26-532

CHAPTER 26

An Introduction to Macroeconomics

A. Short-Answer, Essays, and Problems

1. Classify the following questions as macroeconomics or microeconomics.

a) Why does a tax on soda increase consumption of ice tea?

b) Why are some countries rich while others are poor?

c) Why do some countries enjoy long-run increases in standards of living, while other countries have

stagnate growth?

d) Why are the prices of name-brand products higher than the prices of generic?

2. Macroeconomics is mainly concerned with two topics. What are these two topics and how are they related

to each other?

4. What is the difference between a slowdown in economic growth and a recession?

5. What are the three primary measures used in macroeconomics to assess the performance of an economy?

6. The three major indicators of the health and development of an economy include: real GDP,

unemployment, and inflation. All other things equal, would an economy prefer these numbers to be

7. Describe the difference between real GDP and nominal GDP. Which concept is more useful for measuring

change in the economy over time? Why?

8. Assume that a painter produces 20 paintings this year and 20 paintings next year. What is the annual

change in nominal GPD if the price of paintings rises from $1,000 this year to $1,500 next year? Can you

conclude that the economy grew from this year to next year based on your answer? Why?

9. Assume that in year 1 an economy produces 1000 units of output and they sell for $100 a unit, on average.

In year 2, the economy produces the same 1000 units of output, and sells it for $110 a unit, on average.

Use year 1 prices to calculate real GDP in Year 1 and Year 2. What happened to real GDP between years 1

and 2? Why?

10. What is the opportunity cost of unemployment for an economy? What social problems have been linked to

higher rates of unemployment?

11. Unemployment is not only bad for the economy due to the loss of goods and services. Describe some other

12. How does inflation affect people’s standards of living and savings?

13. Identify at least four important policy questions about the powers and limits of government economic

14. Compare and contrast the characteristics of economic growth in ancient or pre-industrial times with modern

15. What accounts for differences in living standards between rich and poor countries today?

26-533

16. GDP figures can be used to make international comparisons of living standards. What are three

adjustments made by the International Monetary Fund (IMF) to each country’s GDP to allow for

17. Define saving.

18. Why are savings and investment so important for economic growth? How do savings and investment affect

19. (Consider This) What is the difference between economic investment and financial investment? Give an

20. “Households are the principal source of savings. But businesses are the main economic investors.” Briefly

21. How do uncertainty and expectations influence economic behavior?

22. What are demand shocks? Give an example of a positive and a negative demand shock.

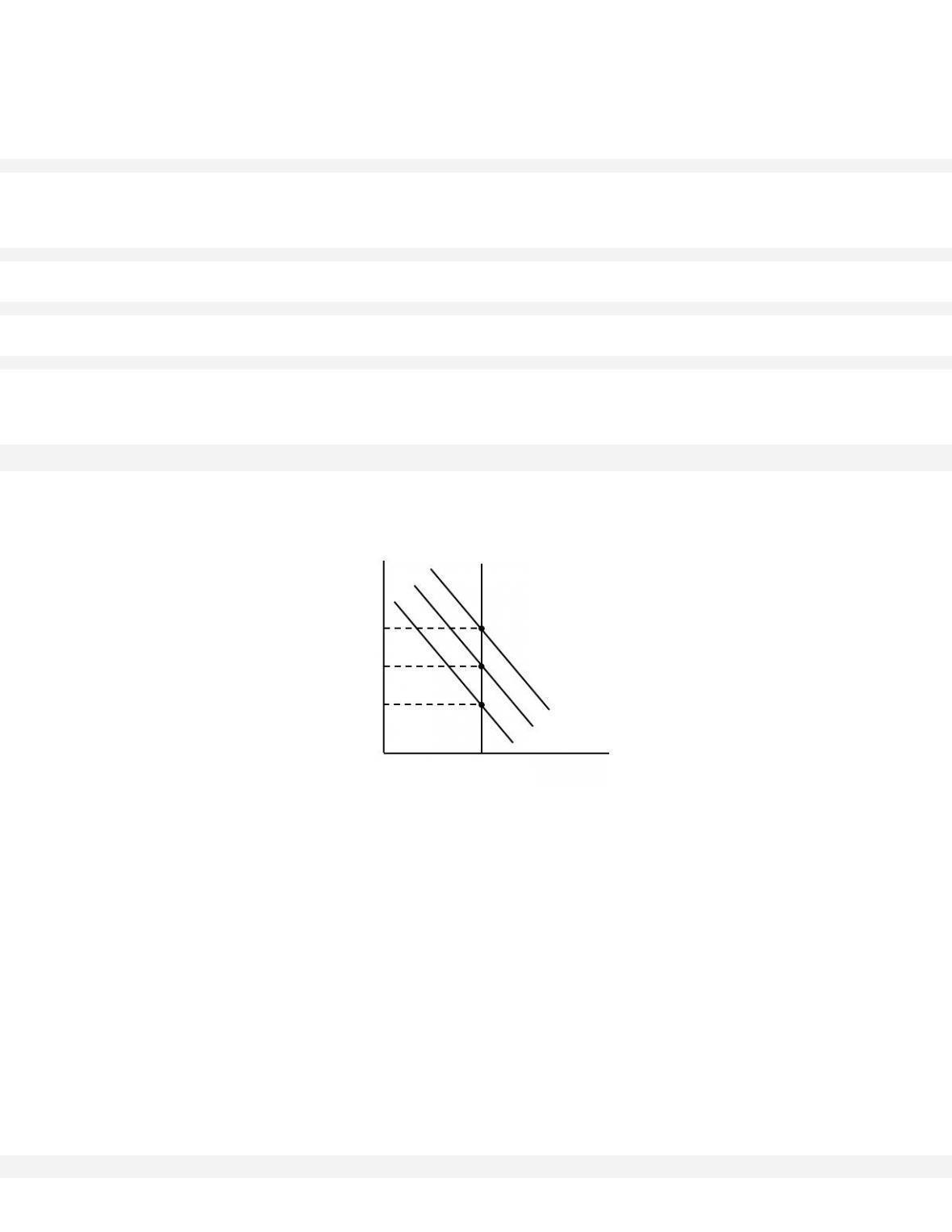

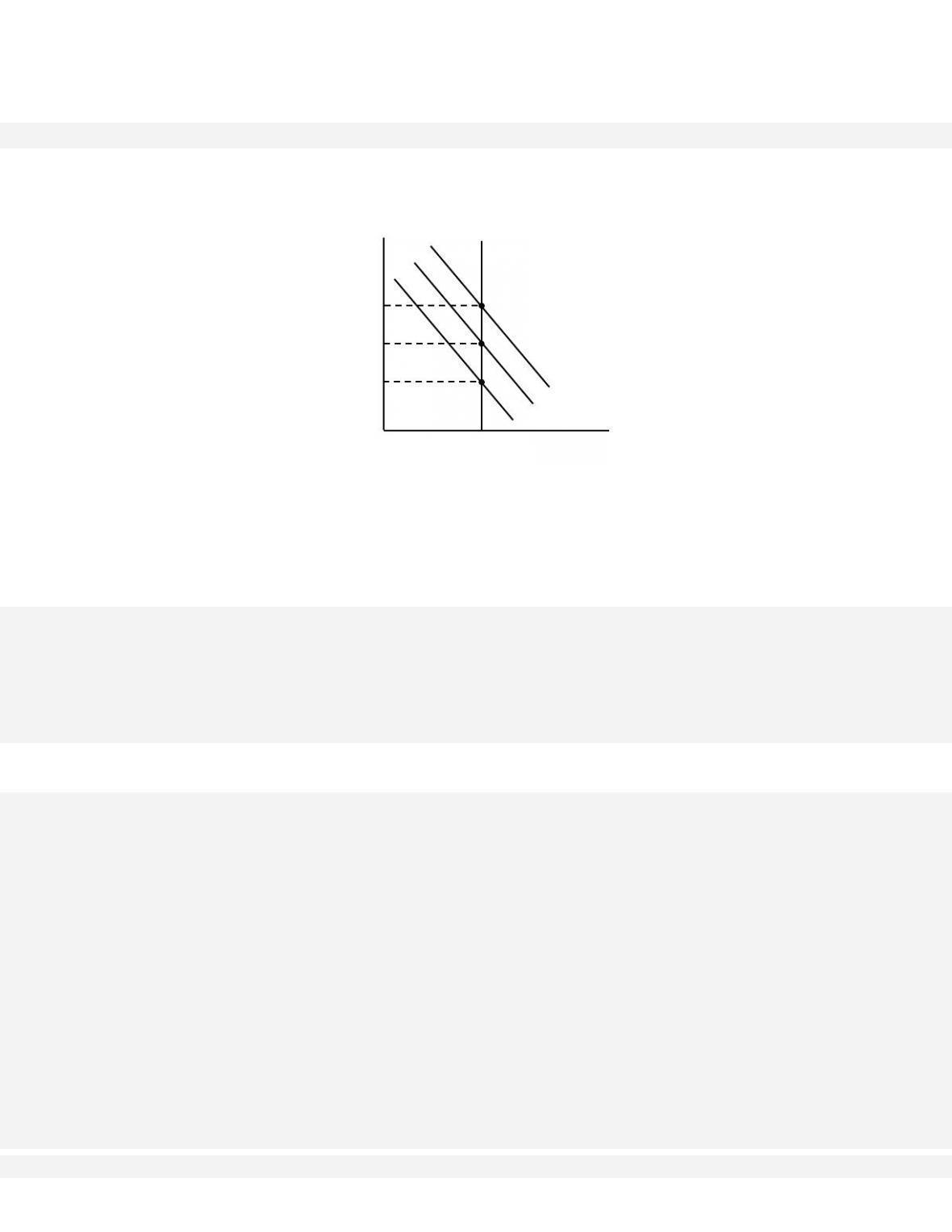

24. Answer the next four questions based on the following demand and supply model for a business firm

producing motorcycles. Assume that 300 motorcycles is the optimal and most profitable level of

production for the firm. All dollars are in thousands.

(a) What are the equilibrium price and quantity at the medium level of demand (DM)?

(b) What will be the equilibrium price and quantity if there is a demand shock that unexpectedly lowers

demand (DL)?

(c) What will be the equilibrium price and quantity if there is a demand shock that unexpectedly increases

demand (DH)?

(d) What can you conclude will happen to prices and output when this model is shocked by changes in

demand?

25. How does an economy adjust to demand shocks when prices are inflexible?

0

P

ri

c

e

30

300

DH

Motorcycle

s

20

10

DM

DL

S

26-534

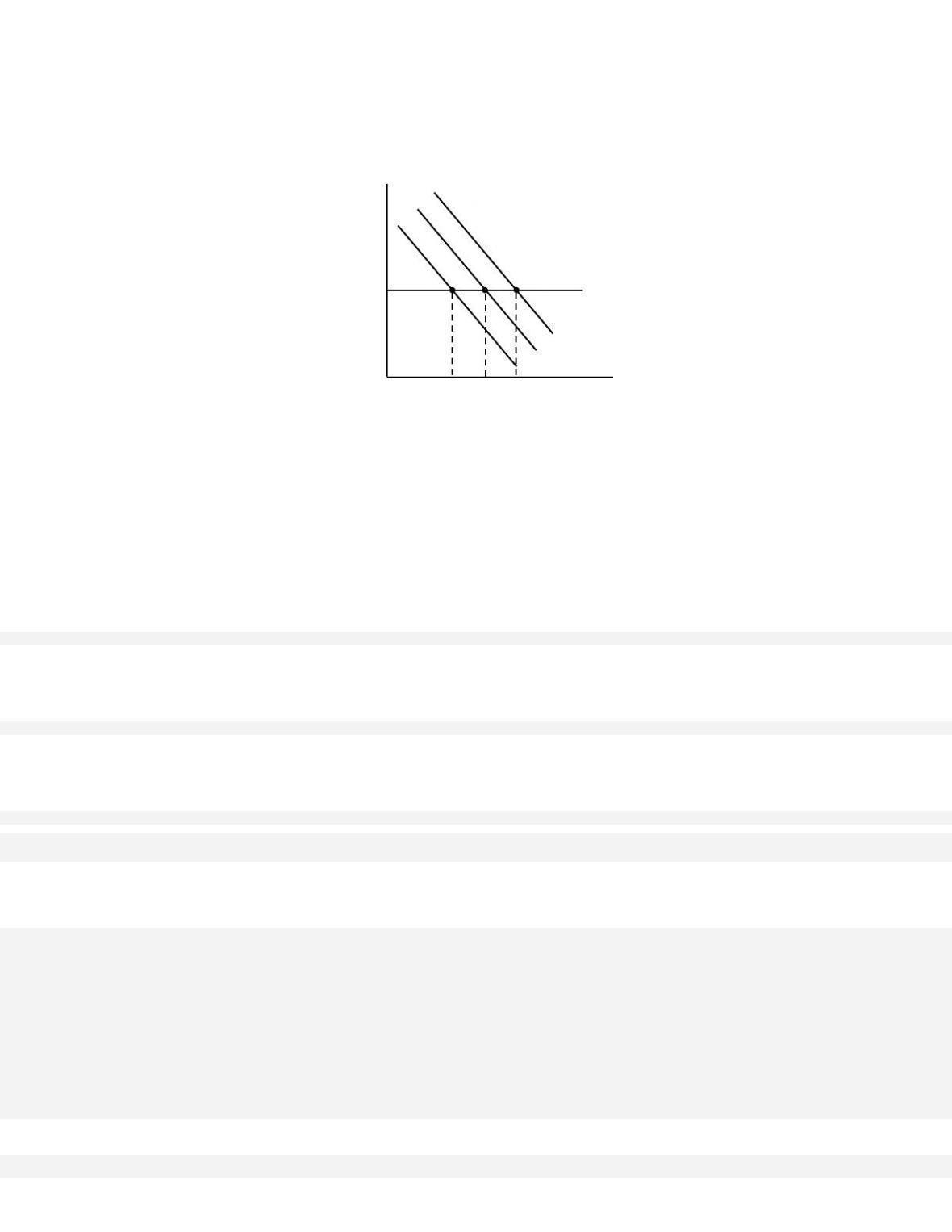

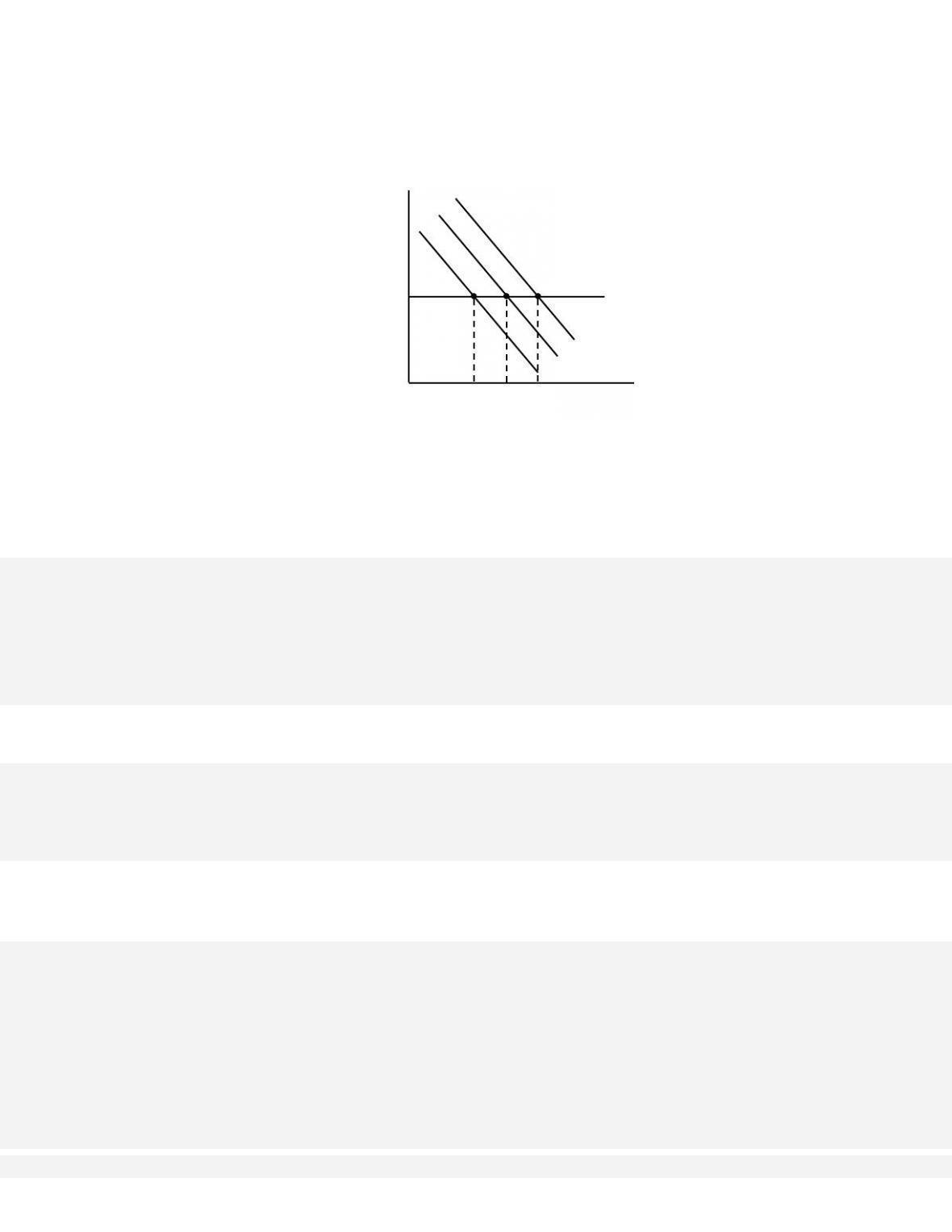

26. The following is a demand and supply model for a business firm producing baseball caps. Assume that 100

baseball caps is the optimal ad most profitable level of production for the firm. Answer the next four

questions assuming that the price of baseball caps is inflexible.

(a) What are the equilibrium price and quantity at the medium level of demand (DM)?

(b) What will be the equilibrium price and quantity if there is a demand shock that unexpectedly lowers

demand (DL)?

(c) What will be the equilibrium price and quantity if there is a demand shock that unexpectedly increases

demand (DH)?

(d) What can you conclude will happen to prices and output when this model is shocked by changes in

demand?

27. How do companies deal with unexpected shifts in quantity demanded when prices are sticky?

28. Evaluate the statement that “unexpected declines in demand, with inflexible prices, generate a rise in

29. (Consider This) Describe the economic conditions of the Great Recession.

30. (Consider This) Which took the major brunt of the decline in total demand in the Great Recession, real

31. What happens to inventories when prices are sticky and there is a demand shock? Explain.

32. Give examples of the stickiness of prices based on the average number of months between price changes

34. Why do economists refer to prices as “sticky” rather than “stuck”?

35. How can price stickiness be used to categorize macroeconomic models?

0

P

ri

c

e

100

DH

Baseball

caps

20

DM

DL

5

0

150

S

B. Answers to Short-Answer, Essays, and Problems

1. Classify the following questions as macroeconomics or microeconomics.

a) Why does a tax on soda increase consumption of ice tea?

b) Why are some countries rich while others are poor?

c) Why do some countries enjoy long-run increases in standards of living, while other countries have

stagnate growth?

d) Why are the prices of name-brand products higher than the prices of generic?

2. Macroeconomics is mainly concerned with two topics. What are these two topics and how are they related

to each other?

3. Contrast the economic growth and business cycles.

4. What is the difference between a slowdown in economic growth and a recession?

5. What are the three primary measures used in macroeconomics to assess the performance of an economy?

6. The three major indicators of the health and development of an economy include: real GDP,

unemployment, and inflation. All other things equal, would an economy prefer these numbers to be

increasing or decreasing? Why?

7. Describe the difference between real GDP and nominal GDP. Which concept is more useful for measuring

change in the economy over time? Why?

8. Assume that a painter produces 20 paintings this year and 20 paintings next year. What is the annual

change in nominal GPD if the price of paintings rises from $1,000 this year to $1,500 next year? Can you

conclude that the economy grew from this year to next year based on your answer? Why?

9. Assume that in year 1 an economy produces 1000 units of output and they sell for $100 a unit, on average.

In year 2, the economy produces the same 1000 units of output, and sells it for $110 a unit, on average.

Use year 1 prices to calculate real GDP in Year 1 and Year 2. What happened to real GDP between years 1

and 2? Why?

10. What is the opportunity cost of unemployment for an economy? What social problems have been linked to

higher rates of unemployment?

26-537

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

been linked to a number of social problems such as crime, political unrest, depression, heart disease and

other illnesses.

11. Unemployment is not only bad for the economy due to the loss of goods and services. Describe some other

reasons why unemployment has a negative effect on the economy.

12. How does inflation affect people’s standards of living and savings?

13. Identify at least four important policy questions about the powers and limits of government economic

policy that macroeconomics models are able to answer.

14. Compare and contrast the characteristics of economic growth in ancient or pre-industrial times with modern

economic growth today.

15. What accounts for differences in living standards between rich and poor countries today?

16. GDP figures can be used to make international comparisons of living standards. What are three

adjustments made by the International Monetary Fund (IMF) to each country’s GDP to allow for

meaningful comparisons of living standards between countries? Explain.

17. Define saving.

26-538

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

Saving is generated when current consumption is less than current output (or when current spending is less

than current income). The economic term used to define a situation where current consumption is more

than current output (or current spending is more than current income) is dissaving.

18. Why are savings and investment so important for economic growth? How do savings and investment affect

present and future consumption? Explain.

19. (Consider This) What is the difference between economic investment and financial investment? Give an

20. “Households are the principal source of savings. But businesses are the main economic investors.” Briefly

explain.

21. How do uncertainty and expectations influence economic behavior?

22. What are demand shocks? Give an example of a positive and a negative demand shock.

26-539

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

economy, if prices of products are completely flexible, then output would remain the same but the price of

goods and services would have to change to maintain a constant level of output.

24. Answer the next four questions based on the following demand and supply model for a business firm

producing motorcycles. Assume that 300 motorcycles is the optimal and most profitable level of

production for the firm. All dollars are in thousands.

(a) What are the equilibrium price and quantity at the medium level of demand (DM)?

(b) What will be the equilibrium price and quantity if there is a demand shock that unexpectedly lowers

demand (DL)?

(c) What will be the equilibrium price and quantity if there is a demand shock that unexpectedly increases

demand (DH)?

(d) What can you conclude will happen to prices and output when this model is shocked by changes in

demand?

25. How does an economy adjust to demand shocks when prices are inflexible?

0

P

ri

c

e

30

300

DH

Motorcycle

s

20

10

DM

DL

S

26. The following is a demand and supply model for a business firm producing baseball caps. Assume that 100

baseball caps is the optimal ad most profitable level of production for the firm. Answer the next four

questions assuming that the price of baseball caps is inflexible.

(a) What are the equilibrium price and quantity at the medium level of demand (DM)?

(b) What will be the equilibrium price and quantity if there is a demand shock that unexpectedly lowers

demand (DL)?

(c) What will be the equilibrium price and quantity if there is a demand shock that unexpectedly increases

demand (DH)?

(d) What can you conclude will happen to prices and output when this model is shocked by changes in

demand?

27. How do companies deal with unexpected shifts in quantity demanded when prices are sticky?

28. Evaluate the statement that “unexpected declines in demand, with inflexible prices, generate a rise in

unemployment and a fall in output.”

0

P

ri

c

e

100

DH

Baseball

caps

20

DM

DL

5

0

150

S

29. (Consider This) Describe the economic conditions of the Great Recession.

30. (Consider This) Which took the major brunt of the decline in total demand in the Great Recession, real

output or prices?

31. What happens to inventories when prices are sticky and there is a demand shock? Explain.

32. Give examples of the stickiness of prices based on the average number of months between price changes

for selected goods and services.

33. Describe two reasons why businesses hesitate to change prices.

34. Why do economists refer to prices as “sticky” rather than “stuck”?

26-542

35. How can price stickiness be used to categorize macroeconomic models?

36. Offer an explanation for how sticky the following prices are:

(a) Airline Tickets

(b) Coin-Operated Laundry Machines

(c) Gasoline

(d) Meals at Restaurants

37. (Last Word) Discuss two of the popular hypotheses economists offer for what caused the Great Recession.

The first hypothesis is the Minksy Explanation: Euphoric Bubbles. Economists Hyman Minksy believed

that recessions are often preceded by asset-price bubbles. In the case of the 2007-2009 recession, a massive

housing price bubble and home-mortgage loans was the driver. When the bubble collapsed many investors

and homeowners lost trillions of dollars. Sticky prices and a leftward shift in demand forced many

companies to reduce output and lay off workers. Weak firms exited the market by claiming bankruptcy and

firing all workers.

38. (Last Word) Explain the two popular opinions held by economists on how to improve the economy.

The first solution is the Stimulus Solution. The majority of economists argued that to improve the economy

shift in demand rightward was necessary. This could have been accomplished in a variety of ways. The