56) Find the hedge ratio for a call option on £10,000 with a strike price of €12,500. The current

exchange rate is €1.50/£1.00 and in the next period the exchange rate can increase to €2.40/£ or

decrease to €0.9375/€1.00 (i.e. u = 1.6 and d = 1/u = 0.625).

The current interest rates are i€ = 3% and are i£ = 4%.

Choose the answer closest to yours.

A) 5/9

B) 8/13

C) 2/3

D) 3/8

E) none of the options

57) You have written a call option on £10,000 with a strike price of $20,000. The current exchange

rate is $2.00/£1.00 and in the next period the exchange rate can increase to $4.00/£1.00 or decrease

to $1.00/€1.00 (i.e. u = 2 and d = 1/u = 0. 5). The current interest rates are i$ = 3% and are i£ = 2%.

Find the hedge ratio and use it to create a position in the underlying asset that will hedge your

option position.

A) Enter into a short position in a futures contract on £6,666.67

B) Lend the present value of £6,666.67 today at i£ = 2%

C) Enter into a long position in a futures contract on £6,666.67

D) Lending the present value of £6,666.67 today at i£ = 2% or entering into a long position in a

futures contract on £6,666.67 would both work.

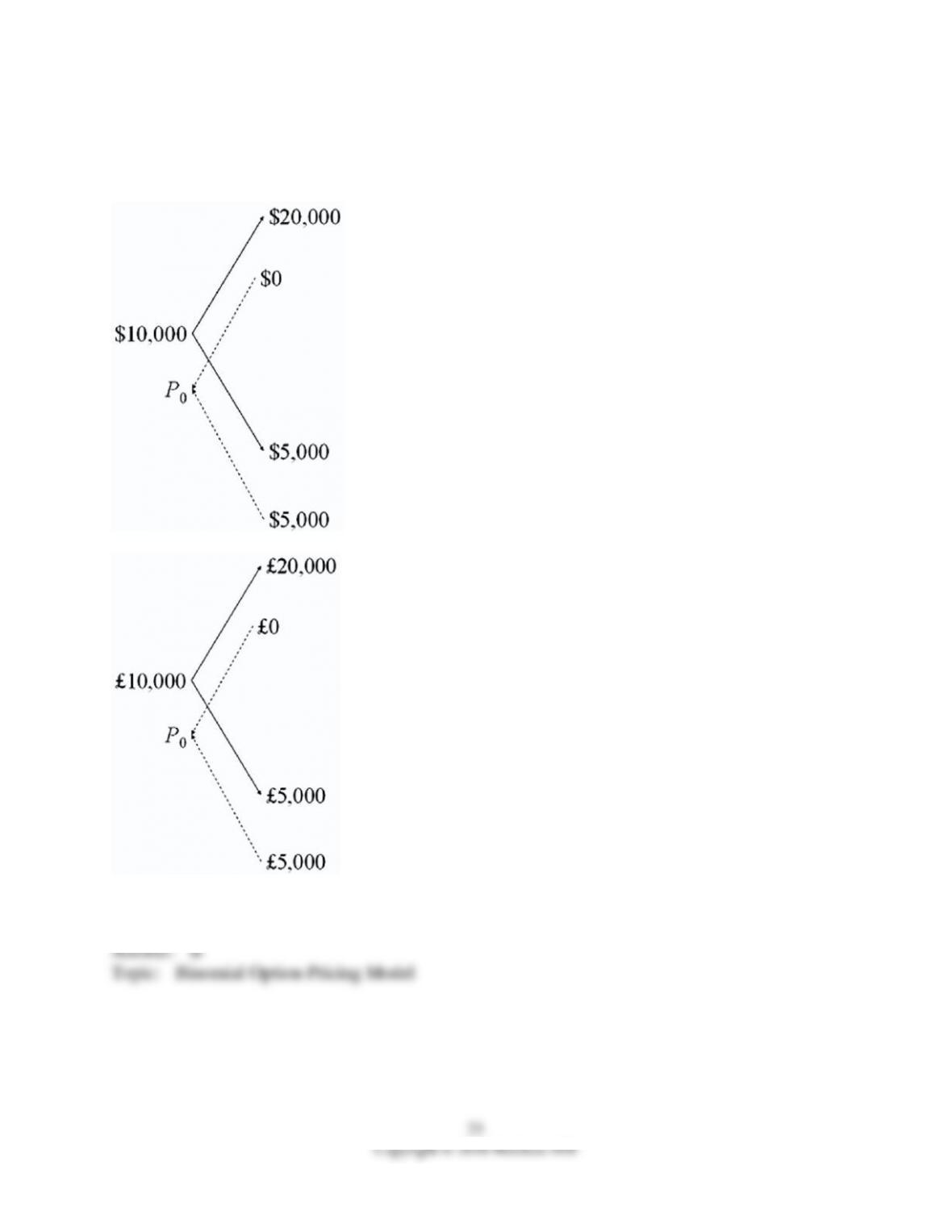

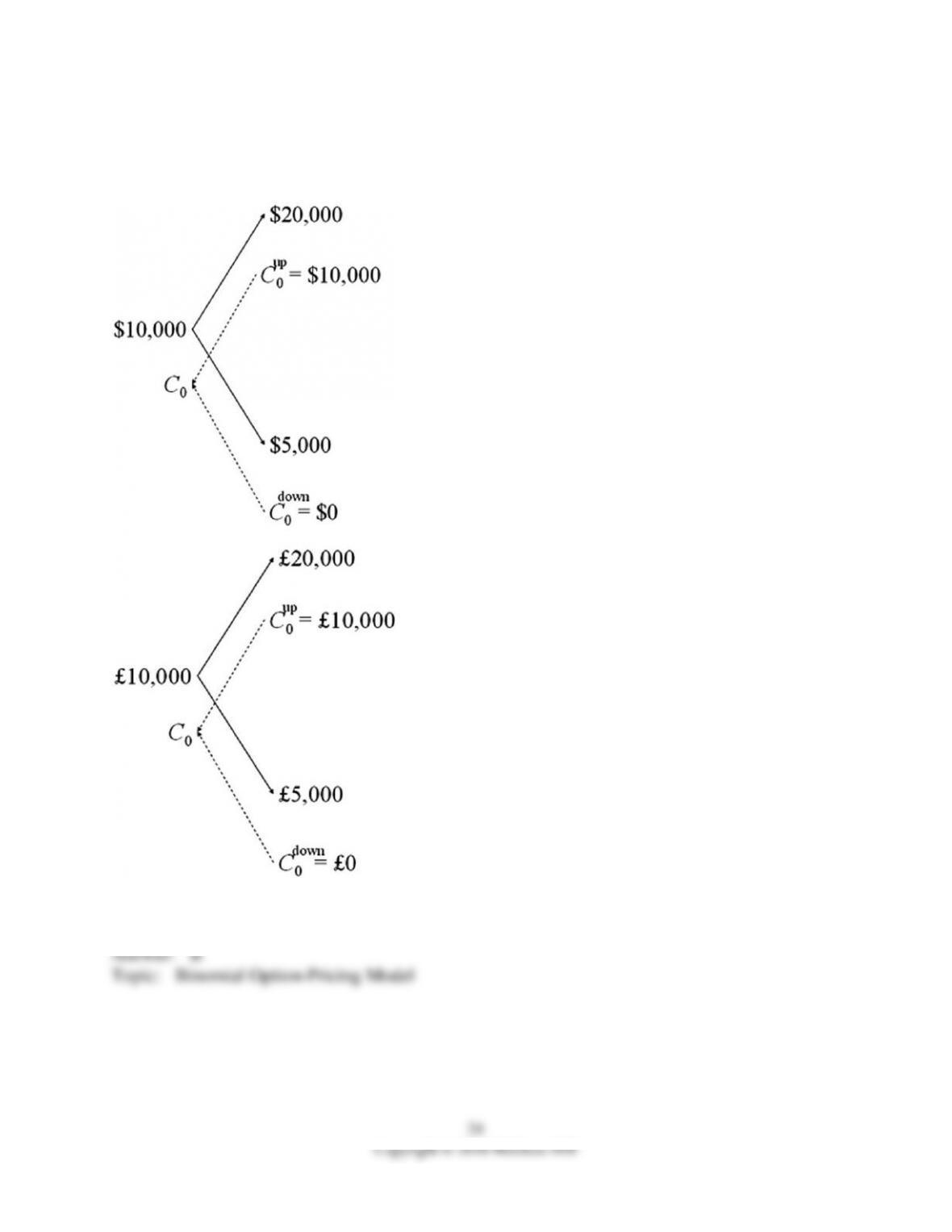

58) Draw the tree for a put option on $20,000 with a strike price of £10,000. The current exchange

rate is £1.00 = $2.00 and in one period the dollar value of the pound will either double or be cut in

half. The current interest rates are i$ = 3% and are i£ = 2%.

A)

B)

C) both of the options

D) none of the options

59) Draw the tree for a call option on $20,000 with a strike price of £10,000. The current exchange

rate is £1.00 = $2.00 and in one period the dollar value of the pound will either double or be cut in

half. The current interest rates are i$ = 3% and are i£ = 2%.

A)

B)

C) both of the options

D) none of the options

60) A binomial call option premium is calculated as

A) C0 = [qCuT + (1 – q)CdT] / (1 + r$)

B) C0 = [qCdT + (1 – q)CuT] / (1 + r$)

C) C0 = [qCuT + (1 – q)CdT] / (1 – r$)

D) C0 = [qCdT + (1 – q)CuT] / (1 – r$)

61) The one-step binomial model assumes that at the end of the option period, the call will have

appreciated to SuT = S0u or depreciated to SdT = S0d. How is u calculated?

A) 1/d

B) e^(σt0.5)

C) both 1/d and e^(σt0.5)

D) none of these options

62) Find the dollar value today of a 1-period at-the-money call option on €10,000. The spot

exchange rate is €1.00 = $1.25. In the next period, the euro can increase in dollar value to $2.00 or

fall to $1.00. The interest rate in dollars is i$ = 27.50%; the interest rate in euro is .

A) $3,308.82

B) $0

C) $3,294.12

D) $4,218.75

63) Suppose that you have written a call option on €10,000 with a strike price in dollars. Suppose

further that the hedge ratio is 1/2. Which of the following would be an appropriate hedge for a

short position in this call option?

A) Buy €5,000 today at today’s spot exchange rate.

B) Agree to buy €5,000 at the maturity of the option at the forward exchange rate for the maturity

of the option that prevails today (i.e., go long in a forward contract on €5,000).

C) Buy the present value of €5,000 discounted at i€ for the maturity of the option.

D) Agree to buy €5,000 at the maturity of the option at the forward exchange rate for the maturity

of the option that prevails today (i.e., go long in a forward contract on €5,000) or buy the present

value of €5,000 discounted at i€ for the maturity of the option.

64) With regard to expiration date,

A) futures contracts do not have delivery dates.

B) forward contracts have standardized delivery dates.

C) futures contracts have tailor-made delivery dates that meet the needs of the investor.

D) futures contracts have standardized delivery dates.

65) With regard to trading location,

A) forward contracts are traded competitively on organized exchanges.

B) futures contracts are traded competitively on organized exchanges.

C) futures contracts are traded by bank dealers via a network of telephones and computerized

dealing systems.

D) none of the options

66) With regard to contractual size,

A) forward contracts are characterized by a standardized amount of the underlying asset.

B) futures contracts are tailor-made to the needs of the participant.

C) futures contracts are characterized by a standardized amount of the underlying asset.

D) none of the options

67) With regard to trading costs,

A) forward contracts involve the bid-ask spread plus the broker’s commission.

B) futures contracts involve the bid-ask spread plus the broker’s commission.

C) futures contracts involve the bid-ask spread plus indirect bank charges via compensating

balance requirements.

D) none of the options

68) Which of the following is correct?

A) The value (in dollars) of a call option on £5,000 with a strike price of $10,000 is equal to the

value (in dollars) of a put option on $10,000 with a strike price of £5,000 only when the spot

exchange rate is $2 = £1.

B) The value (in dollars) of a call option on £5,000 with a strike price of $10,000 is equal to the

value (in dollars) of a put option on $10,000 with a strike price of £5,000.

69) Find the input d1 of the Black-Scholes price of a six-month call option written on €100,000

with a strike price of $1.00 = €1.00. The current exchange rate is $1.25 = €1.00; The U.S. risk-free

rate is 5% over the period and the euro-zone risk-free rate is 4%. The volatility of the underlying

asset is 10.7 percent.

A) d1 = 0.103915

B) d1 = 2.9871

C) d1 = 0.0283

D) none of the options

70) Find the input d1 of the Black-Scholes price of a six-month call option on Japanese yen. The

strike price is $1 = ¥100. The volatility is 25 percent per annum; r$ = 5.5% and r¥ = 6%.

A) d1 = 0.074246

B) d1 = 0.005982

C) d1 = $0.006137/¥

D) none of the options

29

71) The Black-Scholes option pricing formula

A) is used widely in practice, especially by international banks in trading OTC options.

B) is not widely used outside of the academic world.

C) works well enough, but is not used in the real world because no one has the time to flog their

calculator for five minutes on the trading floor.

D) none of the options

72) Find the Black-Scholes price of a six-month call option written on €100,000 with a strike price

of $1.00 = €1.00. The current exchange rate is $1.25 = €1.00; The U.S. risk-free rate is 5 percent

over the period and the euro-zone risk-free rate is 4 percent. The volatility of the underlying asset

is 10.7 percent.

A) Ce = $0.63577

B) Ce = $0.0998

C) Ce = $1.6331

D) none of the options

73) Use the European option pricing formula to find the value of a six-month call option on

Japanese yen. The strike price is $1 = ¥100. The volatility is 25 percent per annum; r$ = 5.5% and

r¥ = 6%.

A) 0.005395

B) 0.005982

C) $0.006137/¥

D) none of the options

74) Empirical tests of the Black-Scholes option pricing formula

A) shows that binomial option pricing is used widely in practice, especially by international banks

in trading OTC options.

B) works well for pricing American currency options that are at-the-money or out-of-the-money.

C) does not do well in pricing in-the-money calls and puts.

D) works well for pricing American currency options that are at-the-money or out-of-the-money,

but does not do well in pricing in-the-money calls and puts.

75) Empirical tests of the Black-Scholes option pricing formula

A) have faced difficulties due to nonsynchronous data.

B) suggest that when using simultaneous price data and incorporating transaction costs they

conclude that the PHLX American currency options are efficiently priced.

C) suggest that the European option-pricing model works well for pricing American currency

options that are at- or out-of-the money, but does not do well in pricing in-the-money calls and

puts.

D) all of the options

76) Consider an option to buy £10,000 for €12,500. In the next period, if the pound appreciates

against the dollar by 37.5 percent then the euro will appreciate against the dollar by ten percent. On

the other hand, the euro could depreciate against the pound by 20 percent.

Big hint: don’t round, keep exchange rates out to at least 4 decimal places.

Spot Rates

Risk-free Rates

S0($/€)

$1.60 = €1.00

i$

3.00%

S0($/£)

$2.00 = £1.00

i€

4.00%

S0(€/£)

€1.25 = £1.00

i£

4.00%

Calculate the current €/£ spot exchange rate.

77) Consider an option to buy £10,000 for €12,500. In the next period, if the pound appreciates

against the dollar by 37.5 percent then the euro will appreciate against the dollar by ten percent. On

the other hand, the euro could depreciate against the pound by 20 percent.

Big hint: don’t round, keep exchange rates out to at least 4 decimal places.

Spot Rates

Risk-free Rates

S0($/€)

$1.60 = €1.00

i$

3.00%

S0($/£)

$2.00 = £1.00

i€

4.00%

S0(€/£)

€1.25 = £1.00

i£

4.00%

Find the risk neutral probability of an “up” move.

78) Consider an option to buy £10,000 for €12,500. In the next period, if the pound appreciates

against the dollar by 37.5 percent then the euro will appreciate against the dollar by ten percent. On

the other hand, the euro could depreciate against the pound by 20 percent.

Big hint: don’t round, keep exchange rates out to at least 4 decimal places.

Spot Rates

Risk-free Rates

S0($/€)

$1.60 = €1.00

i$

3.00%

S0($/£)

$2.00 = £1.00

i€

4.00%

S0(€/£)

€1.25 = £1.00

i£

4.00%

USING RISK NEUTRAL VALUATION (i.e., the binomial option pricing model) find the value

of the call (in euro).

79) Consider an option to buy £10,000 for €12,500. In the next period, if the pound appreciates

against the dollar by 37.5 percent then the euro will appreciate against the dollar by ten percent. On

the other hand, the euro could depreciate against the pound by 20 percent.

Big hint: don’t round, keep exchange rates out to at least 4 decimal places.

Spot Rates

Risk-free Rates

S0($/€)

$1.60 = €1.00

i$

3.00%

S0($/£)

$2.00 = £1.00

i€

4.00%

S0(€/£)

€1.25 = £1.00

i£

4.00%

Calculate the hedge ratio.

80) Consider an option to buy £10,000 for €12,500. In the next period, if the pound appreciates

against the dollar by 37.5 percent then the euro will appreciate against the dollar by ten percent. On

the other hand, the euro could depreciate against the pound by 20 percent.

Big hint: don’t round, keep exchange rates out to at least 4 decimal places.

Spot Rates

Risk-free Rates

S0($/€)

$1.60 = €1.00

i$

3.00%

S0($/£)

$2.00 = £1.00

i€

4.00%

S0(€/£)

€1.25 = £1.00

i£

4.00%

State the composition of the replicating portfolio; your answer should contain “trading orders” of

what to buy and what to sell at time zero.

81) Consider an option to buy £10,000 for €12,500. In the next period, if the pound appreciates

against the dollar by 37.5 percent then the euro will appreciate against the dollar by ten percent. On

the other hand, the euro could depreciate against the pound by 20 percent.

Big hint: don’t round, keep exchange rates out to at least 4 decimal places.

Spot Rates

Risk-free Rates

S0($/€)

$1.60 = €1.00

i$

3.00%

S0($/£)

$2.00 = £1.00

i€

4.00%

S0(€/£)

€1.25 = £1.00

i£

4.00%

Find the value today of your replicating today’s portfolio in euro.

82) Consider an option to buy £10,000 for €12,500. In the next period, if the pound appreciates

against the dollar by 37.5 percent then the euro will appreciate against the dollar by ten percent. On

the other hand, the euro could depreciate against the pound by 20 percent.

Big hint: don’t round, keep exchange rates out to at least 4 decimal places.

Spot Rates

Risk-free Rates

S0($/€)

$1.60 = €1.00

i$

3.00%

S0($/£)

$2.00 = £1.00

i€

4.00%

S0(€/£)

€1.25 = £1.00

i£

4.00%

If the call finishes out-of-the-money what is your replicating portfolio cash flow?

83) Consider an option to buy £10,000 for €12,500. In the next period, if the pound appreciates

against the dollar by 37.5 percent then the euro will appreciate against the dollar by ten percent. On

the other hand, the euro could depreciate against the pound by 20 percent.

Big hint: don’t round, keep exchange rates out to at least 4 decimal places.

Spot Rates

Risk-free Rates

S0($/€)

$1.60 = €1.00

i$

3.00%

S0($/£)

$2.00 = £1.00

i€

4.00%

S0(€/£)

€1.25 = £1.00

i£

4.00%

If the call finishes in-the-money what is your replicating portfolio cash flow?

84) Consider an option to buy £10,000 for €12,500. In the next period, if the pound appreciates

against the dollar by 37.5 percent then the euro will appreciate against the dollar by ten percent. On

the other hand, the euro could depreciate against the pound by 20 percent.

Big hint: don’t round, keep exchange rates out to at least 4 decimal places.

Spot Rates

Risk-free Rates

S0($/€)

$1.60 = €1.00

i$

3.00%

S0($/£)

$2.00 = £1.00

i€

4.00%

S0(€/£)

€1.25 = £1.00

i£

4.00%

FInd the value of the call.

85) Consider an option to buy €12,500 for £10,000. In the next period, the euro can strengthen

against the pound by 25 percent (i.e., each euro will buy 25 percent more pounds) or weaken by 20

percent.

Big hint: don’t round, keep exchange rates out to at least 4 decimal places.

Spot Rates

Risk-Free Rates

S0($/€)

$1.60 = €1.00

i$

3.00%

S0($/£)

$2.00 = £1.00

i€

4.00%

S0(€/£)

€1.25 = £1.00

i£

4.00%

Calculate the current €/£ spot exchange rate.

86) Consider an option to buy €12,500 for £10,000. In the next period, the euro can strengthen

against the pound by 25 percent (i.e., each euro will buy 25 percent more pounds) or weaken by 20

percent.

Big hint: don’t round, keep exchange rates out to at least 4 decimal places.

Spot Rates

Risk-Free Rates

S0($/€)

$1.60 = €1.00

i$

3.00%

S0($/£)

$2.00 = £1.00

i€

4.00%

S0(€/£)

€1.25 = £1.00

i£

4.00%

Find the risk neutral probability of an “up” move.

87) Consider an option to buy €12,500 for £10,000. In the next period, the euro can strengthen

against the pound by 25 percent (i.e., each euro will buy 25 percent more pounds) or weaken by 20

percent.

Big hint: don’t round, keep exchange rates out to at least 4 decimal places.

Spot Rates

Risk-Free Rates

S0($/€)

$1.60 = €1.00

i$

3.00%

S0($/£)

$2.00 = £1.00

i€

4.00%

S0(€/£)

€1.25 = £1.00

i£

4.00%

USING RISK NEUTRAL VALUATION, find the value of the call (in pounds)

88) Consider an option to buy €12,500 for £10,000. In the next period, the euro can strengthen

against the pound by 25 percent (i.e., each euro will buy 25 percent more pounds) or weaken by 20

percent.

Big hint: don’t round, keep exchange rates out to at least 4 decimal places.

Spot Rates

Risk-Free Rates

S0($/€)

$1.60 = €1.00

i$

3.00%

S0($/£)

$2.00 = £1.00

i€

4.00%

S0(€/£)

€1.25 = £1.00

i£

4.00%

Calculate the hedge ratio.

89) Consider an option to buy €12,500 for £10,000. In the next period, the euro can strengthen

against the pound by 25 percent (i.e., each euro will buy 25 percent more pounds) or weaken by 20

percent.

Big hint: don’t round, keep exchange rates out to at least 4 decimal places.

Spot Rates

Risk-Free Rates

S0($/€)

$1.60 = €1.00

i$

3.00%

S0($/£)

$2.00 = £1.00

i€

4.00%

S0(€/£)

€1.25 = £1.00

i£

4.00%

State the composition of the replicating portfolio; your answer should contain “trading orders” of

what to buy and what to sell at time zero.

90) Consider an option to buy €12,500 for £10,000. In the next period, the euro can strengthen

against the pound by 25 percent (i.e., each euro will buy 25 percent more pounds) or weaken by 20

percent.

Big hint: don’t round, keep exchange rates out to at least 4 decimal places.

Spot Rates

Risk-Free Rates

S0($/€)

$1.60 = €1.00

i$

3.00%

S0($/£)

$2.00 = £1.00

i€

4.00%

S0(€/£)

€1.25 = £1.00

i£

4.00%

Find the cost today of your hedge portfolio in pounds.

91) Consider an option to buy €12,500 for £10,000. In the next period, the euro can strengthen

against the pound by 25 percent (i.e., each euro will buy 25 percent more pounds) or weaken by 20

percent.

Big hint: don’t round, keep exchange rates out to at least 4 decimal places.

Spot Rates

Risk-Free Rates

S0($/€)

$1.60 = €1.00

i$

3.00%

S0($/£)

$2.00 = £1.00

i€

4.00%

S0(€/£)

€1.25 = £1.00

i£

4.00%

If the call finishes out-of-the-money what is your portfolio cash flow?

92) Consider an option to buy €12,500 for £10,000. In the next period, the euro can strengthen

against the pound by 25 percent (i.e., each euro will buy 25 percent more pounds) or weaken by 20

percent.

Big hint: don’t round, keep exchange rates out to at least 4 decimal places.

Spot Rates

Risk-Free Rates

S0($/€)

$1.60 = €1.00

i$

3.00%

S0($/£)

$2.00 = £1.00

i€

4.00%

S0(€/£)

€1.25 = £1.00

i£

4.00%

If the call finishes in-the-money what is your portfolio cash flow?

93) Consider an option to buy €12,500 for £10,000. In the next period, the euro can strengthen

against the pound by 25 percent (i.e., each euro will buy 25 percent more pounds) or weaken by 20

percent.

Big hint: don’t round, keep exchange rates out to at least 4 decimal places.

Spot Rates

Risk-Free Rates

S0($/€)

$1.60 = €1.00

i$

3.00%

S0($/£)

$2.00 = £1.00

i€

4.00%

S0(€/£)

€1.25 = £1.00

i£

4.00%

Find the value of the call.

94) Find the dollar value today of a 1-period at-the-money call option on ¥300,000. The spot

exchange rate is ¥100 = $1.00. In the next period, the yen can increase in dollar value by 15 percent

or decrease by 15 percent. The risk-free rate in dollars is i$ = 5%; The risk-free rate in yen is i¥ =

1%.