83) A French firm is considering a one-year investment in the United Kingdom with a

pound-denominated rate of return of i£ = 15%. The firm’s local cost of capital is i€ = 10%. The

project costs £1,000 and will return £1,150 at the end of one year. The current exchange rate is

€2.00 = £1.00.

Suppose that the bank of England is considering either tightening or loosening its monetary policy.

It is widely believed that in one year there are only two possibilities:

S1 (€/£) = €2.20 per £

S1 (€/£) = €1.80 per £

Following revaluation, the exchange rate is expected to remain steady for at least another year.

Find the NPV in euro for the French firm if they wait one year to undertake the project after the

exchange rate falls to S1(€/£) = €1.80 per £.

84) A French firm is considering a one-year investment in the United Kingdom with a

pound-denominated rate of return of i£ = 15%. The firm’s local cost of capital is i€ = 10%. The

project costs £1,000 and will return £1,150 at the end of one year. The current exchange rate is

€2.00 = £1.00.

Suppose that the bank of England is considering either tightening or loosening its monetary policy.

It is widely believed that in one year there are only two possibilities:

S1 (€/£) = €2.20 per £

S1 (€/£) = €1.80 per £

Following revaluation, the exchange rate is expected to remain steady for at least another year.

The CFO who has a CFA notices the optionality in starting this project today. He asks you to

comment and outline your valuation strategy.

85) A French firm is considering a one-year investment in the United Kingdom with a

pound-denominated rate of return of i£ = 15%. The firm’s local cost of capital is i€ = 10%. The

project costs £1,000 and will return £1,150 at the end of one year. The current exchange rate is

€2.00 = £1.00.

Suppose that the bank of England is considering either tightening or loosening its monetary policy.

It is widely believed that in one year there are only two possibilities:

S1 (€/£) = €2.20 per £

S1 (€/£) = €1.80 per £

Following revaluation, the exchange rate is expected to remain steady for at least another year.

Your banker quotes the euro-zone risk-free rate at i€ = 6% and the British risk free rate at i£ = 6%.

Find the value of the option and thereby the project.

86) A French firm is considering a one-year investment in the United Kingdom with a

pound-denominated rate of return of i£ = 15%. The firm’s local cost of capital is i€ = 10%. The

project costs £1,000 and will return £1,150 at the end of one year. The current exchange rate is

€2.00 = £1.00.

Suppose that the bank of England is considering either tightening or loosening its monetary policy.

It is widely believed that in one year there are only two possibilities:

S1 (€/£) = €2.20 per £

S1 (€/£) = €1.80 per £

Following revaluation, the exchange rate is expected to remain steady for at least another year.

Using your results to the last question, make a recommendation vis-à-vis when to undertake the

project.

87) A French firm is considering a one-year investment in the United Kingdom with a

pound-denominated rate of return of i£ = 15%. The firm’s local cost of capital is i€ = 10%. The

project costs £1,000 and will return £1,150 at the end of one year. The current exchange rate is

€2.00 = £1.00.

Suppose that the bank of England is considering either tightening or loosening its monetary policy.

It is widely believed that in one year there are only two possibilities:

S1 (€/£) = €2.20 per £

S1 (€/£) = €1.80 per £

Following revaluation, the exchange rate is expected to remain steady for at least another year.

Using the notion of a hedge ratio, make a recommendation vis-à-vis how to undertake the project

today without “buying” the option.

88) An American Hedge Fund is considering a one-year investment in an Italian government bond

with a one-year maturity and a euro-denominated rate of return of i€ = 5%. The bond costs €1,000

today and will return €1,050 at the end of one year without risk. The current exchange rate is €1.00

= $1.50. U.S. dollar-denominated government bonds currently have a yield to maturity of 4

percent. Suppose that the European Central Bank is considering either tightening or loosening its

monetary policy. It is widely believed that in one year there are only two possibilities:

S1 ($/€) = €1.80 per €

S1 ($/€) = €1.40 per €

Following revaluation, the exchange rate is expected to remain steady for at least another year.

Find the ex post IRR in euro for the American firm if they buy the bond today and then the

exchange rate falls to S1($/€) = $1.40 per €.

89) An American Hedge Fund is considering a one-year investment in an Italian government bond

with a one-year maturity and a euro-denominated rate of return of i€ = 5%. The bond costs €1,000

today and will return €1,050 at the end of one year without risk. The current exchange rate is €1.00

= $1.50. U.S. dollar-denominated government bonds currently have a yield to maturity of 4

percent. Suppose that the European Central Bank is considering either tightening or loosening its

monetary policy. It is widely believed that in one year there are only two possibilities:

S1 ($/€) = €1.80 per €

S1 ($/€) = €1.40 per €

Following revaluation, the exchange rate is expected to remain steady for at least another year.

Find the ex post IRR in euro for the American firm if they buy the bond today and then the

exchange rate rises to S1($/€) = $1.80 per €.

90) An American Hedge Fund is considering a one-year investment in an Italian government bond

with a one-year maturity and a euro-denominated rate of return of i€ = 5%. The bond costs €1,000

today and will return €1,050 at the end of one year without risk. The current exchange rate is €1.00

= $1.50. U.S. dollar-denominated government bonds currently have a yield to maturity of 4

percent. Suppose that the European Central Bank is considering either tightening or loosening its

monetary policy. It is widely believed that in one year there are only two possibilities:

S1 ($/€) = €1.80 per €

S1 ($/€) = €1.40 per €

Following revaluation, the exchange rate is expected to remain steady for at least another year.

Find the IRR in dollars for the American firm if they wait one year to buy the bond after the

exchange rate rises to S1($/€) = $1.80 per €. Assume that i€ doesn’t change.

91) An American Hedge Fund is considering a one-year investment in an Italian government bond

with a one-year maturity and a euro-denominated rate of return of i€ = 5%. The bond costs €1,000

today and will return €1,050 at the end of one year without risk. The current exchange rate is €1.00

= $1.50. U.S. dollar-denominated government bonds currently have a yield to maturity of 4

percent. Suppose that the European Central Bank is considering either tightening or loosening its

monetary policy. It is widely believed that in one year there are only two possibilities:

S1 ($/€) = €1.80 per €

S1 ($/€) = €1.40 per €

Following revaluation, the exchange rate is expected to remain steady for at least another year.

Find the NPV in dollars for the American firm if they wait one year to buy the bond after the

exchange rate rises to S1($/€) = $1.80 per €. Assume that i€ doesn’t change.

92) An American Hedge Fund is considering a one-year investment in an Italian government bond

with a one-year maturity and a euro-denominated rate of return of i€ = 5%. The bond costs €1,000

today and will return €1,050 at the end of one year without risk. The current exchange rate is €1.00

= $1.50. U.S. dollar-denominated government bonds currently have a yield to maturity of 4

percent. Suppose that the European Central Bank is considering either tightening or loosening its

monetary policy. It is widely believed that in one year there are only two possibilities:

S1 ($/€) = €1.80 per €

S1 ($/€) = €1.40 per €

Following revaluation, the exchange rate is expected to remain steady for at least another year.

Find the IRR in dollars for the American firm if they wait one year to buy the bond after the

exchange rate falls to S1($/€) = $1.40 per €. Assume that i€ doesn’t change.

93) An American Hedge Fund is considering a one-year investment in an Italian government bond

with a one-year maturity and a euro-denominated rate of return of i€ = 5%. The bond costs €1,000

today and will return €1,050 at the end of one year without risk. The current exchange rate is €1.00

= $1.50. U.S. dollar-denominated government bonds currently have a yield to maturity of 4

percent. Suppose that the European Central Bank is considering either tightening or loosening its

monetary policy. It is widely believed that in one year there are only two possibilities:

S1 ($/€) = €1.80 per €

S1 ($/€) = €1.40 per €

Following revaluation, the exchange rate is expected to remain steady for at least another year.

Find the NPV in euro for the American firm if they wait one year to undertake the project after the

exchange rate falls to S1($/€) = $1.40 per €. Assume that i€ doesn’t change.

94) An American Hedge Fund is considering a one-year investment in an Italian government bond

with a one-year maturity and a euro-denominated rate of return of i€ = 5%. The bond costs €1,000

today and will return €1,050 at the end of one year without risk. The current exchange rate is €1.00

= $1.50. U.S. dollar-denominated government bonds currently have a yield to maturity of 4

percent. Suppose that the European Central Bank is considering either tightening or loosening its

monetary policy. It is widely believed that in one year there are only two possibilities:

S1 ($/€) = €1.80 per €

S1 ($/€) = €1.40 per €

Following revaluation, the exchange rate is expected to remain steady for at least another year.

The hedge fund manager notices the optionality in starting this project today. He asks you to

comment and outline your valuation strategy.

95) An American Hedge Fund is considering a one-year investment in an Italian government bond

with a one-year maturity and a euro-denominated rate of return of i€ = 5%. The bond costs €1,000

today and will return €1,050 at the end of one year without risk. The current exchange rate is €1.00

= $1.50. U.S. dollar-denominated government bonds currently have a yield to maturity of 4

percent. Suppose that the European Central Bank is considering either tightening or loosening its

monetary policy. It is widely believed that in one year there are only two possibilities:

S1 ($/€) = €1.80 per €

S1 ($/€) = €1.40 per €

Following revaluation, the exchange rate is expected to remain steady for at least another year.

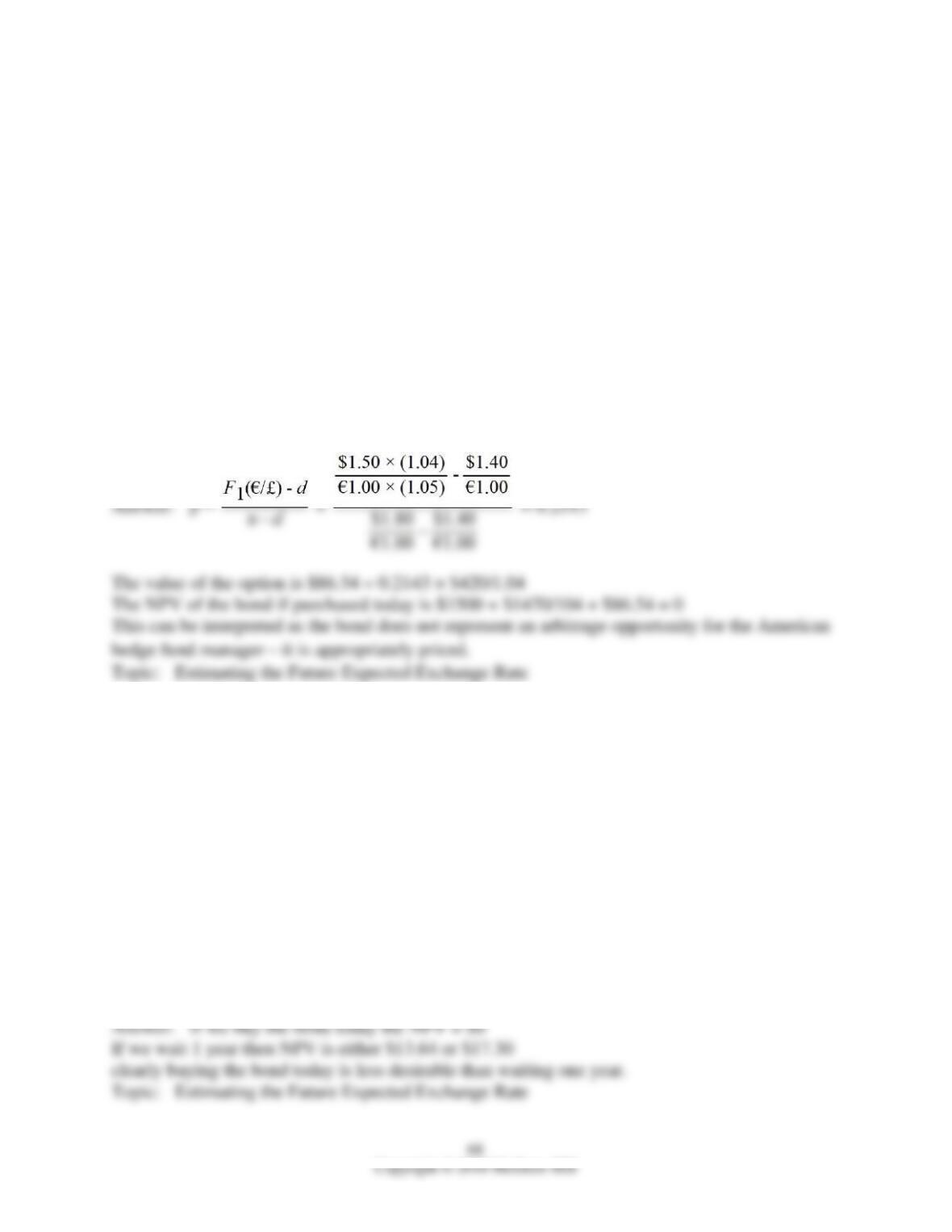

Your banker quotes the euro-zone risk-free rate at i€ = 5% and the U.S. risk free rate at i$ = 4%.

Find the value of the option and thereby the correct value of the bond to a U.S. investor.

96) An American Hedge Fund is considering a one-year investment in an Italian government bond

with a one-year maturity and a euro-denominated rate of return of i€ = 5%. The bond costs €1,000

today and will return €1,050 at the end of one year without risk. The current exchange rate is €1.00

= $1.50. U.S. dollar-denominated government bonds currently have a yield to maturity of 4

percent. Suppose that the European Central Bank is considering either tightening or loosening its

monetary policy. It is widely believed that in one year there are only two possibilities:

S1 ($/€) = €1.80 per €

S1 ($/€) = €1.40 per €

Following revaluation, the exchange rate is expected to remain steady for at least another year.

Using your results to the last question, make a recommendation vis-à-vis when to buy the bond.

97) An American Hedge Fund is considering a one-year investment in an Italian government bond

with a one-year maturity and a euro-denominated rate of return of i€ = 5%. The bond costs €1,000

today and will return €1,050 at the end of one year without risk. The current exchange rate is €1.00

= $1.50. U.S. dollar-denominated government bonds currently have a yield to maturity of 4

percent. Suppose that the European Central Bank is considering either tightening or loosening its

monetary policy. It is widely believed that in one year there are only two possibilities:

S1 ($/€) = €1.80 per €

S1 ($/€) = €1.40 per €

Following revaluation, the exchange rate is expected to remain steady for at least another year.

Using the notion of hedging, make a recommendation vis-à-vis how to undertake the project today

without “buying” the option.

98) The Strik-it-Rich Gold Mining Company is contemplating expanding its operations. To do so

it will need to purchase land that its geologists believe is rich in gold. Strik-it-Rich’s management

believes that the expansion will allow it to mine and sell an additional 2,000 troy ounces of gold

per year. The expansion, including the cost of the land, will cost $500,000. The current price of

gold bullion is $425 per ounce and one-year gold futures are trading at $450.50 = $425 × (1.06).

Extraction costs are $375 per ounce. The firm’s cost of capital is 10 percent.

Strik-it-Rich’s management is, however, concerned with the possibility that large sales of gold

reserves by Russia and the United Kingdom will drive the price of gold down to $390 for the

foreseeable future. On the other hand, management believes there is some possibility that the

world will soon return to a gold reserve international monetary system. In the latter event, the price

of gold would increase to at least $460 per ounce. The course of the future price of gold bullion

should become clear within a year. Strik-it-Rich can postpone the expansion for a year by buying a

purchase option on the land for $25,000.

Compute the NPV at the current price of gold. Hint: think of the gold mine as a perpetuity.

99) The Strik-it-Rich Gold Mining Company is contemplating expanding its operations. To do so

it will need to purchase land that its geologists believe is rich in gold. Strik-it-Rich’s management

believes that the expansion will allow it to mine and sell an additional 2,000 troy ounces of gold

per year. The expansion, including the cost of the land, will cost $500,000. The current price of

gold bullion is $425 per ounce and one-year gold futures are trading at $450.50 = $425 × (1.06).

Extraction costs are $375 per ounce. The firm’s cost of capital is 10 percent.

Strik-it-Rich’s management is, however, concerned with the possibility that large sales of gold

reserves by Russia and the United Kingdom will drive the price of gold down to $390 for the

foreseeable future. On the other hand, management believes there is some possibility that the

world will soon return to a gold reserve international monetary system. In the latter event, the price

of gold would increase to at least $460 per ounce. The course of the future price of gold bullion

should become clear within a year. Strik-it-Rich can postpone the expansion for a year by buying a

purchase option on the land for $25,000.

Compute the NPV at the two possible prices of gold.