International Financial Management, 8e (Eun)

1) The financial manager’s responsibility involves

A) increasing the per share price of the company’s stock at any cost and by any means, ways and

fashion that is possible.

B) the shareholder wealth maximization.

C) which capital projects to select.

D) the shareholder wealth maximization and which capital projects to select.

2) Perhaps the most important decisions that confront the financial manager are

A) which capital projects to select.

B) the correct capital structure for the firm.

C) the correct capital structure for projects.

D) none of the options

3) Capital budgeting analysis is very important, because it

A) involves, usually expensive, investments in capital assets.

B) has to do with the productive capacity of a firm.

C) will determine how competitive and profitable a firm will be.

D) all of the options

4) Tiger Towers, Inc. is considering an expansion of their existing business, student apartments.

The new project will be built on some vacant land that the firm has just contracted to buy. The land

cost $1,000,000 and the payment is due today. Construction of a 20-unit office building will cost

$3 million; this expense will be depreciated straight-line over 30 years to zero salvage value; the

pretax value of the land and building in year 30 will be $18,000,000. The $3,000,000 construction

cost is to be paid today. The project will not change the risk level of the firm. The firm will lease 20

office suites at $20,000 per suite per year; payment is due at the start of the year; occupancy will

begin in one year. Variable cost is $3,500 per suite. Fixed costs, excluding depreciation, are

$75,000 per year. The project will require a $10,000 investment in net working capital.

= 10.0% = 11.20%

= 15.0% tax rate = 34% = 3

= 24.9% = 2%

What is the unlevered after-tax incremental cash flow for year 0?

A) –$3,660,000

B) –$5,100,000

C) –$4,000,000

D) –$4,010,000

5) Tiger Towers, Inc. is considering an expansion of their existing business, student apartments.

The new project will be built on some vacant land that the firm has just contracted to buy. The land

cost $1,000,000 and the payment is due today. Construction of a 20-unit office building will cost

$3 million; this expense will be depreciated straight-line over 30 years to zero salvage value; the

pretax value of the land and building in year 30 will be $18,000,000. The $3,000,000 construction

cost is to be paid today. The project will not change the risk level of the firm. The firm will lease 20

office suites at $20,000 per suite per year; payment is due at the start of the year; occupancy will

begin in one year. Variable cost is $3,500 per suite. Fixed costs, excluding depreciation, are

$75,000 per year. The project will require a $10,000 investment in net working capital.

= 10.0% = 11.20%

= 15.0% tax rate = 34% = 3

= 24.9% = 2%

What is the unlevered after-tax incremental cash flow for year 2?

A) –$4,610

B) $102,300

C) $202,300

D) $255,000

6) Tiger Towers, Inc. is considering an expansion of their existing business, student apartments.

The new project will be built on some vacant land that the firm has just contracted to buy. The land

cost $1,000,000 and the payment is due today. Construction of a 20-unit office building will cost

$3 million; this expense will be depreciated straight-line over 30 years to zero salvage value; the

pretax value of the land and building in year 30 will be $18,000,000. The $3,000,000 construction

cost is to be paid today. The project will not change the risk level of the firm. The firm will lease 20

office suites at $20,000 per suite per year; payment is due at the start of the year; occupancy will

begin in one year. Variable cost is $3,500 per suite. Fixed costs, excluding depreciation, are

$75,000 per year. The project will require a $10,000 investment in net working capital.

= 10.0% = 11.20%

= 15.0% tax rate = 34% = 3

= 24.9% = 2%

What is the unlevered after-tax incremental cash flow for year 30?

A) $12,432,300

B) $12,225,390

C) $12,332,300

D) $12,485,000

7) Tiger Towers, Inc. is considering an expansion of their existing business, student apartments.

The new project will be built on some vacant land that the firm has just contracted to buy. The land

cost $1,000,000 and the payment is due today. Construction of a 20-unit office building will cost

$3 million; this expense will be depreciated straight-line over 30 years to zero salvage value; the

pretax value of the land and building in year 30 will be $18,000,000. The $3,000,000 construction

cost is to be paid today. The project will not change the risk level of the firm. The firm will lease 20

office suites at $20,000 per suite per year; payment is due at the start of the year; occupancy will

begin in one year. Variable cost is $3,500 per suite. Fixed costs, excluding depreciation, are

$75,000 per year. The project will require a $10,000 investment in net working capital.

= 10.0% = 11.20%

= 15.0% tax rate = 34% = 3

= 24.9% = 2%

Assume that the firm will partially finance the project with a $3,000,000 interest-only 30-year loan

at 10.0 percent APR with annual payments.

What is the levered after-tax incremental cash flow for year 0?

A) −$1,010,000

B) −$1,000,000

C) −$660,000

D) −$2,100,000

8) Tiger Towers, Inc. is considering an expansion of their existing business, student apartments.

The new project will be built on some vacant land that the firm has just contracted to buy. The land

cost $1,000,000 and the payment is due today. Construction of a 20-unit office building will cost

$3 million; this expense will be depreciated straight-line over 30 years to zero salvage value; the

pretax value of the land and building in year 30 will be $18,000,000. The $3,000,000 construction

cost is to be paid today. The project will not change the risk level of the firm. The firm will lease 20

office suites at $20,000 per suite per year; payment is due at the start of the year; occupancy will

begin in one year. Variable cost is $3,500 per suite. Fixed costs, excluding depreciation, are

$75,000 per year. The project will require a $10,000 investment in net working capital.

= 10.0% = 11.20%

= 15.0% tax rate = 34% = 3

= 24.9% = 2%

Assume that the firm will partially finance the project with a $3,000,000 interest-only 30-year loan

at 10.0 percent APR with annual payments.

What is the levered after-tax incremental cash flow for year 1?

A) $4,300

B) −$202,610

C) −$95,700

D) $57,000

9) Tiger Towers, Inc. is considering an expansion of their existing business, student apartments.

The new project will be built on some vacant land that the firm has just contracted to buy. The land

cost $1,000,000 and the payment is due today. Construction of a 20-unit office building will cost

$3 million; this expense will be depreciated straight-line over 30 years to zero salvage value; the

pretax value of the land and building in year 30 will be $18,000,000. The $3,000,000 construction

cost is to be paid today. The project will not change the risk level of the firm. The firm will lease 20

office suites at $20,000 per suite per year; payment is due at the start of the year; occupancy will

begin in one year. Variable cost is $3,500 per suite. Fixed costs, excluding depreciation, are

$75,000 per year. The project will require a $10,000 investment in net working capital.

= 10.0% = 11.20%

= 15.0% tax rate = 34% = 3

= 24.9% = 2%

Assume that the firm will partially finance the project with a $3,000,000 interest-only 30-year loan

at 10.0 percent APR with annual payments.

What is the levered after-tax incremental cash flow for year 30?

A) $9,027,390

B) $9,234,300

C) $9,134,300

D) $9,287,000

10) Tiger Towers, Inc. is considering an expansion of their existing business, student apartments.

The new project will be built on some vacant land that the firm has just contracted to buy. The land

cost $1,000,000 and the payment is due today. Construction of a 20-unit office building will cost

$3 million; this expense will be depreciated straight-line over 30 years to zero salvage value; the

pretax value of the land and building in year 30 will be $18,000,000. The $3,000,000 construction

cost is to be paid today. The project will not change the risk level of the firm. The firm will lease 20

office suites at $20,000 per suite per year; payment is due at the start of the year; occupancy will

begin in one year. Variable cost is $3,500 per suite. Fixed costs, excluding depreciation, are

$75,000 per year. The project will require a $10,000 investment in net working capital.

= 10.0% = 11.20%

= 15.0% tax rate = 34% = 3

= 24.9% = 2%

Assume that the firm will partially finance the project with a subsidized $3,000,000 interest only

30-year loan at 8.0 percent APR with annual payments. Note that eight percent is less than the 10

percent that they normally borrow at. What is the NPV of the loan?

A) $198,469

B) $53,979.83

C) $102,727.55

D) $1,334,851.09

11) Tiger Towers, Inc. is considering an expansion of their existing business, student apartments.

The new project will be built on some vacant land that the firm has just contracted to buy. The land

cost $1,000,000 and the payment is due today. Construction of a 20-unit office building will cost

$3 million; this expense will be depreciated straight-line over 30 years to zero salvage value; the

pretax value of the land and building in year 30 will be $18,000,000. The $3,000,000 construction

cost is to be paid today. The project will not change the risk level of the firm. The firm will lease 20

office suites at $20,000 per suite per year; payment is due at the start of the year; occupancy will

begin in one year. Variable cost is $3,500 per suite. Fixed costs, excluding depreciation, are

$75,000 per year. The project will require a $10,000 investment in net working capital.

= 10.0% = 11.20%

= 15.0% tax rate = 34% = 3

= 24.9% = 2%

The firm’s tax rate is 34 percent. The firm’s pre-tax cost of debt is 8 percent; the firm’s

debt-to-equity ratio is 3; the risk-free rate is 3 percent; the beta of the firm’s common stock is 1.5;

the market risk premium is 9 percent. What is the firm’s cost of equity capital?

A) 33.33 percent

B) 10.85 percent

C) 13.12 percent

D) 16.5 percent

12) Tiger Towers, Inc. is considering an expansion of their existing business, student apartments.

The new project will be built on some vacant land that the firm has just contracted to buy. The land

cost $1,000,000 and the payment is due today. Construction of a 20-unit office building will cost

$3 million; this expense will be depreciated straight-line over 30 years to zero salvage value; the

pretax value of the land and building in year 30 will be $18,000,000. The $3,000,000 construction

cost is to be paid today. The project will not change the risk level of the firm. The firm will lease 20

office suites at $20,000 per suite per year; payment is due at the start of the year; occupancy will

begin in one year. Variable cost is $3,500 per suite. Fixed costs, excluding depreciation, are

$75,000 per year. The project will require a $10,000 investment in net working capital.

= 10.0% = 11.20%

= 15.0% tax rate = 34% = 3

= 24.9% = 2%

The firm’s tax rate is 34 percent. The firm’s pre-tax cost of debt is 8 percent; the firm’s

debt-to-equity ratio is 3; the risk-free rate is 3 percent; the beta of the firm’s common stock is 1.5;

the market risk premium is 9 percent. What is the required return on assets?

A) 33.33 percent

B) 10.85 percent

C) 13.12 percent

D) 16.5 percent

13)

i = rdebt = 6% OCF0 = −$100,000

Ku = rassets = 12% OCF1-4 = $39,800 = 25,000 × ($5 − $3) × (1 − 0.34) + $20,000 × 0.34

Kl = requity = 27.84% OCF5 = $43,100 = $39,800 + $5,000 × (1 − 0.34)

K = rWACC = 8.74% π = Tax rate = 34% Debt-to-equity ratio = 4 Risk-free rate = 2%

The 5-year project requires equipment that costs $100,000. If undertaken, the shareholders will

contribute $20,000 cash and borrow $80,000 at 6 percent with an interest-only loan with a maturity

of 5 years and annual interest payments. The equipment will be depreciated straight-line to zero

over the 5-year life of the project. There will be a pre-tax salvage value of $5,000. There are no

other start-up costs at year 0. During years 1 through 5, the firm will sell 25,000 units of product at

$5; variable costs are $3; there are no fixed costs.

What is the NPV of the project using the WACC methodology?

A) $49,613.03

B) $58,028.68

C) $102,727.55

D) $315,666.16

14)

i = rdebt = 6% OCF0 = −$100,000

Ku = rassets = 12% OCF1-4 = $39,800 = 25,000 × ($5 − $3) × (1 − 0.34) + $20,000 × 0.34

Kl = requity = 27.84% OCF5 = $43,100 = $39,800 + $5,000 × (1 − 0.34)

K = rWACC = 8.74% π = Tax rate = 34% Debt-to-equity ratio = 4 Risk-free rate = 2%

The 5-year project requires equipment that costs $100,000. If undertaken, the shareholders will

contribute $20,000 cash and borrow $80,000 at 6 percent with an interest-only loan with a maturity

of 5 years and annual interest payments. The equipment will be depreciated straight-line to zero

over the 5-year life of the project. There will be a pre-tax salvage value of $5,000. There are no

other start-up costs at year 0. During years 1 through 5, the firm will sell 25,000 units of product at

$5; variable costs are $3; there are no fixed costs.

What is the NPV of the project using the APV methodology?

A) $49,613.03

B) $198,469

C) $102,727.55

D) $149,580.12

15)

i = rdebt = 10% OCF0 = −$100,000

Ku = rassets = 15% OCF1-4 = $39,800 = 25,000 × ($5 − $3) × (1 − 0.34) + $20,000 × 0.34

Kl = requity = 24.9% OCF5 = $43,100 = $39,800 + $5,000 × (1 − 0.34)

K = rWACC = 11.20% Tax rate = 34% Debt-to-equity ratio = 3 Risk-free rate = 2%

The 5-year project requires equipment that costs $100,000. If undertaken, the shareholders will

contribute $25,000 cash and borrow $75,000 with an interest-only loan with a maturity of 5 years

and annual interest payments. The equipment will be depreciated straight-line to zero over the

5-year life of the project. There will be a pre-tax salvage value of $5,000. There are no other

start-up costs at year 0. During years 1 through 5, the firm will sell 25,000 units of product at $5;

variable costs are $3; there are no fixed costs.

What is the NPV of the project using the WACC methodology?

A) $58,028.68

B) $49,613.03

C) $48,300.47

D) $102,727.55

16)

i = rdebt = 10% OCF0 = −$100,000

Ku = rassets = 15% OCF1-4 = $39,800 = 25,000 × ($5 − $3) × (1 − 0.34) + $20,000 × 0.34

Kl = requity = 24.9% OCF5 = $43,100 = $39,800 + $5,000 × (1 − 0.34)

K = rWACC = 11.20% Tax rate = 34% Debt-to-equity ratio = 3 Risk-free rate = 2%

The 5-year project requires equipment that costs $100,000. If undertaken, the shareholders will

contribute $25,000 cash and borrow $75,000 with an interest-only loan with a maturity of 5 years

and annual interest payments. The equipment will be depreciated straight-line to zero over the

5-year life of the project. There will be a pre-tax salvage value of $5,000. There are no other

start-up costs at year 0. During years 1 through 5, the firm will sell 25,000 units of product at $5;

variable costs are $3; there are no fixed costs.

When using the APV methodology, what is the NPV of the depreciation tax shield?

A) $32,051.52

B) $25,777.35

C) $22,794.65

D) $97,152.98

17)

i = rdebt = 10% OCF0 = −$100,000

Ku = rassets = 15% OCF1-4 = $39,800 = 25,000 × ($5 − $3) × (1 − 0.34) + $20,000 × 0.34

Kl = requity = 24.9% OCF5 = $43,100 = $39,800 + $5,000 × (1 − 0.34)

K = rWACC = 11.20% Tax rate = 34% Debt-to-equity ratio = 3 Risk-free rate = 2%

The 5-year project requires equipment that costs $100,000. If undertaken, the shareholders will

contribute $25,000 cash and borrow $75,000 with an interest-only loan with a maturity of 5 years

and annual interest payments. The equipment will be depreciated straight-line to zero over the

5-year life of the project. There will be a pre-tax salvage value of $5,000. There are no other

start-up costs at year 0. During years 1 through 5, the firm will sell 25,000 units of product at $5;

variable costs are $3; there are no fixed costs.

When using the APV methodology, what is the NPV of the interest tax shield?

A) $9,666.51

B) $12,019.32

C) $9,377.31

D) $7,000.73

18) Today is January 1, 2009. The state of Iowa has offered your firm a subsidized loan. It will be

in the amount of $10,000,000 at an interest rate of 5 percent and have ANNUAL (amortizing)

payments over 3 years. The first payment is due today and your taxes are due January 1 of each

year on the previous year’s income. The yield to maturity on your firm’s existing debt is 8 percent.

What is the APV of this subsidized loan? If you rounded in your intermediate steps, the answer

may be slightly different from what you got. Choose the closest.

A) −$3,497,224.43

B) $417,201.05

C) $840,797

D) none of the options

19) Today is January 1, 2009. The state of Iowa has offered your firm a subsidized loan. It will be

in the amount of $10,000,000 at an interest rate of 5 percent and have ANNUAL (amortizing)

payments over 3 years. The first payment is due December 31, 2009 and your taxes are due

January 1 of each year on the previous year‘s income. The yield to maturity on your firm’s existing

debt is 8 percent. What is the APV of this subsidized loan? Note that I did not round my

intermediate steps. If you did, your answer may be off by a bit. Select the answer closest to yours.

A) −$3,497,224.43

B) $417,201.05

C) $840,797

D) none of the options

20) The required return on assets is 18 percent. The firm can borrow at 12.5 percent; firm’s target

debt to value ratio is 3/5. The corporate tax rate is 34 percent, and the risk-free rate is 4 percent and

the market risk premium is 9.2 percent.

What is the weighted average cost of capital?

A) 12.15 percent

B) 13.02 percent

C) 14.33 percent

D) 23.45 percent

21) Your firm is in the 34 percent tax bracket. The yield to maturity on your existing bonds is 8

percent. The state of Georgia offers to loan your firm $1,000,000 with a two year amortizing loan

at a 5 percent rate of interest and annual payments due at the end of the year.

The interest will be deductible at the time that you pay. What is the APV of this below-market loan

to your firm? I did not round any of my intermediate steps. You might be a little bit off. Pick the

answer closest to yours.

A) $64,157.38

B) $417,201.05

C) $840,797

D) none of the options

22) The firm’s tax rate is 34 percent. The firm’s pre-tax cost of debt is 8 percent; the firm’s

debt-to-equity ratio is 3; the risk-free rate is 3 percent; the beta of the firm’s common stock is 1.5;

the market risk premium is 9 percent. Calculate the weighted average cost of capital.

A) 33.33 percent

B) 8.09 percent

C) 9.02 percent

D) 16.5 percent

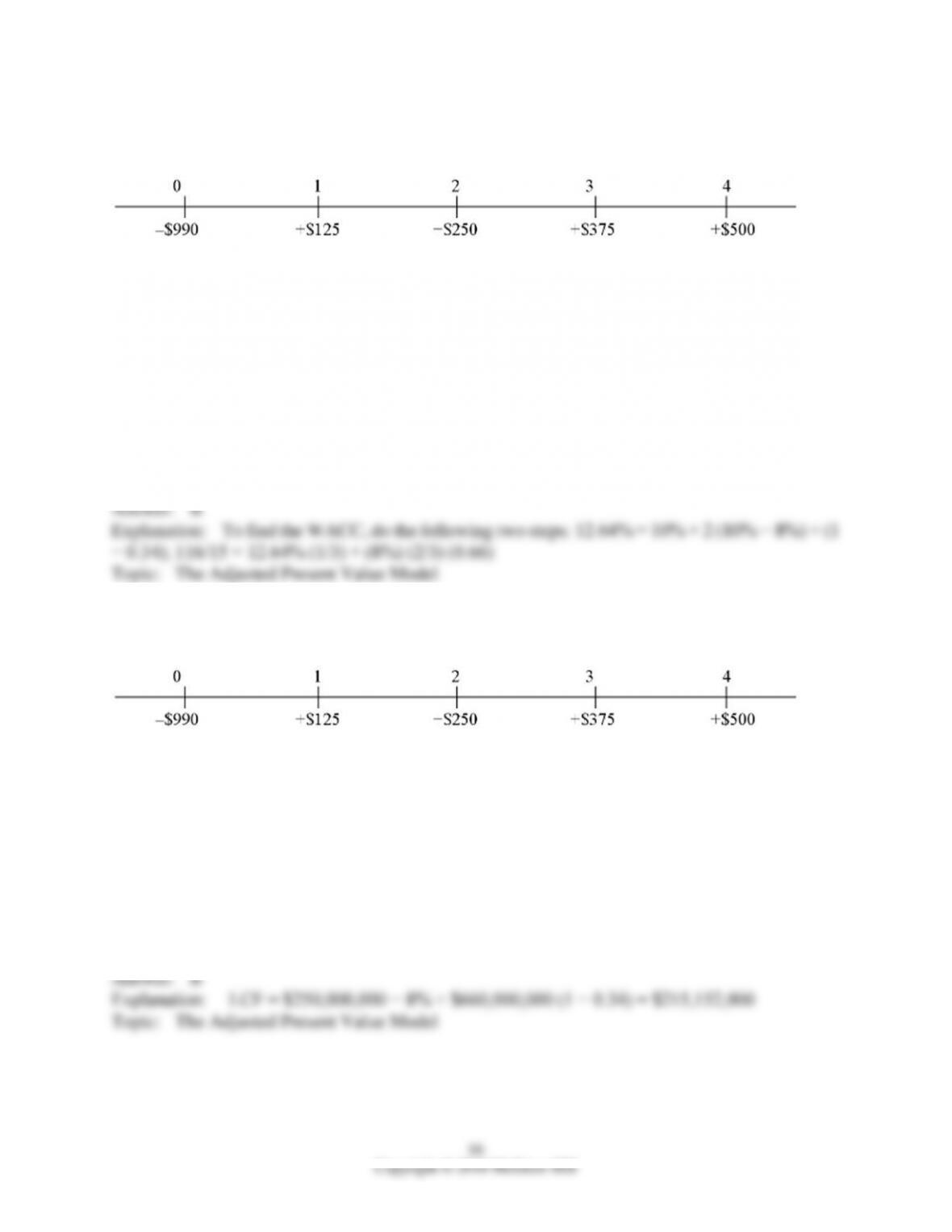

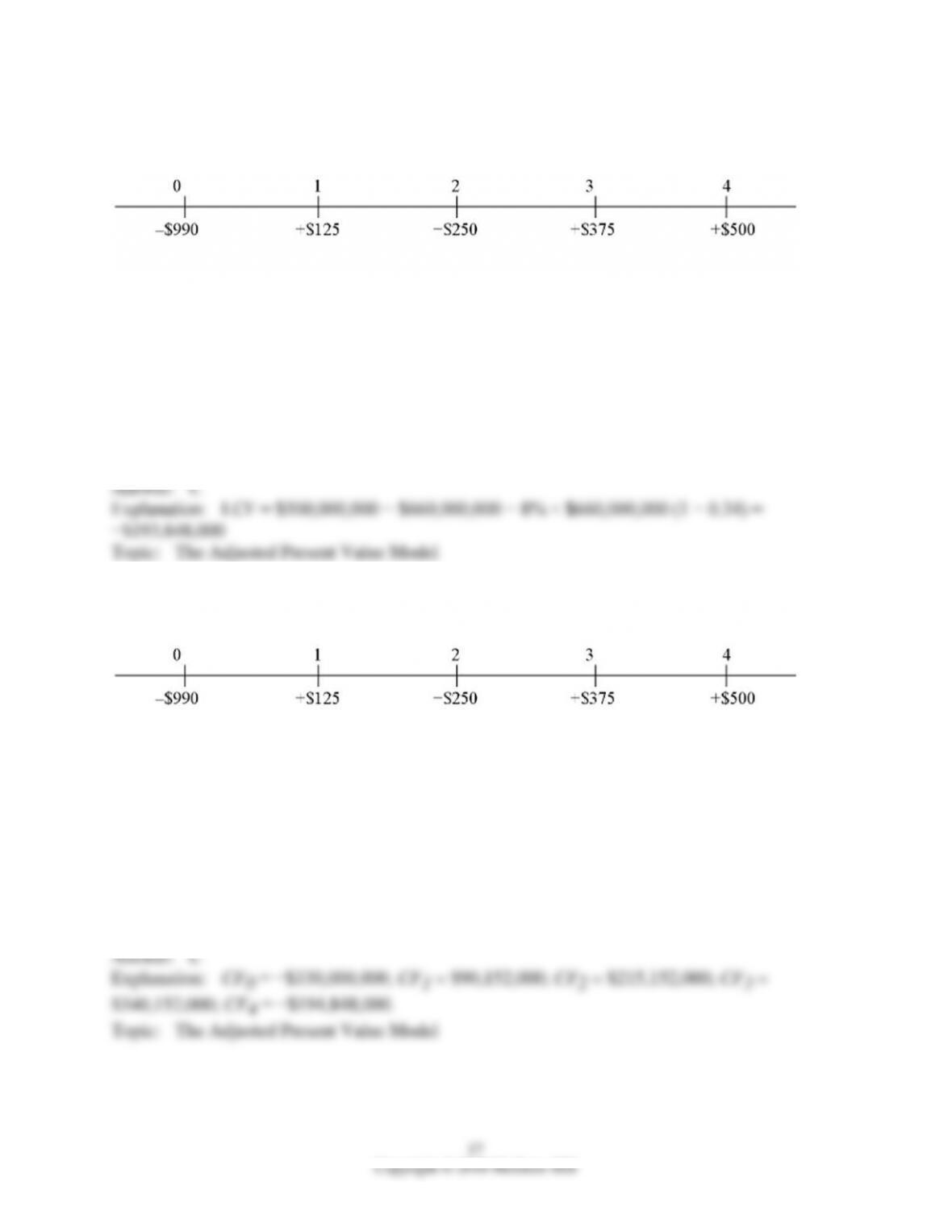

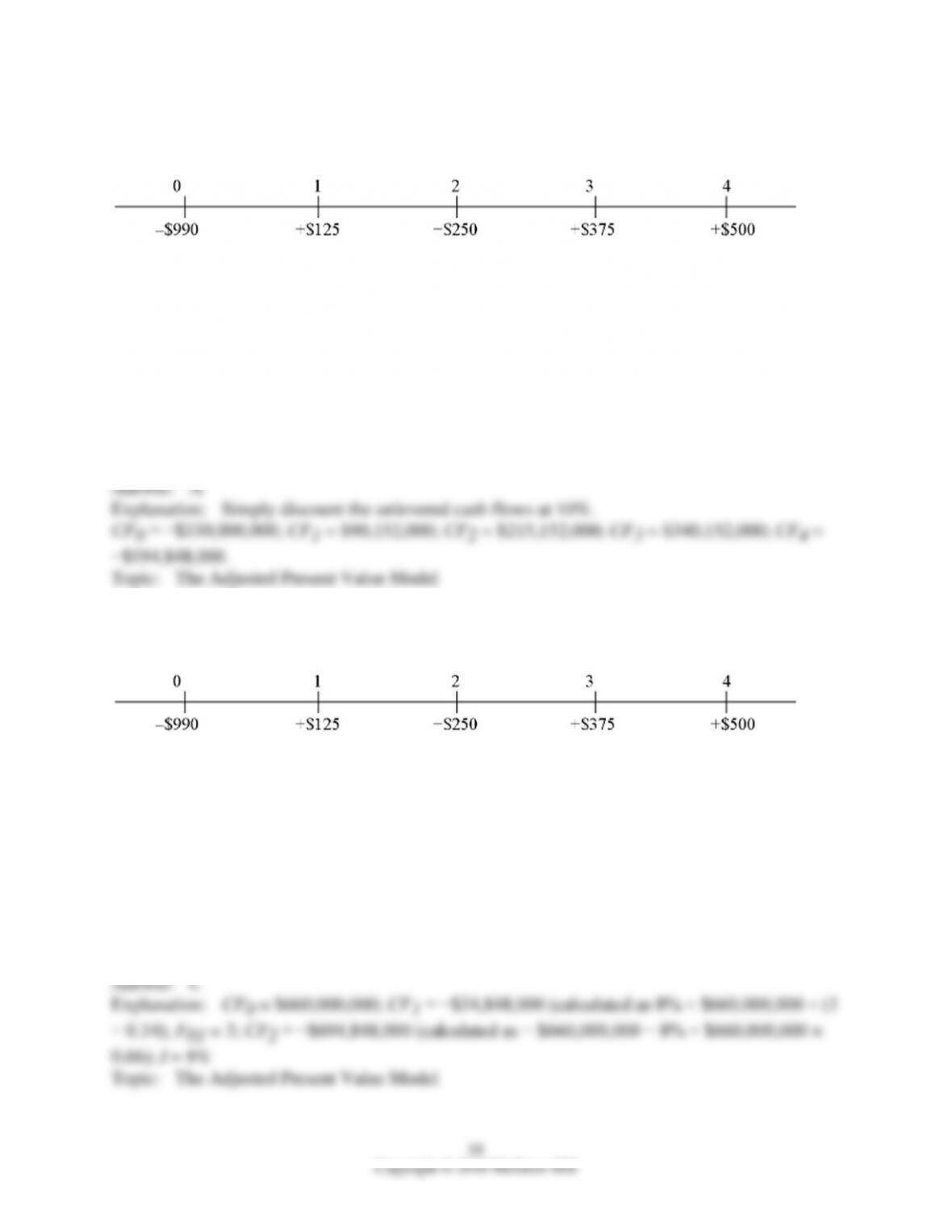

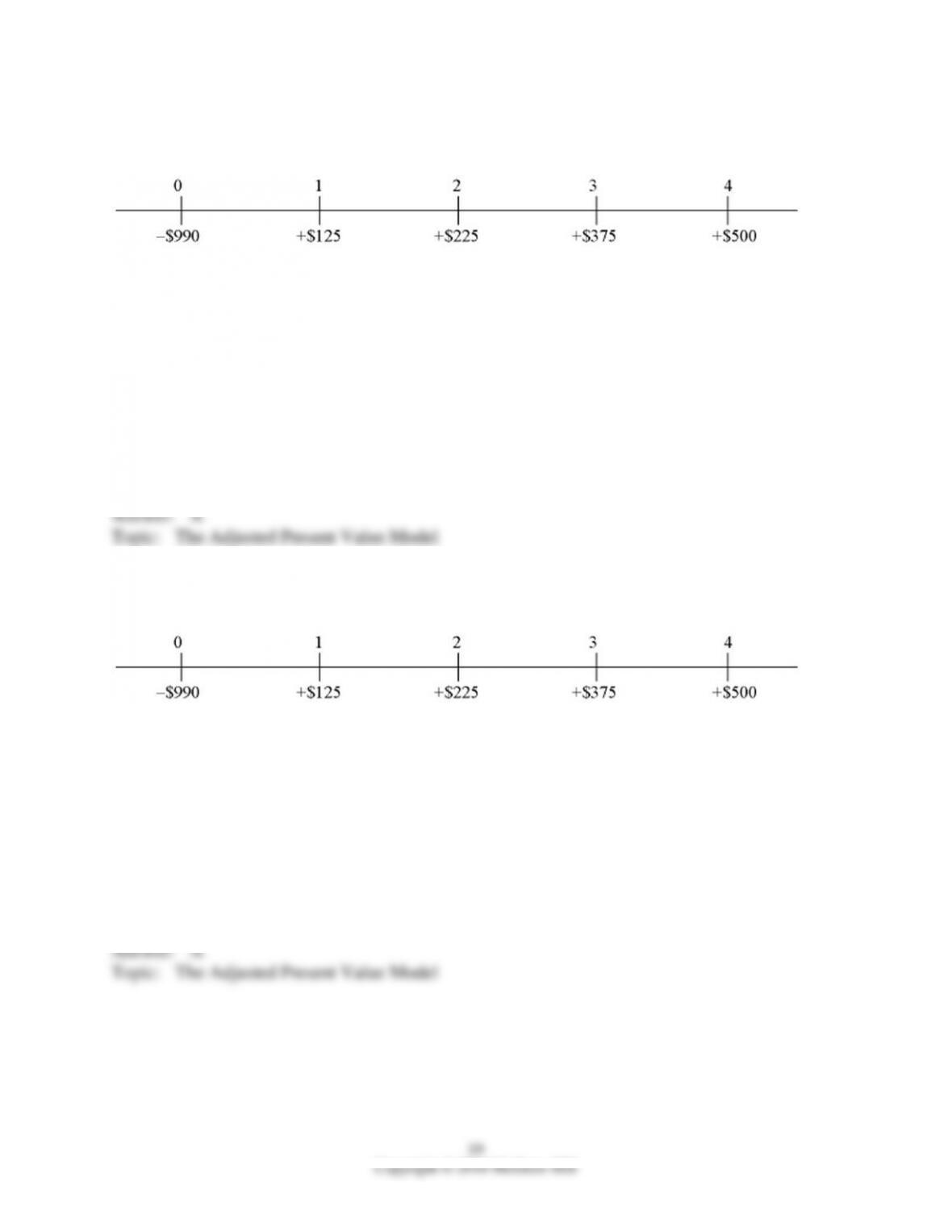

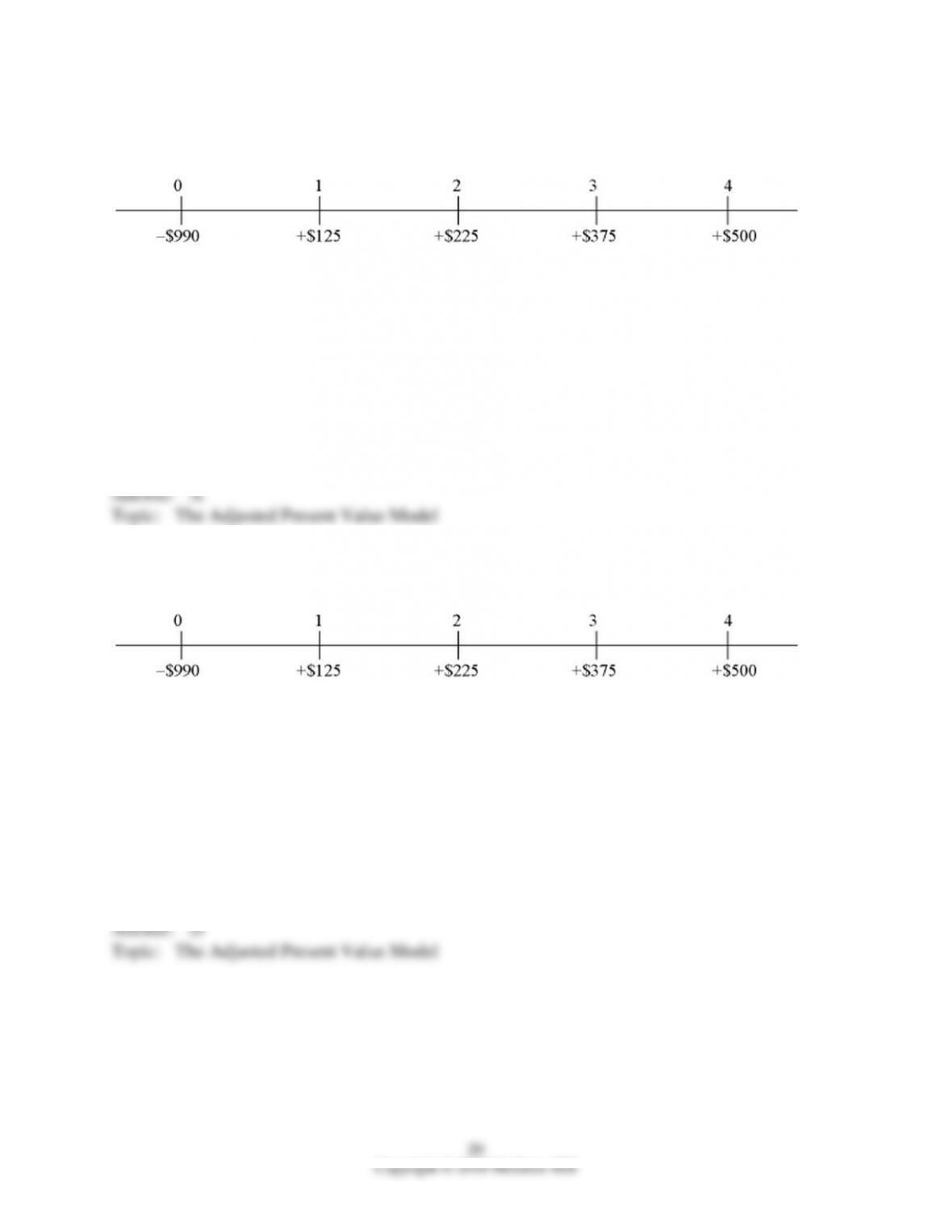

23) Consider a project of the Cornell Haul Moving Company, the timing and size of the

incremental after-tax cash flows (for an all-equity firm) are shown below in millions:

The firm’s tax rate is 34 percent; the firm’s bonds trade with a yield to maturity of 8 percent; the

current and target debt-equity ratio is 2; if the firm were financed entirely with equity, the required

return would be 10 percent.

Using the weighted average cost of capital methodology, what is the NPV? I didn’t round my

intermediate steps. If you do, you’re not going to get the right answer.

A) −$1,406,301.25

B) $12,494,643.75

C) $36,580,767.55

D) $108,994.618.20

24) Consider a project of the Cornell Haul Moving Company, the timing and size of the

incremental after-tax cash flows (for an all-equity firm) are shown below in millions:

The firm’s tax rate is 34 percent; the firm’s bonds trade with a yield to maturity of 8 percent; the

current and target debt-equity ratio is 2; if the firm were financed entirely with equity, the required

return would be 10 percent.

What is the levered after-tax incremental cash flow for year 2?

A) $185,796,000

B) $215,152,000

C) $267,952,000

D) $284,848,000

25) Consider a project of the Cornell Haul Moving Company, the timing and size of the

incremental after-tax cash flows (for an all-equity firm) are shown below in millions:

The firm’s tax rate is 34 percent; the firm’s bonds trade with a yield to maturity of 8 percent; the

current and target debt-equity ratio is 2; if the firm were financed entirely with equity, the required

return would be 10 percent.

What is the levered after-tax incremental cash flow for year 4?

A) $281,704,000

B) $465,152,000

C) −$194,848,000

D) $460,796,000

26) Consider a project of the Cornell Haul Moving Company, the timing and size of the

incremental after-tax cash flows (for an all-equity firm) are shown below in millions:

The firm’s tax rate is 34 percent; the firm’s bonds trade with a yield to maturity of 8 percent; the

current and target debt-equity ratio is 2; if the firm were financed entirely with equity, the required

return would be 10 percent.

Using the flow to equity methodology, what is the value of the equity claim?

A) −$1,540,000

B) $446,570,866.00

C) $36,580,767.55

D) $470,953,393.70

27) Consider a project of the Cornell Haul Moving Company, the timing and size of the

incremental after-tax cash flows (for an all-equity firm) are shown below in millions:

The firm’s tax rate is 34 percent; the firm’s bonds trade with a yield to maturity of 8 percent; the

current and target debt-equity ratio is 2; if the firm were financed entirely with equity, the required

return would be 10 percent.

Using the APV method, what is the value of this project to an all-equity firm?

A) −$46,502,288.10

B) $12,494,643.75

C) $36,580,767.55

D) −$67,163,445.12

28) Consider a project of the Cornell Haul Moving Company, the timing and size of the

incremental after-tax cash flows (for an all-equity firm) are shown below in millions:

The firm’s tax rate is 34 percent; the firm’s bonds trade with a yield to maturity of 8 percent; the

current and target debt-equity ratio is 2; if the firm were financed entirely with equity, the required

return would be 10 percent.

Using the APV method, what is the value of the debt side effects?

A) $239,072,652.70

B) $66,891,713.66

C) $59,459,301.03

D) $660,000,000

29) Consider a project of the Cornell Haul Moving Company, the timing and size of the

incremental after-tax cash flows (for an all-equity firm) are shown below in millions:

The firm’s tax rate is 34 percent; the firm’s bonds trade with a yield to maturity of 8 percent; the

current and target debt-equity ratio is 3; if the firm were financed entirely with equity, the required

return would be 10 percent.

Using the weighted average cost of capital methodology, what is the NPV? I didn’t round my

intermediate steps. If you do, you’re not going to get the right answer.

A) −$1,406,301.25

B) $12,494,643.75

C) $36,580,767.55

D) $108,994.618.20

30) Consider a project of the Cornell Haul Moving Company, the timing and size of the

incremental after-tax cash flows (for an all-equity firm) are shown below in millions:

The firm’s tax rate is 34 percent; the firm’s bonds trade with a yield to maturity of 8 percent; the

current and target debt-equity ratio is 3; if the firm were financed entirely with equity, the required

return would be 10 percent.

What is the levered after-tax incremental cash flow for year 2?

A) $185,796,000

B) $215,152,000

C) $267,952,000

D) $284,848,000

31) Consider a project of the Cornell Haul Moving Company, the timing and size of the

incremental after-tax cash flows (for an all-equity firm) are shown below in millions:

The firm’s tax rate is 34 percent; the firm’s bonds trade with a yield to maturity of 8 percent; the

current and target debt-equity ratio is 3; if the firm were financed entirely with equity, the required

return would be 10 percent.

What is the levered after-tax incremental cash flow for year 4?

A) −$281,704,000

B) $465,152,000

C) −$194,848,000

D) $460,796,000

32) Consider a project of the Cornell Haul Moving Company, the timing and size of the

incremental after-tax cash flows (for an all-equity firm) are shown below in millions:

The firm’s tax rate is 34 percent; the firm’s bonds trade with a yield to maturity of 8 percent; the

current and target debt-equity ratio is 3; if the firm were financed entirely with equity, the required

return would be 10 percent.

Using the flow to equity methodology, what is the value of the equity claim?

A) −$1,540,000

B) $446,570,866.00

C) $36,580,767.55

D) $30,716,236.13