32) Company X wants to borrow $10,000,000 floating for 5 years; company Y wants to borrow

£5,000,000 fixed for 5 years. The exchange rate is $2 = £1 and is not expected to change over the

next 5 years. Their external borrowing opportunities are

$ Borrowing

£ Borrowing

Cost

Cost

Company X

$

10

%

£

10.5

%

Company Y

$

12

%

£

13

%

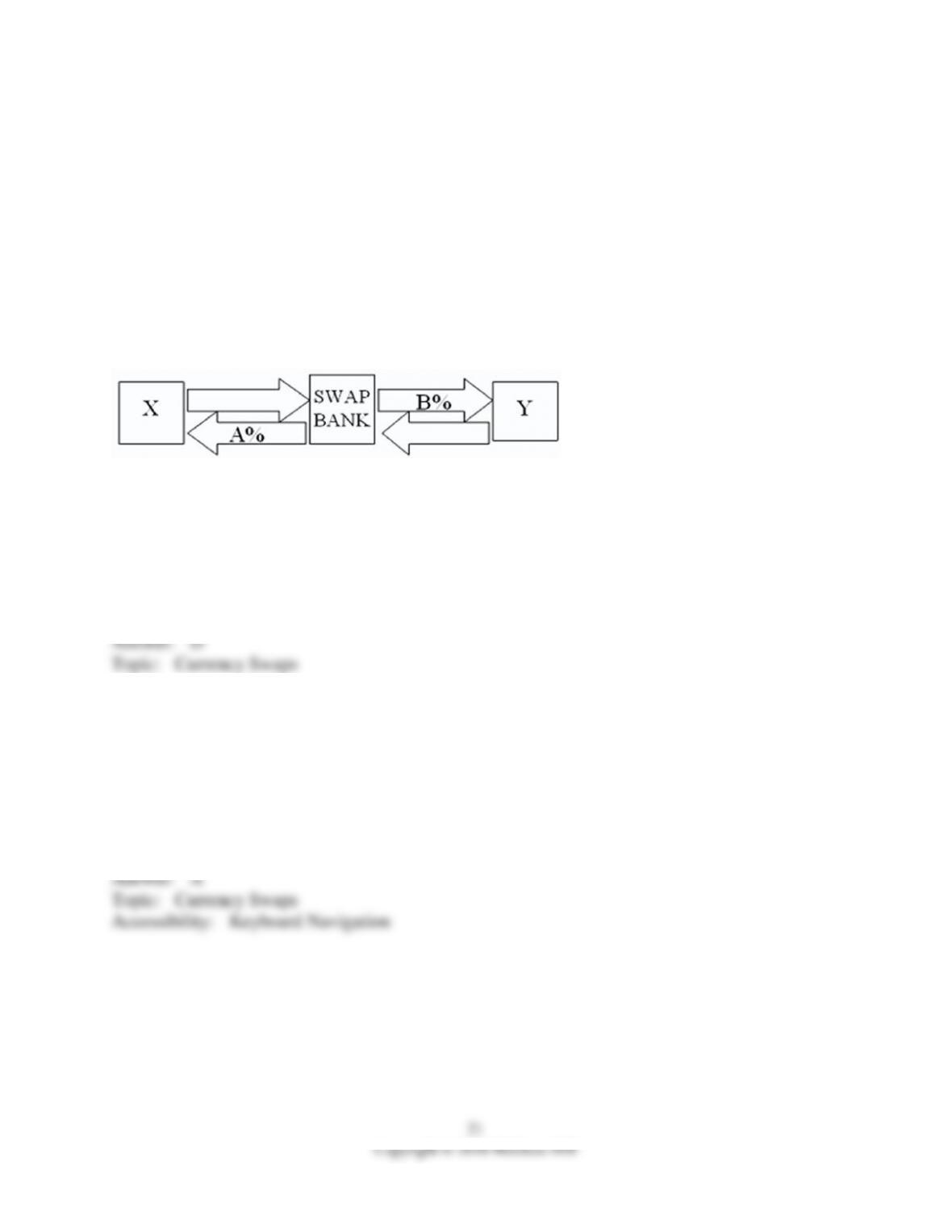

A swap bank wants to design a profitable interest-only fixed-for-fixed currency swap. In order for

X and Y to be interested, they can face no exchange rate risk.

What must the values of A and B in the graph shown above be in order for the swap to be of

interest to firms X and Y?

A) A = $10.50%; B = £12%.

B) A = $10%; B = £13%.

C) A = $12%; B = £13%.

D) A = £10.50%; B = $12%.

33) Pricing a currency swap after inception involves

A) finding the difference between the present values of the payments streams the party will receive

in one currency and pay in the other currency, converted to a common currency.

B) sending a market order to a swap dealer.

C) finding the sum of the present values of the payments streams that each party will receive in one

currency and pay in the other currency, converted to a common currency.

D) none of the options

34) Company X wants to borrow $10,000,000 floating for 1 year; company Y wants to borrow

£5,000,000 fixed for 1 year. The spot exchange rate is $2 = £1 and IRP calculates the one-year

forward rate as $2.00 × (1.08)/£1.00 × (1.06) = $2.0377/£1. Their external borrowing

opportunities are:

$ Borrowing

£ Borrowing

Cost

Cost

Company X

$

8

%

£

7

%

Company Y

$

9

%

£

6

%

A swap bank wants to design a profitable interest-only fixed-for-fixed currency swap. In order for

X and Y to be interested, they can face no exchange rate risk.

What must the values of A and B in the graph shown above be in order for the swap to be of

interest to firms X and Y?

A) A = £7%; B = $9%.

B) A = $8%; B = £6%.

C) A = $7%; B = £7%.

D) A = $8%; B = £8%.

35) Company X wants to borrow $10,000,000 floating for 1 year; company Y wants to borrow

£5,000,000 fixed for 1 year. The spot exchange rate is $2 = £1 and IRP calculates the one-year

forward rate as $2.00 × (1.08)/£1.00 × (1.06) = $2.0377/£1. Their external borrowing

opportunities are:

$ Borrowing

£ Borrowing

Cost

Cost

Company X

$

8

%

£

7

%

Company Y

$

9

%

£

6

%

A swap bank wants to design a profitable interest-only fixed-for-fixed currency swap. In order for

X and Y to be interested, they can face no exchange rate risk.

Company X

A) is probably British.

B) is probably American.

C) has a comparative advantage in borrowing pounds.

D) is probably British, and has a comparative advantage in borrowing pounds.

36) In a currency swap,

A) it may be the case that two counterparties have equivalent credit ratings.

B) it may be the case that firms have a comparative advantage in borrowing in their domestic

markets.

C) it may be the case that two counterparties have equivalent credit ratings, and it may also be the

case that firms have a comparative advantage in borrowing in their domestic markets.

D) none of the options

37) Compute the payments due in the second year on a three-year amortizing swap from company

B to company A. Company A and company B both want to borrow £1,000,000 for three years. A

wants to borrow floating and B wants to borrow fixed. A and B agree to split the QSD.

Fixed-Rate Borrowing

Cost

Floating-Rate Borrowing

Cost

Company A

10

%

LIBOR

Company B

12

%

LIBOR + 1.5

%

A) B pays £402,114.80 to A

B) B pays £100,000 to A

C) B pays £69,788.52 to A

D) none of the options

38) When an interest-only swap is established on an amortizing basis,

A) the debt service exchanges decrease periodically through time as the hypothetical notational

principal is amortized.

B) the debt service exchanges are the same each year, but the level of interest and principal

changes as the loans amortize.

C) there is no such thing as an amortizing interest-only swap.

D) none of the options

39) Floating-for-floating currency swaps

A) have different reference rates for the different currencies: e.g. dollar LIBOR versus euro

LIBOR.

B) do not exist.

C) offer the swap bank a built-in hedge.

D) none of the options

40) Compute the payments due in the first year on a three-year amortizing swap from company B

to company A. Company A and company B both want to borrow £1,000,000 for three years. A

wants to borrow floating and B wants to borrow fixed. A and B agree to split the QSD.

Fixed-Rate Borrowing

Cost

Floating-Rate Borrowing

Cost

Company A

10

%

LIBOR

Company B

12

%

LIBOR + 1.5

%

A) B pays £402,114.80 to A

B) B pays £100,000 to A

C) B pays £69,788.52 to A

D) none of the options

41) In an interest-only currency swap

A) the counterparties must raise the actual notational principal in their home markets; then

exchange it for the foreign currency they desire. They must also hedge with forward contracts on

the currency.

B) the counterparties periodically exchange the amortized portions of the notational principals.

C) the counterparties must raise the actual notational principal in their home markets; then

exchange it for the foreign currency they desire. They must also hedge with forward contracts on

the currency. Additionally, the counterparties periodically exchange the amortized portions of the

notational principals.

D) none of the options

42) Amortizing currency swaps

A) decrease the debt service exchanges periodically through time as the hypothetical notational

principal is amortized.

B) incorporate an amortization feature in which periodically the amortized portions of the

notational principals are re-exchanged.

C) decrease the debt service exchanges periodically through time as the hypothetical notational

principal is amortized. Additionally, amortizing currency swaps incorporate an amortization

feature in which periodically the amortized portions of the notational principals are re-exchanged.

D) none of the options

43) Nominal differences in currency swaps

A) can be explained by the set of international parity relationships.

B) can be explained by the credit risk differentials.

C) can be explained by the quality spread differential.

D) disappear when controlling for volatility.

44) Floating-for-floating currency swaps

A) have reference rates that are different for the different currencies (e.g., dollar LIBOR versus

euro LIBOR).

B) have reference rates that can be the same but have different frequencies.

C) have reference rates that are different for the different currencies (e.g., dollar LIBOR versus

euro LIBOR), and the reference rates can be the same but have different frequencies.

D) none of the options

45) XYZ Corporation enters into a 6-year interest rate swap with a swap bank in which it agrees to

pay the swap bank a fixed-rate of 9 percent annually on a notional amount of SFr10,000,000 and

receive LIBOR −½ percent. As of the third reset date (i.e., midway through the 6-year agreement),

calculate the price of the swap, assuming that the fixed-rate at which XYZ can borrow has

increased to 10 percent.

A) SFr248,685

B) SFr900,000

C) SFr2,700,000

D) SFr7,300,000

46) Which combination of the following represent the risks that a swap dealer confronts.

(i) interest rate risk

(ii) basis risk

(iii) exchange rate risk

(iv) political risk

(v) sovereign risk

A) (i), (ii), (iii), and (v)

B) (i), (iii), and (iv)

C) (iii), (iv), and (iv)

D) (i), (ii), (iii), (iv), and (v)

47) A major risk faced by a swap dealer is credit risk. This is

A) the probability that a counterparty will default.

B) the probability that both counterparties default.

C) the probability floating rates will move against the dealer.

D) none of the options

48) A major that can be eliminated through a swap is exchange rate risk.

A) But only to the extent that a foreign counterparty will not default in a currency swap.

B) But only if the bid-ask spreads are wide.

C) But swaps can be less efficient in this than just trading at the expected spot exchange rates each

year.

D) none of the options

49) A major risk faced by a swap dealer is exchange rate risk. This is

A) the probability that a foreign counterparty will default in a currency swap.

B) the probability that either counterparty defaults in a currency swap.

C) the probability exchange rates will move against the dealer.

D) none of the options

50) A major risk faced by a swap dealer is mismatch risk. This is

A) the probability floating rates and exchange rates will not move together.

B) the difficulty in finding a second counterparty for a swap that the bank has agreed to take with

another party.

C) the probability that both counterparties default.

D) none of the options

51) Some of the risks that a swap dealer confronts are “basis risk” and “sovereign risk.” Select the

definitions that best describe each.

A) “Basis risk” refers to the probability that a country will impose exchange restrictions on a

currency involved in a swap, and “sovereign risk” refers to a situation in which the floating rates of

the two counterparties are not pegged to the same index.

B) “Basis risk” refers to a situation in which the floating rates of the two counterparties are not

pegged to the same index and “sovereign risk” refers to the probability that a country will impose

exchange restrictions on a currency involved in a swap.

C) “Basis risk” refers to interest rate changing unfavorably before the swap bank can lay off to an

opposing counterparty the other side of an interest rate swap entered into with a counter party, and

“sovereign risk” refers to the probability that a country will impose exchange restrictions on a

currency involved in a swap.

D) “Basis risk” refers to the risk of fluctuating exchange rates, and “sovereign risk” refers to a

situation in which the floating rates of the two counterparties are not pegged to the same index.

52) A major risk faced by a swap dealer is sovereign risk. This is

A) the probability that a sovereign counterparty will default.

B) the probability that a country will impose exchange restrictions on a currency involved in an

existing swap.

C) the probability governments will intervene to support an exchange rate.

D) none of the options

53) In an efficient market without barriers to capital flows, the cost-savings argument of the QSD

is difficult to accept, because

A) it implies that an arbitrage opportunity exists because of some mispricing of the default risk

premiums on different types of debt instruments.

B) it implies that an arbitrage opportunity exists because of some mispricing of the exchange rates

on different maturities of forward contracts.

C) it implies that an arbitrage opportunity exists because of some mispricing of the default risk

premiums on different types of debt instruments, and it implies that an arbitrage opportunity exists

because of some mispricing of the exchange rates on different maturities of forward contracts.

D) none of the options

54) When a swap bank serves as a dealer,

A) the swap bank stands willing to accept either side of a swap.

B) the swap bank matches counterparties but does not assume any risk of the swap.

C) the swap bank receives a commission for matching buyers and sellers.

D) none of the options

55) When a swap bank serves as a broker,

A) the swap bank stands willing to accept either side of a swap.

B) the swap bank matches counterparties but does not assume any risk of the swap.

C) the swap bank receives a commission for matching buyers and sellers.

D) none of the options

56) Consider a plain vanilla interest rate swap. Firm A can borrow at 8 percent fixed or can borrow

floating at LIBOR. Firm B is somewhat less creditworthy and can borrow at 10 percent fixed or

can borrow floating at LIBOR + 1 percent. Eun wants to borrow floating and Resnick prefers to

borrow fixed. Both corporations wish to borrow $10 million for 5 years. Which of the following

swaps is mutually beneficial to each party and meets their financing needs?

A) Firm A borrows $10 million externally for 5 years at LIBOR; agrees to swap LIBOR to firm B

for 8 ½ percent fixed for 5 years on a notational principal of $5 million; B borrows $10 million

externally at 10 percent.

B) A borrows $10 million externally for 5 years at LIBOR; agrees to pay 8½ percent to B for

LIBOR fixed for 5 years on a notational principal of $5 million; B borrows $10 million externally

at 10 percent.

C) Since the QSD = 0 there is no mutually beneficial swap.

D) A borrows $10 million externally at 8 percent fixed for 5 years; agrees to swap LIBOR to B for

8½ percent fixed for 5 years on a notational principal of $5 million; B borrows $10 million

externally at LIBOR + 1 percent.

57) Consider fixed-for-fixed currency swap. Firm A is a U.S.-based multinational. Firm B is a

U.K.-based multinational. Firm A wants to finance a £2 million expansion in Great Britain. Firm B

wants to finance a $4 million expansion in the U.S. The spot exchange rate is £1.00 = $2.00. Firm

A can borrow dollars at 10 percent and pounds sterling at 12 percent. Firm B can borrow dollars at

9 percent and pounds sterling at 11 percent. Which of the following swaps is mutually beneficial to

each party and meets their financing needs? Neither party should face exchange rate risk.

A) There is no mutually beneficial swap that has neither party facing exchange rate risk.

B) Firm A should borrow $4 million in dollars, pay 11 percent in pounds to Firm B, who in turn

borrows 2 million pounds and pays 8 percent in dollars to A.

C) Firm A should borrow $2 million in dollars, pay 11 percent in pounds to Firm B, who in turn

borrows 4 million pounds and pays 8 percent in dollars to A.

D) Firm A should borrow $4 million in dollars, pay 11 percent in pounds to Firm B, who in turn

borrows 2 million pounds and pays 10 percent in dollars to A.

58) Consider a bank that has entered into a five-year swap on a notational balance of $10,000,000

with a corporate customer who has agreed to pay a fixed payment of 10 percent in exchange for

LIBOR. As of the fourth reset date, determine the price of the swap from the bank’s point of view

assuming that the fixed-rate side of the swap has increased to 11 percent. LIBOR is at 5 percent.

A) $909,090.91 gain.

B) $90,090.09 loss.

C) No loss or no gain since maturity has not arrived.

D) $90,090.09 gain.

59) Find the all-in-cost of a swap to a party that has agreed to borrow $5 million at 5 percent

externally and pays LIBOR + ½ percent on a notational principal of $5 million in exchange for

fixed rate payments of 6 percent.

A) LIBOR + ½ percent

B) LIBOR

C) LIBOR − ½ percent

D) none of the options

60) Consider a fixed for fixed currency swap. The Dow Corporation is a U.S.-based multinational.

The Jones Corporation is a U.K.-based multinational. Dow wants to finance a £2 million

expansion in Great Britain. Jones wants to finance a $4 million expansion in the U.S. The spot

exchange rate is £1.00 = $2.00. Dow can borrow dollars at $10 percent and pounds sterling at 12

percent. Jones can borrow dollars at 9 percent and pounds sterling at 10 percent. Assuming that the

swap bank is willing to take on exchange rate risk, but the other counterparties are not, which of

the following swaps is mutually beneficial to each party and meets their financing needs?

A) Dow should borrow $4 million in dollars externally at $10 percent; pay £11¾ percent in pounds

to the swap bank on a notational principal of £2 million; receive $10 percent from the swap bank

on a notational principal of $4 million. Jones, borrows £2 million pounds externally at £10 percent;

pays $8¾ percent to the swap bank on a notational principal of $4 million and receives £10 percent

in pounds from the swap bank on a notational principal of £2 million.

B) Dow should borrow $4 million in dollars externally at $10 percent; pay £11½ percent in pounds

to the swap bank on a notational principal of £2 million; receive $10 percent from the swap bank

on a notational principal of $4 million. Jones, borrows £2 million pounds externally at £10 percent;

pays $8½ percent to the swap bank on a notational principal of $4 million and receives £10 percent

in pounds from the swap bank on a notational principal of £2 million.

C) Dow should borrow $4 million in dollars externally at $10 percent; pay £11 percent in pounds

to the swap bank on a notational principal of £2 million; receive $8 percent from the swap bank on

a notational principal of $4 million. Jones, borrows £2 million pounds externally at £10 percent;

pays $10 percent to the swap bank on a notational principal of $4 million and receives £11 percent

in pounds from the swap bank on a notational principal of £2 million.

D) There is no swap that is possible.

61) With regard to a swap bank acting as a dealer in swap transactions, interest rate risk refers to

A) the risk that arises from the situation in which the floating-rates of the two counterparties are

not pegged to the same index.

B) the risk that interest rates changing unfavorably before the swap bank can lay off to an opposing

counterparty on the other side of an interest rate swap entered into with the first counterparty.

C) the risk the swap bank faces from fluctuating exchange rates during the time it takes for the

bank to lay off a swap it undertakes with one counterparty with an opposing transaction.

D) the risk that a counterparty will default.

62) With regard to a swap bank acting as a dealer in swap transactions, mismatch risk refers to

A) the risk that arises from the situation in which the floating-rates of the two counterparties are

not pegged to the same index.

B) the risk that interest rates changing unfavorably before the swap bank can lay off to an opposing

counterparty on the other side of an interest rate swap entered into with the first counterparty.

C) the risk the swap bank faces from fluctuating exchange rates during the time it takes for the

bank to lay off a swap it undertakes with one counterparty with an opposing transaction.

D) the risk that it may be difficult or impossible to find an exact opposite match for a swap the bank

has agreed take.

63) You are the debt manager for a U.S.-based multinational. You need to borrow €100,000,000

for five years. You can either borrow the €100,000,000 directly in Germany or borrow dollars in

the U.S. and enter into a combined interest rate and currency swap with a swap bank. One risk that

you face by using the swap that you do not face by borrowing euros directly is

A) exchange rate risk.

B) sovereign risk.

C) credit risk.

D) interest rate risk.

64) Suppose that you are a swap bank and you notice that interest rates on zero coupon bonds are

as shown. Develop the 3-year bid price of a euro swap quoted against flat USD LIBOR.

Zero Rates

1-year

2-year

3-year

USD

$

3

%

$

4

%

$

5

%

Euro

€

2

%

€

3

%

€

4

%

In other words, what will you be willing to pay in euro against receiving USD LIBOR?

A) 5 percent

B) 4 percent

C) 3 percent

D) 2 percent

65) Suppose that you are a swap bank and you notice that interest rates on zero coupon bonds are

as shown. Develop the 3-year bid price of a dollar swap quoted against flat USD LIBOR.

Zero Rates

1-year

2-year

3-year

USD

$

3

%

$

4

%

$

5

%

Euro

€

2

%

€

3

%

€

4

%

In other words, what will you be willing to pay in euro against receiving USD LIBOR?

A) 5 percent

B) 4 percent

C) 3 percent

D) 2 percent

66) Suppose that you are a swap bank and you notice that interest rates on coupon bonds are as

shown. Develop the 3-year bid price of a euro swap quoted against flat USD LIBOR. The current

spot exchange rate is $1.50 per €1.00. The size of the swap is €40 million versus $60 million.

Rates

3-year

USD

$

7

%

Euro

€

5

%

In other words, what will you be willing to pay in euro against receiving USD LIBOR?

A) 7 percent

B) 6 percent

C) 5 percent

D) none of the options

67) Come up with a swap (exchange of interest and principal) for parties A and B who have the

following borrowing opportunities.

€

$

A

€5%

$LIBOR%

B

€6%

$LIBOR + ½%

The current exchange rate is $1.60 = €1.00. Company “A” is in Milan, Italy and wishes to borrow

$1,000,000 at a floating rate for 5 years and company “B” is a U.S. firm that wants to borrow

€625,000 for 5 years at a fixed rate of interest. You are a swap dealer. Quote A and B a swap that

makes money for all parties and eliminates exchange rate risk for both A and B.

68) Suppose that the swap that you proposed is now 4 years old (i.e., there is exactly one year to go

on the swap). The fourth payment has already been made. If the spot exchange rate prevailing in

year 4 is $1.8778 = €1 and the 1–year forward exchange rate prevailing in year 4 is $1.95 = €1,

what is the value of the swap to the party paying dollars? If the swap were initiated today the

correct rates would be as shown.

37

Copyright © 2018 McGraw-Hill

69) Come up with a swap (principal + interest) for two parties A and B who have the following

borrowing opportunities.

€

$

A

€LIBOR%

$

8

%

B

€LIBOR + ½%

$

8.20

%

The current exchange rate is $1.60 = €1.00. Company “A” wishes to borrow $1,000,000 for 5 years

and “B” wants to borrow €625,000 for 5 years. You are a swap dealer. Quote A and B a swap that

makes money for all parties and eliminates exchange rate risk for both A and B. Firms A and B are

more concerned with what currency that they borrow in than whether the debt is fixed or floating.

Answer:

Topic: Miscellaneous Swap Problems

70) Suppose that the swap that you proposed is now 4 years old (i.e., there is exactly one year to go

on the swap). If the spot exchange rate prevailing in year 4 is $1.8778 = €1 and the 1-year forward

exchange rate prevailing in year 4 is $1.95 = €1, what is the value of the swap to the party paying

dollars? If the swap were initiated today the correct rates would be as shown.

€

$

A

€LIBOR%

$

7.9

%

B

€LIBOR + ¾%

$

8.50

%

71) Consider the situation of firm A and firm B. The current exchange rate is $1.50/€. Firm A is a

U.S. MNC and wants to borrow €40 million for 2 years. Firm B is a French MNC and wants to

borrow $60 million for 2 years. Their borrowing opportunities are as shown; both firms have AAA

credit ratings.

$

€

A

$

7

%

€

6

%

B

$

8

%

€

5

%

What are the IRP 1-year and 2-year forward exchange rates?

72) Consider the situation of firm A and firm B. The current exchange rate is $1.50/€. Firm A is a

U.S. MNC and wants to borrow €40 million for 2 years. Firm B is a French MNC and wants to

borrow $60 million for 2 years. Their borrowing opportunities are as shown; both firms have AAA

credit ratings.

$

€

A

$

7

%

€

6

%

B

$

8

%

€

5

%

Explain how firm A could use the forward exchange markets to redenominate a 2-year $60m 7

percent USD loan into a 2-year euro denominated loan.

73) Consider the situation of firm A and firm B. The current exchange rate is $1.50/€. Firm A is a

U.S. MNC and wants to borrow €40 million for 2 years. Firm B is a French MNC and wants to

borrow $60 million for 2 years. Their borrowing opportunities are as shown; both firms have AAA

credit ratings.

$

€

A

$

7

%

€

6

%

B

$

8

%

€

5

%

If firm A could use the forward exchange markets to redenominate a 2-year $60m 7 percent USD

loan into a 2-year euro denominated loan, what would be the interest rate?

74) Consider the situation of firm A and firm B. The current exchange rate is $1.50/€. Firm A is a

U.S. MNC and wants to borrow €40 million for 2 years. Firm B is a French MNC and wants to

borrow $60 million for 2 years. Their borrowing opportunities are as shown; both firms have AAA

credit ratings.

$

€

A

$

7

%

€

6

%

B

$

8

%

€

5

%

Explain how this opportunity affects which swap firm A will be willing to participate in.

75) Consider the situation of firm A and firm B. The current exchange rate is $1.50/€. Firm A is a

U.S. MNC and wants to borrow €40 million for 2 years. Firm B is a French MNC and wants to

borrow $60 million for 2 years. Their borrowing opportunities are as shown; both firms have AAA

credit ratings.

$

€

A

$

7

%

€

6

%

B

$

8

%

€

5

%

Explain how firm B could use the forward exchange markets to redenominate a 2-year €40m 5

percent euro loan into a 2-year USD-denominated loan.