10-158

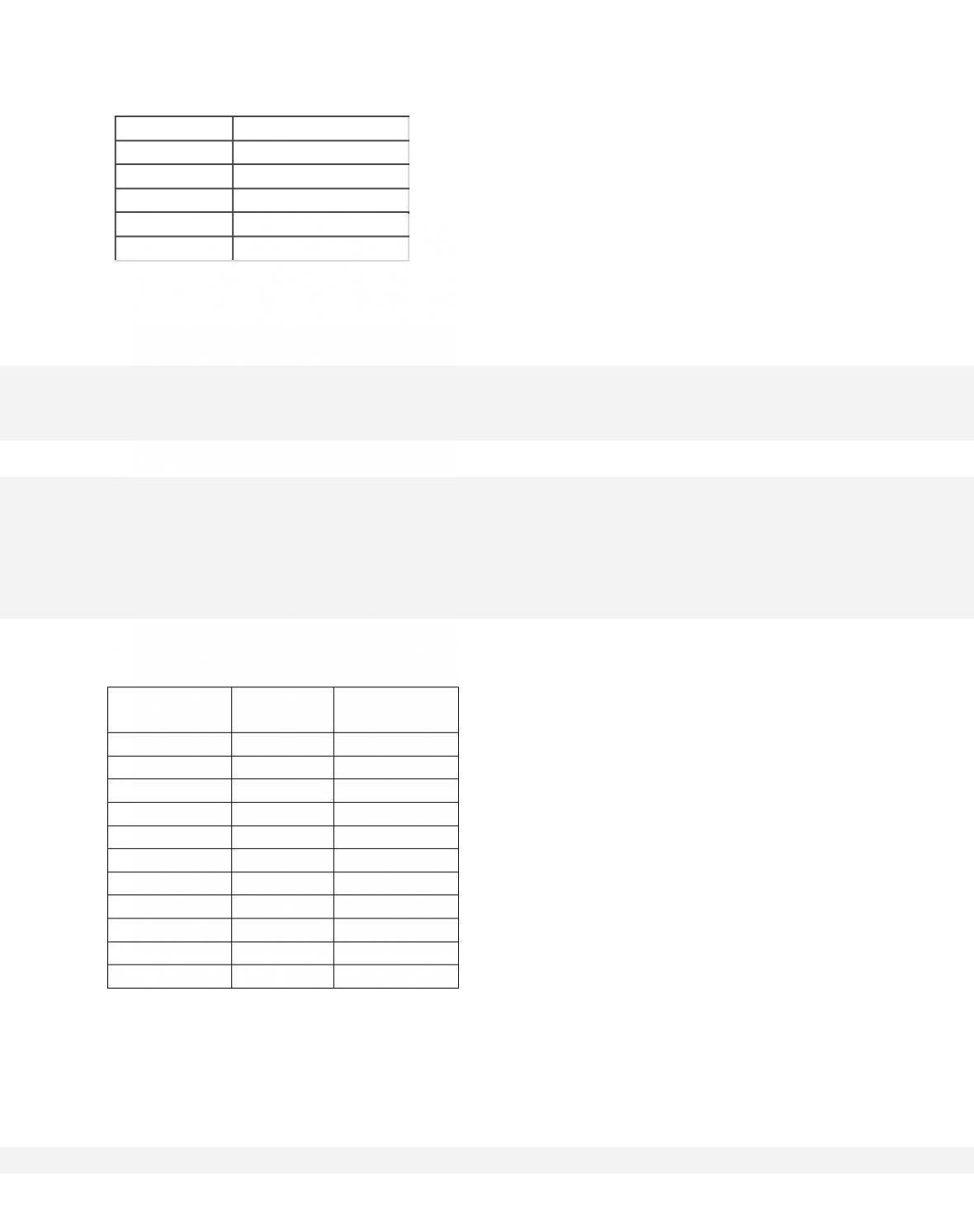

45

5,500

60

5,125

75

4,500

95

4,200

120

3,600

150

2,400

Based on all these data, the equilibrium price of the product in the market will be

264.

Total Product

Total

Fixed Cost

Total

Variable Cost

0

$150

$ 0

1

150

50

2

150

75

3

150

105

4

150

145

5

150

200

6

150

270

7

150

360

8

150

475

9

150

620

10

150

800

The first table shows cost data for a single firm. Now suppose that there are 600 identical firms

in this industry, each with the same cost data.

Suppose, too, that the demand curve for this

industry is as shown in the second table.

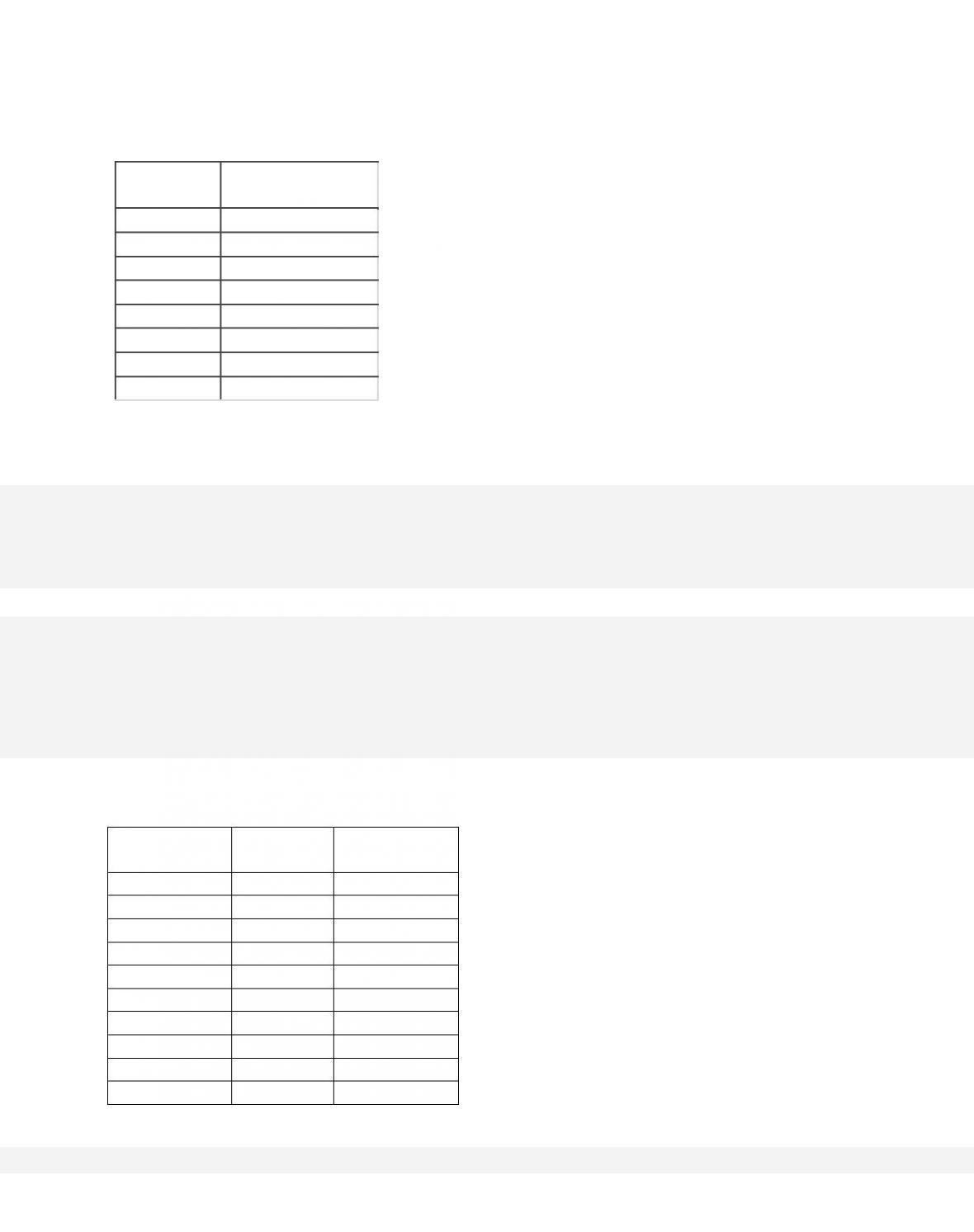

10-159

Price

Quantity

Demanded

$20

6,800

30

5,975

45

5,500

60

5,125

75

4,500

95

4,200

120

3,600

150

2,400

When the market is in equilibrium, each of the firms will be producing

265.

Total Product

Total

Fixed Cost

Total

Variable Cost

0

$150

$ 0

1

150

50

2

150

75

3

150

105

4

150

145

5

150

200

6

150

270

7

150

360

8

150

475

9

150

620

10-160

10

150

800

The first table shows cost data for a single firm. Now suppose that there are 600 identical firms

in this industry, each with the same cost data.

Suppose, too, that the demand curve for this

industry is as shown in the second table.

Price

Quantity

Demanded

$20

6,800

30

5,975

45

5,500

60

5,125

75

4,500

95

4,200

120

3,600

150

2,400

At equilibrium, each firm will realize

266.

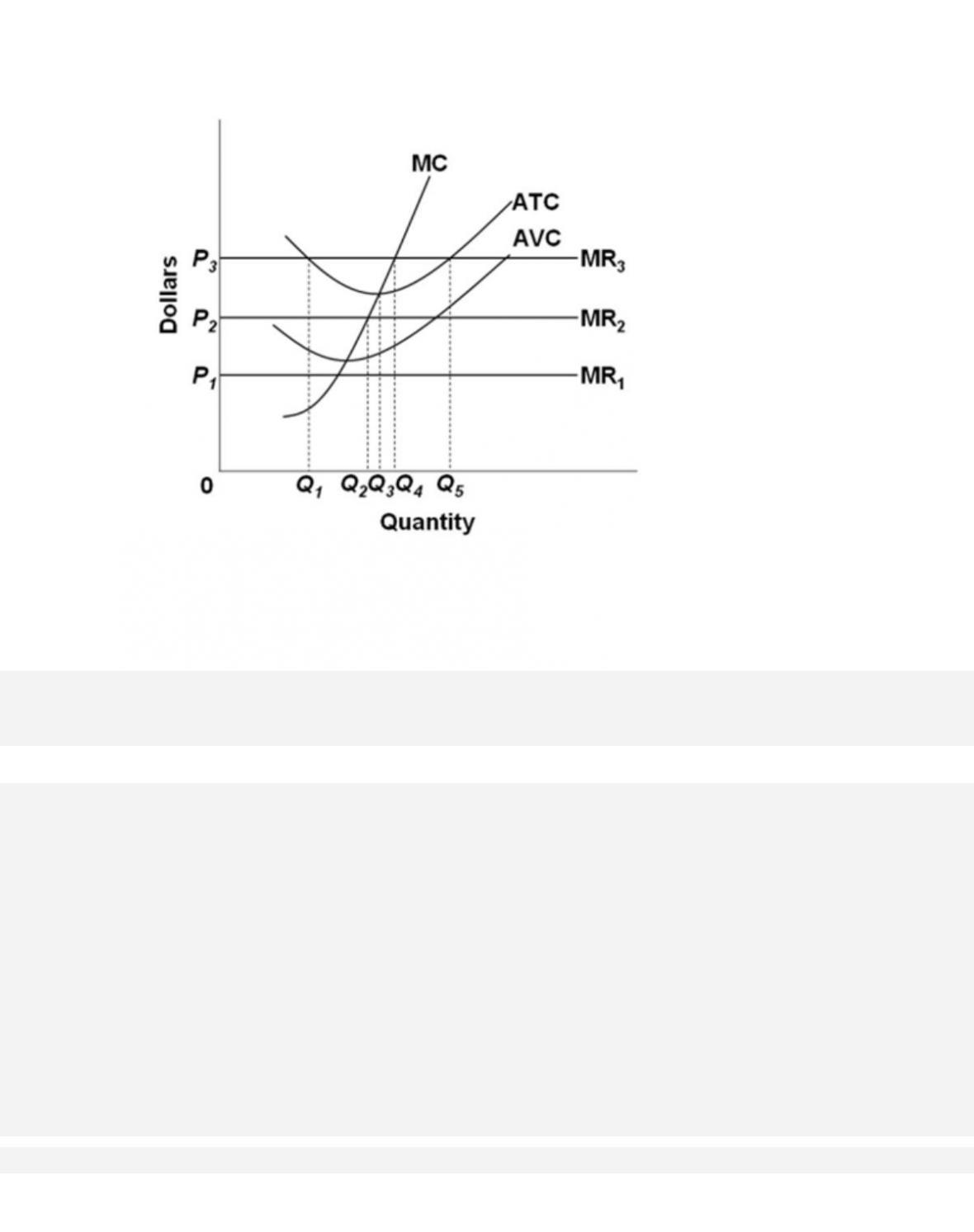

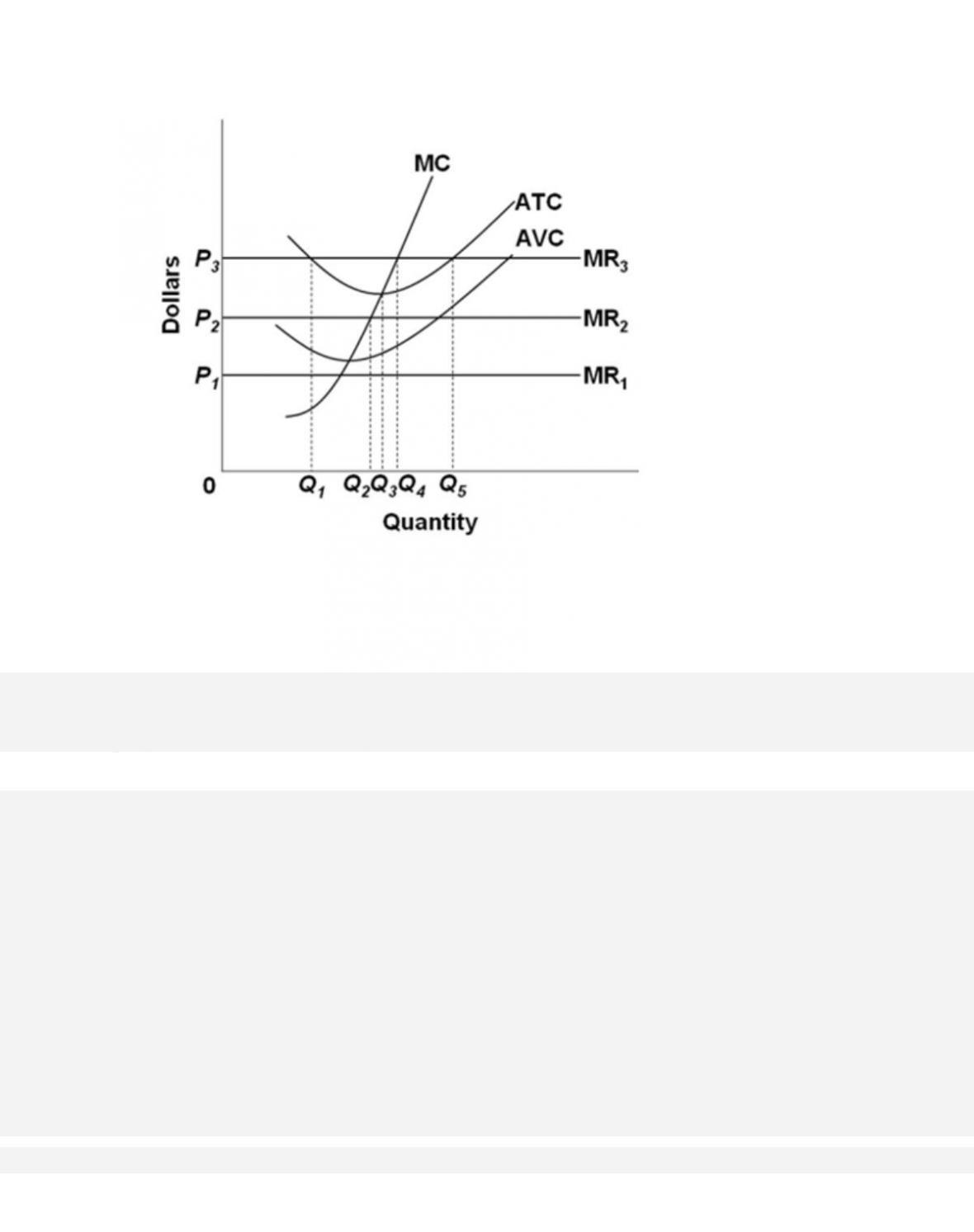

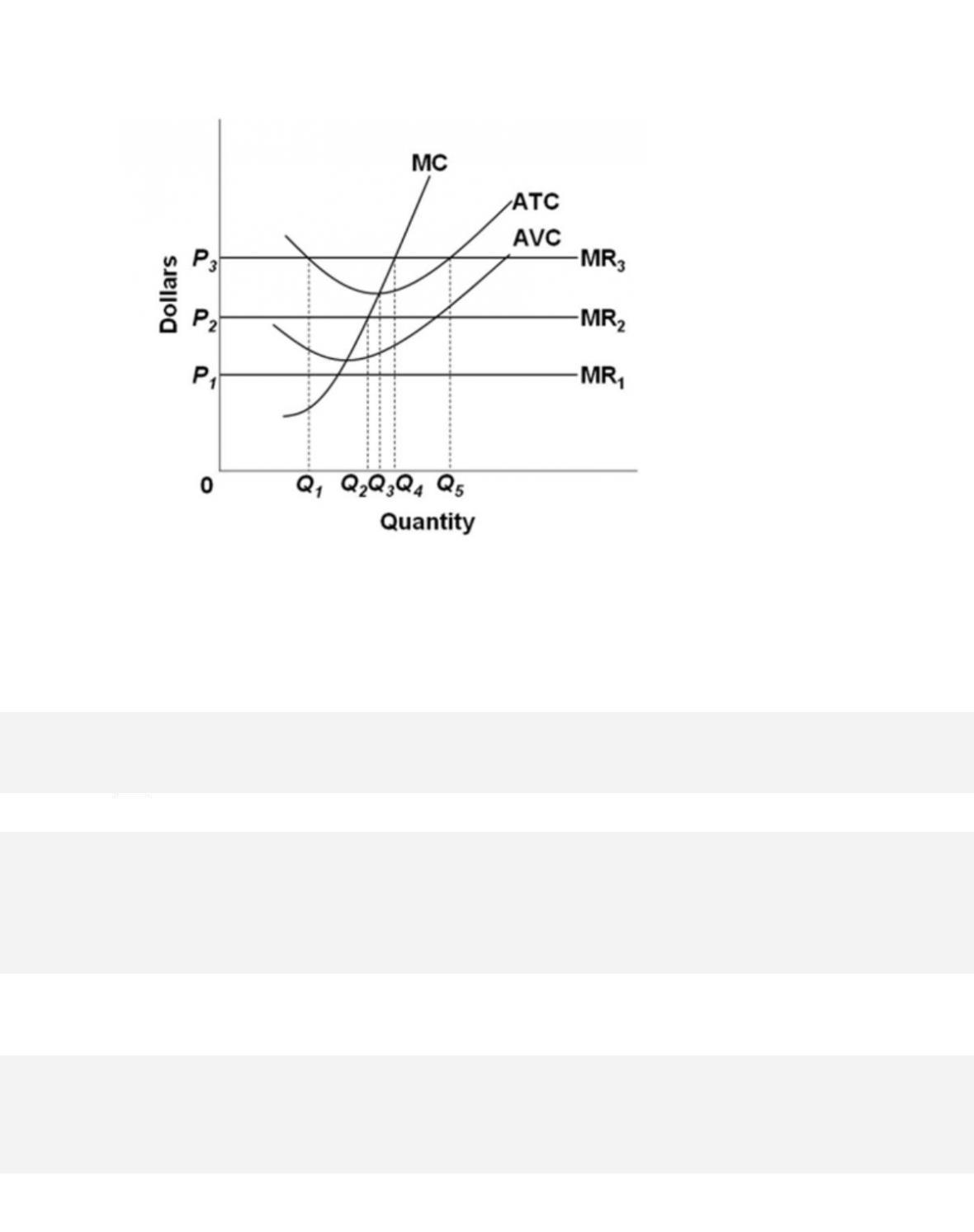

The firm represented in this diagram, which gives short-run data, is selling under conditions of

267.

The provided graph gives short-run data for a firm. If the product price is P2, the firm will

268.

The provided graph gives short-run data for a firm. Which of the following statements is

correct?

269. In the short run, fixed costs for a profitable competitive firm are

10-164

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

D. irrelevant in determining the optimal level of output.

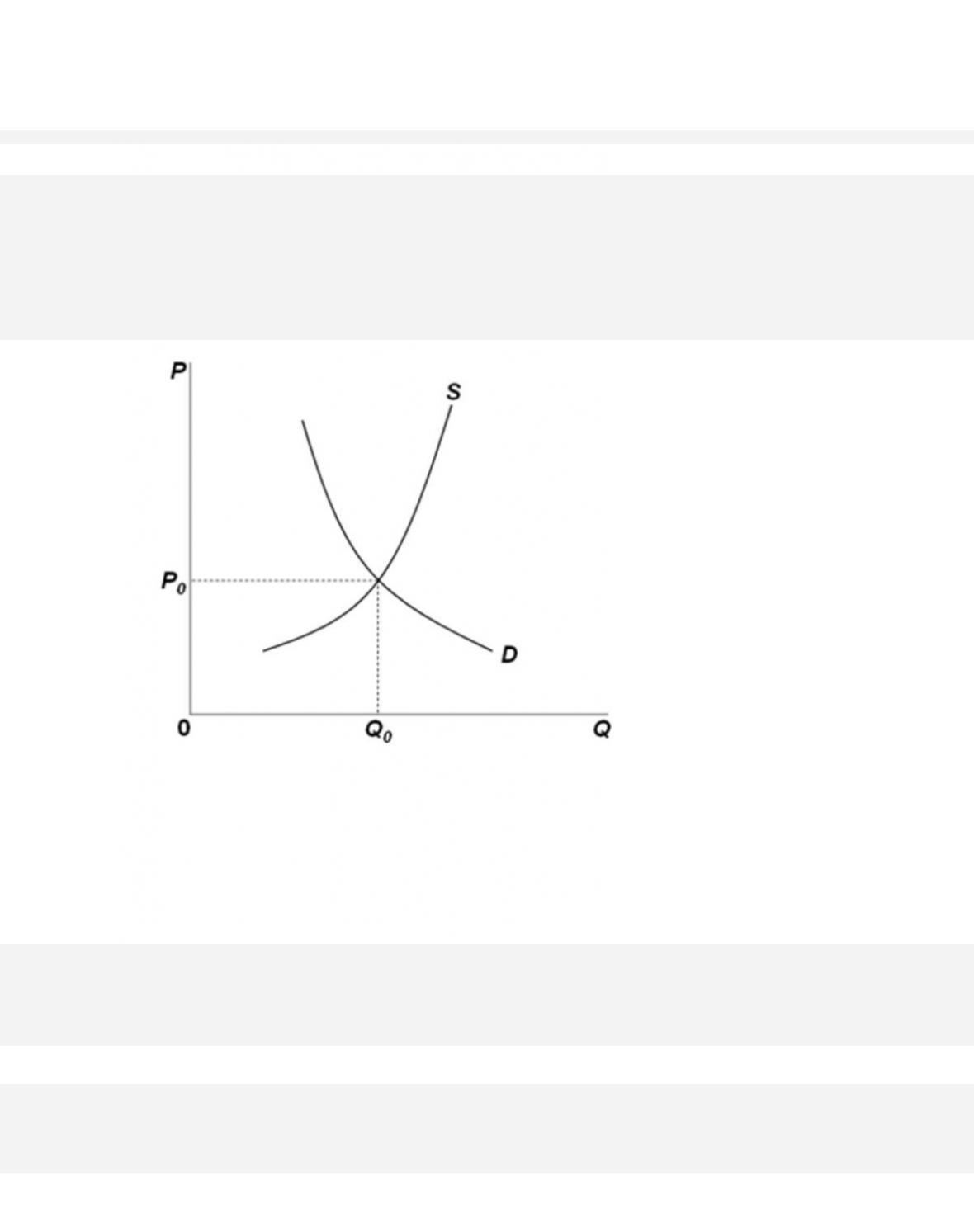

270.

If the supply and demand curves in the provided graph represent the market supply and demand

for a purely competitive industry, then the demand

curve that an individual firm in the industry

faces

10-165

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

Blooms: Understand

D i f f i c u lt y :

02 Medium

Learning Objective: 10–06 Explain why a competitive firms marginal cost curve is the same as

its supply curve.

Test Bank: II

Topic:

Marginal Cost and Short-Run Supply

271.

In pure competition, price is determined where the industry

272.

If the market demand for the product increases, in the short run a purely competitive firm

273.

The prices of raw materials increase in a purely competitive industry. This change will

result in a(n)

274.

Technological advance improves productivity in a purely competitive industry. This

change will result in a shift

275.

The resource cost falls in a purely competitive industry. This change will result in a(n)

10-167

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

AACSB: Knowledge Application

A c c e s s i b i l i t y :

Keyboard Navigation

Blooms: Understand

D i f f i c u lt y :

02 Medium

Learning Objective: 10–06 Explain why a competitive firms marginal cost curve is the same as

its supply curve.

Test Bank: II

Topic:

Marginal Cost and Short-Run Supply

276.

Assume that labor is a variable input. The average wage of workers increases in a purely

competitive industry. This change will result in a(n)

277.

Which of the following changes will not affect the market supply or the market demand in

a purely competitive industry?

10-168

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

Test Bank: II

Topic:

Marginal Cost and Short-Run Supply

278.

A competitive firm faces fixed costs even if it produces zero output. If it starts producing

and selling some output, which of the following would

happen?

True / False Questions

279.

If there are many firms in an industry, then it must be a purely competitive market.

280.

The basic difference between pure competition and monopolistic competition is in the

number of firms in the industry.

10-169

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

Learning Objective: 10–01 Give the names and summarize the main characteristics of the four

basic market models.

Test Bank: II

Topic:

Four Market Models

281.

Competitive firms are price takers largely because of intensive advertising by their

competitors.

282.

For a purely competitive firm, the demand curve facing it is the same as its marginal

revenue curve.

283.

In pure competition, the industry demand curve is infinitely price elastic.

284.

For an individual firm in pure competition, the firm‘s average revenue and marginal

revenue at any output level are both equal to the product’s price.

285.

If a purely competitive firm is producing a level of output greater than its profit-

maximizing output, then its profits must be negative.

286.

As long as its total revenues are greater than its total costs, a firm will earn positive

economic profits.

287.

If the firm produces an output level below its break-even point, then the firm will earn

negative economic profits.

288.

If a purely competitive firm is producing a level of output where the marginal revenue is

less than the marginal cost, then its profits must be negative.

289.

As long as an additional unit of output yields a marginal revenue larger than its marginal

cost, it will be adding to total profits of the firm.

290.

If MR > MC for a competitive firm, it should reduce its level of output in order to make

MR equal to MC.

10-172

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

AACSB: Knowledge Application

A c c e s s i b i l i t y :

Keyboard Navigation

Blooms: Understand

D i f f i c u lt y :

02 Medium

Learning Objective: 10–05 Explain how purely competitive firms can use the marginal-revenue–

marginal-cost approach to maximize profits or minimize losses in the short run.

Test Bank: II

Topic:

Profit Maximization in the Short Run: Marginal-Revenue–Marginal-Cost Approach

291.

In the short run, a competitive firm will not produce unless price is at least equal to

average total costs.

292.

In the short run, fixed costs are important in determining a competitive firm‘s optimal level

of output.

293.

In pure competition, a competitive firm‘s supply curve is that section of its marginal cost

curve above ATC, and at any price below the average cost,

the firm will produce nothing.

10-173

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

Blooms: Understand

D i f f i c u lt y :

02 Medium

Learning Objective: 10–03 Explain how demand is seen by a purely competitive seller.

Test Bank: II

Topic:

Demand as Seen by a Purely Competitive Seller