CHAPTER 11

Pure Competition in the Long Run

A. Short-Answer, Essays, and Problems

1. What is the major difference between the long run and the short run in pure competition? Explain in terms

2. Is there a specific amount of time that distinguishes the long run from the short run? Is the amount of time

3. What three assumptions are used in the chapter to keep the analysis relatively simple?

4. What is the basic conclusion that is to be drawn from the chapter? On what two facts is this conclusion

based? What are the implications?

5. Explain why the long-run product price for a perfectly competitive firm will equal its minimum average

6. Assume that in a purely competitive industry: (1) the entry and exodus of firms are the only long-run

adjustments; (2) firms in the industry have identical cost curves; and (3) the industry is a constant-cost

7. An airline is flying between two cities. The airline has the following costs associated with the flight:

Crew $4000 Plane daily depreciation $2000

Fuel 1000 Plane daily insurance 2000

Landing fee 1000

8. Suppose that Helen’s Hotdog Hut operates in a purely competitive market. Helen produces 1,000 hotdogs a

week and has an average variable cost of $1.25, average fixed costs of $1.00, and a marginal cost of $2.00.

10. Firms in the market for soccer balls are selling in a purely competitive market. A firm in the soccer ball

expect the firm to do in the short run? The market in the long run?

11. Firms in the market for dog food are selling in a purely competitive market. A firm producing dog food has

an output of 10,000 pounds of dog food, for which it sells for $0.50 a pound. At the output level of 10,000

pounds the average variable cost is $0.30, the average total cost is $0.70, and the marginal cost is $0.50.

What would you expect the firm to do in the short run? The market in the long run?

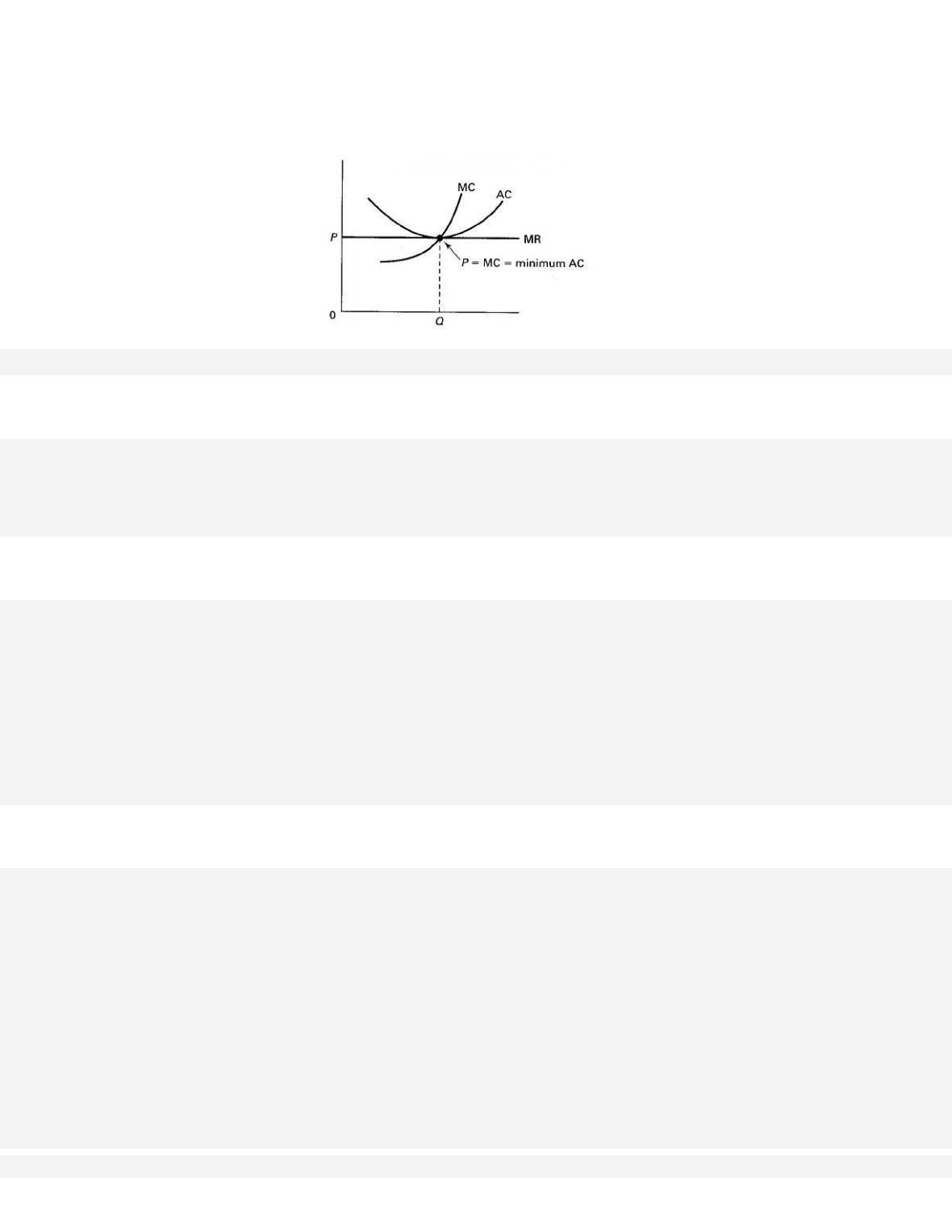

11–247

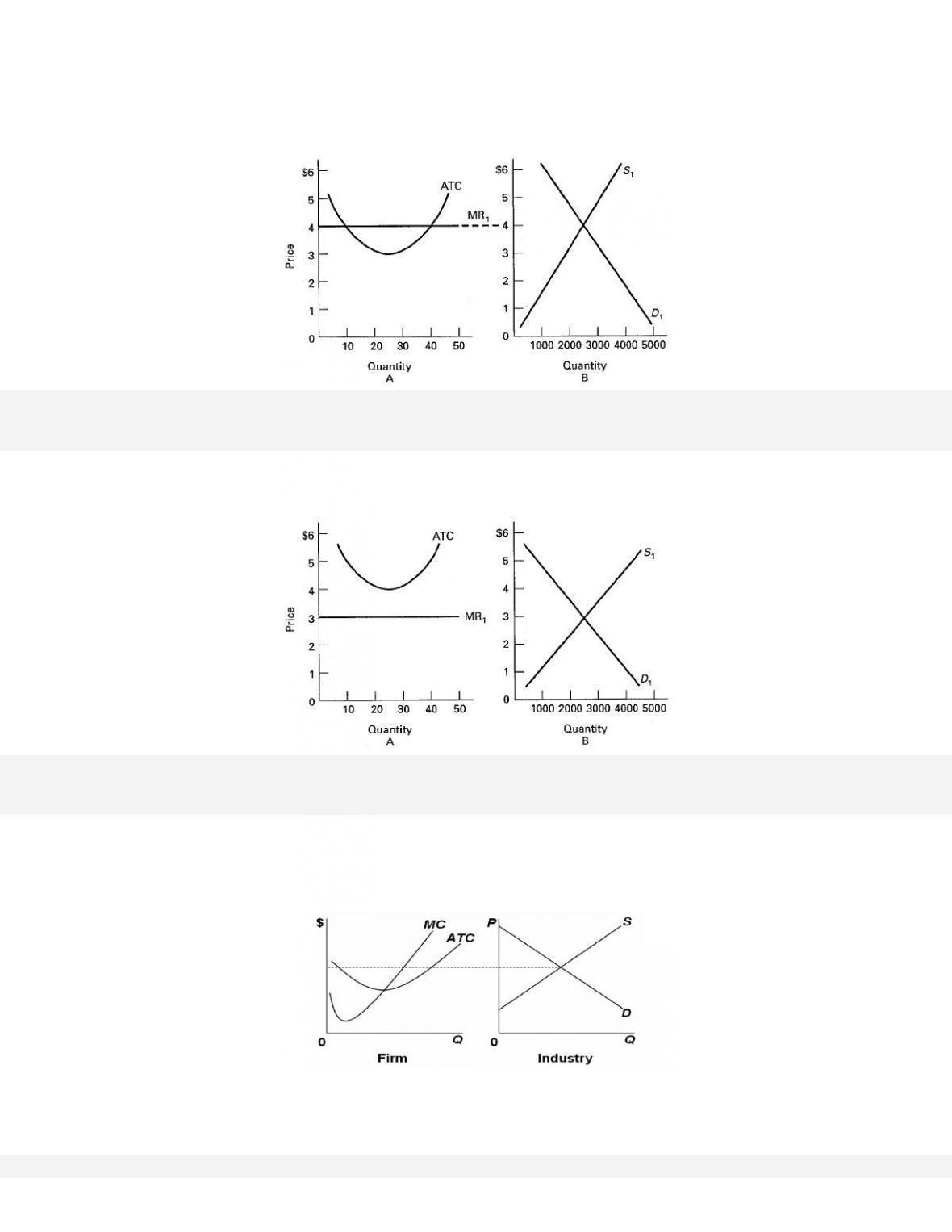

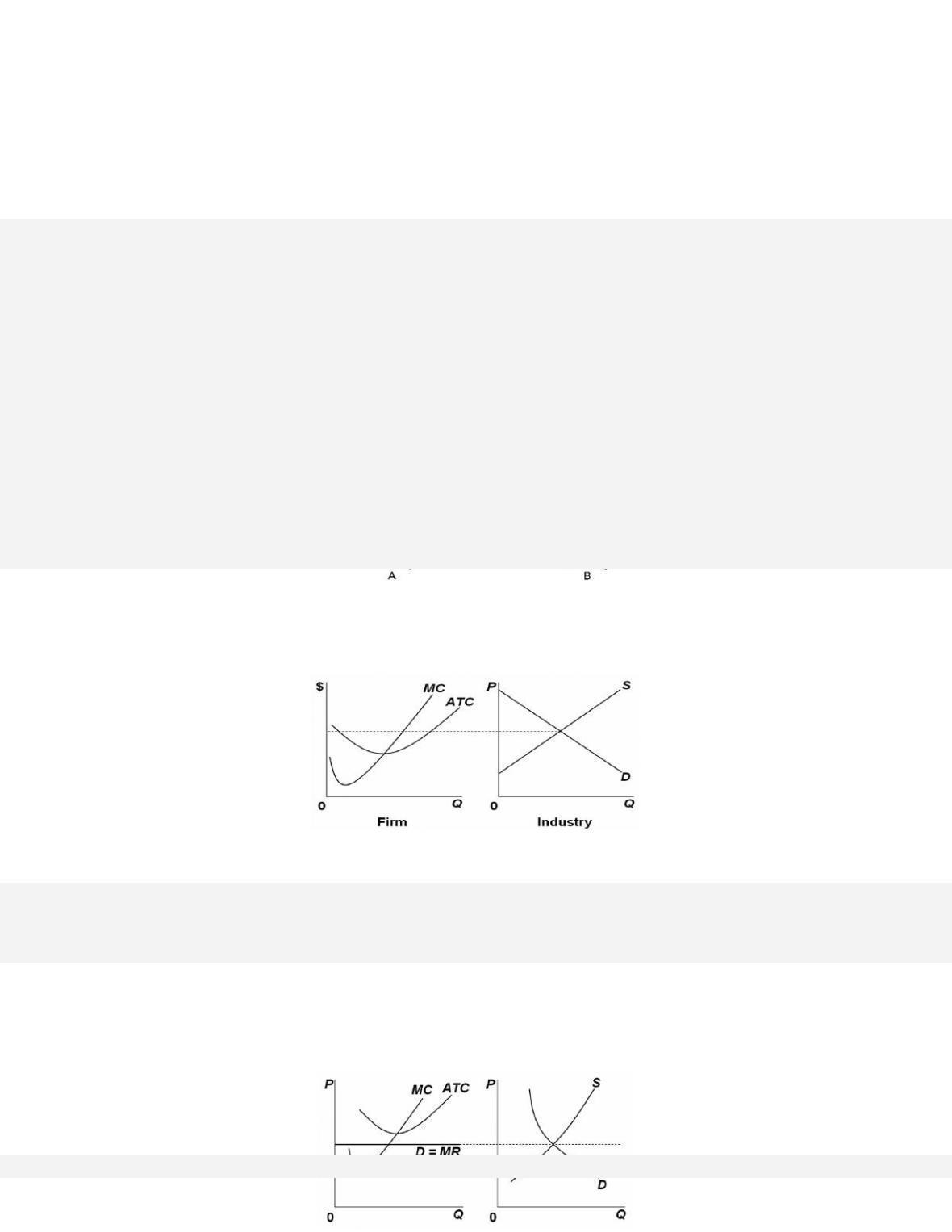

12. Consider the two graphs below. Graph A represents a typical firm in a purely competitive industry. Graph

B represents the supply and demand conditions in that industry.

13. Consider the two graphs below. Graph A represents a typical firm in a purely competitive industry. Graph

B represents the supply and demand conditions in that industry.

14. Consider the two graphs below. Graph A represents a typical firm in a purely competitive industry. Graph

B represents the supply and demand conditions in that industry. The dashed horizontal line represents the

current market price for firms and for the industry. In the long run, what will happen to price, profit, the

supply curve, and the number of firms in the industry?

11–248

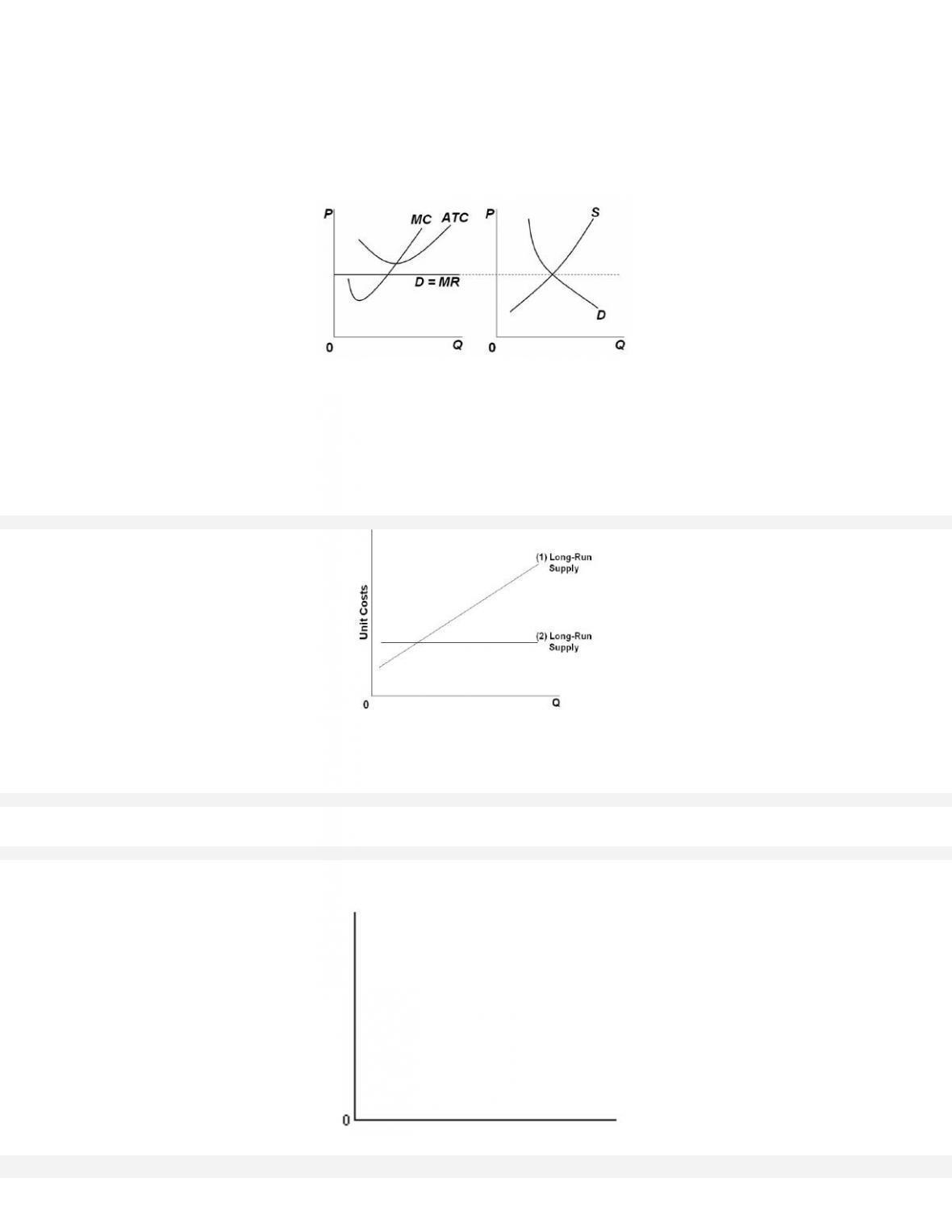

15. Consider the two graphs below. Graph A represents a typical firm in a purely competitive industry. Graph

B represents the supply and demand conditions in that industry. The dashed horizontal line represents the

current market price for firms and for the industry. In the long run, what will happen to price, profit, the

supply curve, and the number of firms in the industry?

16. “The long-run industry supply curve in a constant-cost industry graphs as a horizontal line.” Explain.

17. What is the relationship between the long-run supply curve in a constant-cost industry and elasticity?

18. Describe the graph for a long-run supply curve in an increasing-cost industry. Why does it have this slope?

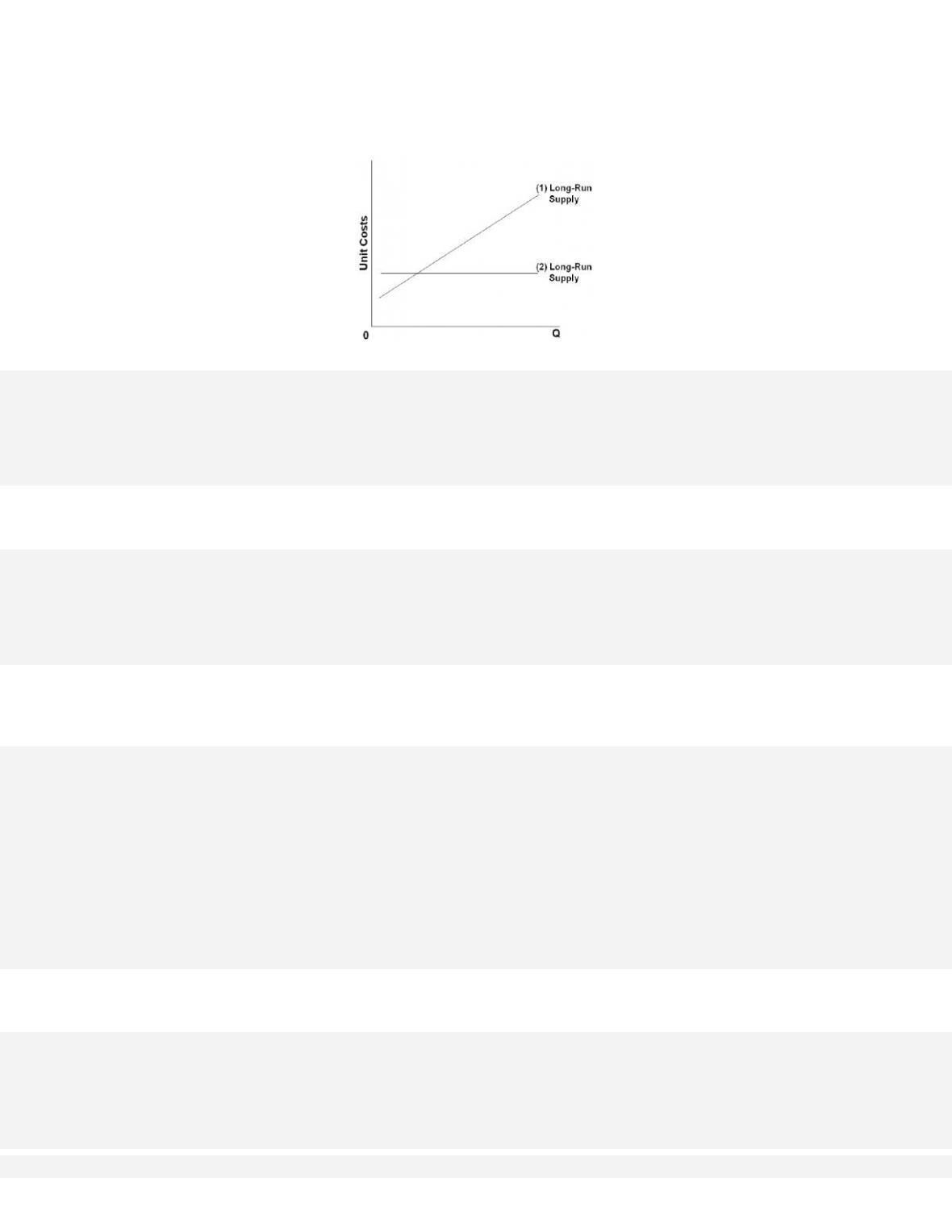

19. Below is a graph of two possible long-run industry supply curves for a purely competitive industry.

20. Describe the graph for a long-run supply curve in a decreasing-cost industry. Why does it have this slope?

21. Compare the long-run supply curve for a constant-cost industry, a decreasing-cost industry, and an

22. What economic conditions are necessary to achieve productive and allocative efficiency under pure

23. Draw a graph on the diagraph below showing the long-run equilibrium position of a competitive firm.

Write a formula to express the equalities in the graph.

11–249

24. What economic conditions are necessary to achieve allocative efficiency under pure competition?

25. Explain what allocative efficiency is and how it is achieved in pure competition.

26. Why does pure competition provide consumers with the largest consumer and producer surpluses?

28. How are producer and consumer surpluses maximized in a competitive market?

29. How would a purely competitive industry adjust and restore allocative efficiency when there is an increase

in the demand for a product?

30. How does the “invisible hand” work in a competitive market system?

31. What are the differences between competition in a purely competitive industry and competition in an

32. What are two strategies that entrepreneurs use to earn more than the normal profit? Will these strategies

33. What is the concept of creative destruction? Describe two industry examples and how it has worked over

34. Define creative destruction. Describe the transition of the music listening industry in terms of creative

35. (Last Word) Assess the arguments for and against patents in terms of creative destruction.

B. Answers to Short-Answer, Essays, and Problems

1. What is the major difference between the long run and the short run in pure competition? Explain in terms

of the number of firms and the flexibility of firms.

2. Is there a specific amount of time that distinguishes the long run from the short run? Is the amount of time

important? Explain.

3. What three assumptions are used in the chapter to keep the analysis relatively simple?

4. What is the basic conclusion that is to be drawn from the chapter? On what two facts is this conclusion

based? What are the implications?

The basic conclusion is that after all adjustments have been made in the long run in a purely competitive

industry, product price will be equal to, and production will occur at, the minimum average total cost for

5. Explain why the long-run product price for a perfectly competitive firm will equal its minimum average

total cost.

6. Assume that in a purely competitive industry: (1) the entry and exodus of firms are the only long-run

adjustments; (2) firms in the industry have identical cost curves; and (3) the industry is a constant-cost

industry. Explain how long-run equilibrium is eventually achieved in the industry when there are initially

economic profits and losses.

7. An airline is flying between two cities. The airline has the following costs associated with the flight:

Crew $4000 Plane daily depreciation $2000

Fuel 1000 Plane daily insurance 2000

Landing fee 1000

The airline has an average of 40 passengers paying an average of $200 for this flight. Do you think the

airline should be flying between the two cities? Evaluate from a long-run perspective.

8. Suppose that Helen’s Hotdog Hut operates in a purely competitive market. Helen produces 1,000 hotdogs a

week and has an average variable cost of $1.25, average fixed costs of $1.00, and a marginal cost of $2.00.

a) What is the price of a hot dog?

b) What would you expect Helen to do in the short run? Why.

c) What would you expect Helen to do in the long run? Why.

9. Explain why a firm might continue to operate in the short run even though they are earning an economic

loss.

11–252

10. Firms in the market for soccer balls are selling in a purely competitive market. A firm in the soccer ball

market has an output of 5,000 balls, which it sells for $10 each. At the output level of 5,000 the average

variable cost is $6.00, the average total cost is $7.50, and the marginal cost is $10.00. What would you

expect the firm to do in the short run? The market in the long run?

11. Firms in the market for dog food are selling in a purely competitive market. A firm producing dog food has

an output of 10,000 pounds of dog food, for which it sells for $0.50 a pound. At the output level of 10,000

pounds the average variable cost is $0.30, the average total cost is $0.70, and the marginal cost is $0.50.

What would you expect the firm to do in the short run? The market in the long run?

12. Consider the two graphs below. Graph A represents a typical firm in a purely competitive industry. Graph

B represents the supply and demand conditions in that industry.

(a) Describe the price, output, and profit situation for the individual firm in the short run.

(b) Describe what will happen to the individual firm and the industry in the long run. Show the changes

11–253

13. Consider the two graphs below. Graph A represents a typical firm in a purely competitive industry. Graph

B represents the supply and demand conditions in that industry.

(a) Describe the price, output, and profit situation for the individual firm in the short run.

(b) Describe what will happen to the individual firm and the industry in the long run. Show the changes

on graphs A and B.

14. Consider the two graphs below. Graph A represents a typical firm in a purely competitive industry. Graph

B represents the supply and demand conditions in that industry. The dashed horizontal line represents the

current market price for firms and for the industry. In the long run, what will happen to price, profit, the

supply curve, and the number of firms in the industry?

15. Consider the two graphs below. Graph A represents a typical firm in a purely competitive industry. Graph

B represents the supply and demand conditions in that industry. The dashed horizontal line represents the

current market price for firms and for the industry. In the long run, what will happen to price, profit, the

supply curve, and the number of firms in the industry?

16. “The long-run industry supply curve in a constant-cost industry graphs as a horizontal line.” Explain.

17. What is the relationship between the long-run supply curve in a constant-cost industry and elasticity?

18. Describe the graph for a long-run supply curve in an increasing-cost industry. Why does it have this slope?

19. Below is a graph of two possible long-run industry supply curves for a purely competitive industry.

Explain why (1) is upsloping and (2) is horizontal.

20. Describe the graph for a long-run supply curve in a decreasing-cost industry. Why does it have this slope?

21. Compare the long-run supply curve for a constant-cost industry, a decreasing-cost industry, and an

increasing-cost industry. Give an example with an explanation for each.

22. What economic conditions are necessary to achieve productive efficiency under pure competition?

23. Draw a graph on the diagram below showing the long-run equilibrium position of a competitive firm.

Write a formula to express the equalities in the graph.

24. What economic conditions are necessary to achieve allocative efficiency under pure competition?

25. Explain what allocative efficiency is and how it is achieved in pure competition.

26. Why does pure competition provide consumers with the largest consumer and producer surpluses?

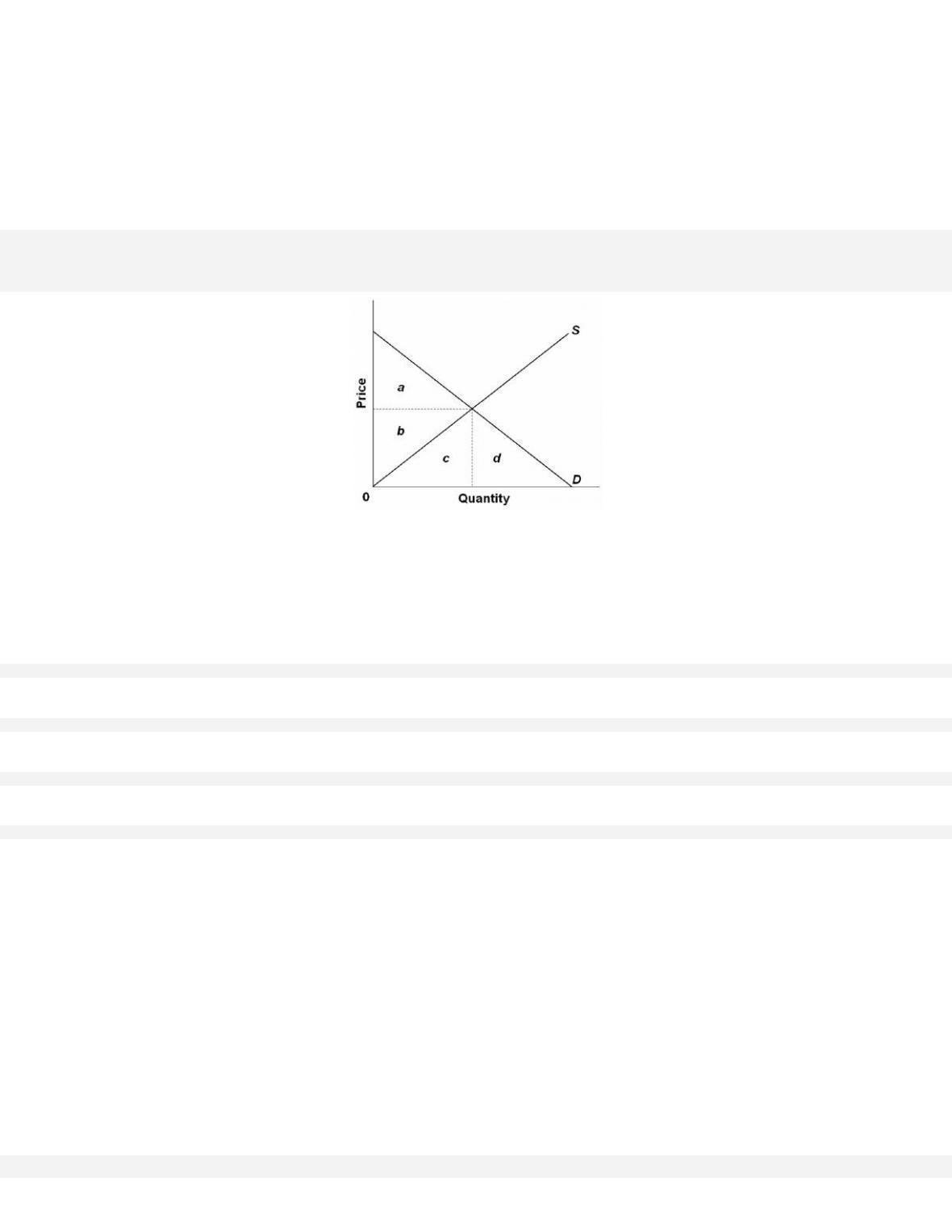

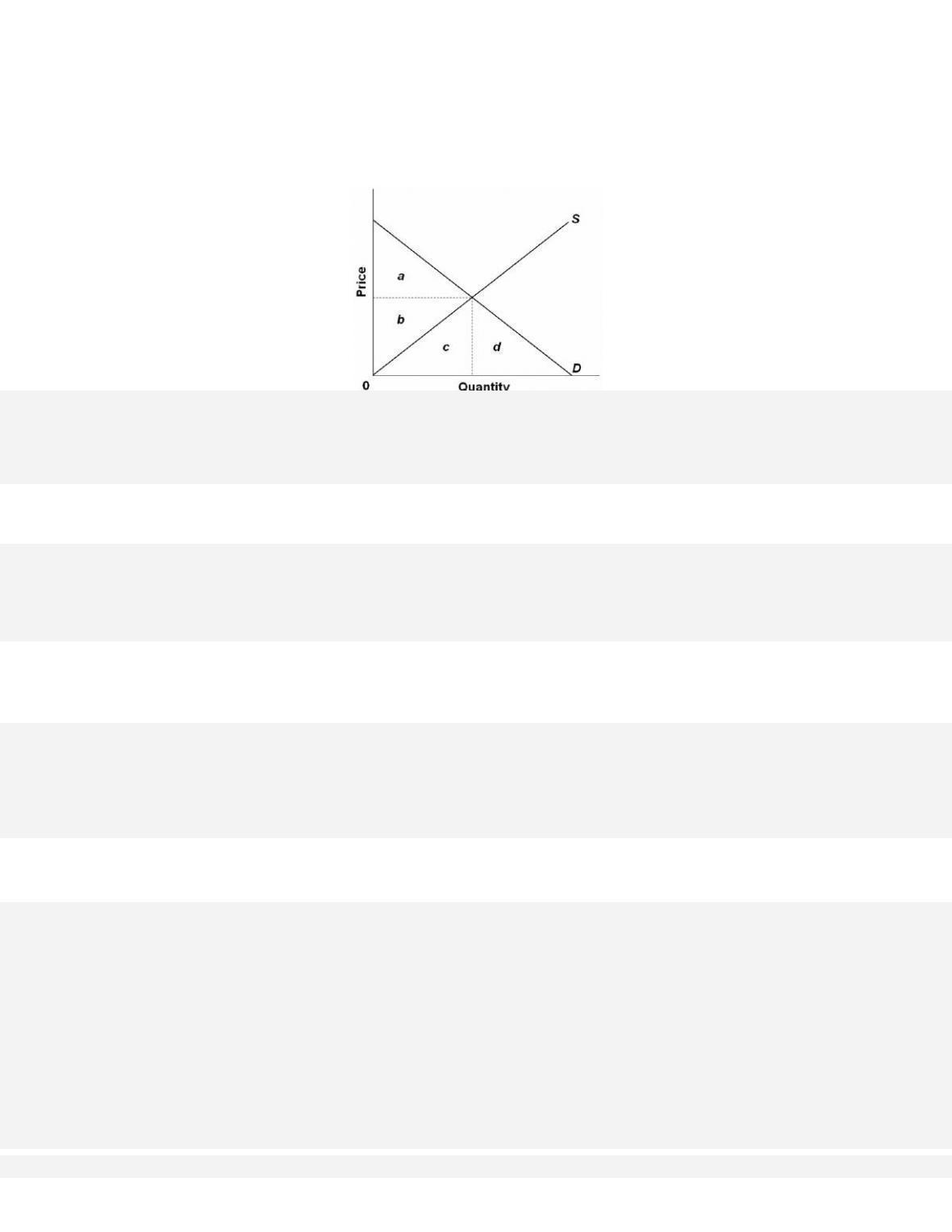

27. Consider the supply and demand graph below to answer three questions: (a) Use a letter to identify the area

of maximum consumer surplus; (b) Use a letter to identify the area of maximum producer surplus; (c) Why

is the output level shown by the vertical dashed line one that is allocatively efficient from a marginal cost

and marginal benefit perspective?

28. How are producer and consumer surpluses maximized in a competitive market?

29. How would a purely competitive industry adjust and restore allocative efficiency when there is an increase

in the demand for a product?

30. How does the “invisible hand” work in a competitive market system?

11–258

31. What are the differences between competition in a purely competitive industry and competition in an

industry with technological advance and innovation?

32. What are two strategies that entrepreneurs use to earn more than the normal profit? Will these strategies

earn economic profits that normally persist over time? Explain.

33. What is the concept of creative destruction? Describe two industry examples and how it has worked over

34. Define creative destruction. Describe the transition of the music listening industry in terms of creative

destruction.

35. (Last Word) Assess the arguments for and against patents in terms of creative destruction.