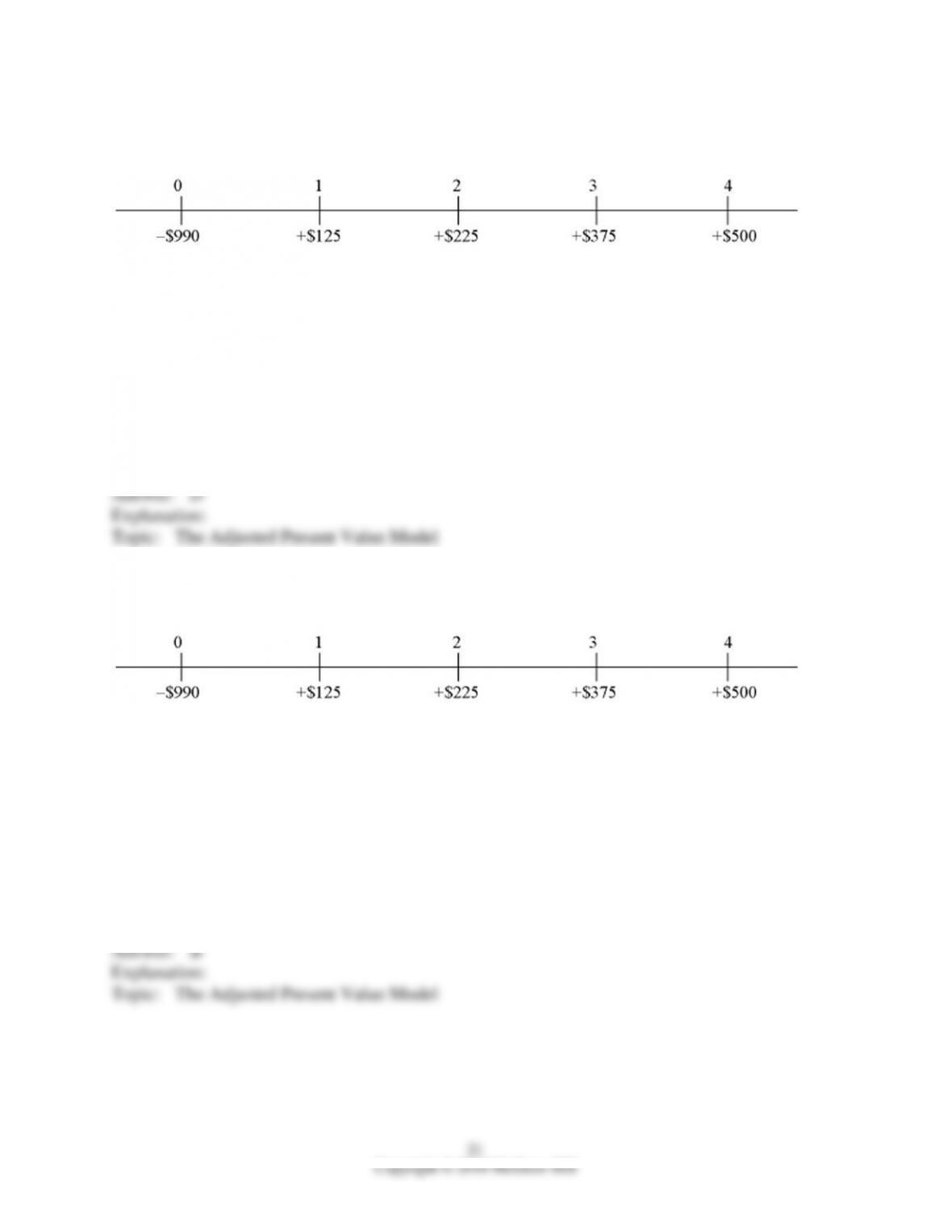

33) Consider a project of the Cornell Haul Moving Company, the timing and size of the

incremental after-tax cash flows (for an all-equity firm) are shown below in millions:

The firm’s tax rate is 34 percent; the firm’s bonds trade with a yield to maturity of 8 percent; the

current and target debt-equity ratio is 3; if the firm were financed entirely with equity, the required

return would be 10 percent.

Using the APV method, what is the value of this project to an all-equity firm?

A) −$46,502,288.10

B) $12,494,643.75

C) $36,580,767.55

D) −$67,163,445.12

34) Consider a project of the Cornell Haul Moving Company, the timing and size of the

incremental after-tax cash flows (for an all-equity firm) are shown below in millions:

The firm’s tax rate is 34 percent; the firm’s bonds trade with a yield to maturity of 8 percent; the

current and target debt-equity ratio is 3; if the firm were financed entirely with equity, the required

return would be 10 percent.

Using the APV method, what is the value of the debt side effects?

A) $239,072,652.70

B) $66,891,713.66

C) $59,459,301.03

D) $660,000,000

35) In the APV model

A) interest tax shields are discounted at i.

B) operating cash flows are discounted at Ku.

C) depreciation tax shields are discounted at i.

D) all of the options

36) Your firm’s existing bonds trade with a yield to maturity of eight percent. The state of Missouri

has offered to loan your firm $10,000,000 at zero percent for five years. Repayment will be of the

form of $2,000,000 per year for five years; the first payment is due in one year.

What is the value of this offer?

A) $4,729,622.75

B) $2,014,579.93

C) $0

D) $196,929.88

37) What proportion of the firm is financed by debt for a firm that expects a 15 percent return on

equity, a 12 percent return on assets, and a 10 percent return on debt?

The tax rate is 25 percent.

A) 20 percent

B) 1/3

C) 60 percent

D) 2/3

38) The required return on equity for a levered firm is 10.60 percent. The debt to equity ratio is ½

the tax rate is 40 percent, the pre-tax cost of debt is 8 percent. Find the cost of capital if this firm

were financed entirely with equity.

A) 10 percent

B) 12 percent

C) 8.67 percent

D) none of the options

39) The required return on equity for an all-equity firm is 10.0 percent. They are considering a

change in capital structure to a debt-to-equity ratio of ½ the tax rate is 40 percent, the pre-tax cost

of debt is 8 percent. Find the new cost of capital if this firm changes capital structure.

A) 14.93 percent

B) 8.67 percent

C) 7.40 percent

D) none of the options

40) The required return on equity for an all-equity firm is 10.0 percent. They currently have a beta

of one and the risk-free rate is 5 percent and the market risk premium is 5 percent. They are

considering a change in capital structure to a debt-to-equity ratio of ½ the tax rate is 40 percent, the

pre-tax cost of debt is 8 percent. Find the beta if this firm changes capital structure.

A) 1.12

B) 1

C) 7.4 percent

D) none of the options

41) What is the expected return on equity for a tax-free firm with a 15 percent expected return on

assets that pays 12 percent on its debt, which totals 25 percent of assets?

A) 24 percent

B) 15.60 percent

C) 16 percent

D) 20 percent

42) What is the expected return on equity for firm in the 40 percent tax bracket with a 15 percent

expected return on assets that pays 12 percent on its debt, which totals 25 percent of assets?

A) 24 percent

B) 15.60 percent

C) 16 percent

D) 20 percent

43) Assume that XYZ Corporation is a leveraged company with the following information:

Kl = cost of equity capital for XYZ = 13%

i = before-tax borrowing cost = 8%

t = marginal corporate income tax rate = 30%

Calculate the debt–to-total-market-value ratio that would result in XYZ having a weighted average

cost of capital of 9.3 percent.

A) 35 percent

B) 40 percent

C) 45 percent

D) 50 percent

44) Today is January 1, 2009. The state of Iowa has offered your firm a subsidized loan. It will be

in the amount of $10,000,000 at an interest rate of 5 percent and have ANNUAL (amortizing)

payments over 3 years. The first payment is due today and your taxes are due January 1 of each

year on the previous year’s income. The yield to maturity on your firm’s existing debt is 8 percent.

What is the NPV of this subsidized loan?

Note that I did not round my intermediate steps. If you did, your answer may be off by a bit. Select

the answer closest to yours.

A) $406,023.10

B) $840,797

C) $64,157.38

D) $20,659.77

45) Today is January 1, 2009. The state of Iowa has offered your firm a subsidized loan. It will be

in the amount of $10,000,000 at an interest rate of 5 percent and have ANNUAL (amortizing)

payments over 3 years. The first payment is due today and your taxes are due January 1 of each

year on the previous year’s income. The yield to maturity on your firm’s existing debt is 8 percent.

What is the €-denominated NPV of this project? I did not round my intermediate steps, if you did,

select the answer closest to yours.

A) €5,563.23

B) €2,270.79

C) €7,223.14

D) €3,554.29

46) The spot exchange rate is ¥125 = $1. The U.S. discount rate is 10 percent; inflation over the

next three years is 3 percent per year in the U.S. and 2 percent per year in Japan. Calculate the

dollar NPV of this project.

I did not round my intermediate steps, if you did, select the answer closest to yours.

A) $267,181.87

B) $14,176.67

C) $2,536.49

D) $2,137.46

47) Some of the factors (with selected explanations) used in calculating the basic “net present

value” and the “incremental” cash flows of a capital project are:

(i) expected after-tax terminal value, including recapture of working capital

(ii) net income, which belongs to the equity holders of the firm

(iii) initial investment at inception

(iv) depreciation, and the fact that depreciation is a noncash expense (i.e., it is removed from the

calculation of net income, for tax purposes, but added back because it did not actually flow out of

the firm)

(v) weighted-average cost of capital

(vi) the firm’s after-tax payment of interest to debtholders

(vii) economic life of the capital project in years

The “net present value” of a capital project is calculated by using

A) (i), (ii), and (iii).

B) (ii), (iv), and (vi).

C) (i), (iii), (v), and (vii).

D) (iv), (v), (vi), and (vii).

48) Some of the factors (with selected explanations) used in calculating the basic “net present

value” and the “incremental” cash flows of a capital project are:

(i) expected after-tax terminal value, including recapture of working capital

(ii) net income, which belongs to the equity holders of the firm

(iii) initial investment at inception

(iv) depreciation, and the fact that depreciation is a noncash expense (i.e., it is removed from the

calculation of net income, for tax purposes, but added back because it did not actually flow out of

the firm)

(v) weighted-average cost of capital

(vi) the firm’s after-tax payment of interest to debtholders

(vii) economic life of the capital project in years

The “incremental” cash flows of a capital project is calculated by using

A) (i), (ii), and (iii).

B) (ii), (iv), and (vi).

C) (i), (iii), (v), and (vii).

D) (iv), (v), (vi), and (vii).

49) In the context of the capital budgeting analysis of an MNC that has strong foreign competitors,

“lost sales” refers to

A) the cannibalization of existing projects by new projects.

B) the entire sales revenue of a new foreign manufacturing facility representing the incremental

sales revenue of the new project.

C) the cannibalization of existing projects by new projects and the entire sales revenue of a new

foreign manufacturing facility representing the incremental sales revenue of the new project.

D) none of the options

50) Which of the following statements is false about “borrowing capacity”?

A) It is an especially important point in international capital budgeting analysis because of the

frequency of large concessionary loans.

B) It creates tax shields for APV analysis regardless of how the project is actually financed.

C) It is synonymous to the “project debt.”

D) It is based on the firm’s optimal capital structure.

51) The adjusted present value (APV) model that is suitable for an MNC is the basic net present

value (NPV) model expanded to

A) distinguish between the market value of a levered firm and the market value of an unlevered

firm.

B) discern the blocking of certain cash flows by the host country from being legally remitted to the

parent.

C) consider foreign currency fluctuations or extra taxes imposed by the host country on foreign

exchange remittances.

D) all of the options

52) Sensitivity analysis in the calculation of the adjusted present value (APV) allows the financial

manager to

A) analyze all of the risks (business, economic, exchange rate uncertainty, political, etc.) inherent

in the investment.

B) more fully understand the implications of planned capital expenditures.

C) consider in advance actions that can be taken should an investment not develop as anticipated.

D) all of the options

53) The ABC Company, a U.S.-based MNC, plans to establish a subsidiary in Spain to

manufacture and sell water pumps. ABC has total assets of $80 million, of which $60 million is

equity financed. The remainder is financed with debt. ABC considers its current capital structure

optimal. The construction cost of the facility in Spain is estimated to be €8,500 million, of which

€6,500 million is to be financed at a below-market rate of interest arranged by the Spanish

government. The proposed project will increase the borrowing capacity by

A) €1,215 million.

B) €2,215 million.

C) €3,215 million.

D) €4,215 million.

54) Given the following information for a levered and unlevered firm, calculate the difference in

the cash flow available to investors. Assume the corporate tax rate is 40 percent.

(Hint: Calculate the tax savings arising from the tax deductibility of interest payments).

Levered

Unlevered

Revenue

$

250

$

250

Operating cost

−$

100

−$

100

Interest expense

−$

20

$

0

A) $8

B) $18

C) $78

D) $90

55) As of today, the spot exchange rate is €1.00 = $1.25 and the rates of inflation expected to

prevail for the next year in the U.S. is 2 percent and 3 percent in the euro zone. What is the

one-year forward rate that should prevail?

A) €1.00 = $1.2379

B) €1.00 = $1.2139

C) €1.00 = $0.9903

D) $1.00 = €1.2623

56) As of today, the spot exchange rate is €1.00 = $1.50 and the rates of inflation expected to

prevail for the next year in the U.S. is 2 percent and 3 percent in the euro zone. What is the

one-year forward rate that should prevail?

A) €1.00 = $1.5147

B) €1.00 = $1.4854

C) €1.00 = $0.6602

D) $1.00 = €0.6602

57) As of today, the spot exchange rate is €1.00 = $1.25 and the rates of inflation expected to

prevail for the next three years in the U.S. is 2 percent and 3 percent in the euro zone. What spot

exchange rate should prevail three years from now?

A) €1.00 = $1.2379

B) €1.00 = $1.2139

C) €1.00 = $0.9903

D) $1.00 = €1.2623

58) Your firm is based in southern Ireland (and thereby operates in euro, not pounds) and is

considering an investment in the United States.

The project involves selling widgets: you project a sales volume of 50,000 widgets per year, sales

price of $20 per widget with a contribution margin of $15 per widget.

The project will last for 5 years, require an investment of $1,000,000 at time zero (which will be

depreciated straight-line to $10,000 over the 5 years). Salvage value for the equipment is projected

to be $10,000. The project will operate in rented quarters: $300,000 rent is due at the start of each

year.

The corporate tax rate is 12½ percent in Ireland and 40 percent in the U.S.

For simplicity, assume that taxes are paid like sales taxes: immediately.

The spot exchange rate is $1.50 = €1.00. The cost of capital to the Irish firm for a domestic project

of this risk is 8 percent. The U.S. risk-free rate is 3 percent; the Irish risk-free rate is 2 percent.

What is CF0 in dollars?

59) Your firm is based in southern Ireland (and thereby operates in euro, not pounds) and is

considering an investment in the United States.

The project involves selling widgets: you project a sales volume of 50,000 widgets per year, sales

price of $20 per widget with a contribution margin of $15 per widget.

The project will last for 5 years, require an investment of $1,000,000 at time zero (which will be

depreciated straight-line to $10,000 over the 5 years). Salvage value for the equipment is projected

to be $10,000. The project will operate in rented quarters: $300,000 rent is due at the start of each

year.

The corporate tax rate is 12½ percent in Ireland and 40 percent in the U.S.

For simplicity, assume that taxes are paid like sales taxes: immediately.

The spot exchange rate is $1.50 = €1.00. The cost of capital to the Irish firm for a domestic project

of this risk is 8 percent. The U.S. risk-free rate is 3 percent; the Irish risk-free rate is 2 percent.

What is CF1 in dollars?

60) Your firm is based in southern Ireland (and thereby operates in euro, not pounds) and is

considering an investment in the United States.

The project involves selling widgets: you project a sales volume of 50,000 widgets per year, sales

price of $20 per widget with a contribution margin of $15 per widget.

The project will last for 5 years, require an investment of $1,000,000 at time zero (which will be

depreciated straight-line to $10,000 over the 5 years). Salvage value for the equipment is projected

to be $10,000. The project will operate in rented quarters: $300,000 rent is due at the start of each

year.

The corporate tax rate is 12½ percent in Ireland and 40 percent in the U.S.

For simplicity, assume that taxes are paid like sales taxes: immediately.

The spot exchange rate is $1.50 = €1.00. The cost of capital to the Irish firm for a domestic project

of this risk is 8 percent. The U.S. risk-free rate is 3 percent; the Irish risk-free rate is 2 percent.

What is CF5 in dollars?

61) Your firm is based in southern Ireland (and thereby operates in euro, not pounds) and is

considering an investment in the United States.

The project involves selling widgets: you project a sales volume of 50,000 widgets per year, sales

price of $20 per widget with a contribution margin of $15 per widget.

The project will last for 5 years, require an investment of $1,000,000 at time zero (which will be

depreciated straight-line to $10,000 over the 5 years). Salvage value for the equipment is projected

to be $10,000. The project will operate in rented quarters: $300,000 rent is due at the start of each

year.

The corporate tax rate is 12½ percent in Ireland and 40 percent in the U.S.

For simplicity, assume that taxes are paid like sales taxes: immediately.

The spot exchange rate is $1.50 = €1.00. The cost of capital to the Irish firm for a domestic project

of this risk is 8 percent. The U.S. risk-free rate is 3 percent; the Irish risk-free rate is 2 percent.

What is the NPV of the U.S.-based project to the Irish firm?

62) Your firm is based in southern Ireland (and thereby operates in euro, not pounds) and is

considering an investment in the United States.

The project involves selling widgets: you project a sales volume of 50,000 widgets per year, sales

price of $20 per widget with a contribution margin of $15 per widget.

The project will last for 5 years, require an investment of $1,000,000 at time zero (which will be

depreciated straight-line to $10,000 over the 5 years). Salvage value for the equipment is projected

to be $10,000. The project will operate in rented quarters: $300,000 rent is due at the start of each

year.

The corporate tax rate is 12½ percent in Ireland and 40 percent in the U.S.

For simplicity, assume that taxes are paid like sales taxes: immediately.

The spot exchange rate is $1.50 = €1.00. The cost of capital to the Irish firm for a domestic project

of this risk is 8 percent. The U.S. risk-free rate is 3 percent; the Irish risk-free rate is 2 percent.

What is the dollar-denominated IRR?

63) Your firm is based in southern Ireland (and thereby operates in euro, not pounds) and is

considering an investment in the United States.

The project involves selling widgets: you project a sales volume of 50,000 widgets per year, sales

price of $20 per widget with a contribution margin of $15 per widget.

The project will last for 5 years, require an investment of $1,000,000 at time zero (which will be

depreciated straight-line to $10,000 over the 5 years). Salvage value for the equipment is projected

to be $10,000. The project will operate in rented quarters: $300,000 rent is due at the start of each

year.

The corporate tax rate is 12½ percent in Ireland and 40 percent in the U.S.

For simplicity, assume that taxes are paid like sales taxes: immediately.

The spot exchange rate is $1.50 = €1.00. The cost of capital to the Irish firm for a domestic project

of this risk is 8 percent. The U.S. risk-free rate is 3 percent; the Irish risk-free rate is 2 percent.

What is the euro-denominated IRR?

64) Your firm is based in southern Ireland (and thereby operates in euro, not pounds) and is

considering an investment in the United States.

The project involves selling widgets: you project a sales volume of 50,000 widgets per year, sales

price of $20 per widget with a contribution margin of $15 per widget.

The project will last for 5 years, require an investment of $1,000,000 at time zero (which will be

depreciated straight-line to $10,000 over the 5 years). Salvage value for the equipment is projected

to be $10,000. The project will operate in rented quarters: $300,000 rent is due at the start of each

year.

The corporate tax rate is 12½ percent in Ireland and 40 percent in the U.S.

For simplicity, assume that taxes are paid like sales taxes: immediately.

The spot exchange rate is $1.50 = €1.00. The cost of capital to the Irish firm for a domestic project

of this risk is 8 percent. The U.S. risk-free rate is 3 percent; the Irish risk-free rate is 2 percent.

Find the break-even price (in dollars) and break-even quantity for the U.S. project.

65) Your firm is based in southern Ireland (and thereby operates in euro, not pounds) and is

considering an investment in the United States.

The project involves selling widgets: you project a sales volume of 50,000 widgets per year, sales

price of $20 per widget with a contribution margin of $15 per widget.

The project will last for 5 years, require an investment of $1,000,000 at time zero (which will be

depreciated straight-line to $10,000 over the 5 years). Salvage value for the equipment is projected

to be $10,000. The project will operate in rented quarters: $300,000 rent is due at the start of each

year.

The corporate tax rate is 12½ percent in Ireland and 40 percent in the U.S.

For simplicity, assume that taxes are paid like sales taxes: immediately.

The spot exchange rate is $1.50 = €1.00. The cost of capital to the Irish firm for a domestic project

of this risk is 8 percent. The U.S. risk-free rate is 3 percent; the Irish risk-free rate is 2 percent.

Repeat the above project analysis assuming that the Irish firm could replicate the project in Ireland.

(i.e. cash flow out the project in Ireland and find break-even price (in €), quantity, NPV, IRR (in

euro not dollars).

66) Consider the following international investment opportunity. It involves a gold mine that can

be opened at a cost, then produces a positive cash flow, but then requires environmental clean-up.

The current exchange rate is $1.60 = €1.00. The inflation rate in the U.S. is 6 percent and in the

euro zone 2 percent. The appropriate cost of capital to a U.S.-based firm for a domestic project of

this risk is 8 percent.

Find the euro-zone cost of capital to compute is the dollar-denominated NPV of this project.

67) Consider the following international investment opportunity. It involves a gold mine that can

be opened at a cost, then produces a positive cash flow, but then requires environmental clean-up.

The current exchange rate is $1.60 = €1.00. The inflation rate in the U.S. is 6 percent and in the

euro zone 2 percent. The appropriate cost of capital to a U.S.-based firm for a domestic project of

this risk is 8 percent.

Find the dollar cash flows to compute the dollar-denominated NPV of this project.

68) Consider the following international investment opportunity. It involves a gold mine that can

be opened at a cost, then produces a positive cash flow, but then requires environmental clean-up.

The current exchange rate is $1.60 = €1.00. The inflation rate in the U.S. is 6 percent and in the

euro zone 2 percent. The appropriate cost of capital to a U.S.-based firm for a domestic project of

this risk is 8 percent.

What is the dollar-denominated IRR of this project?