67) Restate the following one-, three-, and six-month outright forward American term bid-ask

quotes in forward points:

S($/SFr)

=

0.8500

−

0.8505

F1($/SFr)

=

0.8505

−

0.8505

F3($/SFr)

=

0.8510

−

0.8520

F6($/SFr)

=

0.8515

−

0.8530

A)

Forward Point Quotations

One-Month

05-05

Three-Month

10-15

Six-Month

15-25

B)

Forward Point Quotations

One-Month

05-05

Three-Month

05-10

Six-Month

05-10

C)

Forward Point Quotations

One-Month

00-05

Three-Month

05-10

Six-Month

05-10

D) none of the options

68) If one has agreed to buy a foreign exchange forward,

A) you have a short position in the forward contract.

B) you have a long position in the forward contract.

C) until the exchange rate moves, you haven’t made money, so you’re neither short nor long.

D) you have a long position in the spot market.

69) The current spot exchange rate is $1.55/€ and the three–month forward rate is $1.50/€. You

enter into a short position on €1,000. At maturity, the spot exchange rate is $1.60/€. How much

have you made or lost?

A) Lost $100

B) Made €100

C) Lost $50

D) Made $150

70) The current spot exchange rate is $1.55/€ and the three–month forward rate is $1.50/€. Based

on your analysis of the exchange rate, you are confident that the spot exchange rate will be $1.52/€

in three months. Assume that you would like to buy or sell €1,000,000. What actions do you need

to take to speculate in the forward market?

A) Take a long position in a forward contract on €1,000,000 at $1.50/€.

B) Take a short position in a forward contract on €1,000,000 at $1.50/€.

C) Buy euro today at the spot rate, sell them forward.

D) Sell euro today at the spot rate, buy them forward.

71) The current spot exchange rate is $1.45/€ and the three–month forward rate is $1.55/€. Based

upon your economic forecast, you are pretty confident that the spot exchange rate will be $1.50/€

in three months. Assume that you would like to buy or sell €100,000. What actions would you take

to speculate in the forward market? How much will you make if your prediction is correct?

A) Take a short position in a forward. If you’re right you will make $15,000.

B) Take a long position in a forward contract on euro. If you’re right you will make $5,000.

C) Take a short position in a forward contract on euro. If you’re right you will make $5,000.

D) Take a long position in a forward contract on euro. If you’re right you will make $15,000.

72) Consider a trader who takes a long position in a six-month forward contract on the euro. The

forward rate is $1.75 = €1.00; the contract size is €62,500. At the maturity of the contract the spot

exchange rate is $1.65 = €1.00.

A) The trader has lost $625.

B) The trader has lost $6,250.

C) The trader has made $6,250.

D) The trader has lost $66,287.88.

73) The current spot exchange rate is $1.55/€ and the three–month forward rate is $1.50/€. Based

on your analysis of the exchange rate, you are confident that the spot exchange rate will be $1.62/€

in three months. Assume that you would like to buy or sell €1,000,000. What actions do you need

to take to speculate in the forward market? What is the expected dollar profit from speculation?

A) Sell €1,000,000 forward for $1.50/€.

B) Buy €1,000,000 forward for $1.50/€.

C) Wait three months, if your forecast is correct buy €1,000,000 at $1.52/€.

D) Buy €1,000,000 today at $1.55/€; wait three months, if your forecast is correct sell €1,000,000

at $1.62/€.

74) The current spot exchange rate is $1.50/€ and the three–month forward rate is $1.55/€. Based

on your analysis of the exchange rate, you are confident that the spot exchange rate will be $1.62/€

in three months. Assume that you would like to buy or sell €1,000,000. What actions do you need

to take to speculate in the forward market? What is the expected dollar profit from speculation?

A) Sell €1,000,000 forward for $1.50/€.

B) Buy €1,000,000 forward for $1.55/€.

C) Wait three months, if your forecast is correct buy €1,000,000 at $1.62/€.

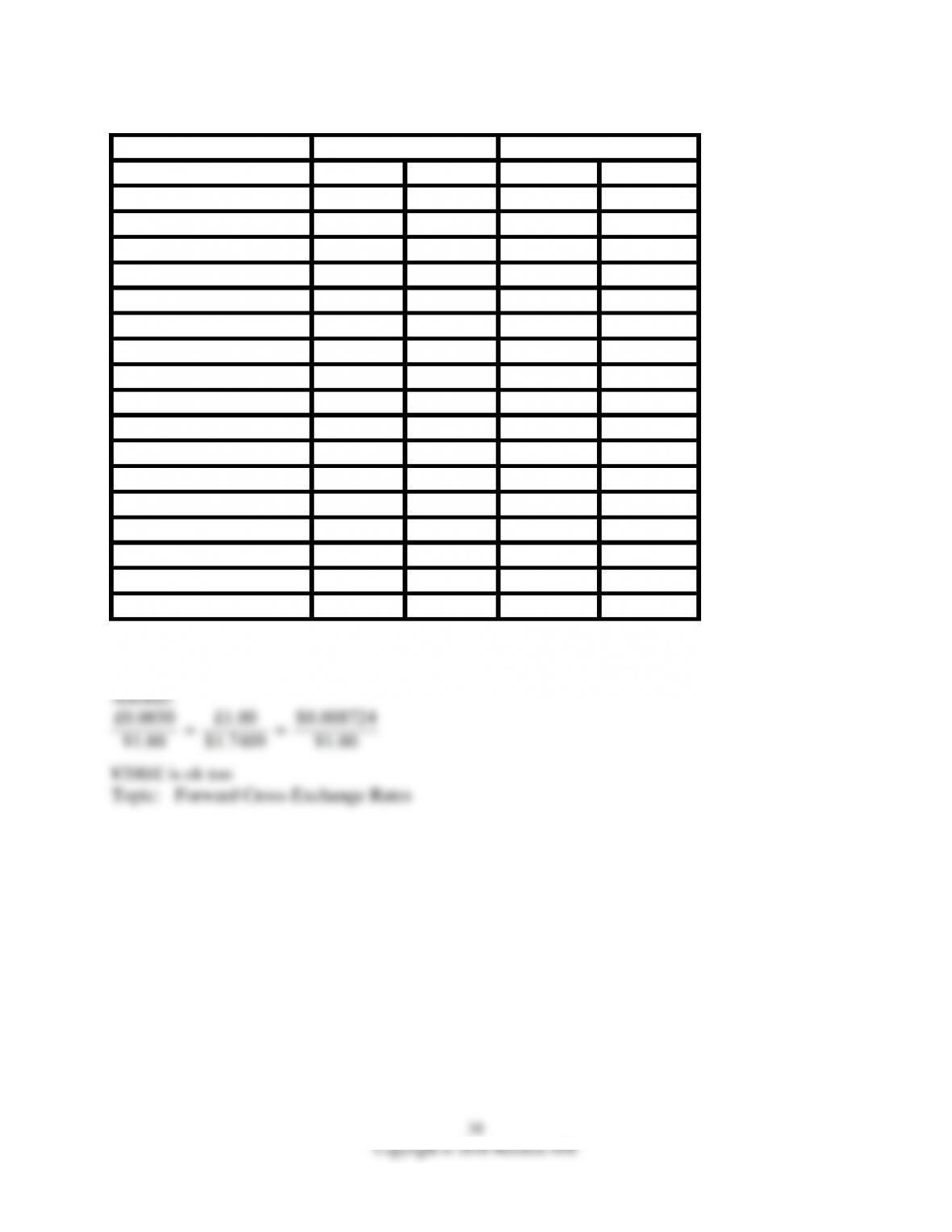

D) Buy €1,000,000 today at $1.50/€; wait three months, if your forecast is correct sell €1,000,000

at $1.62/€.

75) Which of the following are correct?

A) (j / k) =

B) (j / k) =

C) (k / j) =

D) all of the options

76) Which of the following are correct?

A) (j / k) =

B) (j / k) =

C) (k / j) =

D) all of the options

77) Which of the following are correct?

A) (j / k) =

B) (j / k) =

C) (j / k) =

D) all of the options

78) Which of the following are correct?

A) (k / j) =

B) (k / j) =

C) (k / j) =

D) all of the options

79) When a currency trades at a premium in the forward market

A) the exchange rate is more than one dollar (e.g., €1.00 = $1.28).

B) the exchange rate is less than one dollar.

C) the forward rate is less than the spot rate.

D) the forward rate is more than the spot rate.

80) When a currency trades at a discount in the forward market

A) the forward rate is less than the spot rate.

B) the forward rate is more than the spot rate.

C) the forward exchange rate is less than one dollar (e.g. €1.00 = $0.928).

D) the exchange rate is less than it was yesterday.

81) The SF/$ spot exchange rate is SF1.25/$ and the 180 day forward exchange rate is SF1.30/$.

The forward premium (discount) is

A) the dollar trading at an 8% premium to the Swiss franc for delivery in 180 days.

B) the dollar trading at a 4% premium to the Swiss franc for delivery in 180 days.

C) the dollar trading at an 8% discount to the Swiss franc for delivery in 180 days.

D) the dollar trading at a 4% discount to the Swiss franc for delivery in 180 days.

82) The €/$ spot exchange rate is $1.50/€ and the 120 day forward exchange rate is 1.45/€. The

forward premium (discount) is

A) the dollar trading at an 8% premium to the euro for delivery in 120 days.

B) the dollar trading at a 5% premium to the Swiss franc for delivery in 120 days.

C) the dollar trading at a 10% discount to the euro for delivery in 120 days.

D) the dollar trading at a 5% discount to the euro for delivery in 120 days.

83) The €/$ spot exchange rate is $1.50/€ and the 90-day forward premium is 10 percent. Find the

90-day forward price.

A) $1.65/€

B) $1.50375/€

C) $1.9125/€

D) none of the options

84) The SF/$ spot exchange rate is SF1.25/$ and the 180 day forward premium is 8 percent. What

is the outright 180 day forward exchange rate?

A) SF1.30/$

B) SF1.35/$

C) SF6.25/$

D) none of the options

85) The SF/$ 180-day forward exchange rate is SF1.30/$ and the 180 day forward premium is 8

percent. What is the outright spot exchange rate?

A) SF1.30/$

B) SF1.35/$

C) SF1.25/$

D) none of the options

86) Consider the following spot and forward rate quotations for the Swiss franc.

S($/SFr) = 0.85

F1($/SFr) = 0.86

F2($/SFr) = 0.87

F3($/SFr) =0.88

Which of the following is true?

A) The Swiss franc is definitely going to be worth more dollars in six months.

B) The Swiss franc is probably going to be worth less in dollars in six months.

C) The Swiss franc is trading at a forward discount.

D) The Swiss franc is trading at a forward premium.

87) Consider the following spot and forward rate quotations for the Swiss franc.

S($/SFr) = 0.85

F1($/SFr) = 0.86

F2($/SFr) = 0.87

F3($/SFr) =0.88

Calculate the 3-month forward premium in American terms. Assume 30-360 pricing convention.

A) 0.353.

B) 0.4235.

C) 0.1364.

D) 0.1412.

88) Swap transactions

A) involve the simultaneous sale (or purchase) of spot foreign exchange against a forward

purchase (or sale) of approximately an equal amount of the foreign currency.

B) account for about half of Interbank FX trading.

C) involve trades of one foreign currency for another without going through the U.S. dollar.

D) all of the options

89) As a rule, when the interest rate of the foreign currency is greater than the interest rate of the

quoting currency,

A) the outright forward rate is less than the spot exchange rate.

B) the outright forward rate is more than the spot exchange rate.

C) the currency will trade at a premium in the forward contract.

D) none of the options

90) Bank dealers in conversations among themselves use a shorthand notation to quote bid and ask

forward prices in terms of forward points. This is convenient because

A) forward points may change faster than spot and forward quotes.

B) forward points may remain constant for long periods of time, even if the spot rates change

frequently.

C) in swap transactions where the trader is attempting to minimize currency exposure, the actual

spot and outright forward rates are often of no consequence.

D) forward points may remain constant for long periods of time, even if the spot rates change

frequently, and in swap transactions where the trader is attempting to minimize currency exposure,

the actual spot and outright forward rates are often of no consequence.

91) Bank dealers in conversations among themselves use a shorthand notation to quote bid and ask

forward prices in terms of forward points. Complete the following table:

Spot

Forward Point Quotations

1.9072-1.9077

One-month

32-30

Three-month

57-54

1.9015-1.9023

Six-month

145-138

1.8927-1.8939

A) 1.9040–1.9047

B) 1.9042–1.9049

C) 1.9032–1.9030

D) none of the options

92) An exchange-traded fund (ETF) is

A) the same thing as a mutual fund.

B) a portfolio of financial assets in which shares representing fractional ownership of the fund are

sold and redeemed by the fund sponsor.

C) a portfolio of financial assets in which shares representing fractional ownership of the fund

trade on an organized exchange.

D) none of the options

93) The largest and most active financial market in the world is

A) the Fleet Street Exchange in London.

B) the NYSE in New York.

C) the FX market.

D) none of the options

94) Nondollar currency transactions

A) are priced by looking at the price that must exist to eliminate arbitrage.

B) allow for triangular arbitrage opportunities to keep the currency dealers employed.

C) are only for poor people who don’t have dollars.

D) none of the options

31

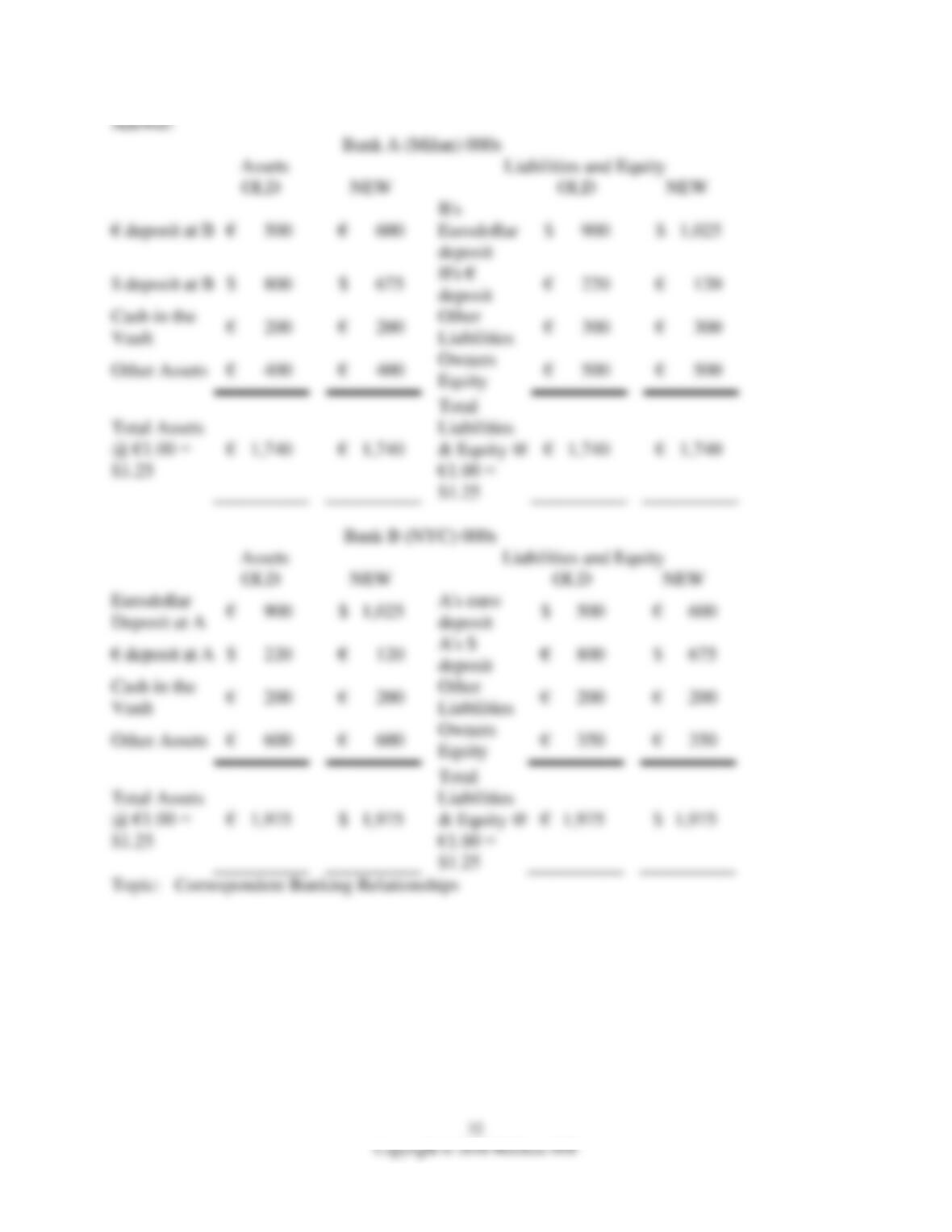

95) Consider the balance sheets of Bank A and Bank B. Bank A is in Milan, Bank B is in New

York. The current exchange rate is €1.00 = $1.25. Show the correct balances in each account if a

currency trader employed at Bank A buys €100,000 from a currency trader at Bank B for $125,000

using its correspondent relationship with Bank B.

Bank A (Milan) 000s

Assets

Liabilities and Equity

OLD

NEW

OLD

NEW

€ deposit at B

€

500

B’s

Eurodollar

deposit

$

900

$ deposit at B

$

800

B’s €

deposit

€

220

Cash in the

Vault

€

200

€

200

Other

Liabilities

€

300

€

300

Other Assets

€

400

€

400

Owners

Equity

€

500

€

500

Total Assets

@ €1.00 =

$1.25

€

1,740

Total

Liabilities

& Equity @

€1.00 =

$1.25

€

1,740

Bank B (NYC) 000s

Assets

Liabilities and Equity

OLD

NEW

OLD

NEW

Eurodollar

Deposit at A

€

900

A’s euro

deposit

$

500

€ deposit at A

$

220

A’s $

deposit

€

800

Cash in the

Vault

€

200

€

200

Other

Liabilities

€

200

€

200

Other Assets

€

600

€

600

Owners

Equity

€

350

€

350

Total Assets

@ €1.00 =

$1.25

€

1,975

Total

Liabilities

& Equity @

€1.00 =

$1.25

€

1,975

32

Copyright © 2018 McGraw-Hill

Answer:

Bank A (Milan) 000s

Assets

Liabilities and Equity

OLD

NEW

OLD

NEW

€ deposit at B

€

500

€

600

B’s

Eurodollar

deposit

$

900

$

1,025

$ deposit at B

$

800

$

675

B’s €

deposit

€

220

€

120

Cash in the

Vault

€

200

€

200

Other

Liabilities

€

300

€

300

Other Assets

€

400

€

400

Owners

Equity

€

500

€

500

Total Assets

@ €1.00 =

$1.25

€

1,740

€

1,740

Total

Liabilities

& Equity @

€1.00 =

$1.25

€

1,740

€

1,740

Bank B (NYC) 000s

Assets

Liabilities and Equity

OLD

NEW

OLD

NEW

Eurodollar

Deposit at A

€

900

$

1,025

A’s euro

deposit

$

500

€

600

€ deposit at A

$

220

€

120

A’s $

deposit

€

800

$

675

Cash in the

Vault

€

200

€

200

Other

Liabilities

€

200

€

200

Other Assets

€

600

€

600

Owners

Equity

€

350

€

350

Total Assets

@ €1.00 =

$1.25

€

1,975

$

1,975

Total

Liabilities

& Equity @

€1.00 =

$1.25

€

1,975

$

1,975

Topic: Correspondent Banking Relationships

33

96) Consider the balance sheets of Bank A and Bank B. Bank A is in London, Bank B is in New

York. The current exchange rate is £1.00 = $2.00. Show the correct balances in each account if a

currency trader employed at Bank A buys £45,000 from a currency trader at Bank B for $90,000

using its correspondent relationship with Bank B.

Bank A (London) 000s

Assets

Liabilities and Equity

OLD

NEW

OLD

NEW

£ deposit at B

£

500

B’s Eurodollar

deposit

$

850

$ deposit at B

$

1,000

B’s £ deposit

£

100

Cash in the

Vault

£

200

Other Liabilities

£

300

Other Assets

£

400

Owners Equity

£

775

Total Assets

£

1,600

Total Liabilities

& Equity

£

1,600

Bank B (NYC) 000s

Assets

Liabilities and Equity

OLD

NEW

OLD

NEW

Eurodollar

Deposit at A

$

850

A’s £ deposit

£

500

£ deposit at A

£

100

A’s $ deposit

$

1,000

Cash in the Vault

$

200

Other

Liabilities

$

200

Other Assets

$

1,000

Owners Equity

$

50

Total Assets

$

2,250

Total

Liabilities &

Equity

$

2,250

34

Copyright © 2018 McGraw-Hill

Answer:

Bank A (London) 000s

Assets

Liabilities and Equity

OLD

NEW

OLD

NEW

£ deposit at

B

£

500

£

545

B’s

Eurodollar

deposit

$

850

$

940

$ deposit at

B

$

1,000

$

910

B’s £ deposit

£

100

£

55

Cash in the

Vault

£

200

£

200

Other

Liabilities

£

300

£

300

Other

Assets

£

400

£

400

Owners

Equity

£

775

£

775

Total Assets

£

1,600

£

1,600

Total

Liabilities &

Equity

£

1,600

£

1,600

Bank B (NYC) 000s

Assets

Liabilities and Equity

OLD

NEW

OLD

NEW

Eurodollar

Deposit at A

$

850

$

940

A’s £

deposit

£

500

£

545

£ deposit at A

£

100

£

55

A’s $

deposit

$

1,000

$

910

Cash in the

Vault

$

200

$

200

Other

Liabilities

$

200

$

200

Other Assets

$

1,000

$

1,000

Owners

Equity

$

50

$

50

Total Assets

$

2,250

$

2,250

Total

Liabilities

& Equity

$

2,250

$

2,250

Topic: Correspondent Banking Relationships

35

97) Consider the balance sheets of Bank A and Bank B. Bank A is in London, Bank B is in New

York. The current exchange rate is & pound;1.00 = $2.00. Show the correct balances in each

account if a currency trader employed at Bank A buys £50,000 from a currency trader at Bank B

for $100,000 using its correspondent relationship with Bank B.

Bank A (London) 000s

Assets

Liabilities and Equity

OLD

NEW

OLD

NEW

£ deposit at B

£

500

B’s Eurodollar

deposit

$

850

$ deposit at B

$

1,000

B’s £ deposit

£

100

Cash in the

Vault

£

200

Other Liabilities

£

300

Other Assets

£

400

Owners Equity

£

775

Total Assets

£

1,600

Total Liabilities

& Equity

£

1,600

Bank B (NYC) 000s

Assets

Liabilities and Equity

OLD

NEW

OLD

NEW

Eurodollar

Deposit at A

$

850

A’s £ deposit

£

500

£ deposit at A

£

100

A’s $ deposit

$

1,000

Cash in the Vault

$

200

Other

Liabilities

$

200

Other Assets

$

1,000

Owners Equity

$

50

Total Assets

$

2,250

Total

Liabilities &

Equity

$

2,250

36

Copyright © 2018 McGraw-Hill

Answer:

Bank A (London) 000s

Assets

Liabilities and Equity

OLD

NEW

OLD

NEW

£ deposit at

B

£

500

£

550

B’s

Eurodollar

deposit

$

850

$

950

$ deposit at

B

$

1,000

$

900

B’s £ deposit

£

100

£

50

Cash in the

Vault

£

200

£

200

Other

Liabilities

£

300

£

300

Other

Assets

£

400

£

400

Owners

Equity

£

775

£

775

Total Assets

£

1,600

£

1,600

Total

Liabilities &

Equity

£

1,600

£

1,600

Bank B (NYC) 000s

Assets

Liabilities and Equity

OLD

NEW

OLD

NEW

Eurodollar

Deposit at A

$

850

$

950

A’s £

deposit

£

500

£

550

£ deposit at A

£

100

£

50

A’s $

deposit

$

1,000

$

900

Cash in the

Vault

$

200

$

200

Other

Liabilities

$

200

$

200

Other Assets

$

1,000

$

1,000

Owners

Equity

$

50

$

50

Total Assets

$

2,250

$

2,250

Total

Liabilities

& Equity

$

2,250

$

2,250

Topic: Correspondent Banking Relationships

98)

Country

USD equiv.

Currency per USD

Tuesday

Monday

Tuesday

Monday

U.K. (Pound)

1.7368

1.7424

0.5758

0.5739

1 Month Forward

1.7369

1.7425

0.5757

0.5739

3 Months Forward

1.738

1.7434

0.5754

0.5736

6 Months Forward

1.7409

1.7461

0.5744

0.5727

Canada (Dollar)

0.8667

0.8653

1.1538

1.1557

1 Month Forward

0.8674

0.866

1.1529

1.1547

3 Months Forward

0.8688

0.8674

1.151

1.1529

6 Months Forward

0.8708

0.8693

1.1484

1.1504

Japan (Yen)

0.008518

0.008495

117.3985

117.7163

1 Month Forward

0.008548

0.008525

116.0631

117.3021

3 Months Forward

0.008616

0.008593

116.0631

116.3738

6 Months Forward

0.008724

0.0087

114.6263

114.9425

Switzerland (Franc)

0.7648

0.7652

1.3075

1.3068

1 Month Forward

0.767

0.7674

1.3038

1.3031

3 Months Forward

0.7718

0.7722

1.2957

1.295

6 Months Forward

0.7791

0.7794

1.2835

1.283

Euro

1.2000

1.1906

0.8333

0.8399

Using the table, what is the Canadian dollar–euro spot cross-exchange rate?

99)

Country

USD equiv.

Currency per USD

Tuesday

Monday

Tuesday

Monday

U.K. (Pound)

1.7368

1.7424

0.5758

0.5739

1 Month Forward

1.7369

1.7425

0.5757

0.5739

3 Months Forward

1.738

1.7434

0.5754

0.5736

6 Months Forward

1.7409

1.7461

0.5744

0.5727

Canada (Dollar)

0.8667

0.8653

1.1538

1.1557

1 Month Forward

0.8674

0.866

1.1529

1.1547

3 Months Forward

0.8688

0.8674

1.151

1.1529

6 Months Forward

0.8708

0.8693

1.1484

1.1504

Japan (Yen)

0.008518

0.008495

117.3985

117.7163

1 Month Forward

0.008548

0.008525

116.0631

117.3021

3 Months Forward

0.008616

0.008593

116.0631

116.3738

6 Months Forward

0.008724

0.0087

114.6263

114.9425

Switzerland (Franc)

0.7648

0.7652

1.3075

1.3068

1 Month Forward

0.767

0.7674

1.3038

1.3031

3 Months Forward

0.7718

0.7722

1.2957

1.295

6 Months Forward

0.7791

0.7794

1.2835

1.283

Euro

1.2000

1.1906

0.8333

0.8399

Using the table what is the 6-month forward pound–yen cross-exchange rate?

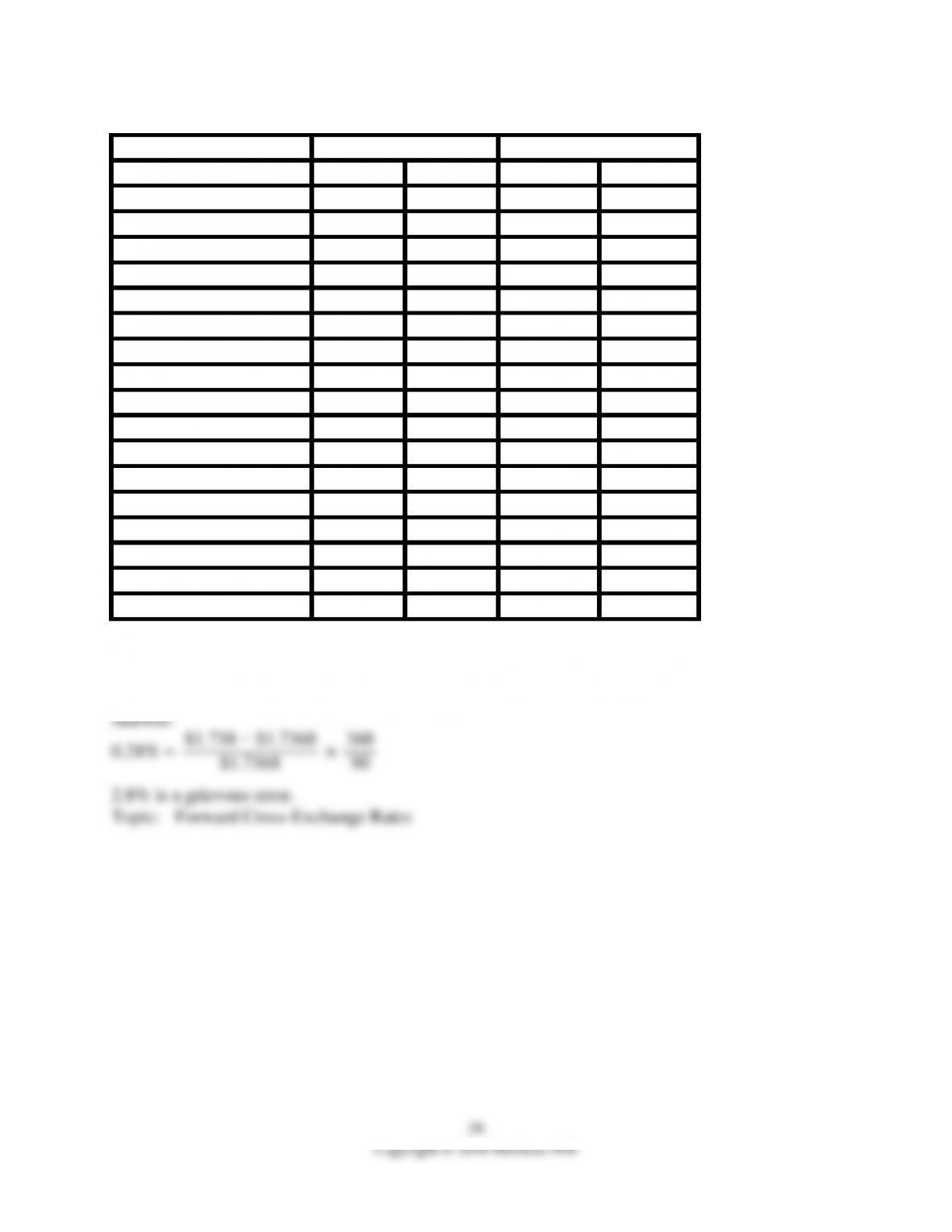

100)

Country

USD equiv.

Currency per USD

Tuesday

Monday

Tuesday

Monday

U.K. (Pound)

1.7368

1.7424

0.5758

0.5739

1 Month Forward

1.7369

1.7425

0.5757

0.5739

3 Months Forward

1.738

1.7434

0.5754

0.5736

6 Months Forward

1.7409

1.7461

0.5744

0.5727

Canada (Dollar)

0.8667

0.8653

1.1538

1.1557

1 Month Forward

0.8674

0.866

1.1529

1.1547

3 Months Forward

0.8688

0.8674

1.151

1.1529

6 Months Forward

0.8708

0.8693

1.1484

1.1504

Japan (Yen)

0.008518

0.008495

117.3985

117.7163

1 Month Forward

0.008548

0.008525

116.0631

117.3021

3 Months Forward

0.008616

0.008593

116.0631

116.3738

6 Months Forward

0.008724

0.0087

114.6263

114.9425

Switzerland (Franc)

0.7648

0.7652

1.3075

1.3068

1 Month Forward

0.767

0.7674

1.3038

1.3031

3 Months Forward

0.7718

0.7722

1.2957

1.295

6 Months Forward

0.7791

0.7794

1.2835

1.283

Euro

1.2000

1.1906

0.8333

0.8399

Using the table, what is 3-month forward premium or discount (expressed as an annual percentage

rate) for the British pound in terms of U.S. dollars?