9-21

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

AACSB: Knowledge Application

A c c e s s i b i l i t y : Keyboard Navigation

Blooms: Understand

Difficu lty: 02 Medium

Learning Objective: 09–02 Relate the law of diminishing returns to a firms short-run

production costs.

Test Bank: I

To pi c : Short-Run Production Relationships

47.

Which of the following is correct?

A.

When total product is rising, both average product and marginal product must also be rising.

48.

Which of the following is not correct?

A.

Where marginal product is greater than average product, average product is rising.

9-22

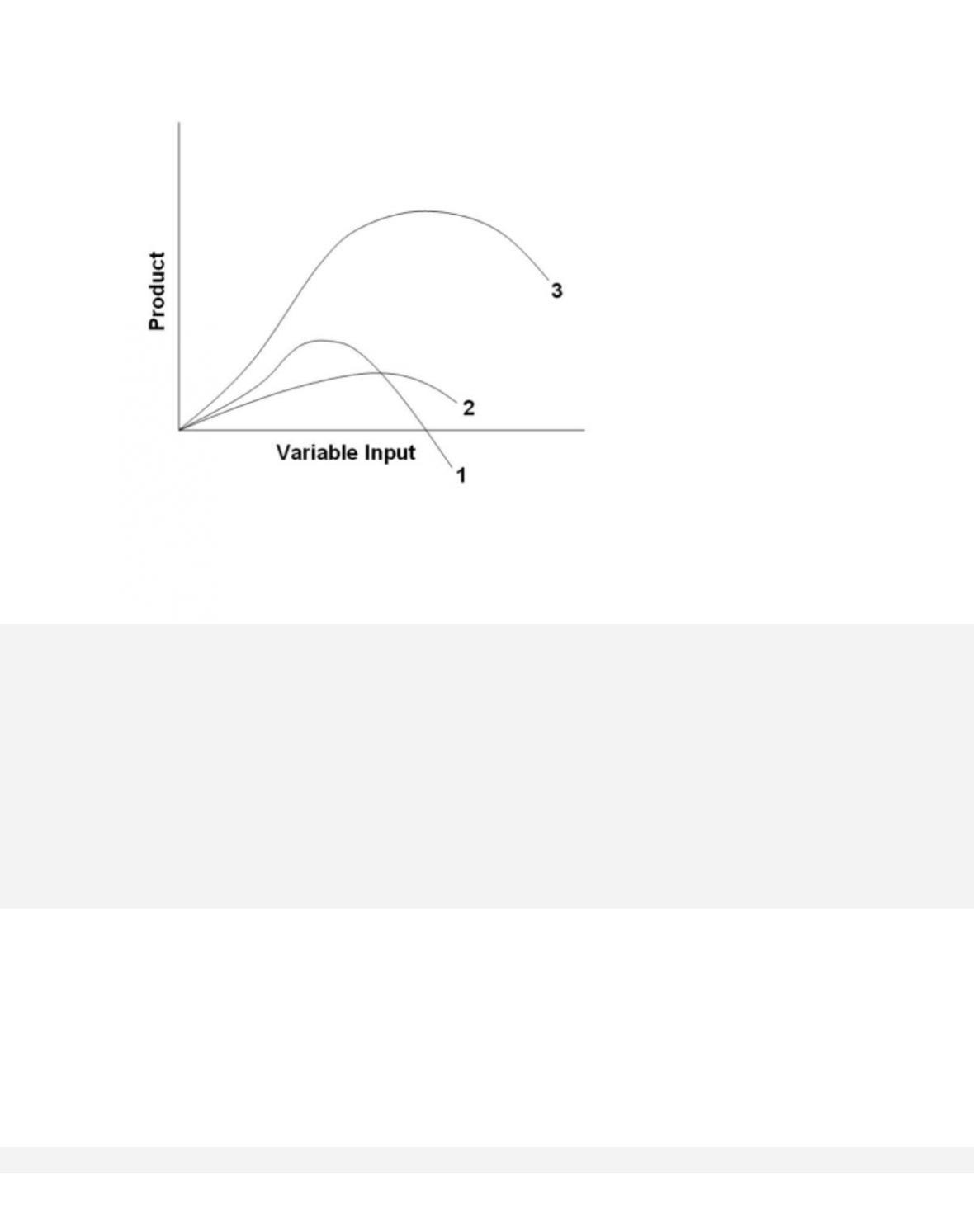

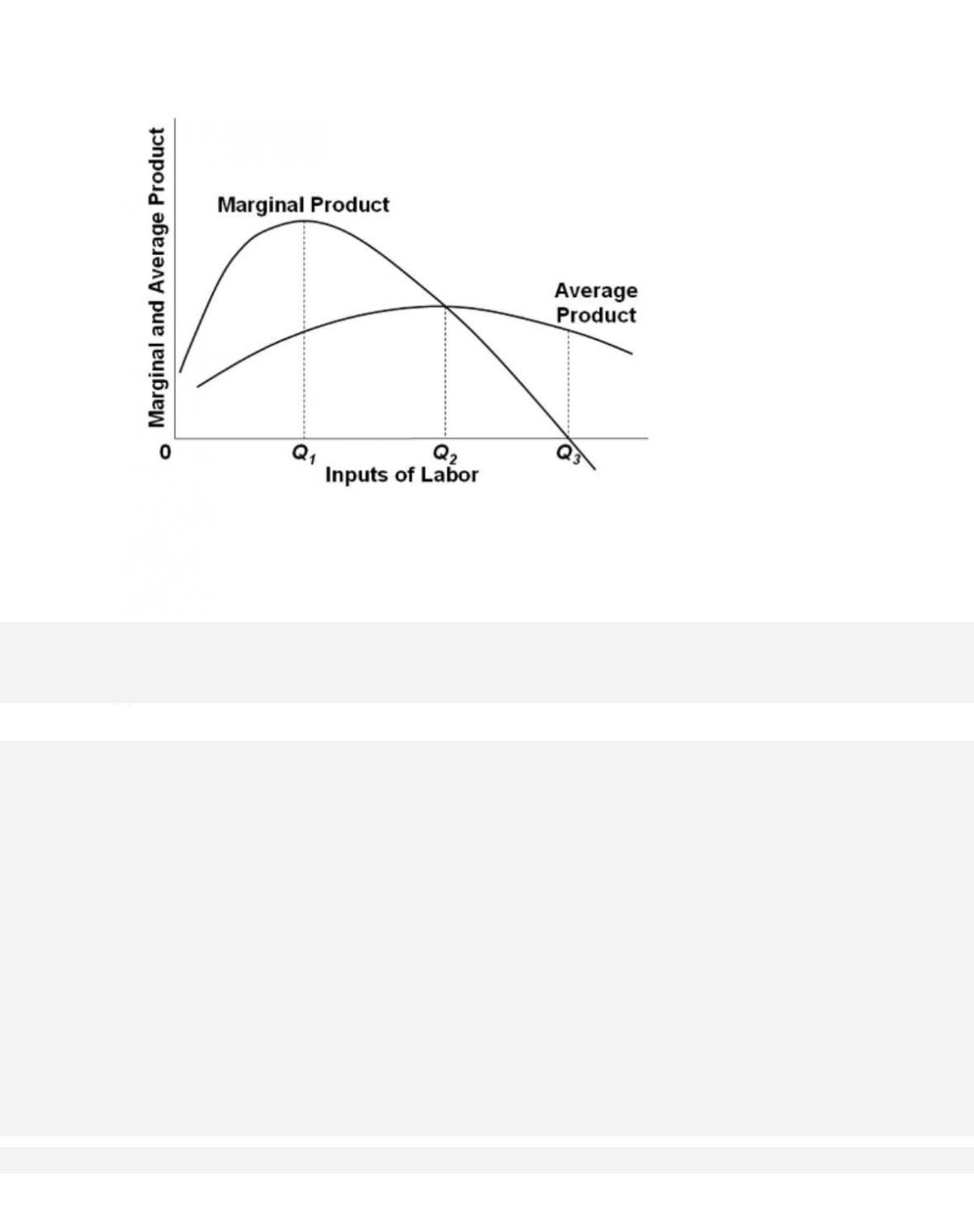

49.

In the diagram, curves 1, 2, and 3 represent the

A. average, marginal, and total product curves respectively.

50.

The diagram suggests that

A. when marginal product is zero, total product is at a minimum.

51.

The total output of a firm will be at a maximum where

A.

MP is at a maximum.

9-24

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

A c c e s s i b i l i t y : Keyboard Navigation

Blooms: Understand

Difficu lty: 02 Medium

Learning Objective: 09–02 Relate the law of diminishing returns to a firms short-run

production costs.

Test Bank: I

To pi c : Short-Run Production Relationships

52.

Answer the question on the basis of the following information.

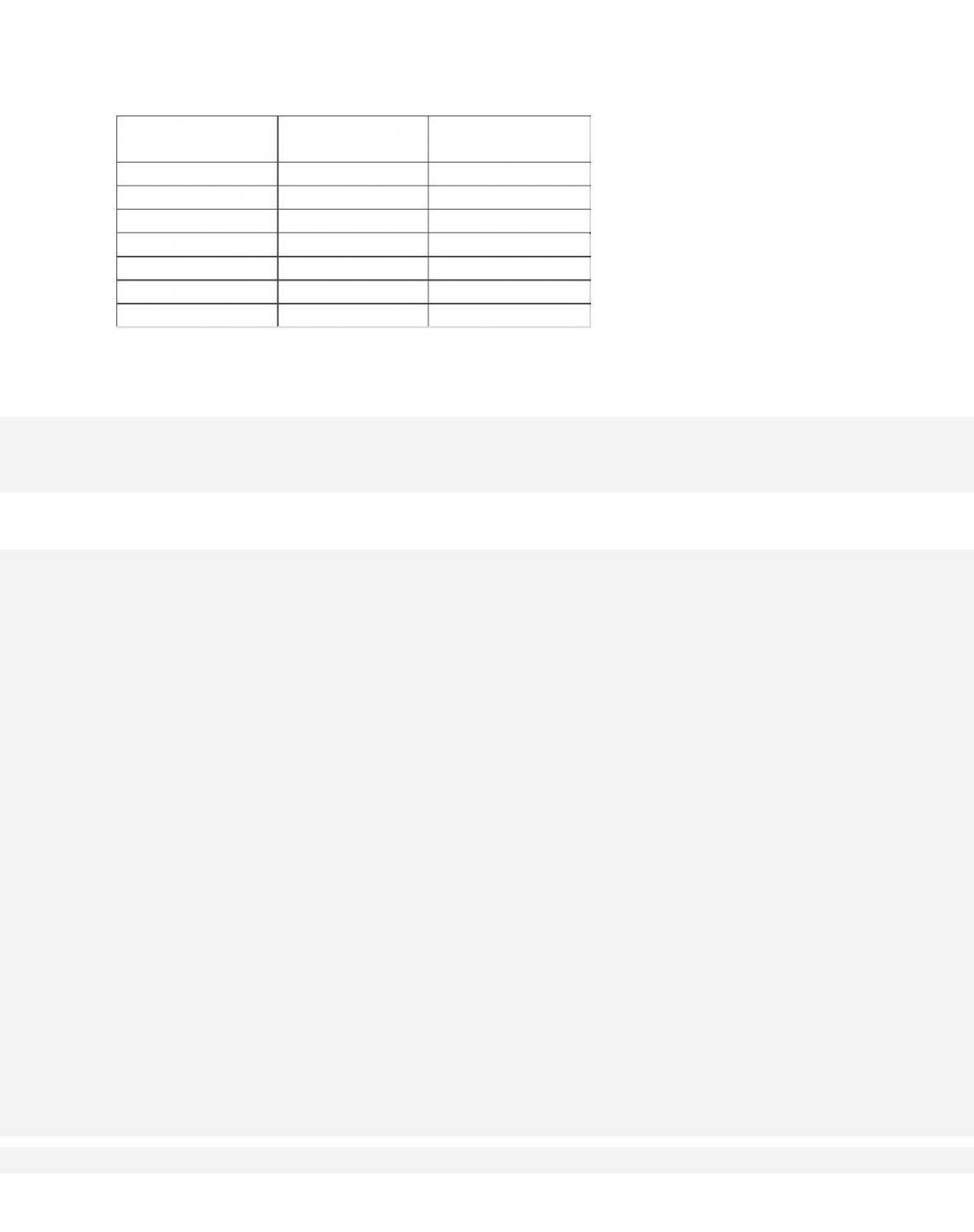

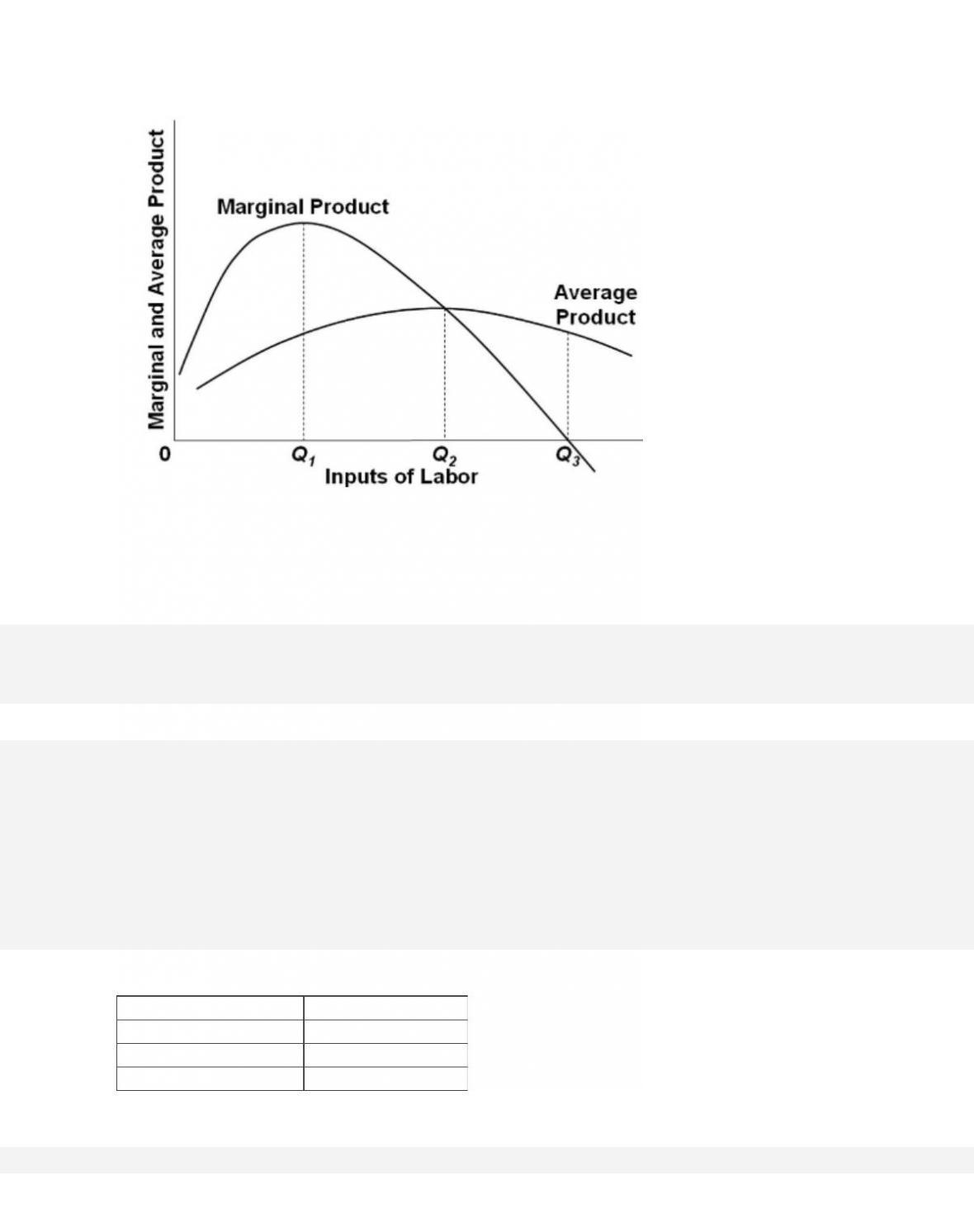

Number of

Workers

Total Product

Marginal Product

0

0

—

1

8

8

2

10

3

25

4

30

5

3

6

34

When two workers are employed,

Number of

Workers

Total Product

Marginal Product

0

0

—

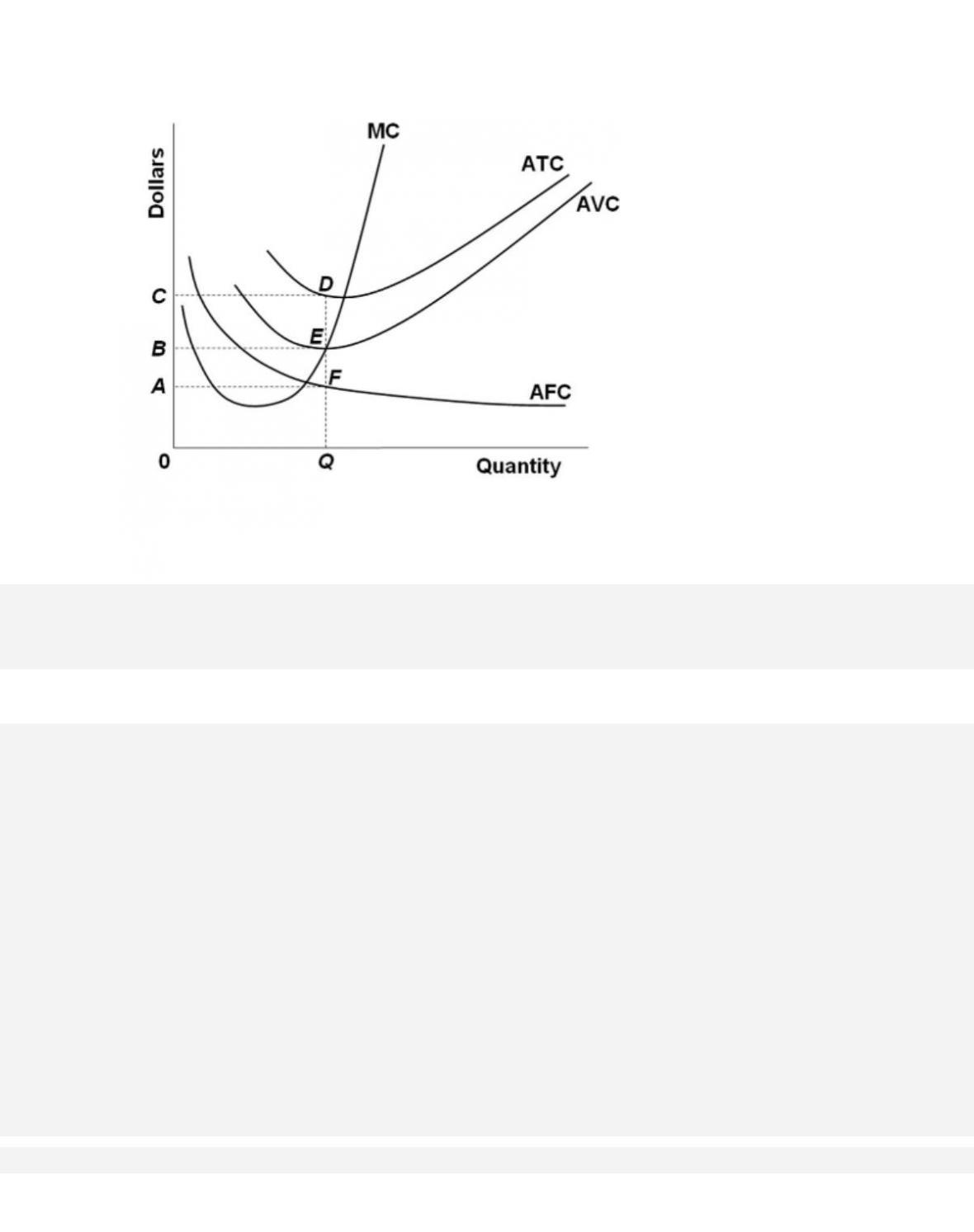

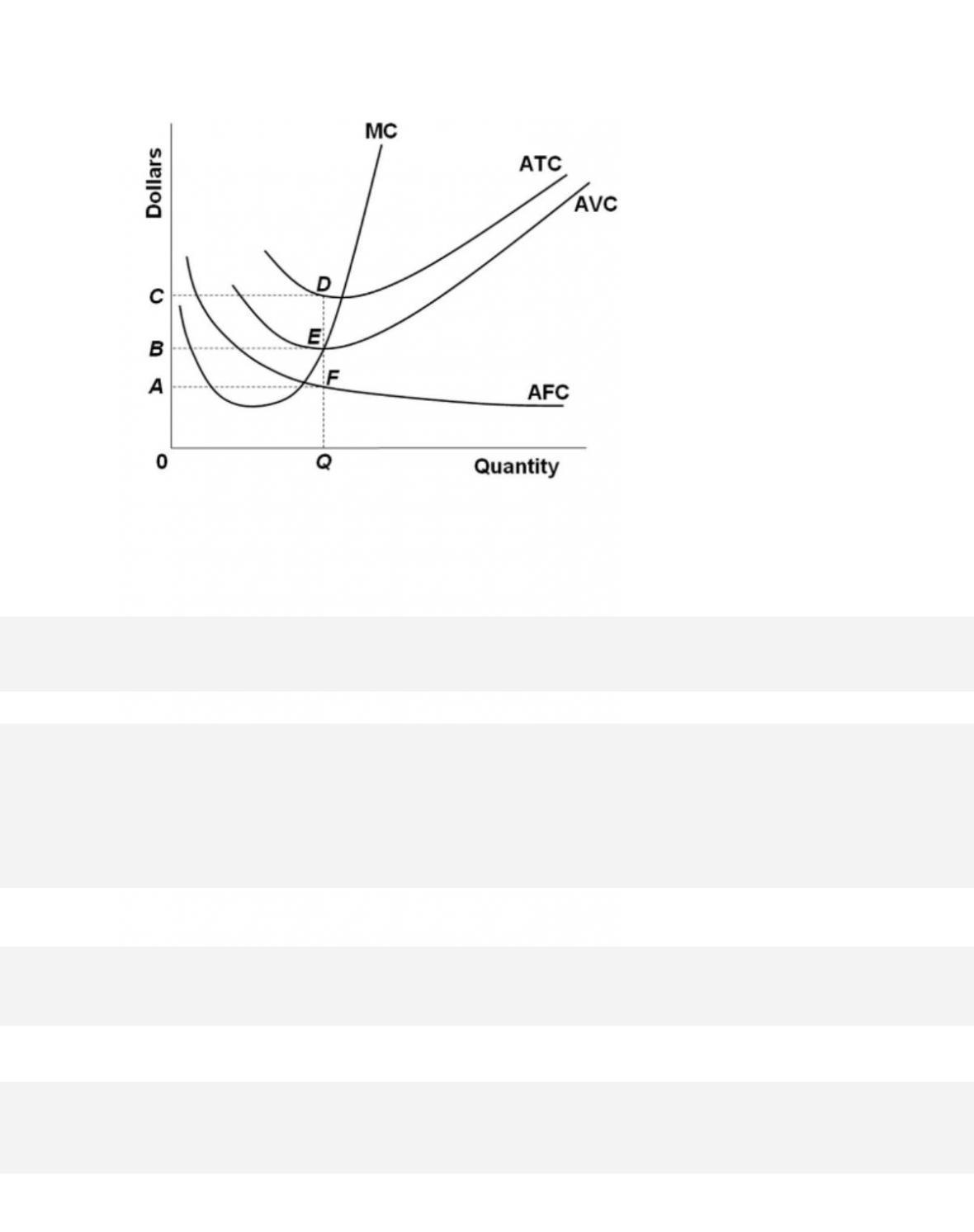

1

8

8

2

10

3

25

4

30

5

3

6

34

The marginal product of the fourth worker

D. cannot be calculated from the information given.

54.

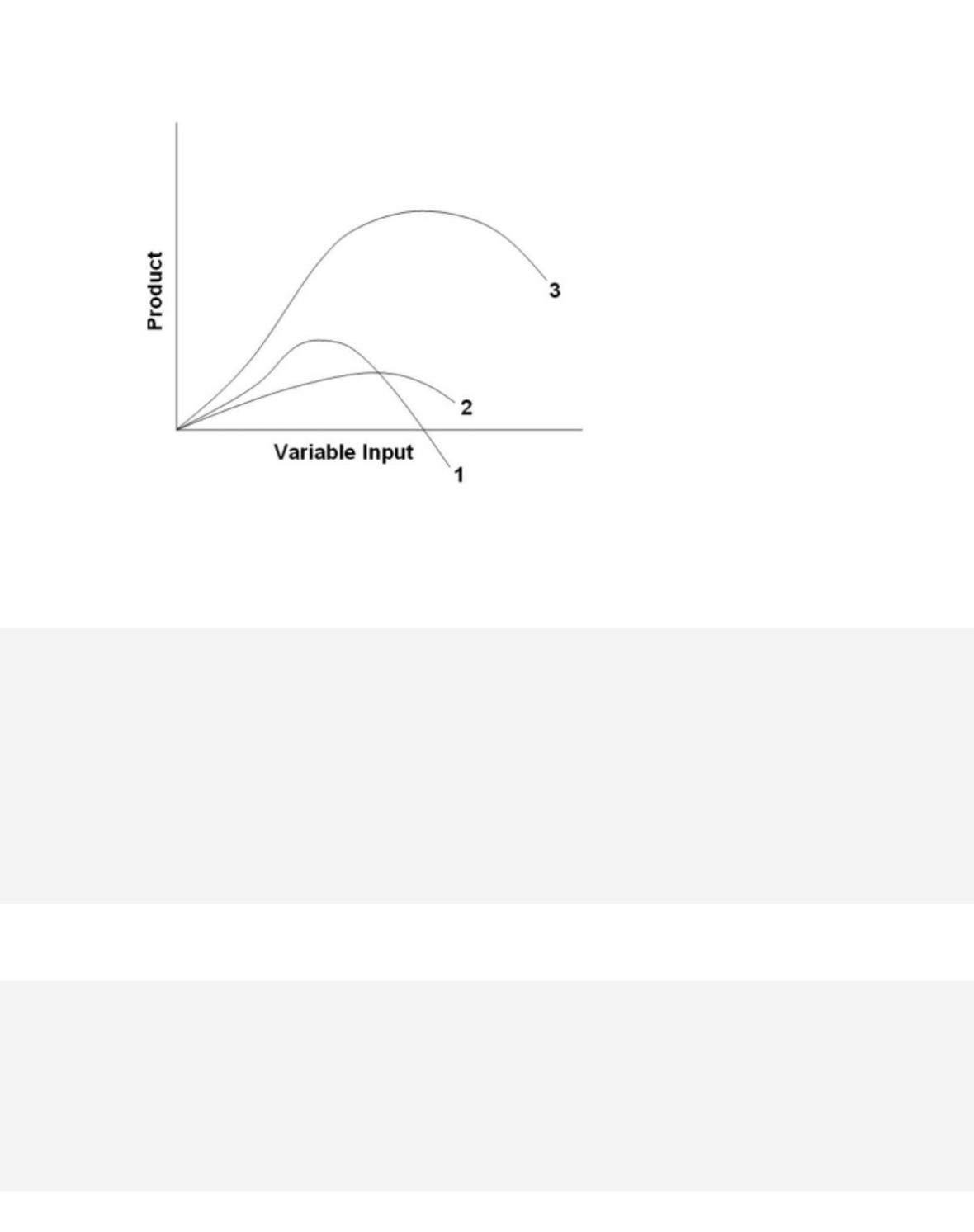

In the diagram, the range of diminishing marginal returns is

9-27

55.

In the diagram, total product will be at a maximum at

Inputs of Labor

Total Product

0

0

1

8

2

18

9-28

3

25

4

30

5

33

6

34

7

32

The average product (AP) when two units of labor are hired is

Inputs of Labor

Total Product

0

0

1

8

2

18

3

25

4

30

5

33

6

34

7

32

Diminishing returns begin to occur with the hiring of the unit of labor.

A.

first

B.

second

9-29

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

C. third

D. seventh

AACSB: Knowledge Application

Blooms: Understand

Difficu lty: 02 Medium

Learning Objective: 09–02 Relate the law of diminishing returns to a firms short-run

production costs.

Test Bank: I

To pi c : Short-Run Production Relationships

Type: Table

58.

Use the following data to answer the question.

Inputs of Labor

Total Product

0

0

1

8

2

18

3

25

4

30

5

33

6

34

7

32

Marginal product becomes negative with the hiring of the unit of labor.

A.

third

59.

When total product is increasing at an increasing rate, marginal product is

60.

When total product is increasing at a decreasing rate, marginal product is

D.

negative.

61.

Fixed cost is

A.

the cost of producing one more unit of capital, for example, machinery.

9-31

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

among total, average, and marginal costs.

Test Bank: I

To pi c : Short-Run Production Costs

62.

Which of the following is most likely to be a fixed cost?

A.

shipping charges

63.

If you owned a small farm, which of the following would most likely be a fixed cost?

64.

Which of the following is most likely to be a variable cost?

D. real estate taxes

9-32

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

A c c e s s i b i l i t y : Keyboard Navigation

Blooms: Understand

Difficu lty: 02 Medium

Learning Objective: 09–03 Describe the distinctions between fixed and variable costs and

among total, average, and marginal costs.

Test Bank: I

To pi c : Short-Run Production Costs

65.

If you operated a small bakery, which of the following would be a variable cost in the short

run?

66.

Marginal cost is the

A.

rate of change in total fixed cost that results from producing one more unit of output.

67.

For most producing firms,

A.

marginal cost rises as output is carried to a certain level, and then begins to decline.

9-33

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

B.

total costs rise as output is carried to a certain level, and then begin to decline.

C.

average total costs decline as output is carried to a certain level, and then begin to rise.

D. average total costs rise as output is carried to a certain level, and then begin to decline.

AACSB: Knowledge Application

A c c e s s i b i l i t y : Keyboard Navigation

Blooms: Understand

Difficu lty: 02 Medium

Learning Objective: 09–03 Describe the distinctions between fixed and variable costs and

among total, average, and marginal costs.

Test Bank: I

To pi c : Short-Run Production Costs

68.

Average fixed cost

A.

equals marginal cost when average total cost is at its minimum.

69.

Which of the following is correct as it relates to cost curves?

70.

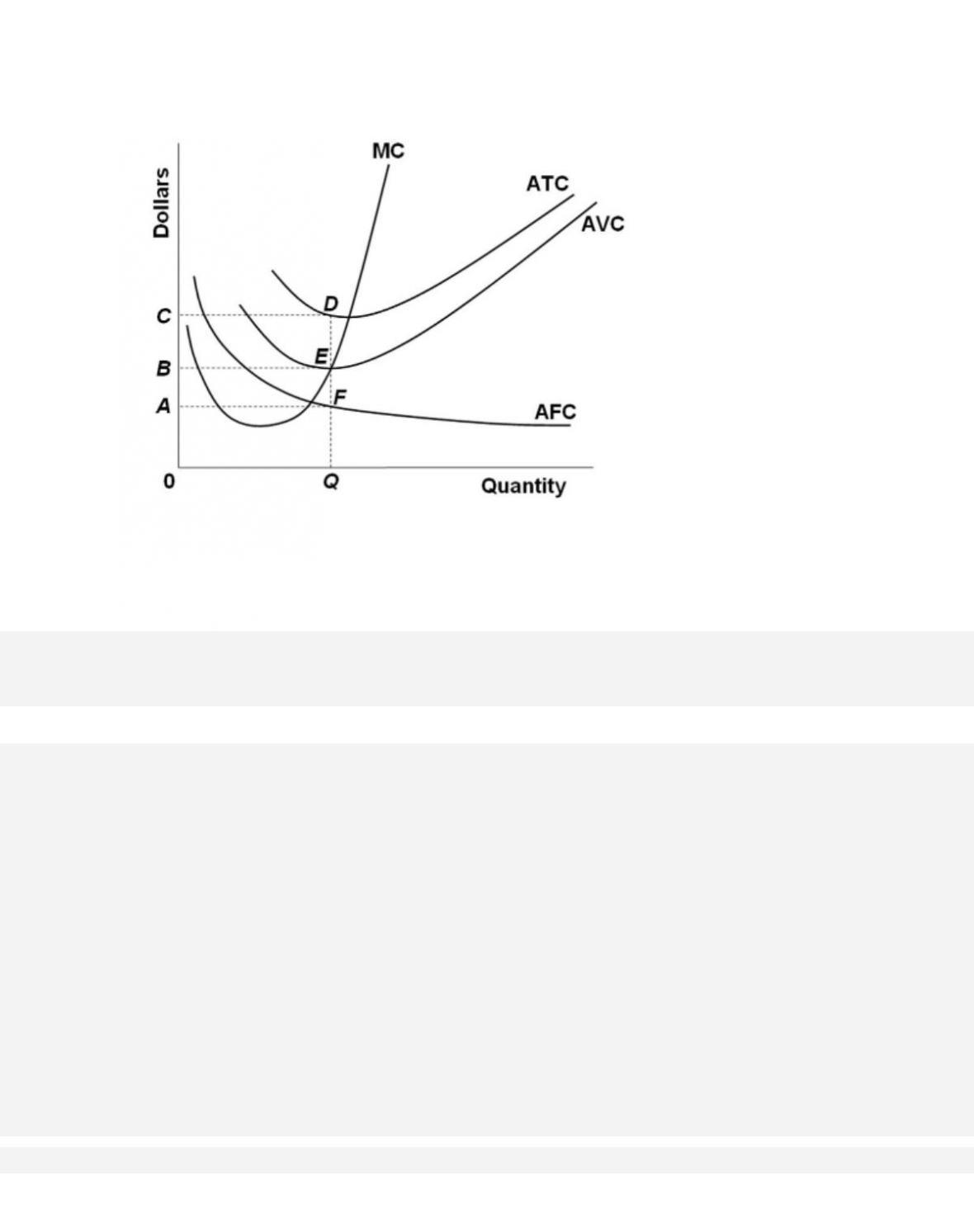

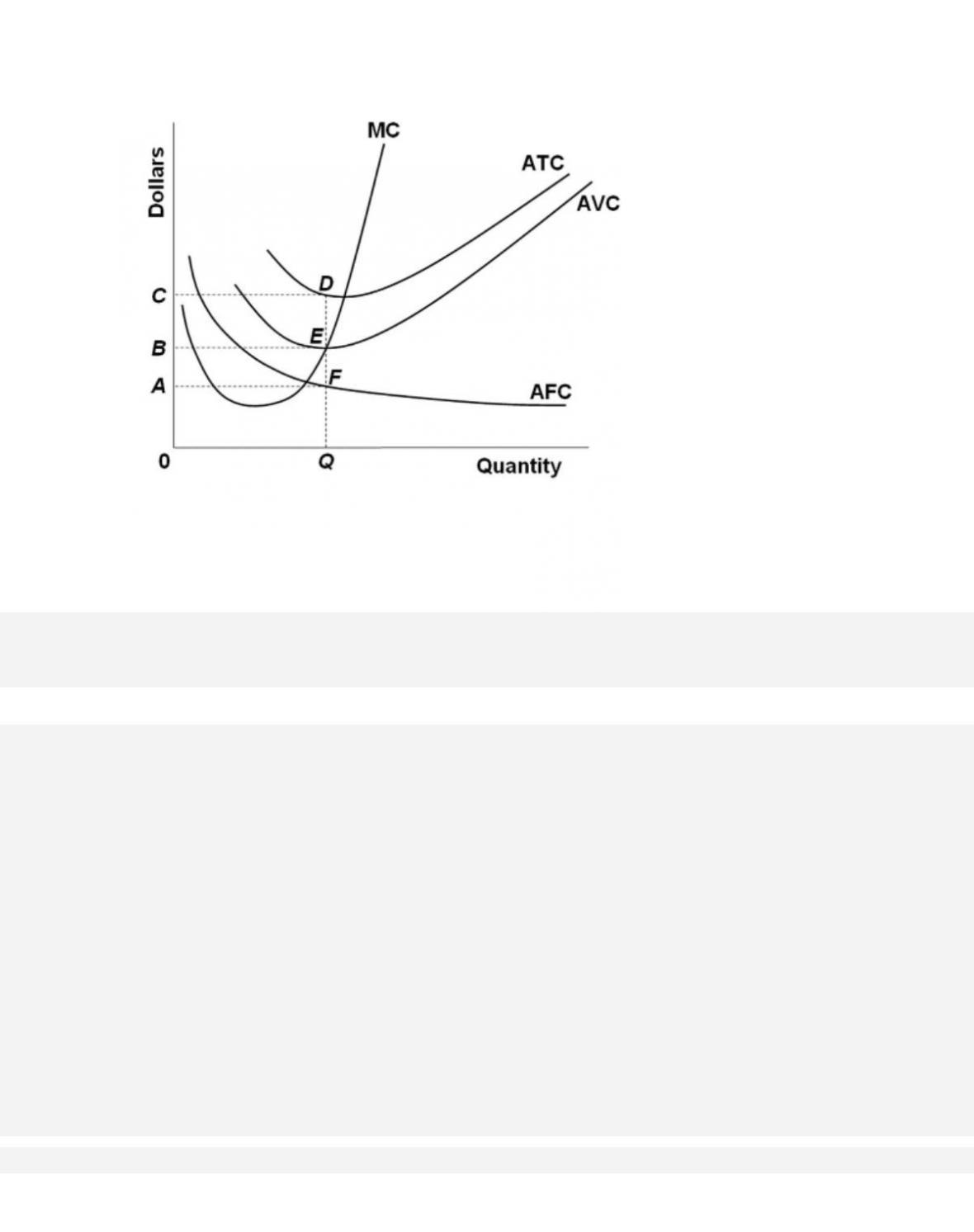

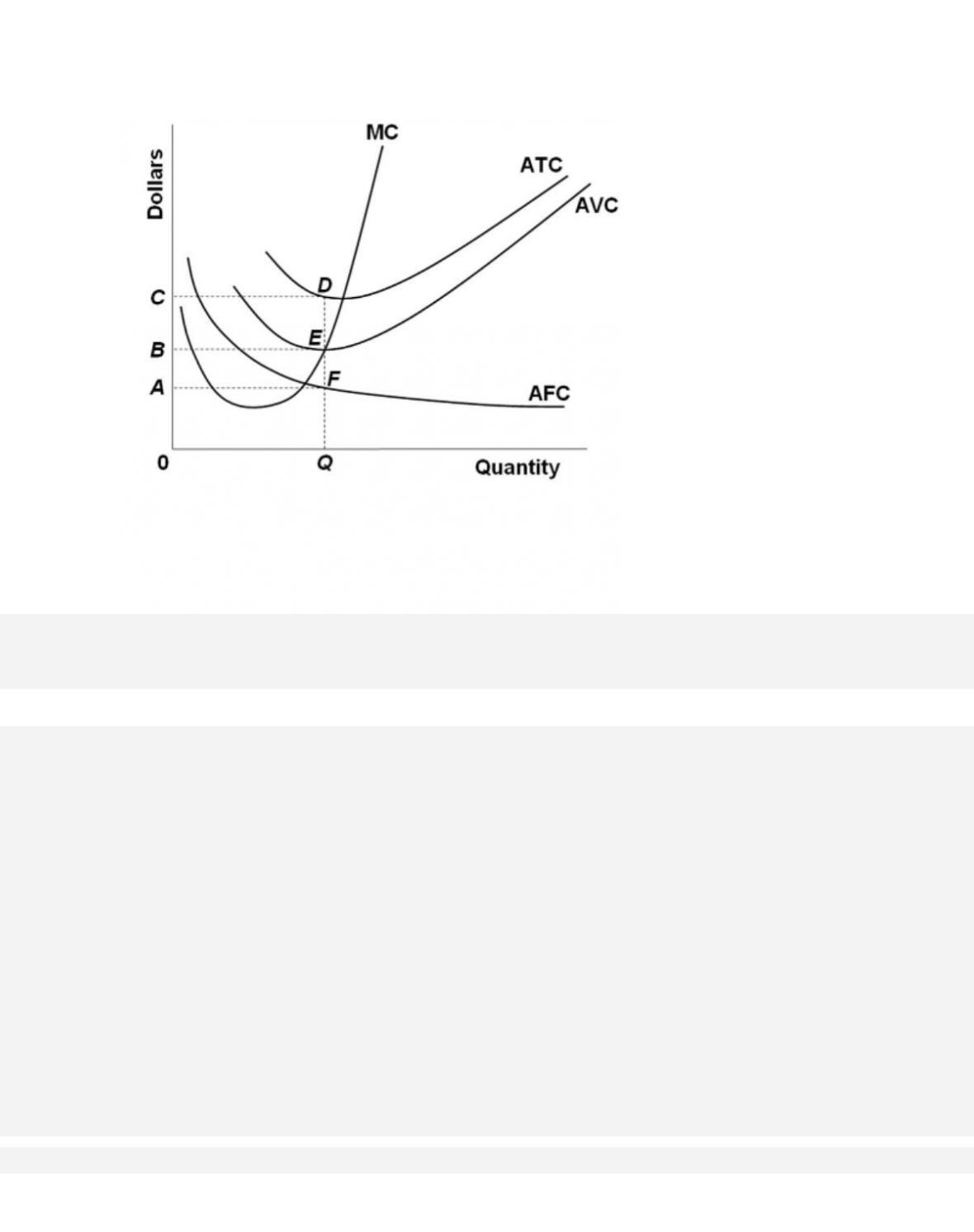

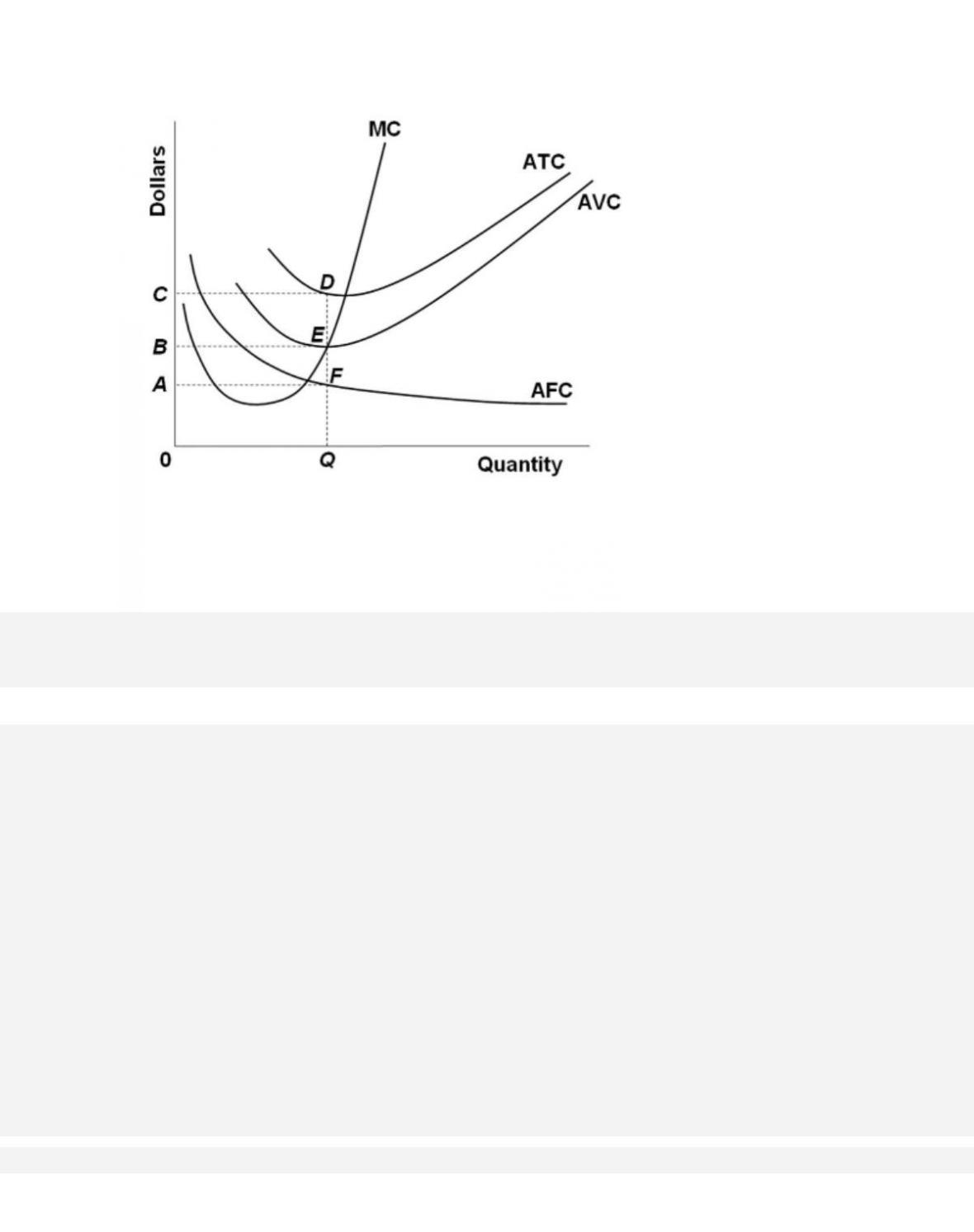

Refer to the diagram. At output level Q, total variable cost is

71.

Refer to the diagram. At output level Q, total fixed cost is

72.

Refer to the diagram. At output level Q, total cost is

73.

Refer to the diagram. At output level Q, average fixed cost

74.

Refer to the diagram. At output level Q,

D.

one cannot determine whether marginal product is falling or rising.

75.

Refer to the diagram. The vertical distance between ATC and AVC reflects

A. the law of diminishing returns.

76. Marginal cost

D.

declines continuously as output increases.

9-40

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

Blooms: Understand

Difficu lty: 02 Medium

Learning Objective: 09–03 Describe the distinctions between fixed and variable costs and

among total, average, and marginal costs.

Test Bank: I

To pi c : Short-Run Production Costs

77.

Which of the following statements is correct?

A. Average total cost is the difference between average variable cost and average fixed

cost.

78.

Assume that in the short run a firm is producing 100 units of output, has average total costs of

$200, and has average variable costs of $150. The firm’s total fixed costs are

D. $50.