Chapter 11 Pure Competition in the Long Run Answer Key

Multiple Choice Questions

1. Which of the following distinguishes the short run from the long run in pure competition?

2. The primary force encouraging the entry of new firms into a purely competitive industry is

3. In a purely competitive industry,

11-2

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

Blooms: Understand

Diff icult y:

02 Medium

Learning Objective: 11–01 Explain how the long run differs from the short run in pure

competition.

Test Bank: I

Topic:

The Long Run in Pure Competition

4. Balin’s Burger Barn operates in a perfectly competitive market. Balin’s is currently earning

economic profits of $20,000 per year. Based on this information, we can conclude that

5. Suppose a firm in a purely competitive market discovers that the price of its product is above

its minimum AVC point but everywhere below ATC. Given this, the firm

6. Karlee’s Kreations sells handbags in a purely competitive market. Karlee’s is currently

breaking even. Based on this information, we can conclude that Karlee’s Kreations

11-3

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

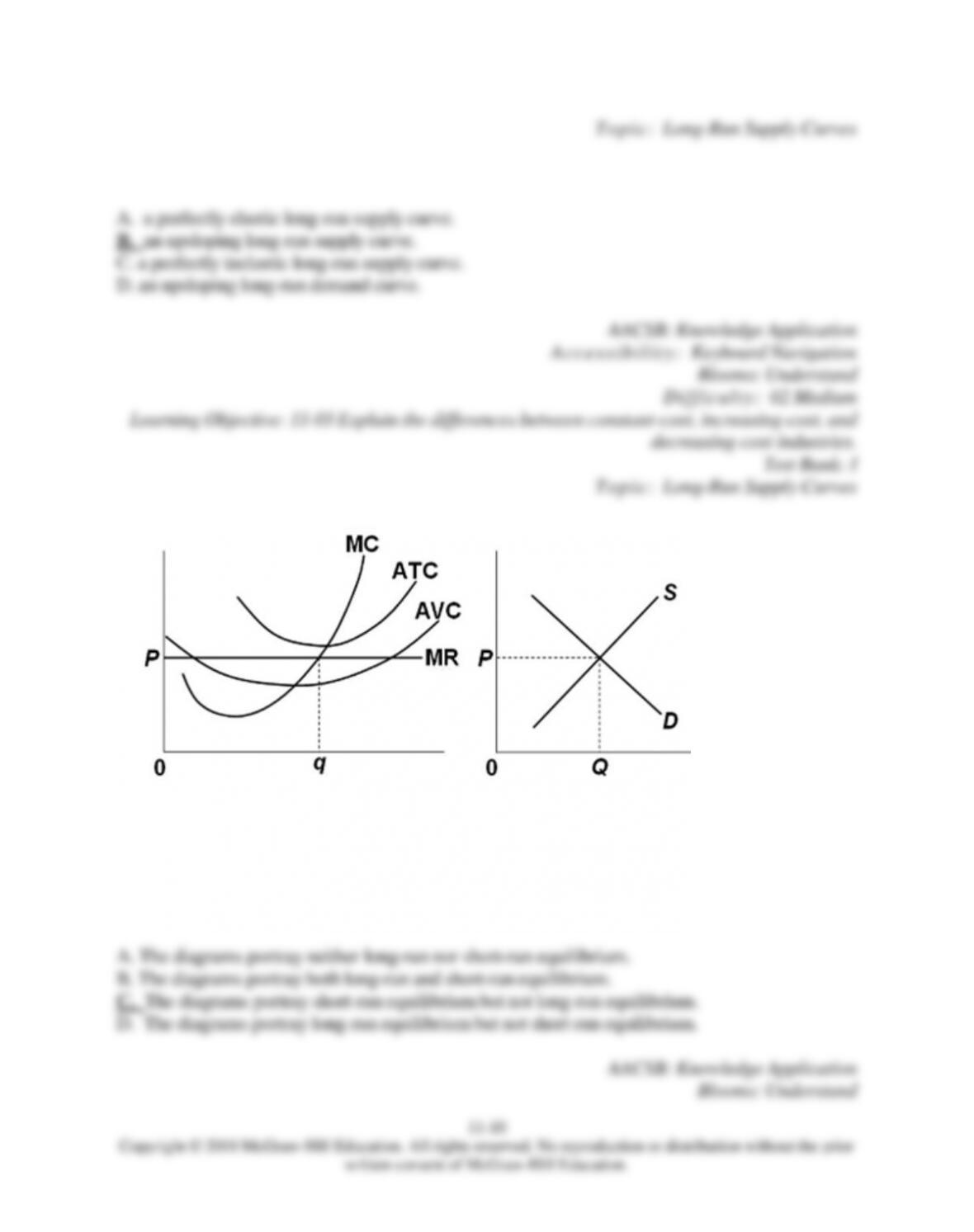

A. must be operating in long–run equilibrium.

B. will leave this market in the long run because no economic profits are being earned.

C. will continue operating in this market only if the market price rises.

D. may be operating in either short-run or long–run equilibrium.

AACSB: Knowledge Application

Ac c e s s i b ili t y :

Keyboard Navigation

Blooms: Understand

Diff icult y:

02 Medium

Learning Objective: 11–01 Explain how the long run differs from the short run in pure

competition.

Test Bank: I

Topic:

The Long Run in Pure Competition

7. Which of the following is true concerning purely competitive industries?

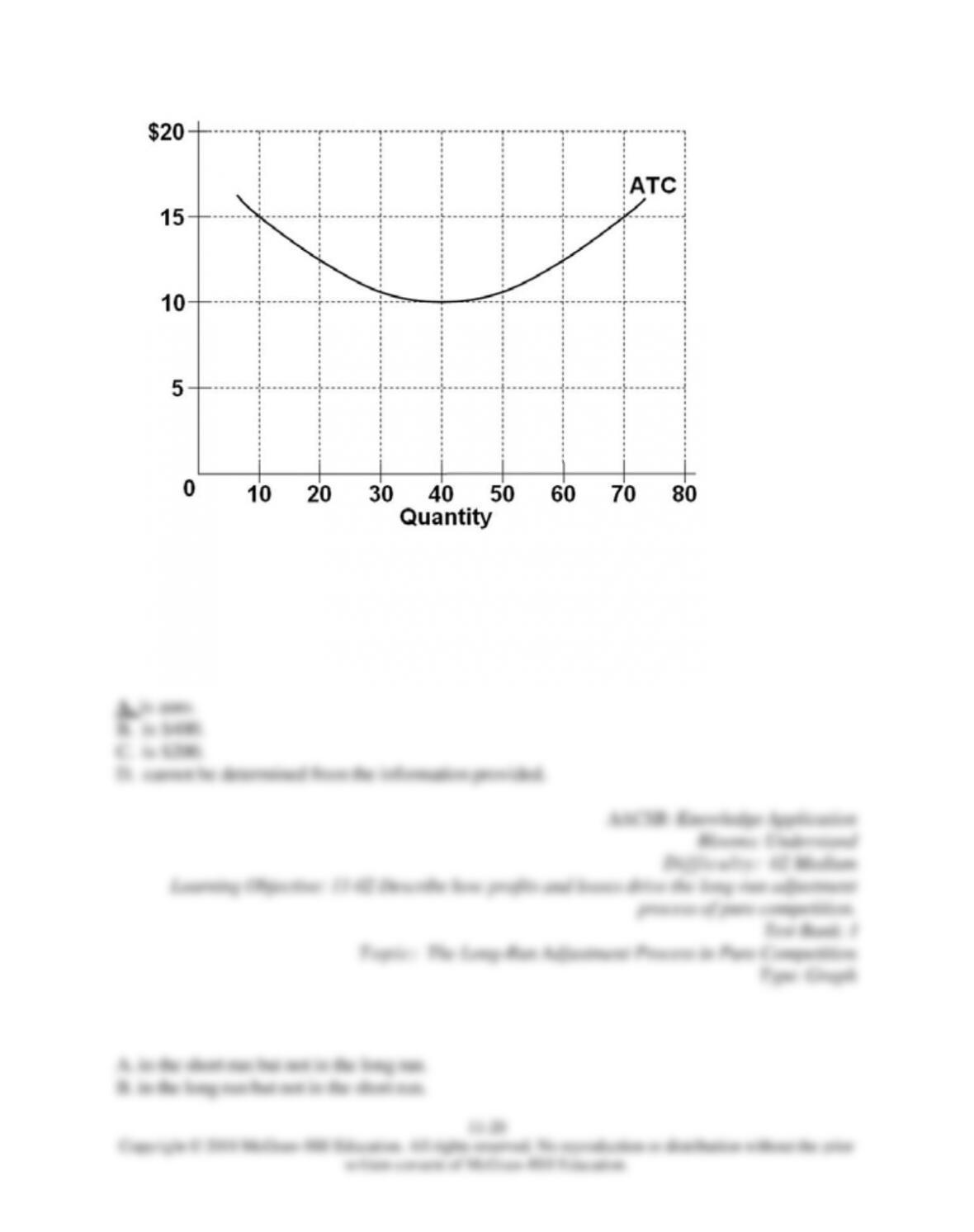

8. If a purely competitive firm is producing at the MR = MC output level and earning an

economic profit, then

11-4

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

Learning Objective: 11–02 Describe how profits and losses drive the long-run adjustment

process of pure competition.

Test Bank: I

Topic:

The Long-Run Adjustment Process in Pure Competition

9. Long-run adjustments in purely competitive markets primarily take the form of

10. Long-run competitive equilibrium

11. Suppose that Betty’s Beads is a typical firm operating in a perfectly competitive market.

Currently Betty’s MR = $15, MC = $12, ATC = $10, and AVC = $8. Based on this information,

we can conclude that

11-5

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

D. potential new firms will be discouraged by Betty’s struggles and not enter the market.

AACSB: Knowledge Application

Ac c e s s i b ili t y :

Keyboard Navigation

Blooms: Understand

Diff icult y:

02 Medium

Learning Objective: 11–02 Describe how profits and losses drive the long-run adjustment

process of pure competition.

Test Bank: I

Topic:

The Long-Run Adjustment Process in Pure Competition

12. We would expect an industry to expand if firms in that industry are

13. Which of the following statements is correct?

14. Suppose a purely competitive, increasing-cost industry is in long-run equilibrium. Now

assume that a decrease in consumer demand occurs. After all resulting adjustments have been

completed, the new equilibrium price

15. Suppose the market for corn is a purely competitive, constant-cost industry that is in long-run

equilibrium. Now assume that an increase in consumer demand occurs. After all resulting

adjustments have been completed, the new equilibrium price will be

16. Which of the following statements is correct?

11-7

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

B. The long-run supply curve for a purely competitive increasing-cost industry will be perfectly

elastic.

C. The long-run supply curve for a purely competitive industry will be less elastic than the

industry’s short-run supply curve.

D. The long-run supply curve for a purely competitive decreasing-cost industry will be

upsloping.

AACSB: Knowledge Application

Ac c e s s i b ili t y :

Keyboard Navigation

Blooms: Understand

Diff icult y:

02 Medium

Learning Objective: 11–03 Explain the differences between constant-cost, increasing-cost, and

decreasing-cost industries.

Test Bank: I

Topic:

Long-Run Supply Curves

17. A constant-cost industry is one in which

18. Which of the following will not hold true for a competitive firm in long-run equilibrium?

11-8

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

Learning Objective: 11–01 Explain how the long run differs from the short run in pure

competition.

Test Bank: I

Topic:

The Long Run in Pure Competition

19. Assume a purely competitive increasing-cost industry is initially in long-run equilibrium and

that an increase in consumer demand occurs. After all economic adjustments have been

completed, product price will be

20. Assume a purely competitive, increasing-cost industry is in long–run equilibrium. If a decline

in demand occurs, firms will

21. When a purely competitive firm is in long-run equilibrium,

11-9

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

C. total revenue exceeds total cost.

D. minimum average total cost is less than the product price.

AACSB: Knowledge Application

Ac c e s s i b ili t y :

Keyboard Navigation

Blooms: Understand

Diff icult y:

02 Medium

Learning Objective: 11–01 Explain how the long run differs from the short run in pure

competition.

Learning Objective: 11–04 Show how long-run equilibrium in pure competition

produces an efficient allocation of resources.

Test Bank: I

Topic:

Pure Competition and Efficiency

Topic:

The Long Run in Pure Competition

22. A purely competitive firm

23. A constant-cost industry is one in which

11–10

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

Topic:

Long-Run Supply Curves

24. An increasing-cost industry is associated with

25.

Refer to the diagrams, which pertain to a purely competitive firm producing output q and the

industry in which it operates. Which of the following is correct?

11–11

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

Diff icult y:

02 Medium

Learning Objective: 11–01 Explain how the long run differs from the short run in pure

competition.

Test Bank: I

Topic:

The Long Run in Pure Competition

Type: Graph

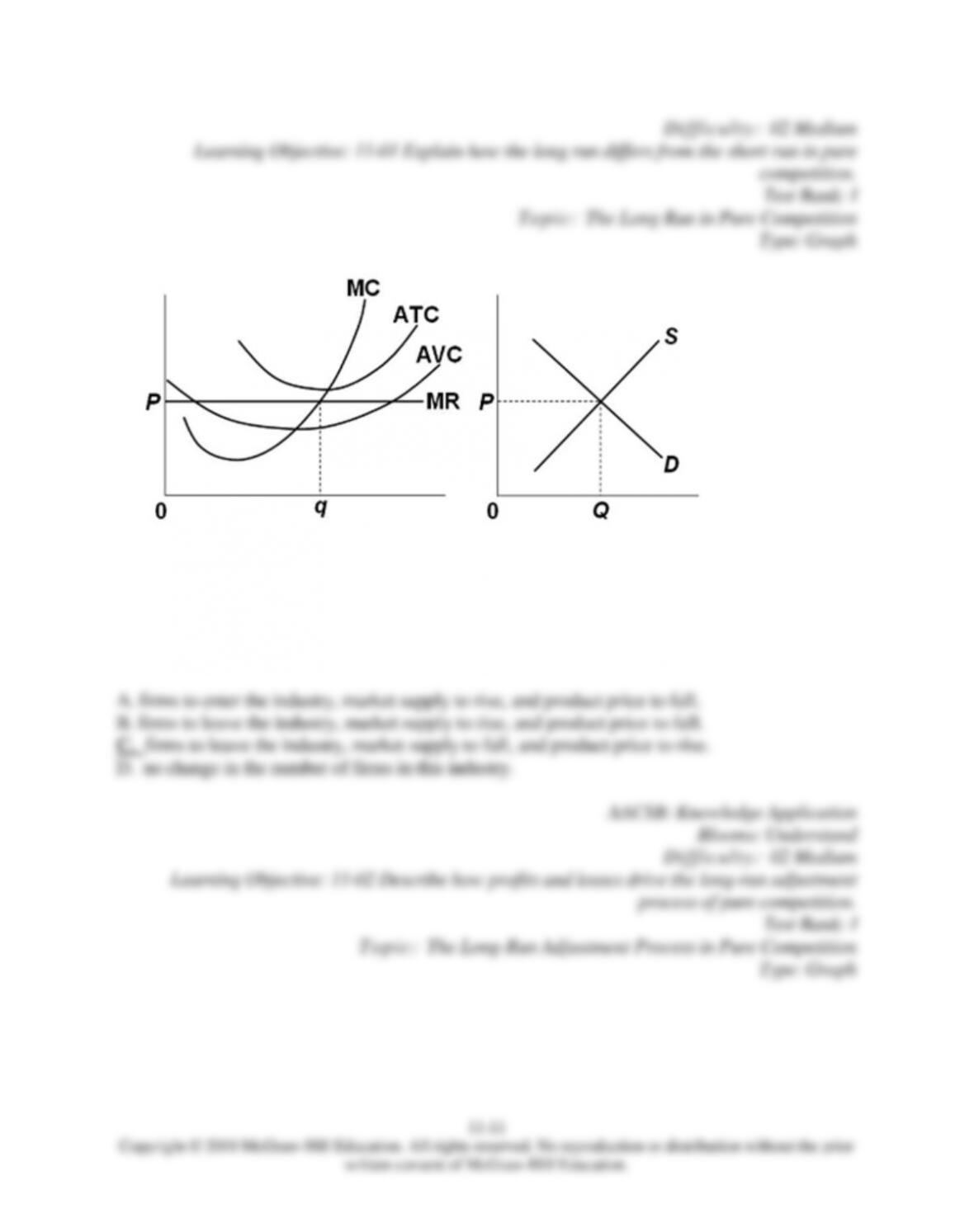

26.

Refer to the diagrams, which pertain to a purely competitive firm producing output q and the

industry in which it operates. In the long run we should expect

27.

Refer to the diagrams, which pertain to a purely competitive firm producing output q and the

industry in which it operates. The predicted long-run adjustments in this industry might be offset

by

28. Assume a purely competitive firm is maximizing profit at some output at which long-run

average total cost is at a minimum. Then

11–13

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

Diff icult y:

02 Medium

Learning Objective: 11–02 Describe how profits and losses drive the long-run adjustment

process of pure competition.

Test Bank: I

Topic:

The Long-Run Adjustment Process in Pure Competition

29. An increasing-cost industry is the result of

30. A purely competitive firm is precluded from making economic profits in the long run because

31. If a purely competitive constant-cost industry is realizing economic profits, we can expect

industry supply to

11–14

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

D. increase, output to decrease, price to decrease, and profits to decrease.

AACSB: Knowledge Application

Ac c e s s i b ili t y :

Keyboard Navigation

Blooms: Understand

Diff icult y:

02 Medium

Learning Objective: 11–02 Describe how profits and losses drive the long-run adjustment

process of pure competition.

Test Bank: I

Topic:

The Long-Run Adjustment Process in Pure Competition

32. Assume that a decline in consumer demand occurs in a purely competitive industry that is

initially in long-run equilibrium. We can

33. Under what conditions would an increase in demand lead to a lower long-run equilibrium

price?

11–15

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

Topic:

Long-Run Supply Curves

34. In a decreasing-cost industry,

35. A decreasing-cost industry is one in which

36. When LCD televisions first came on the market, they sold for at least $1,000, and some for

much more. Now many units can be purchased for under $400. These facts imply that

11–16

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

Ac c e s s i b ili t y :

Keyboard Navigation

Blooms: Understand

Diff icult y:

02 Medium

Learning Objective: 11–03 Explain the differences between constant-cost, increasing-cost, and

decreasing-cost industries.

Test Bank: I

Topic:

Long-Run Supply Curves

37. Suppose that an industry‘s long-run supply curve is downsloping. This suggests that

38. Suppose an increase in product demand occurs in a decreasing-cost industry. As a result,

39. Purely competitive industry X has constant costs and its product is an inferior good. The

industry is currently in long-run equilibrium. The economy now goes into a recession and

average incomes decline. The result will be

11–17

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

A. an increase in output and in the price of the product.

B. an increase in output, but not in the price, of the product.

C. a decrease in the output, but not in the price, of the product.

D. a decrease in output and in the price of the product.

AACSB: Knowledge Application

Ac c e s s i b ili t y :

Keyboard Navigation

Blooms: Understand

Diff icult y:

02 Medium

Learning Objective: 11–03 Explain the differences between constant-cost, increasing-cost, and

decreasing-cost industries.

Test Bank: I

Topic:

Long-Run Supply Curves

40. Suppose losses cause industry X to contract and, as a result, the prices of relevant inputs

decline. Industry X is

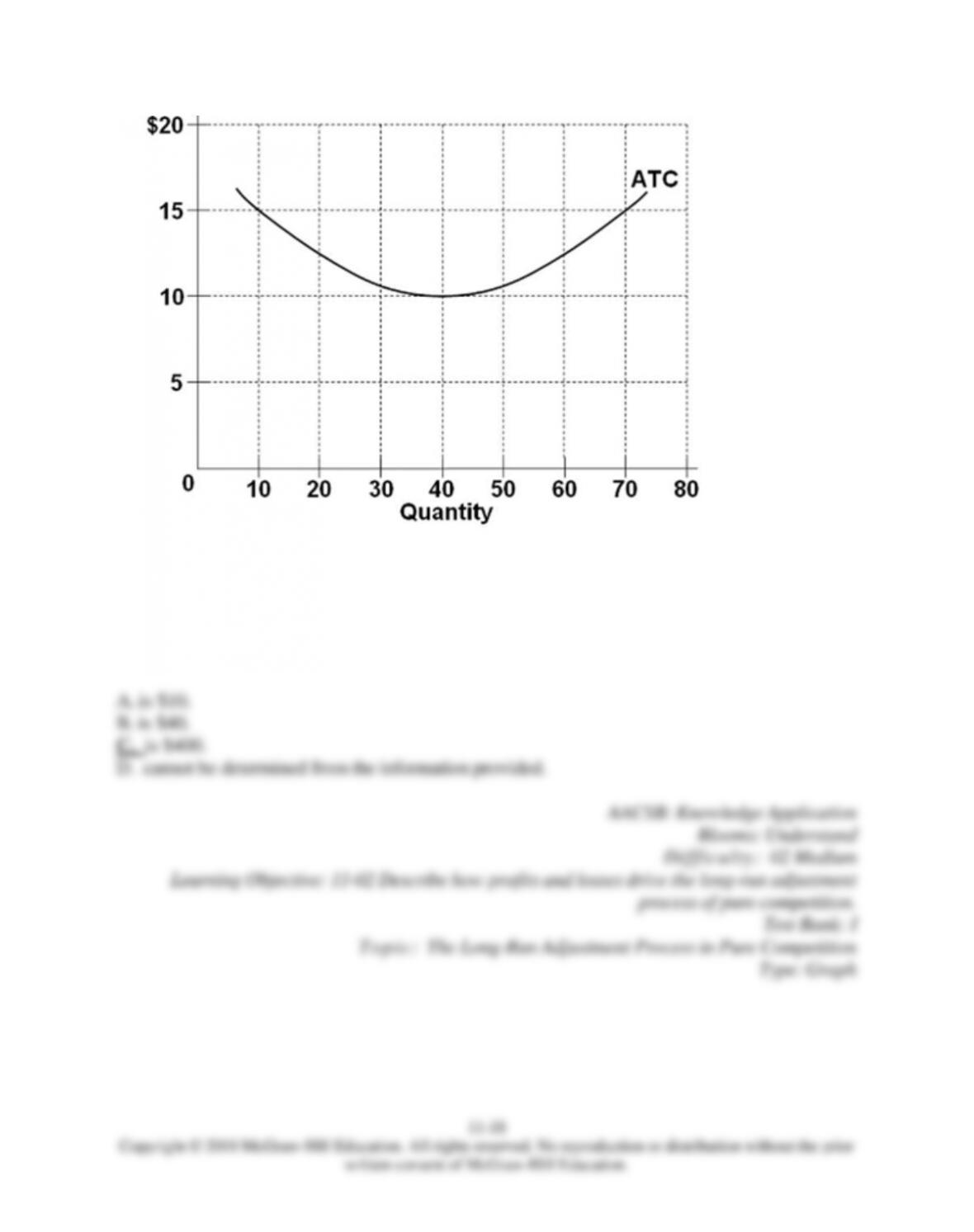

41.

The diagram shows the average total cost curve for a purely competitive firm. At the long-run

equilibrium level of output, this firm‘s total revenue

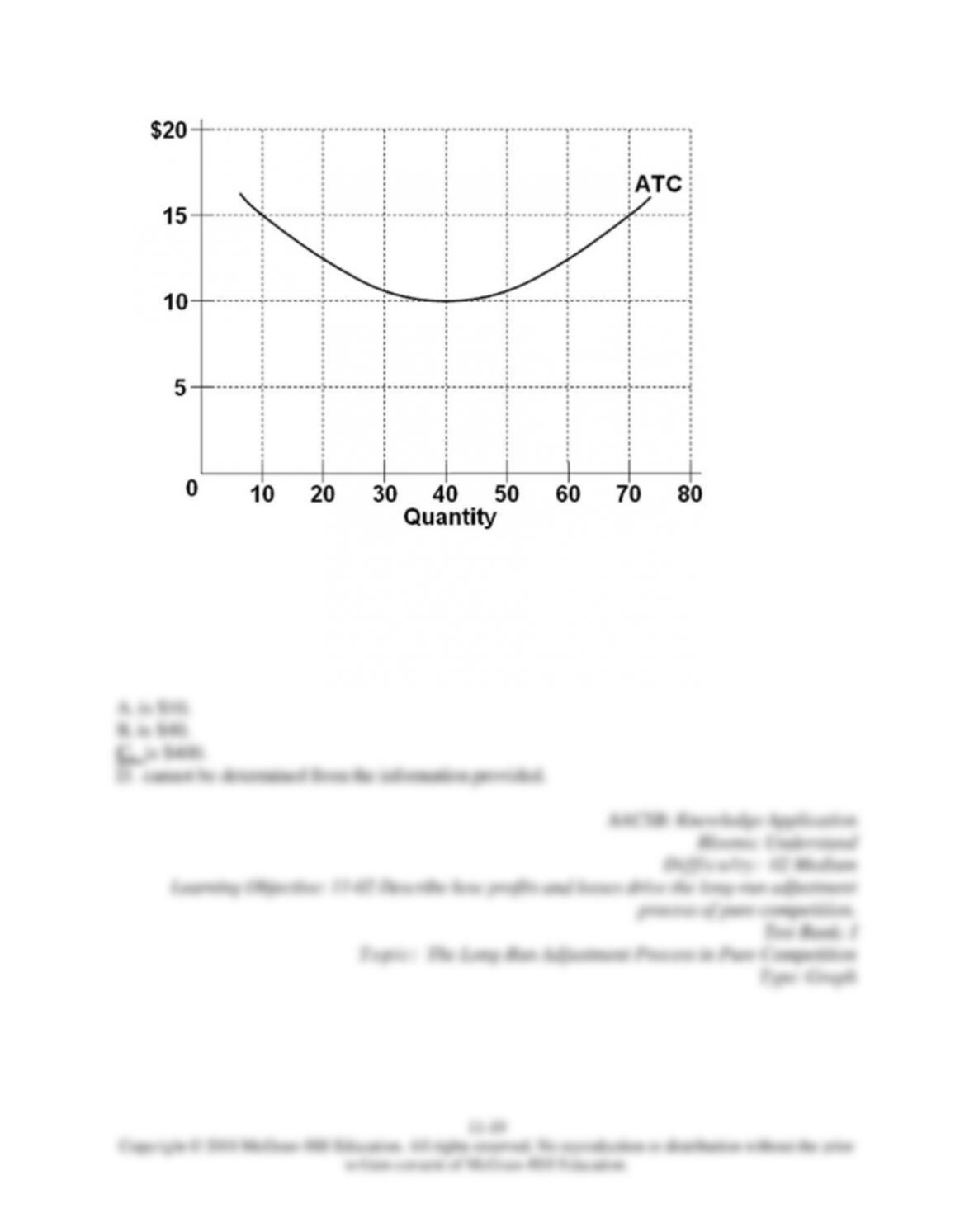

42.

The diagram shows the average total cost curve for a purely competitive firm. At the long-run

equilibrium level of output, this firm‘s total cost

43.

The diagram shows the average total cost curve for a purely competitive firm. At the long-run

equilibrium level of output, this firm‘s economic profit

44. The MR = MC rule applies