International Financial Management, 8e (Eun)

Chapter 4 Corporate Governance Around the World

1) Countries with strong shareholder protection tend to have more valuable stock markets and

more companies listed on stock exchanges per capita than countries with weak protection.

2) Corporate governance can be defined as

A) the economic, legal, and institutional framework in which corporate control and cash flow

rights are distributed among shareholders, managers and other stakeholders of the company.

B) the general framework in which company management is selected and monitored.

C) the rules and regulations adopted by boards of directors specifying how to manage companies.

D) the government-imposed rules and regulations affecting corporate management.

3) When managerial self-dealings are excessive and left unchecked,

A) they can have serious negative effects on share values.

B) they can impede the proper functions of capital markets.

C) they can impede such measures as GDP growth.

D) all of the options

4) Corporate governance structure

A) varies a great deal across countries.

B) has become homogenized following the integration of capital markets.

C) has become homogenized due to cross-listing of shares of many public corporations.

D) none of the options

5) The genius of public corporations stems from their capacity to allow efficient sharing or

spreading of risk among many investors, who can buy and sell their ownership shares on liquid

stock exchanges and let professional managers run the company on behalf of shareholders. This

risk sharing stems from

A) the liquidity of the shares.

B) the limited liability of shareholders.

C) the limited liability of bondholders.

D) the limited ability of shareholders.

6) In a public company with diffused ownership, the board of directors is entrusted with

A) monitoring the auditors and safeguarding the interests of shareholders.

B) monitoring the shareholders and safeguarding the interests of management.

C) monitoring the management and safeguarding the interests of shareholders.

D) none of the options

7) The key weakness of the public corporation is

A) too many shareholders, which makes it difficult to make corporate decisions.

B) relatively high corporate income tax rates.

C) conflicts of interest between managers and shareholders.

D) conflicts of interests between shareholders and bondholders.

8) When company ownership is diffuse,

A) a “free rider” problem encourages shareholder activism.

B) the large number of shareholders ensures strong monitoring of managerial behavior because

with a large enough group, there’s almost always someone who will to incur the costs of

monitoring management.

C) most shareholders will have a strong enough incentive to incur the costs of monitoring

management.

D) a “free rider” problem discourages shareholder activism and few shareholders have a strong

enough incentive to incur the costs of monitoring management.

9) In many countries with concentrated ownership

A) the conflicts of interest between shareholders and managers are worse than in countries with

diffuse ownership of firms.

B) the conflicts of interest are greater between large controlling shareholders and small outside

shareholders than between managers and shareholders.

C) the conflicts of interest are greater between managers and shareholders than between large

controlling shareholders and small outside shareholders.

D) corporate forms of business organization with concentrated ownership are rare.

10) In what country do the three largest shareholders control, on average, about 60 percent of the

shares of a public company?

A) United States

B) Canada

C) Great Britain

D) Italy

11) The public corporation

A) is jointly owned by a (potentially) large number of shareholders.

B) offers shareholders limited liability.

C) separates the ownership and control of a firm’s assets.

D) all of the options

12) The key strength(s) of the public corporation is/are

A) their capacity to allow efficient risk sharing among many investors.

B) their capacity to raise large amounts of funds at relatively low cost.

C) their capacity to consolidate decision-making.

D) all of the options

13) The central issue of corporate governance is

A) how to protect creditors from managers and controlling shareholders.

B) how to protect outside investors from the controlling insiders.

C) how to alleviate the conflicts of interest between managers and shareholders.

D) how to alleviate the conflicts of interest between shareholders and bondholders.

14) In theory,

A) managers are hired by the shareholders at the annual stockholders meeting. If the managers turn

in a bad year, new ones get hired.

B) shareholders hire the managers to oversee the board of directors.

C) managers are hired by the board of directors; the board is accountable to the shareholders.

D) none of the options

15) In the reality of corporate governance at the turn of this century,

A) boards of directors are often dominated by management-friendly insiders.

B) a typical board of directors often has relatively few outside directors who can independently

and objectively monitor the management.

C) managers of one firm often sit on the boards of other firms, whose managers are on the board of

the first firm. Due to the interlocking nature of these boards, there can exist a culture of “I’ll

overlook your problems if you overlook mine.”

D) all of the options have been true to a greater or lesser extent in the recent past.

16) The strongest protection for investors is provided by

A) English common law countries, such as Canada, the United States, and the U.K.

B) French civil law countries, such as Belgium, Italy, and Mexico.

C) a weak board of directors.

D) socialized firms.

17) The public corporation has a key weakness which is

A) the conflicts of interest between bondholders and shareholders.

B) the conflicts of interest between managers and bondholders.

C) the conflicts of interest between stakeholders and shareholders.

D) the conflicts of interest between managers and shareholders.

18) The separation of the company’s ownership and control,

A) is especially prevalent in such countries as the United States and the United Kingdom, where

corporate ownership is highly diffused.

B) is especially prevalent in such countries as Italy and Mexico, where corporate ownership is

highly concentrated.

C) is a rational response to the agency problem.

D) none of the options

19) In the United States, managers are legally bound by the “duty of loyalty” to

A) the board of directors.

B) the shareholders.

C) the bondholders.

D) the government.

20) In the United States, managers are bound by the “duty of loyalty” to serve the shareholders.

A) This is an ethical, not legal, obligation.

B) This is a legal obligation.

C) This is only a moral obligation; there are no penalties.

D) none of the options

21) Outside the United States and the United Kingdom,

A) concentrated ownership of the company is more the exception than the rule.

B) diffused ownership of the company is more the exception than the rule.

C) partnerships are more important than corporations.

D) none of the options

22) A complete contract between shareholders and managers

A) would specify exactly what the manager will do under each of all possible future contingencies.

B) would be an expensive contract to write and a very expensive contract to monitor.

C) would eliminate any conflicts of interest (and managerial discretion).

D) all of the options

23) Why is it rational to make shareholders “weak” by giving control to the managers of the firm?

A) This may be rational when shareholders may be neither qualified nor interested in making

business decisions.

B) This may be rational since many shareholders find it easier to sell their shares in an

underperforming firm than to monitor the management.

C) This may be rational to the extent that managers are answerable to the board of directors.

D) All of the options are explanations for the separation of ownership and control.

24) Free cash flow refers to

A) a firm’s cash reserve in excess of tax obligation.

B) a firm’s funds in excess of what’s needed for undertaking all profitable projects.

C) a firm’s cash reserve in excess of interest and tax payments.

D) a firm’s income tax refund that is due to interest payments on borrowing.

25) The investors supply funds to the company but are not involved in the company’s daily

decision making. As a result, many public companies come to have

A) strong shareholders and weak managers.

B) strong managers and weak shareholders.

C) strong managers and strong shareholders.

D) weak managers and weak shareholders.

26) The agency problem refers to the possible conflicts of interest between

A) self-interested managers as principals and shareholders of the firm who are the agents.

B) altruistic managers as agents and shareholders of the firm who are the principals.

C) self-interested managers as agents and shareholders of the firm who are the principals.

D) dutiful managers as principals and shareholders of the firm who are the agents.

27) Self-interested managers may be tempted to

A) indulge in expensive perquisites at company expense.

B) adopt anti-takeover measures for their company to ensure their personal job security.

C) waste company funds by undertaking unprofitable projects that benefit themselves but not

shareholders.

D) All of the options are potential abuses that self-interested managers may be tempted to visit

upon shareholders.

28) Suppose in order to defraud the shareholders, a manager sets up an independent company that

he owns and sells the main company’s output to this company. He would be tempted to set the

transfer price

A) below market prices.

B) above market prices.

C) at the market price.

D) in accordance with GAAP.

29) Suppose in order to defraud the shareholders, a manager sets up an independent company that

he owns and buys one of the main company’s inputs of production from this company. He would

be tempted to set the transfer price

A) below market prices.

B) above market prices.

C) at the market price.

D) in accordance with GAAP.

30) Why do managers tend to retain free cash flow?

A) Managers are in the best position to decide the best use of those funds.

B) These funds are needed for undertaking profitable projects and the issue costs are less than new

issues of stocks or bonds.

C) Managers may not be acting in the shareholders best interest, and for a variety of reasons, want

to use the free cash flow.

D) none of the options

31) Managerial entrenchment efforts are clear signs of the agency problem. They include

A) anti-takeover defenses.

B) poison pills.

C) changes in the voting procedures to make it more difficult for the firm to be taken over.

D) all of the options

32) In high-growth industries where companies’ internally generated funds fall short of profitable

investment opportunities,

A) managers are less likely to waste funds in unprofitable projects.

B) managers are more likely to waste funds in unprofitable projects.

33) The agency problem tends

A) to be more serious in firms with free cash flows.

B) to be more serious in firms with excessive amounts of excess cash.

C) to be less serious in firms with few numbers of shareholders.

D) all of the options

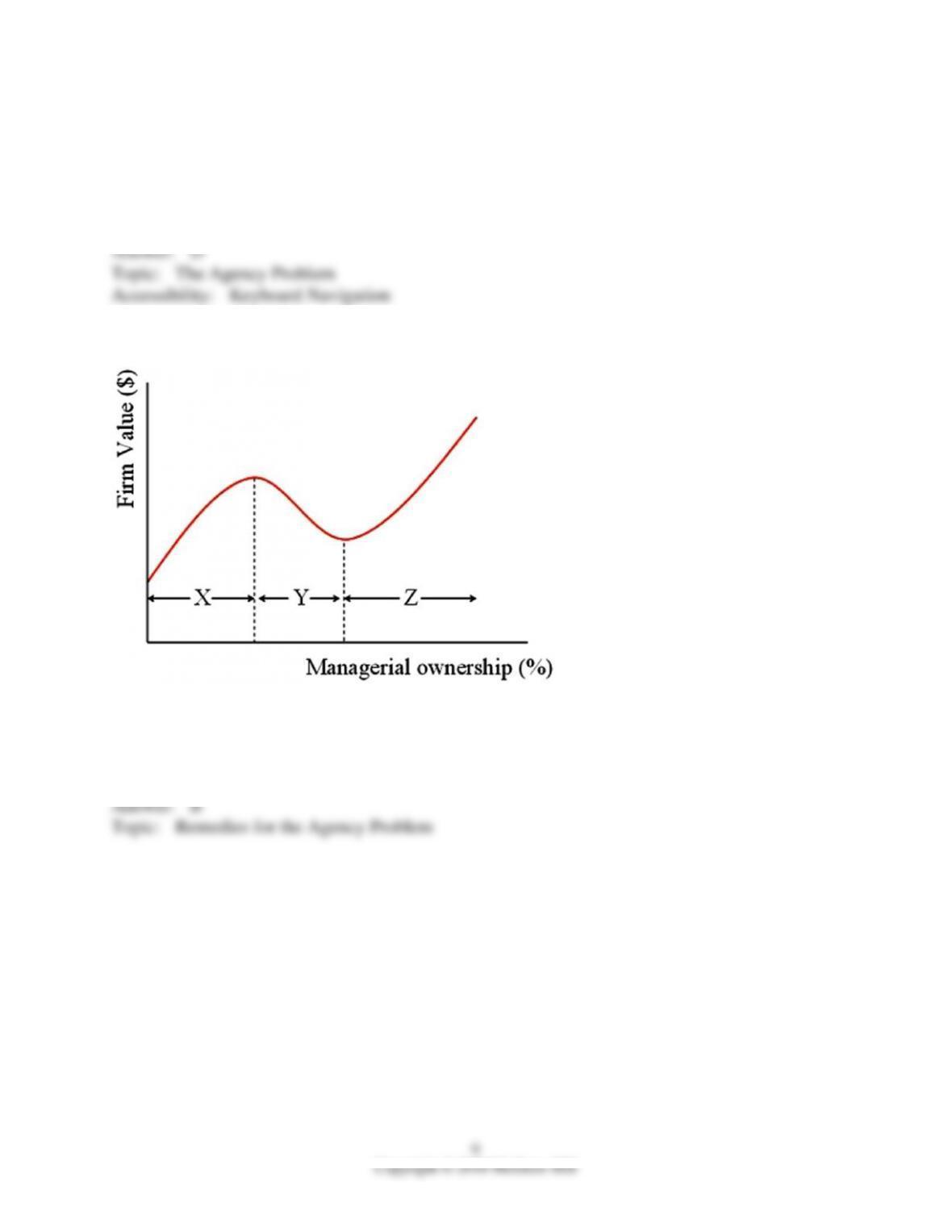

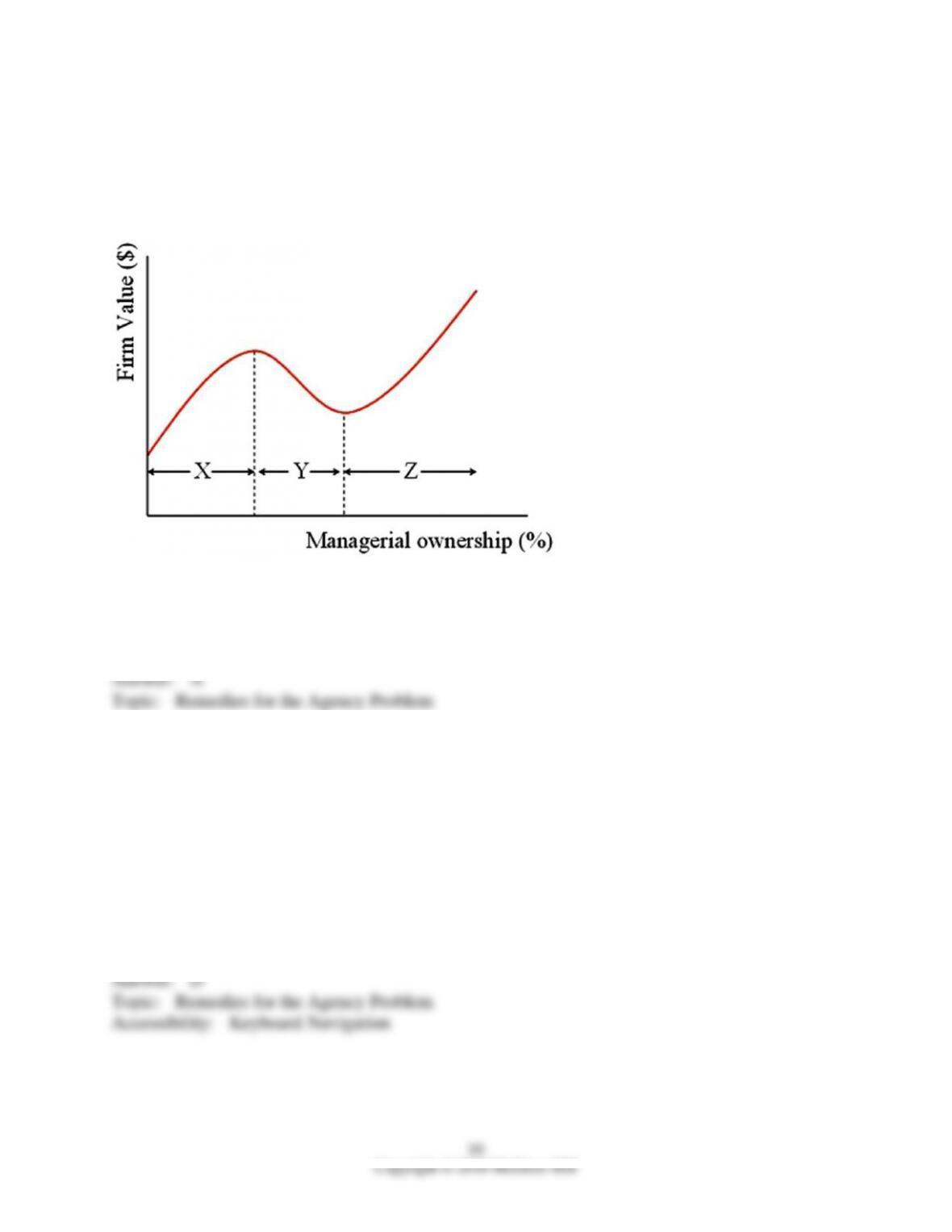

34) In the graph, X, Y, and Z represent

A) entrenchment, alignment, entrenchment.

B) alignment, entrenchment, alignment.

C) misalignment and alignment.

D) agency costs of debt and equity.

35) Morck, Shleifer, and Vishny (1988) studied the relationship between managerial ownership

share and firm value for Fortune 500 U.S. companies. The results of their analysis suggested that

the first turning point (the first vertical, dashed line between X and Y) is reached at ________

percent and the second turning point (the second vertical, dashed line between Y and Z) at about

________ percent, respectively.

A) 5; 25.

B) 15; 50.

C) 50; 75.

D) none of the options

36) Which of the following is true regarding leveraged buy-outs (LBOs)?

A) LBOs involve managers or buyout partners acquiring controlling interests in public companies,

usually financed by heavy borrowing.

B) Concentrated ownership and high levels of debt associated with LBOs are the mechanism for

solving the agency problem.

C) LBOs improve a company’s free cash flow and this is the mechanism by which they can solve

the agency problem.

D) LBOs involve managers or buyout partners acquiring controlling interests in public companies

(usually financed by heavy borrowing), and concentrated ownership and high levels of debt

associated with LBOs are the mechanism for solving the agency problem.

37) Tobin’s Q is

A) the ratio of the market value of company assets to the replacement costs of the assets.

B) a means to find overvalued stocks: If Q is high it means that the cost to replace a firm’s assets is

greater than the value of its stock.

C) the same as the price-to-book ratio.

D) the ratio of the market value of company assets to the replacement costs of the assets, as well as

a means to find overvalued stocks: If Q is high it means that the cost to replace a firm’s assets is

greater than the value of its stock.

38) It is important for society as a whole to solve the agency problem, since the agency problem

A) leads to waste of scarce resources.

B) hampers capital market functions.

C) retards economic growth.

D) all of the options

39) In the U.S., the chief role of the board of directors is

A) to hire the management team.

B) to decide on the annual capital budget.

C) to design an effective incentive compatible compensation scheme for themselves.

D) none of the options

40) In the United Kingdom, the majority of public companies

A) voluntarily abide by the Code of Best Practice on corporate governance.

B) are compelled by law to abide by the Code of Best Practice on corporate governance.

C) do not abide by the Code of Best Practice on corporate governance.

D) none of the options

41) In Germany, the corporate board is

A) legally charged with representing the interests of shareholders exclusively.

B) legally charged with looking after the interests of stakeholders (e.g., workers, creditors, etc.) in

general, not just shareholders.

C) legally charged as a supervisory board only.

D) legally charged as a management board only.

42) In the United States,

A) boards of directors are legally responsible for representing the interests of the shareholders.

B) due to the diffused ownership structure of the public company, management often gets to

choose board members who are likely to be friendly to management.

C) there is a correlation between underperforming firms and boards of directors who are not fully

independent.

D) all of the options

43) In the United States, it is not uncommon for the same person to serve as both CEO and

chairman of the board.

A) This situation must not have much conflict of interest since it is common.

B) This situation has a built-in conflict of interest.

C) This is only legal if that individual owns a controlling number of shares in the firm.

D) none of the options

44) Suppose you are the CEO of company A, and you serve on the board of company B, while the

CEO of B is on your board.

A) This is a potential conflict of interest for both parties.

B) This is normal and even a desirable situation since it allows for efficient information sharing

between the firms.

C) There is a potential conflict for the shareholders of the two firms.

D) all of the options

45) In the United States, it is well documented that

A) boards dominated by their chief executives are prone to trouble.

B) public scrutiny can help improve corporate governance.

C) as public firms improve their corporate governance, the stock price goes up.

D) all of the options

46) The board of directors may grant stock options to managers. These are

A) call options.

B) put options.

C) both of the options

D) none of the options

47) If an incentive contract specifies certain accounting performance,

A) that accounting number will likely be the focus of managers.

B) managers will set aside the accounting goal if it conflicts with the goal of maximizing

shareholder wealth.

C) managers will be unable to manipulate the GAAP, so shareholders can be confident of having

their wealth maximized.

D) none of the options

48) The board of directors may grant stock options to managers

A) to save executive compensation costs.

B) to use as a substitute for bonus.

C) to align the interest of managers with that of shareholders.

D) none of the options

49) When designing an incentive contract,

A) it is important for the board of directors to set up an independent compensation committee that

can carefully design the contract and diligently monitor manager’s actions.

B) senior executives can be trusted to not abuse incentive contracts by artificially manipulating

accounting numbers since the auditors should look in to that.

C) the presence of any incentive is enough, whether it is accounting based or stock-price based.

D) the board of directors should always give the managers a “heads I win, tails you lose” type of

option.

50) Concentrated ownership of a public company

A) is normal in the United States, following the well-publicized scandals of recent years.

B) is relatively rare in the United States and common in many other parts of the world.

C) leads to a free-rider problem with the minority shareholders relying on the majority

shareholders to assume an undue burden in monitoring the management.

D) is the norm in Great Britain.

51) Concentrated ownership of a public company

A) can be an effective way to alleviate the agency problem between shareholders and managers.

B) is the norm in Great Britain.

C) tends to be an ineffective way to alleviate conflicts of interest between groups of shareholders.

D) none of the options

52) The goal of greater accounting transparency

A) is to impose more rules and harsher penalties for their violation.

B) is to reduce the information asymmetry between corporate insiders and the public.

C) is to discourage managerial self-dealings.

D) is to reduce the information asymmetry between corporate insiders and the public, as well as

discourage managerial self-dealings.