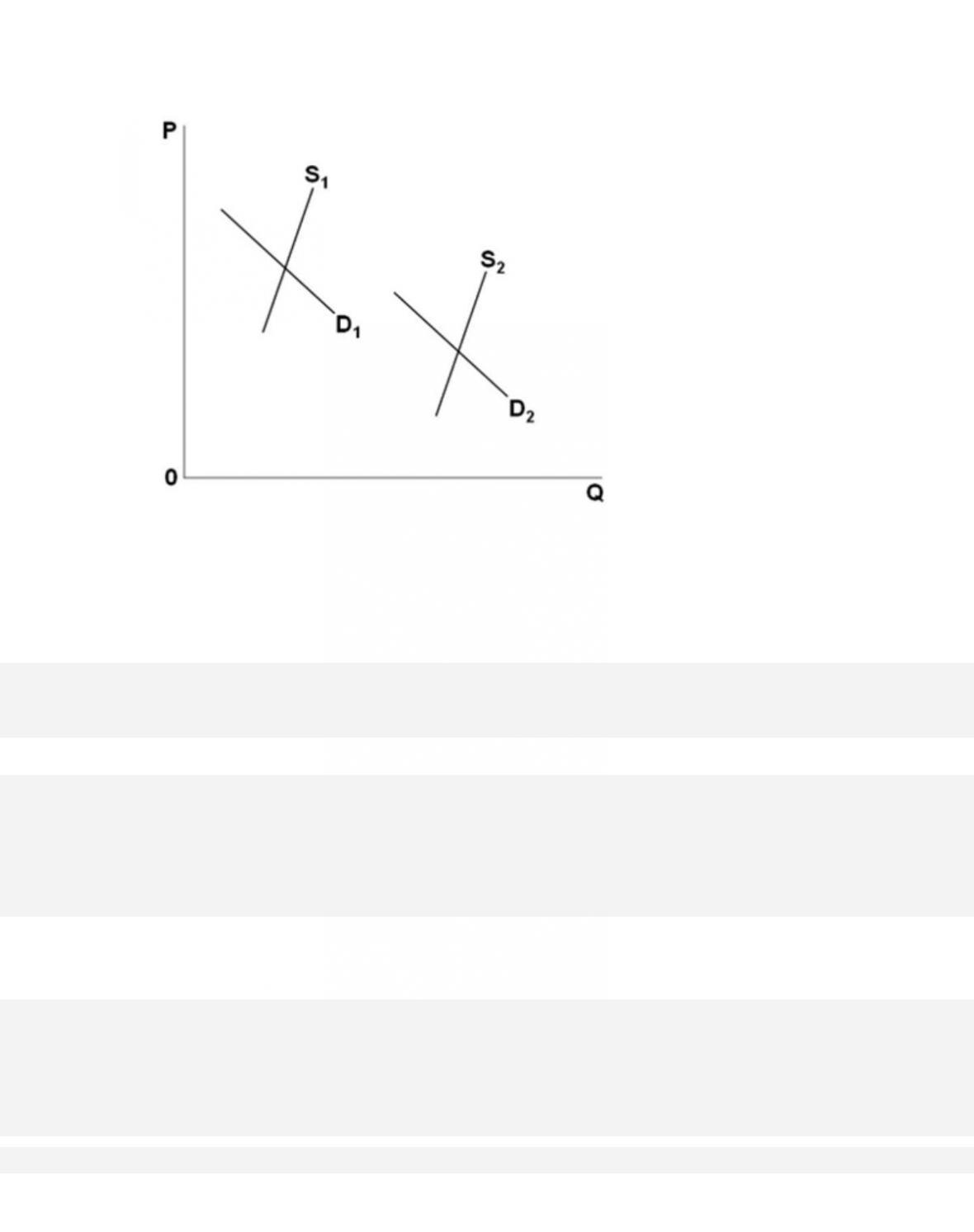

146.

The industry represented by the accompanying graph must be one where

147. Productive efficiency refers to

11–74

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

AACSB: Knowledge Application

Ac c e s s ib i l i t y:

Keyboard Navigation

Blooms: Understand

Diffi culty :

02 Medium

Learning Objective: 11-04 Show how long-run equilibrium in pure competition produces an

efficient allocation of resources.

Test Bank: II

Topic:

Pure Competition and Efficiency

148. An industry is producing at the least-cost rate of production when

149. Allocative efficiency occurs when the

150. Allocative efficiency means that

11–75

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

B. society’s scarce resources are used to produce products that align with consumer

preferences.

C. the product is sold at a price equal to the average cost of producing it.

D. the marginal benefit of the product exceeds its marginal cost.

151. In long-run equilibrium, a purely competitive firm will operate where price is

152. Which would indicate that a firm is operating under conditions of pure competition and is

being productively efficient?

11–76

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

Test Bank: II

Topic:

Pure Competition and Efficiency

153. Which of the following statements about a competitive firm is correct?

154. In long-run equilibrium under pure competition, all firms will produce at minimum

155. In the context of analyzing economic efficiency, we can interpret the market demand curve

to be showing

11–77

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

C. the marginal benefit that consumers place on each unit of the product.

D. the average variable cost of producing the product.

156. In the context of analyzing economic efficiency, we can interpret the market supply curve to

be showing

157. Pure competition produces a socially optimal allocation of resources in the long run

because

158. When a purely competitive firm is in long-run equilibrium, it is said to achieve allocative

efficiency because

159. Which is true of a purely competitive firm in long-run equilibrium?

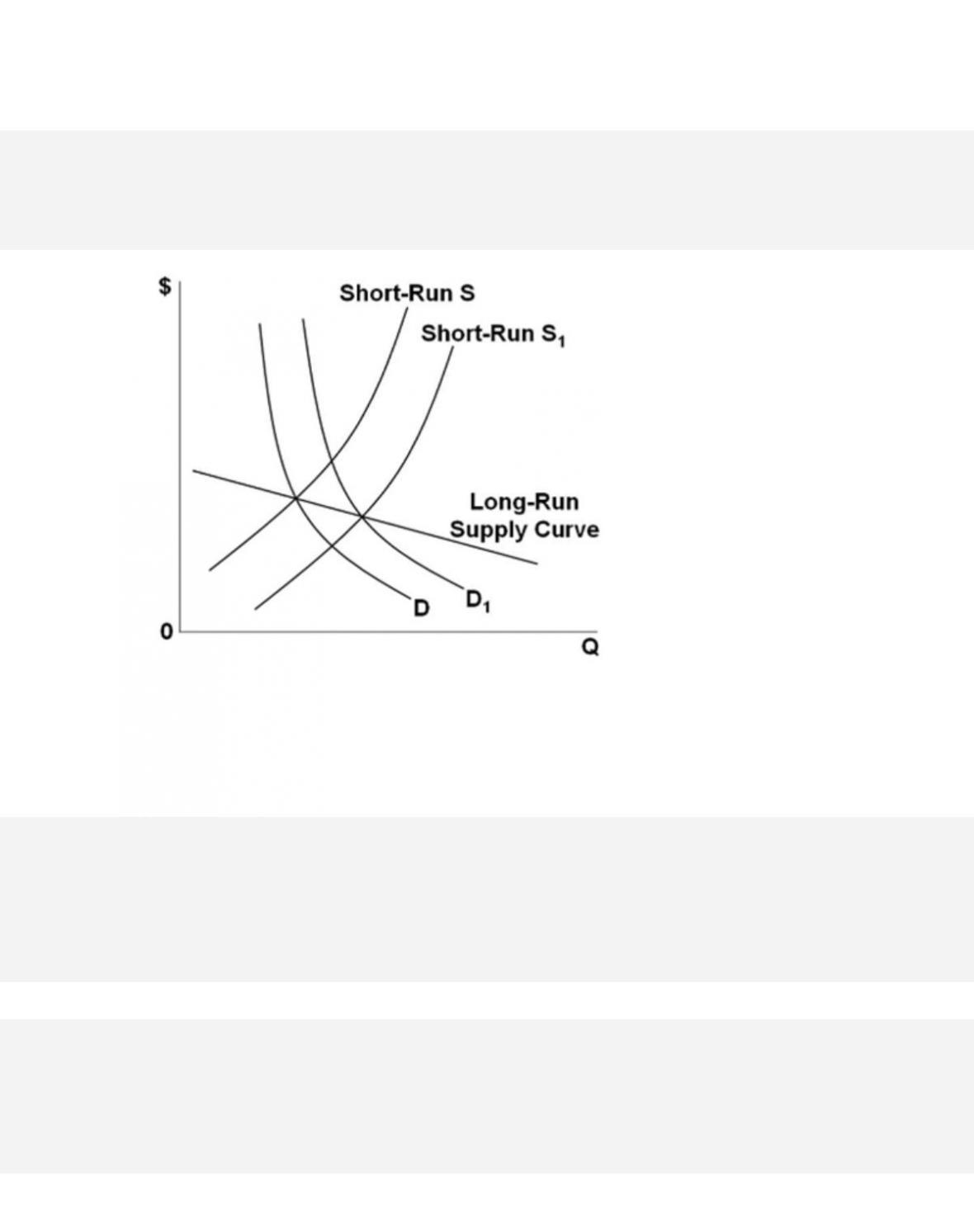

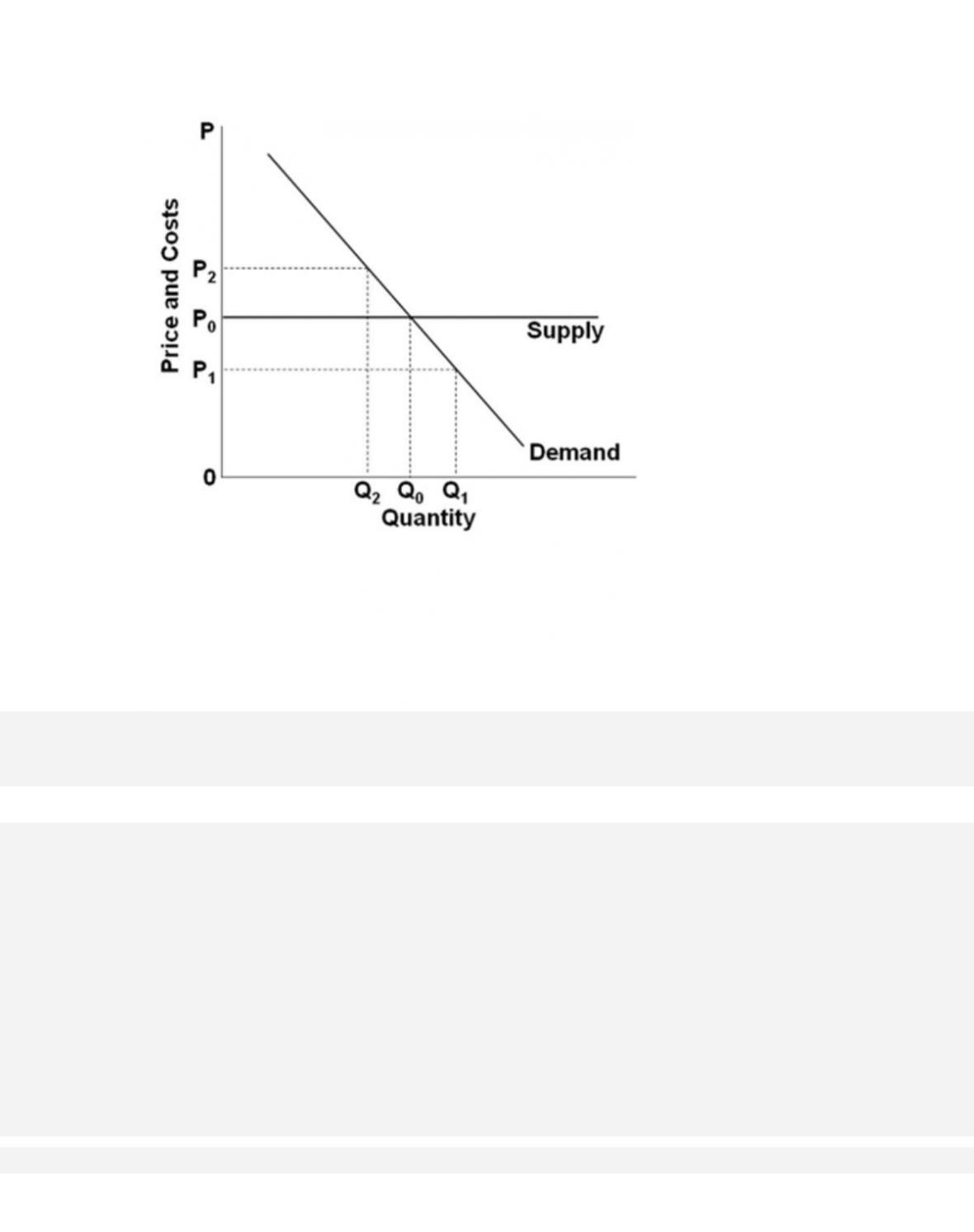

160. Resources are efficiently allocated when production occurs at that output at which

11–79

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

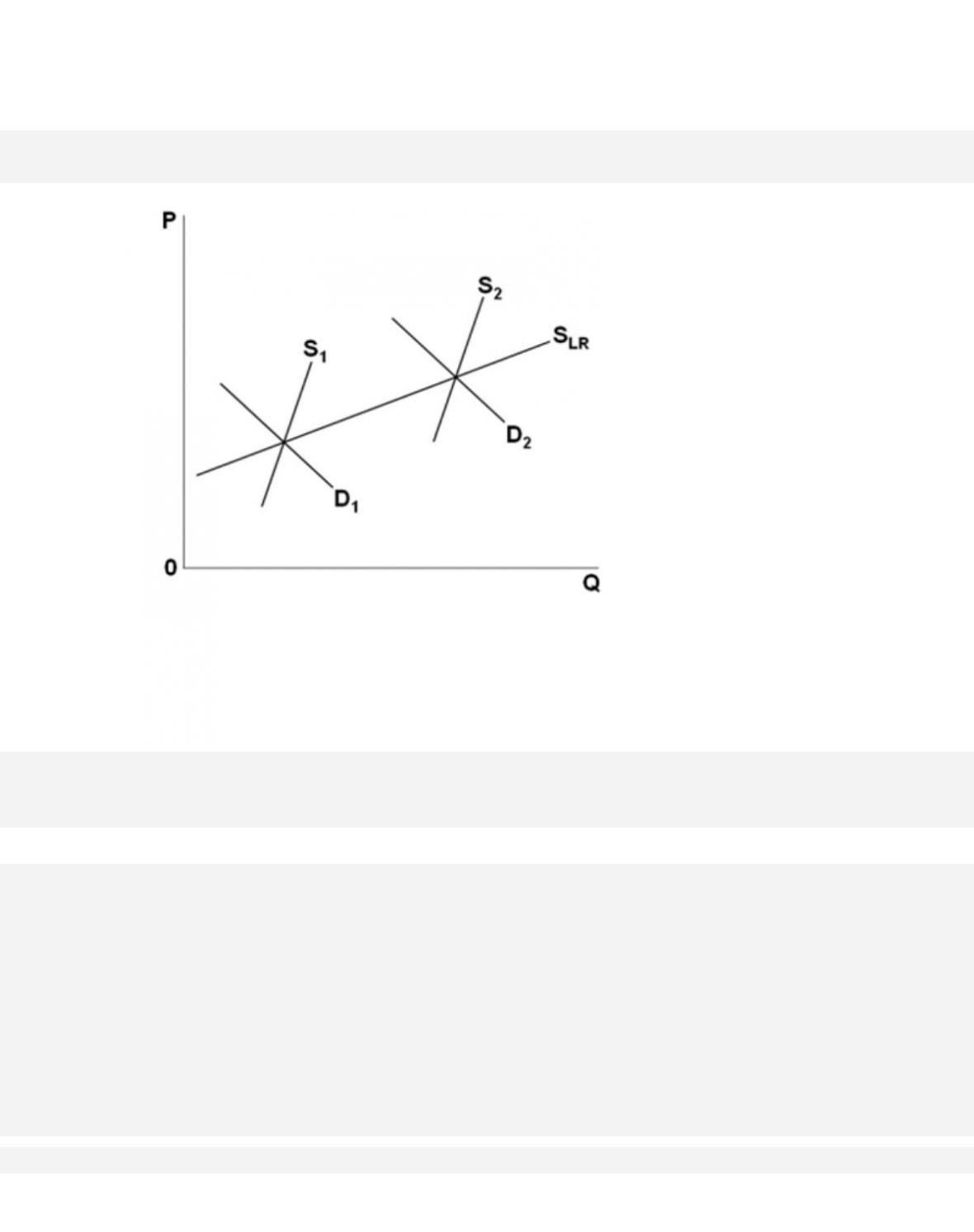

Diffi culty :

02 Medium

Learning Objective: 11-04 Show how long-run equilibrium in pure competition produces an

efficient allocation of resources.

Test Bank: II

Topic:

Pure Competition and Efficiency

161. Resources are efficiently allocated when production occurs at that output level where price

162. When a purely competitive firm is in long-run equilibrium, price is equal to

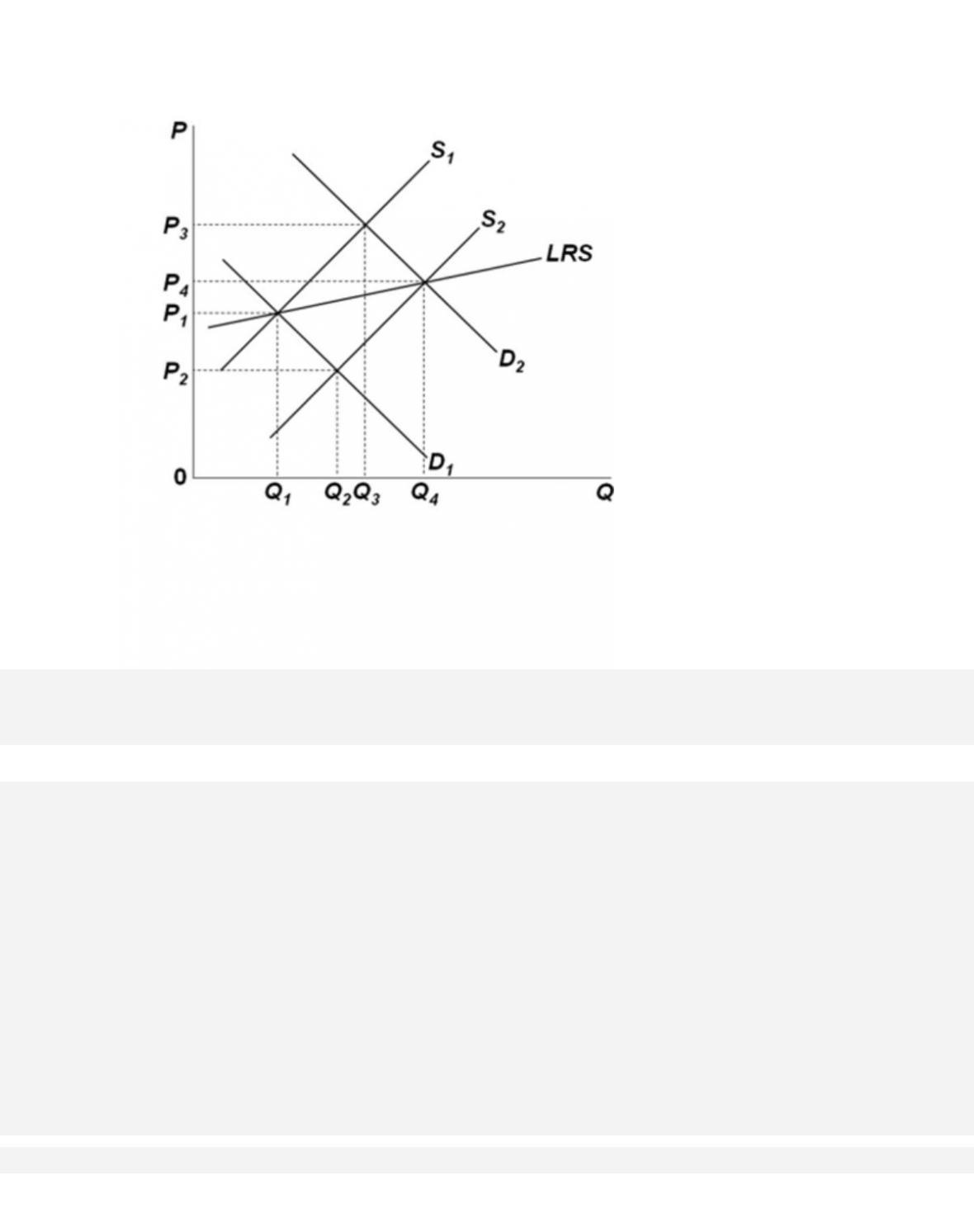

163.

The accompanying graph shows the long-run supply and demand curves in a purely competitive

market. The curves suggest that this industry is