76) Consider the situation of firm A and firm B. The current exchange rate is $1.50/€. Firm A is a

U.S. MNC and wants to borrow €40 million for 2 years. Firm B is a French MNC and wants to

borrow $60 million for 2 years. Their borrowing opportunities are as shown; both firms have AAA

credit ratings.

$

€

A

$

7

%

€

6

%

B

$

8

%

€

5

%

If firm B could use the forward exchange markets to redenominate a 2-year €40m 5 percent euro

loan into a 2-year USD-denominated loan, what would be the interest rate?

77) Consider the situation of firm A and firm B. The current exchange rate is $1.50/€. Firm A is a

U.S. MNC and wants to borrow €40 million for 2 years. Firm B is a French MNC and wants to

borrow $60 million for 2 years. Their borrowing opportunities are as shown; both firms have AAA

credit ratings.

$

€

A

$

7

%

€

6

%

B

$

8

%

€

5

%

Explain how this opportunity affects which swap firm B will be willing to participate in.

78) Consider the situation of firm A and firm B. The current exchange rate is $1.50/€. Firm A is a

U.S. MNC and wants to borrow €40 million for 2 years. Firm B is a French MNC and wants to

borrow $60 million for 2 years. Their borrowing opportunities are as shown; both firms have AAA

credit ratings.

$

€

A

$

7

%

€

6

%

B

$

8

%

€

5

%

Devise a direct swap for A and B that has no swap bank. Show their external borrowing.

79) Consider the situation of firm A and firm B. The current exchange rate is $1.50/€. Firm A is a

U.S. MNC and wants to borrow €40 million for 2 years. Firm B is a French MNC and wants to

borrow $60 million for 2 years. Their borrowing opportunities are as shown; both firms have AAA

credit ratings.

$

€

A

$

7

%

€

6

%

B

$

8

%

€

5

%

Act as a swap bank and quote bid and ask prices to A and B that are attractive to A and B and

promise to make at least 20bp for your firm.

USD

Euro

Bid

Ask

Bid

Ask

Bid

7

%

7.1

%

%

%

$

€

A

$

7

%

€

6

%

B

$

8

%

€

5

%

81) Consider the situation of firm A and firm B. The current exchange rate is $2.00/£ Firm A is a

U.S. MNC and wants to borrow £30 million for 2 years. Firm B is a British MNC and wants to

borrow $60 million for 2 years. Their borrowing opportunities are as shown, both firms have AAA

credit ratings.

$

£

A

$

6

%

£

5

%

B

$

7

%

£

4

%

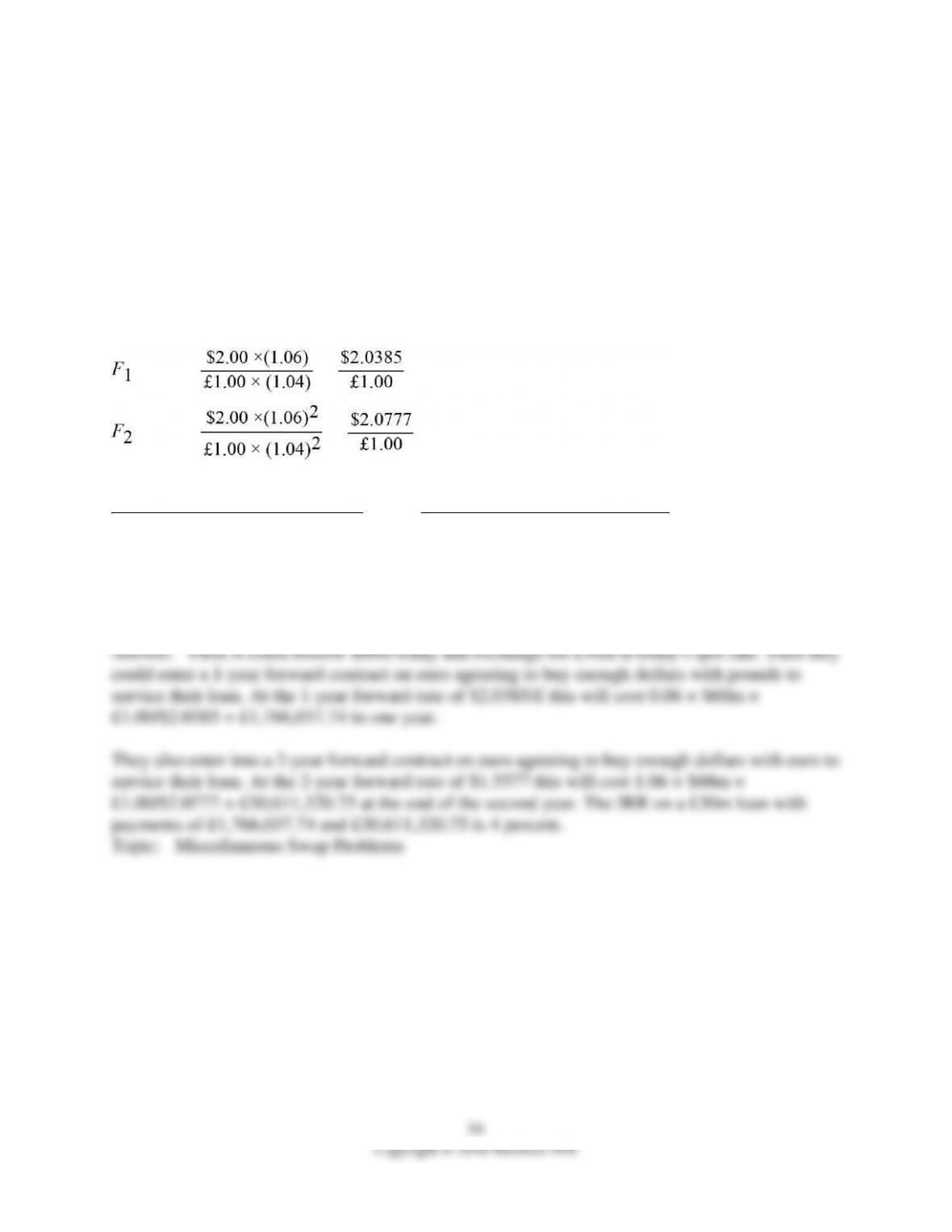

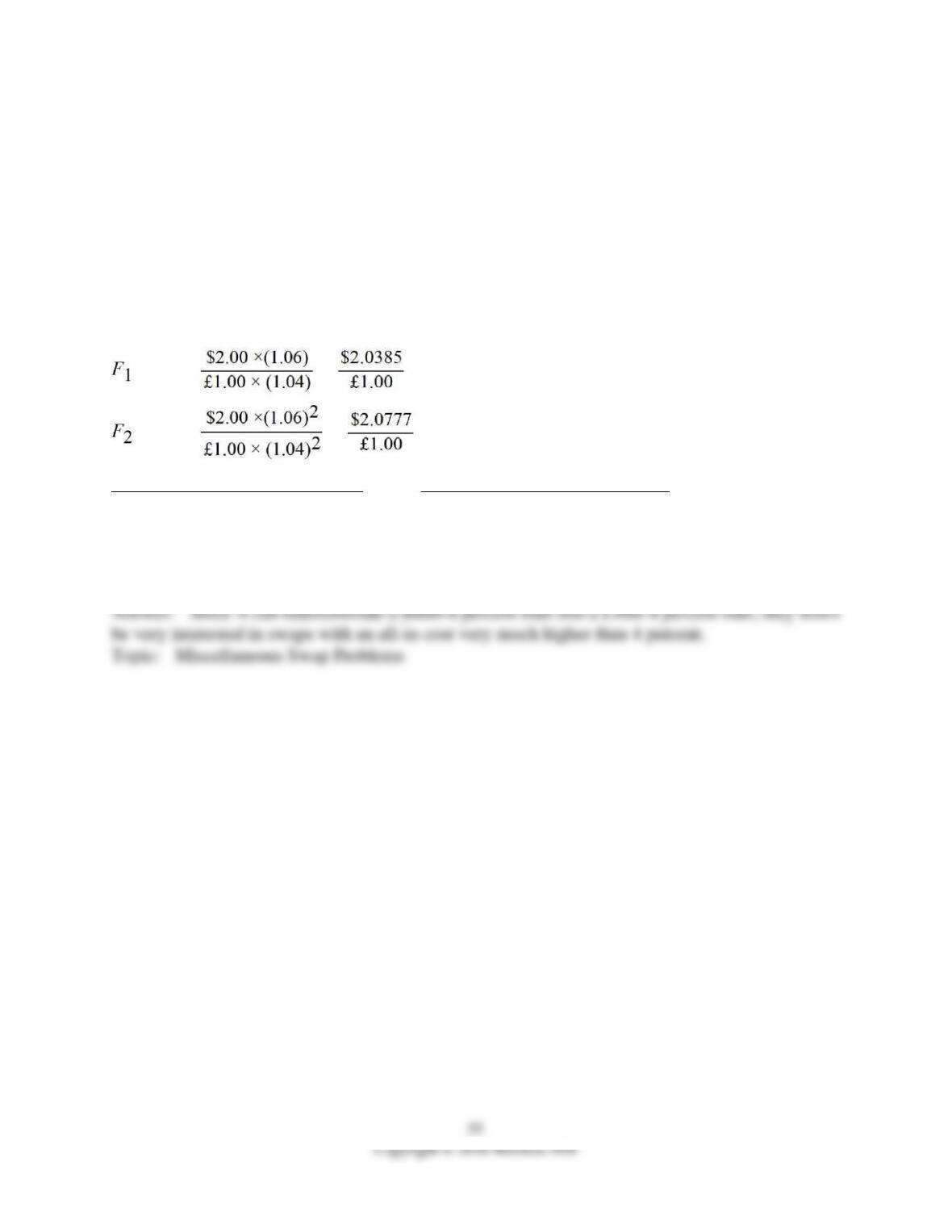

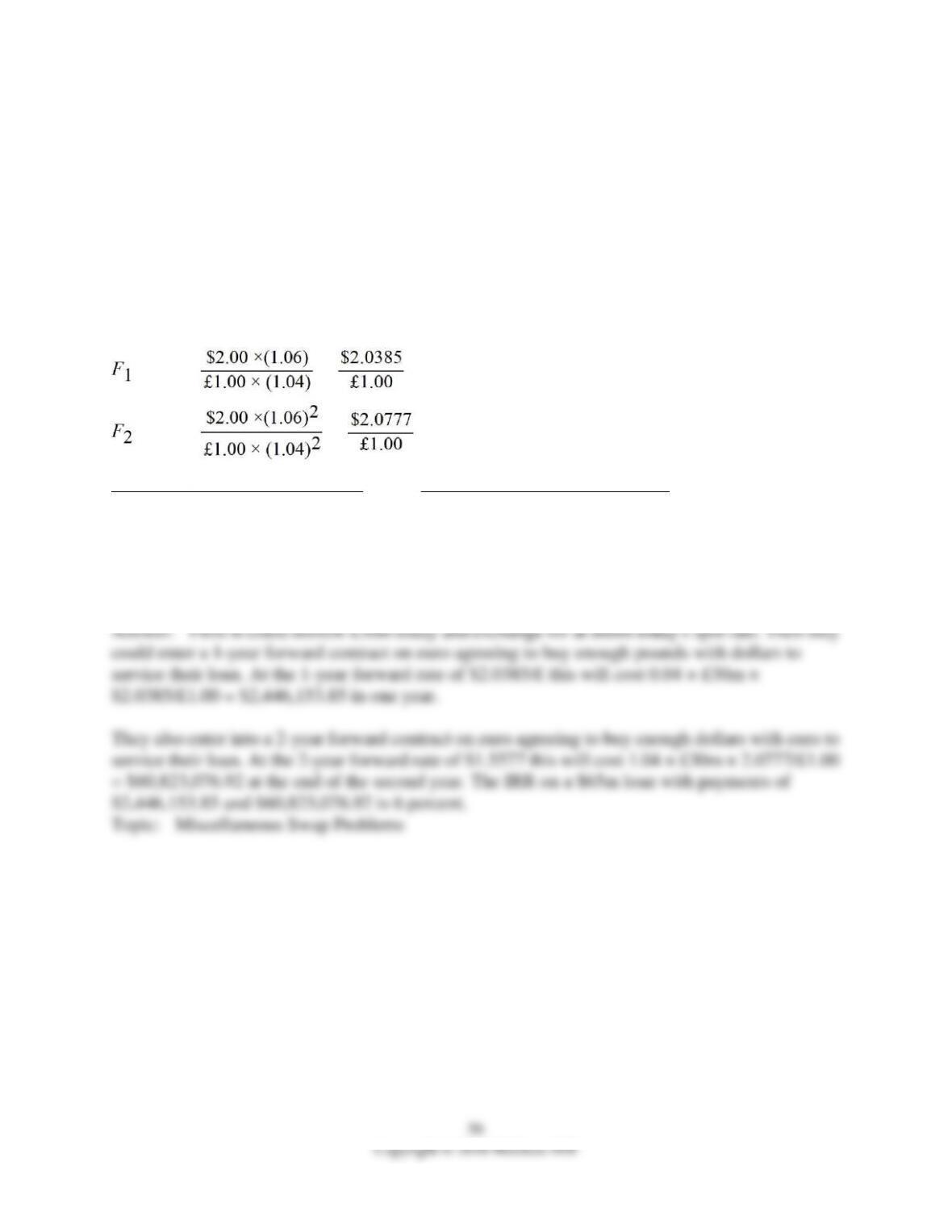

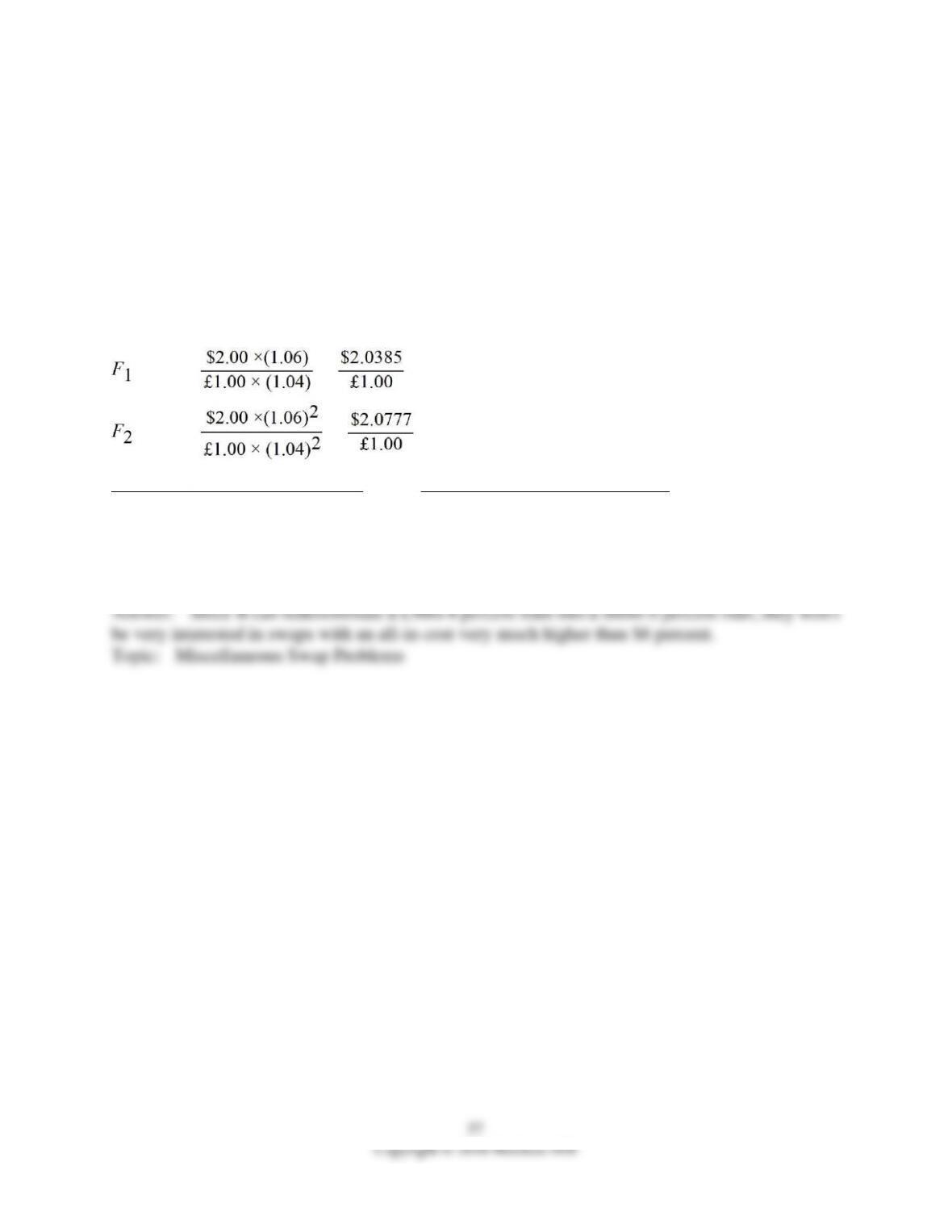

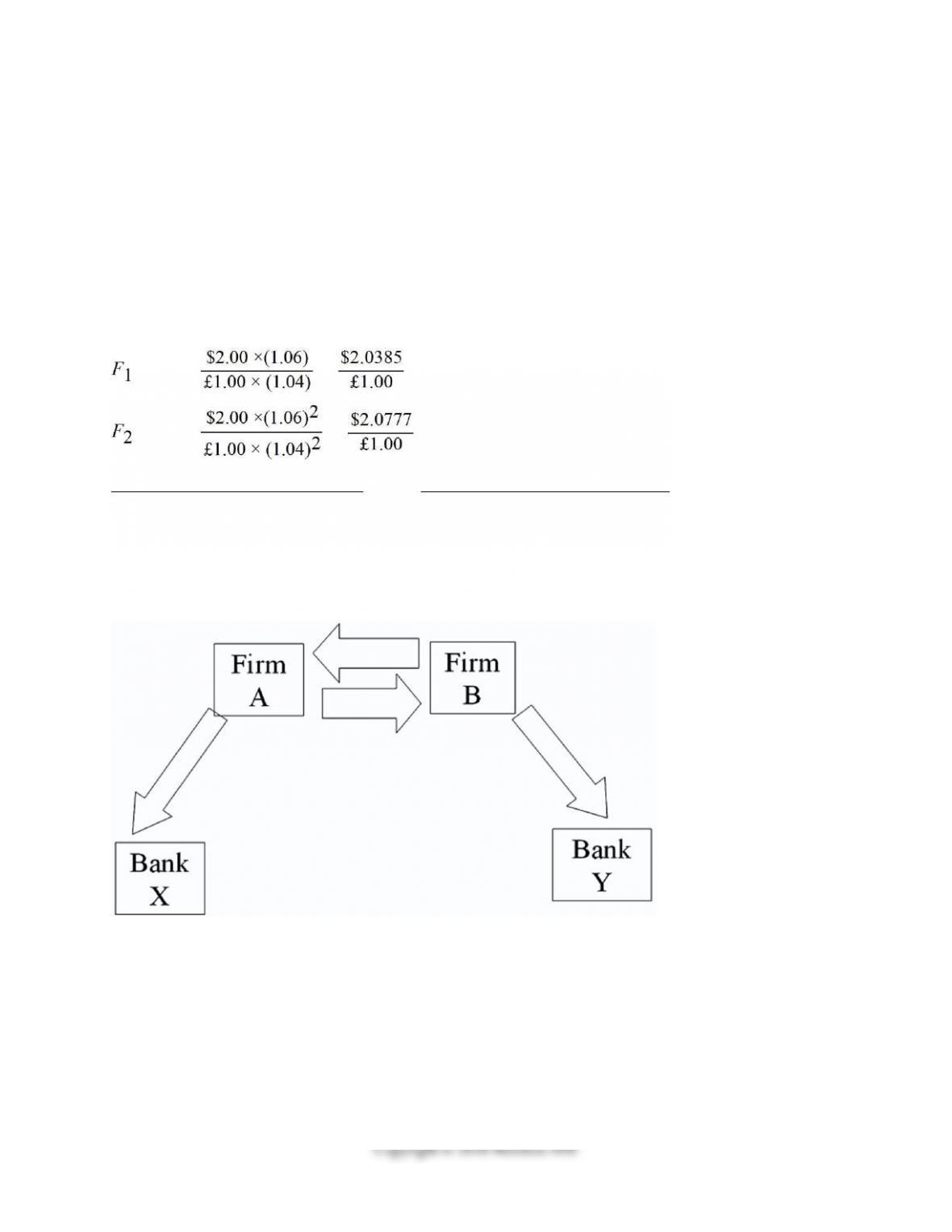

What are the IRP 1-year and 2-year forward exchange rates?

82) Consider the situation of firm A and firm B. The current exchange rate is $2.00/£ Firm A is a

U.S. MNC and wants to borrow £30 million for 2 years. Firm B is a British MNC and wants to

borrow $60 million for 2 years. Their borrowing opportunities are as shown, both firms have AAA

credit ratings.

$

£

A

$

6

%

£

5

%

B

$

7

%

£

4

%

Explain how firm A could use the forward exchange markets to redenominate a 2-year $60m 6

percent USD loan into a 2-year pound denominated loan.

83) Consider the situation of firm A and firm B. The current exchange rate is $2.00/£ Firm A is a

U.S. MNC and wants to borrow £30 million for 2 years. Firm B is a British MNC and wants to

borrow $60 million for 2 years. Their borrowing opportunities are as shown, both firms have AAA

credit ratings.

$

£

A

$

6

%

£

5

%

B

$

7

%

£

4

%

If firm A could use the forward exchange markets to redenominate a 2-year $60m 6 percent USD

loan into a 2-year pound denominated loan, what would be the interest rate?

84) Consider the situation of firm A and firm B. The current exchange rate is $2.00/£ Firm A is a

U.S. MNC and wants to borrow £30 million for 2 years. Firm B is a British MNC and wants to

borrow $60 million for 2 years. Their borrowing opportunities are as shown, both firms have AAA

credit ratings.

$

£

A

$

6

%

£

5

%

B

$

7

%

£

4

%

Explain how this opportunity affects which swap firm A will be willing to participate in.

85) Consider the situation of firm A and firm B. The current exchange rate is $2.00/£ Firm A is a

U.S. MNC and wants to borrow £30 million for 2 years. Firm B is a British MNC and wants to

borrow $60 million for 2 years. Their borrowing opportunities are as shown, both firms have AAA

credit ratings.

$

£

A

$

6

%

£

5

%

B

$

7

%

£

4

%

Explain how firm B could use the forward exchange markets to redenominate a 2-year £30m 4

percent pound sterling loan into a 2-year USD-denominated loan.

86) Consider the situation of firm A and firm B. The current exchange rate is $2.00/£ Firm A is a

U.S. MNC and wants to borrow £30 million for 2 years. Firm B is a British MNC and wants to

borrow $60 million for 2 years. Their borrowing opportunities are as shown, both firms have AAA

credit ratings.

$

£

A

$

6

%

£

5

%

B

$

7

%

£

4

%

If firm B could use the forward exchange markets to redenominate a 2-year £30m 4 percent pound

sterling loan into a 2-year USD-denominated loan, what would be the interest rate?

87) Consider the situation of firm A and firm B. The current exchange rate is $2.00/£ Firm A is a

U.S. MNC and wants to borrow £30 million for 2 years. Firm B is a British MNC and wants to

borrow $60 million for 2 years. Their borrowing opportunities are as shown, both firms have AAA

credit ratings.

$

£

A

$

6

%

£

5

%

B

$

7

%

£

4

%

Explain how this opportunity affects which swap firm B will be willing to participate in.

88) Consider the situation of firm A and firm B. The current exchange rate is $2.00/£ Firm A is a

U.S. MNC and wants to borrow £30 million for 2 years. Firm B is a British MNC and wants to

borrow $60 million for 2 years. Their borrowing opportunities are as shown, both firms have AAA

credit ratings.

$

£

A

$

6

%

£

5

%

B

$

7

%

£

4

%

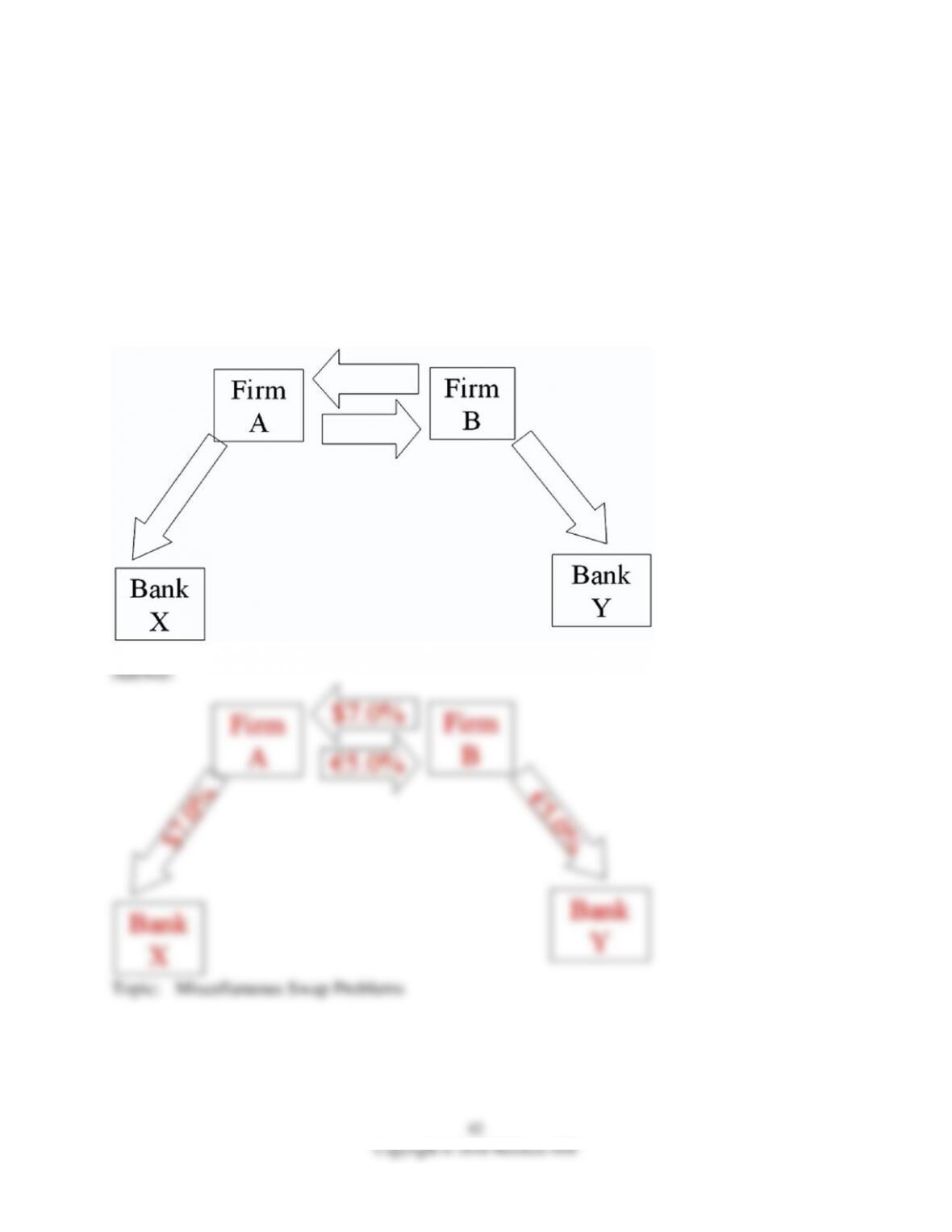

Devise a direct swap for A and B that has no swap bank. Show their external borrowing.

89) Consider the situation of firm A and firm B. The current exchange rate is $2.00/£ Firm A is a

U.S. MNC and wants to borrow £30 million for 2 years. Firm B is a British MNC and wants to

borrow $60 million for 2 years. Their borrowing opportunities are as shown, both firms have AAA

credit ratings.

$

£

A

$

6

%

£

5

%

B

$

7

%

£

4

%

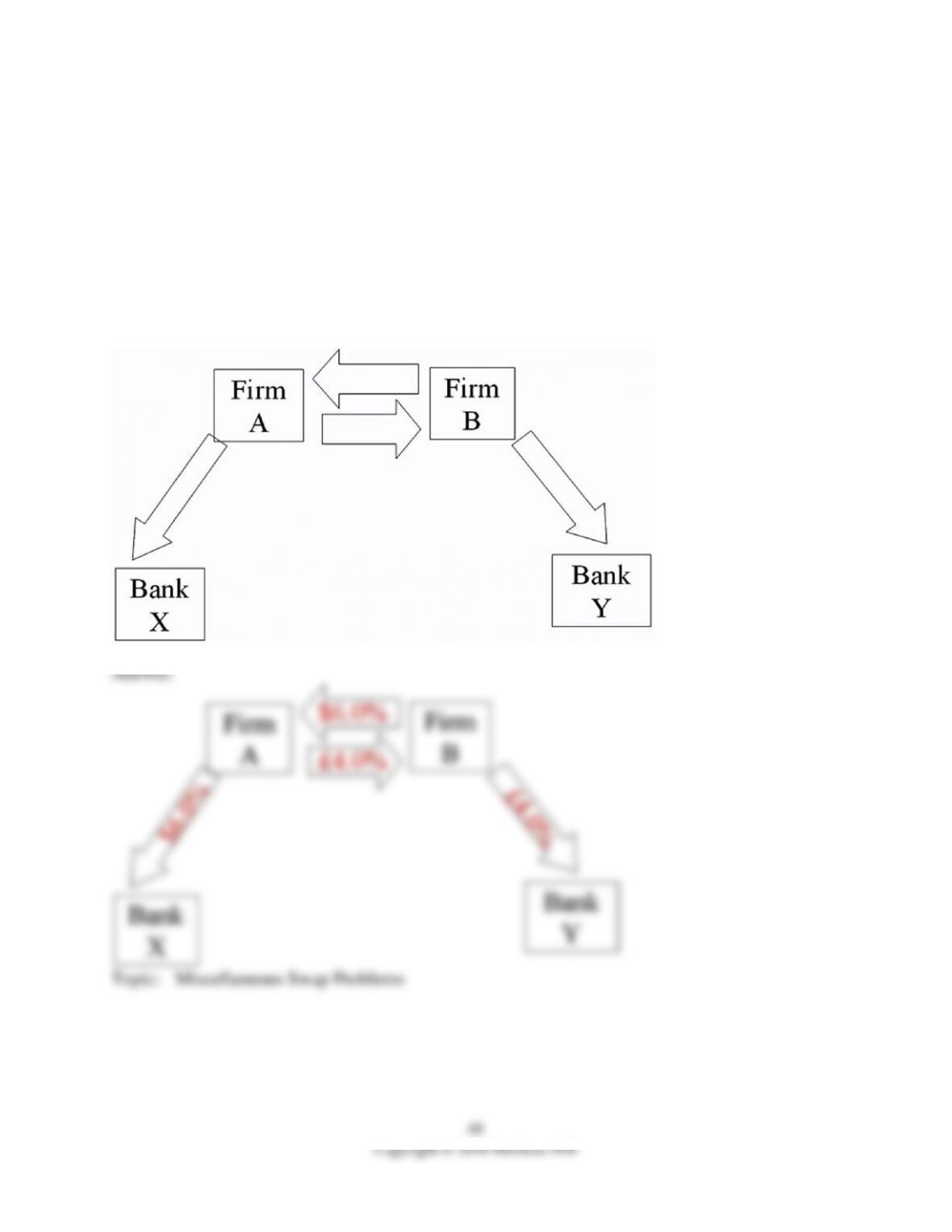

Act as a swap bank and quote bid and ask prices to A and B that are attractive to A and B and

promise to make at least 20bp for your firm.

USD

pounds

Bid

Ask

Bid

Ask

Bid

Ask

Bid

Ask

6

%

6.1

%

4

%

4.1

%

90) Consider the situation of firm A and firm B. The current exchange rate is $2.00/£ Firm A is a

U.S. MNC and wants to borrow £30 million for 2 years. Firm B is a British MNC and wants to

borrow $60 million for 2 years. Their borrowing opportunities are as shown, both firms have AAA

credit ratings.

$

£

A

$

6

%

£

5

%

B

$

7

%

£

4

%

Show how your proposed swap would work for firm A. (e.g., if you were acting as an agent for the

swap bank, try to “sell” firm A on your swap)

91) Consider the borrowing rates for Parties A and B. A wants to finance a $100,000,000 project at

a fixed rate. B wants to finance a $100,000,000 project at a floating rate. Both firms want the same

maturity, 5 years.

Firm

Fixed Rate

Floating

A

$

10.3

%

Prime + 1%

B

$

8.9

%

Prime + 1/2%

Construct a mutually beneficial interest only swap that makes money for A, B, and the swap bank

in equal measure.

92) Consider the borrowing rates for Parties A and B. A wants to finance a $100,000,000 project at

a fixed rate. B wants to finance a $100,000,000 project at a floating rate. Both firms want the same

maturity, 5 years.

Firm

Fixed Rate

Floating

A

$

10.3

%

Prime + 1%

B

$

8.9

%

Prime + 1/2%

For your swap (the one you have shown above) how would the swap bank quote the swap against

prime? (Hint: they are quoting a bid-ask spread against “flat” prime.)

93) An interest-only currency swap has a remaining life of 18 months. It involves exchanging

interest at 14 percent on £20 million for interest at 10 percent on $14 million once a year. The term

structure of interest rates is currently flat in both the U.S. and in the U.K. If the swap were

negotiated today the interest rates exchanged would be $8 percent and £11 percent. All rates were

quoted with annual compounding. The current exchange rate is $1.95 = £1. What is the value of the

swap to the party paying dollars?

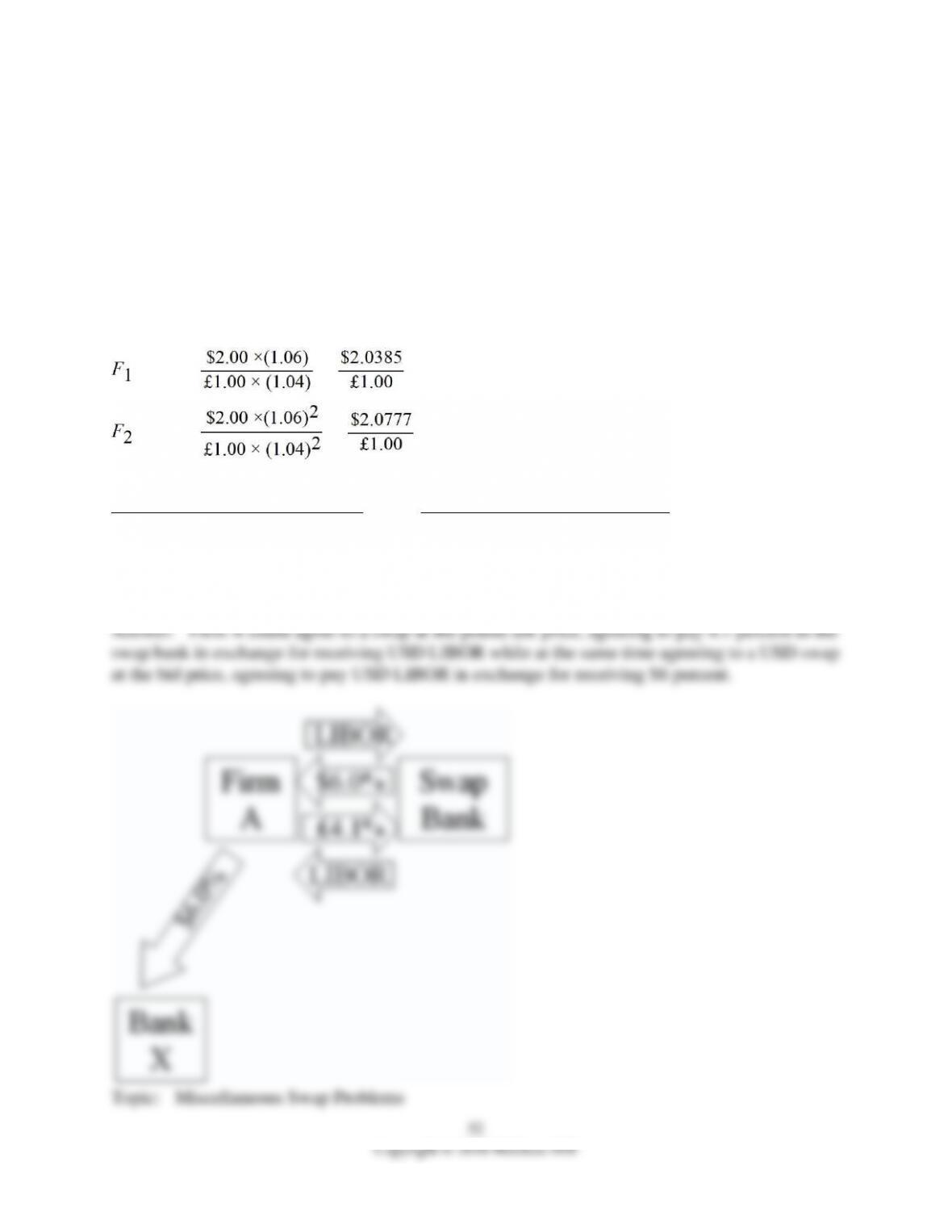

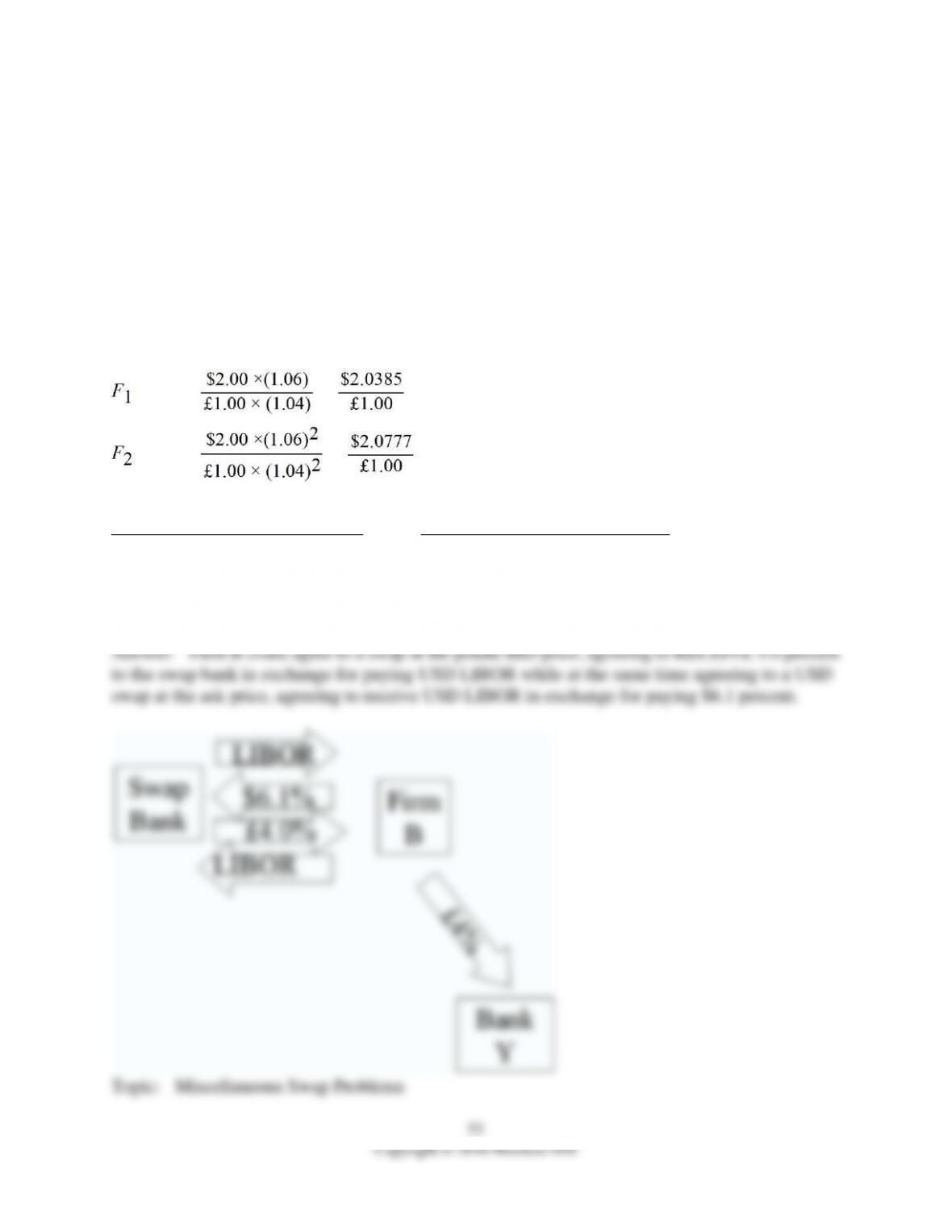

94) Consider the situation of firm A and firm B. The current exchange rate is $2.00/£ Firm A is a

U.S. MNC and wants to borrow £30 million for 2 years. Firm B is a British MNC and wants to

borrow $60 million for 2 years. Their borrowing opportunities are as shown, both firms have AAA

credit ratings.

$

£

A

$

6

%

£

5

%

B

$

7

%

£

4

%

The IRP 1-year and 2-year forward exchange rates are

($ ∣ £) = =

($ ∣ £) = =

USD pounds

Bid

Ask

Bid

Ask

6

%

6.1

%

4

%

4.1

%

Explain how firm A could use two of the swaps offered above to hedge its exchange rate risk.

95) Consider the situation of firm A and firm B. The current exchange rate is $2.00/£ Firm A is a

U.S. MNC and wants to borrow £30 million for 2 years. Firm B is a British MNC and wants to

borrow $60 million for 2 years. Their borrowing opportunities are as shown, both firms have AAA

credit ratings.

$

£

A

$

6

%

£

5

%

B

$

7

%

£

4

%

The IRP 1-year and 2-year forward exchange rates are

($ ∣ £) = =

($ ∣ £) = =

USD pounds

Bid

Ask

Bid

Ask

6

%

6.1

%

4

%

4.1

%

Explain how firm B could use two of the swaps offered above to hedge its exchange rate risk.

96) Consider the situation of firm A and firm B. The current exchange rate is $2.00/£ Firm A is a

U.S. MNC and wants to borrow £30 million for 2 years. Firm B is a British MNC and wants to

borrow $60 million for 2 years. Their borrowing opportunities are as shown, both firms have AAA

credit ratings.

$

£

A

$

6

%

£

5

%

B

$

7

%

£

4

%

The IRP 1-year and 2-year forward exchange rates are

($ ∣ £) = =

($ ∣ £) = =

USD pounds

Bid

Ask

Bid

Ask

6

%

6.1

%

4

%

4.1

%

Explain how firm A could use the forward exchange markets to redenominate a 2-year $60m 6

percent USD loan into a 2-year pound denominated loan.

97) Consider the situation of firm A and firm B. The current exchange rate is $2.00/£ Firm A is a

U.S. MNC and wants to borrow £30 million for 2 years. Firm B is a British MNC and wants to

borrow $60 million for 2 years. Their borrowing opportunities are as shown, both firms have AAA

credit ratings.

$

£

A

$

6

%

£

5

%

B

$

7

%

£

4

%

The IRP 1-year and 2-year forward exchange rates are

($ ∣ £) = =

($ ∣ £) = =

USD pounds

Bid

Ask

Bid

Ask

6

%

6.1

%

4

%

4.1

%

Explain how this opportunity affects which swap firm A will be willing to participate in.

98) Consider the situation of firm A and firm B. The current exchange rate is $2.00/£ Firm A is a

U.S. MNC and wants to borrow £30 million for 2 years. Firm B is a British MNC and wants to

borrow $60 million for 2 years. Their borrowing opportunities are as shown, both firms have AAA

credit ratings.

$

£

A

$

6

%

£

5

%

B

$

7

%

£

4

%

The IRP 1-year and 2-year forward exchange rates are

($ ∣ £) = =

($ ∣ £) = =

USD pounds

Bid

Ask

Bid

Ask

6

%

6.1

%

4

%

4.1

%

Explain how firm B could use the forward exchange markets to redenominate a 2-year £30m 4

percent-pound sterling loan into a 2-year USD-denominated loan.

99) Consider the situation of firm A and firm B. The current exchange rate is $2.00/£ Firm A is a

U.S. MNC and wants to borrow £30 million for 2 years. Firm B is a British MNC and wants to

borrow $60 million for 2 years. Their borrowing opportunities are as shown, both firms have AAA

credit ratings.

$

£

A

$

6

%

£

5

%

B

$

7

%

£

4

%

The IRP 1-year and 2-year forward exchange rates are

($ ∣ £) = =

($ ∣ £) = =

USD pounds

Bid

Ask

Bid

Ask

6

%

6.1

%

4

%

4.1

%

Explain how this opportunity affects which swap firm B will be willing to participate in.

58

100) Consider the situation of firm A and firm B. The current exchange rate is $2.00/£ Firm A is a

U.S. MNC and wants to borrow £30 million for 2 years. Firm B is a British MNC and wants to

borrow $60 million for 2 years. Their borrowing opportunities are as shown, both firms have AAA

credit ratings.

$

£

A

$

6

%

£

5

%

B

$

7

%

£

4

%

The IRP 1-year and 2-year forward exchange rates are

($ ∣ £) = =

($ ∣ £) = =

USD pounds

Bid

Ask

Bid

Ask

6

%

6.1

%

4

%

4.1

%

Devise a direct swap for A and B that has no swap bank. Show their external borrowing. Answer

the problem in the template provided

59

Copyright © 2018 McGraw-Hill

Answer:

Topic: Miscellaneous Swap Problems