International Financial Management, 8e (Eun)

1) The term interest rate swap

A) refers to a “single-currency interest rate swap” shortened to “interest rate swap.”

B) involves “counterparties” who make a contractual agreement to exchange cash flows at periodic

intervals.

C) can be “fixed-for-floating rate” or “fixed-for-fixed rate.”

D) all of the options

2) Examples of “single-currency interest rate swap” and “cross-currency interest rate swap” are:

A) fixed-for-floating rate interest rate swap, where one counterparty exchanges the interest

payments of a floating-rate debt obligations for fixed-rate interest payments of the other counter

party.

B) fixed-for-fixed rate debt service (currency swap), where one counterparty exchanges the debt

service obligations of a bond denominated in one currency for the debt service obligations of the

other counterparty denominated in another currency.

C) fixed-for-floating rate interest rate swap, where one counterparty exchanges the interest

payments of a floating-rate debt obligations for fixed-rate interest payments of the other counter

party, as well as fixed-for-fixed rate debt service (currency swap), where one counterparty

exchanges the debt service obligations of a bond denominated in one currency for the debt service

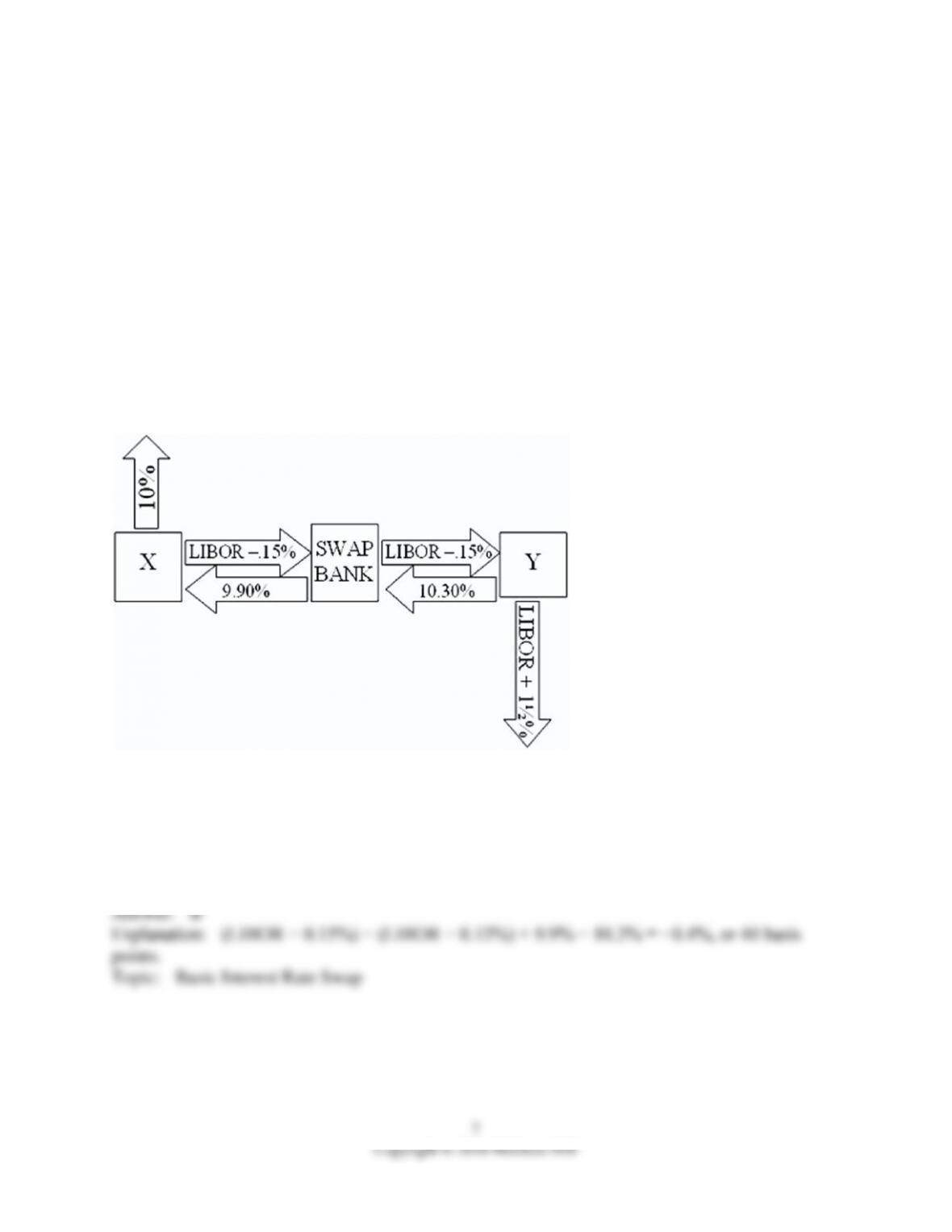

obligations of the other counterparty denominated in another currency.

D) none of the options

3) The primary reasons for a counterparty to use a currency swap are

A) to hedge and to speculate.

B) to play in the futures and forward markets.

C) to obtain debt financing in the swapped currency at an interest cost reduction brought about

through comparative advantages each counterparty has in its national capital market, and the

benefit of hedging long-run exchange rate exposure.

D) to hedge and to speculate, as well as to play in the futures and forward markets.

4) The size of the swap market (as of mid-year 2015) is

A) measured by notational principal.

B) over 23 trillion dollars.

C) measured by notational principal and over 23 trillion dollars.

D) none of the options

5) Which combination of the following statements is true about a swap bank?

(i) it is a generic term to describe a financial institution that facilitates swaps between

counterparties

(ii) it can be an international commercial bank

(iii) it can be an investment bank

(iv) it can be a merchant bank

(v) it can be an independent operator

A) (i) and (ii)

B) (i), (ii) and (iii)

C) (i), (ii), (iii) and (iv)

D) (i), (ii), (iii), (iv) and (v)

6) A swap bank

A) can act as a broker, bringing together counterparties to a swap.

B) can act as a dealer, standing ready to buy and sell swaps.

C) can act as a broker, bringing together counterparties to a swap and standing ready to buy and

sell swaps.

D) only sometimes acts as a broker, bringing together counterparties to a swap, but never ever acts

as a dealer, standing ready to buy and sell swaps.

7) In the swap market, which position potentially carries greater risks, broker or dealer?

A) Broker

B) Dealer

C) They are the same swaps, therefore the same risks.

D) none of the options

8) Suppose the quote for a five-year swap with semiannual payments is 8.50–8.60 percent. This

means

A) the swap bank will pay semiannual fixed-rate dollar payments of 8.50 percent against receiving

six-month dollar LIBOR.

B) the swap bank will receive semiannual fixed-rate dollar payments of 8.60 percent against

paying six-month dollar LIBOR.

C) the swap bank will pay semiannual fixed-rate dollar payments of 8.50 percent against receiving

six-month dollar LIBOR, and the swap bank will receive semiannual fixed-rate dollar payments of

8.60 percent against paying six-month dollar LIBOR.

D) none of the options

9) Suppose the quote for a five-year swap with semiannual payments is 8.50–8.60 percent. This

means

A) the swap bank will pay semiannual fixed-rate dollar payments of 8.60 percent against receiving

six-month dollar LIBOR

B) the swap bank will receive semiannual fixed-rate dollar payments of 8.50 percent against

paying six-month dollar LIBOR.

C) if the swap bank is successful in getting counterparties to both legs of the swap at these prices,

he will have an annual profit of ten basis points.

D) none of the options

10) A swap bank makes the following quotes for 5-year swaps and AAA-rated firms:

USD Euro

Bid

Ask

Bid

Ask

5

%

5.2

%

7

%

7.2

%

A) The bank stands ready to pay $5.2 percent against receiving dollar LIBOR on 5-year loans.

B) The bank stands ready to receive €7 percent against receiving dollar LIBOR on 5-year loans.

C) The bank stands ready to pay €7 percent against receiving dollar LIBOR on 5-year loans.

D) none of the options

11) Suppose the quote for a five-year swap with semiannual payments is 8.50−8.60 percent in

dollars and 6.60−6.80 percent in euro against six-month dollar LIBOR. This means

A) the swap bank will enter into a currency swap in which it would pay semiannual fixed-rate

dollar payments of 8.50 percent against receiving semiannual fixed-rate euro payments of 6.80.

B) the swap bank will enter into a currency swap in which it would pay semiannual fixed-rate euro

payments of 6.60 percent against receiving semiannual fixed-rate dollar payments of 8.60.

C) the swap bank will enter into a currency swap in which it would pay semiannual fixed-rate

dollar payments of 8.50 percent against receiving semiannual fixed-rate euro payments of 6.80,

and the swap bank will enter into a currency swap in which it would pay semiannual fixed-rate

euro payments of 6.60 percent against receiving semiannual fixed-rate dollar payments of 8.60.

D) none of the options

12) An interest-only single currency interest rate swap

A) is also known as a plain vanilla swap.

B) is also known as an interest rate swap.

C) is about as simple as swaps can get.

D) all of the options

13) Company X and company Y have mirror-image financing needs (they both want to borrow

equivalent amounts for the same amount of time. Company X has a AAA credit rating, but

company Y’s credit standing is considerably lower.

A) Company X should demand most of the QSD in any swap with Y as compensation for default

risk.

B) Since Y has a poor credit rating, it would not be a participant in the swap market.

C) Company X should more readily agree to a swap involving Y if there is also a swap bank

providing credit risk intermediation.

D) Company X should demand most of the QSD in any swap with Y as compensation for default

risk, and Company X should more readily agree to a swap involving Y if there is also a swap bank

providing credit risk intermediation.

14) A swap bank has identified two companies with mirror-image financing needs (they both want

to borrow equivalent amounts for the same amount of time. Company X has agreed to one leg of

the swap but company Y is “playing hard to get.”

A) If the swap bank has already contracted one leg of the swap, they should be anxious to offer

better terms to company Y to just get the deal done.

B) The swap bank could just sell the company X side of the swap.

C) Company X should lobby Y to “get on board.”

D) If the swap bank has already contracted one leg of the swap, they should be anxious to offer

better terms to company Y to just get the deal done, and the swap bank could just sell the company

X side of the swap.

15) A swap bank has identified two companies with mirror-image financing needs—they both

want to borrow equivalent amounts for the same amount of time. Company X has agreed to one leg

of the swap but company Y is “playing hard to get.”

A) The swap bank could just sell the company X side of the swap.

B) Company X should lobby Y to “get on board.”

C) Company Y should calculate the QSD and subtract that from their best outside offer.

D) none of the options

16) Company X wants to borrow $10,000,000 floating for 5 years; company Y wants to borrow

$10,000,000 fixed for 5 years. Their external borrowing opportunities are shown here:

Fixed-Rate

Floating-Rate

Borrowing Cost

Borrowing Cost

Company X

10%

LIBOR

Company Y

12%

LIBOR + 1.5%

A swap bank proposes the following interest only swap:

X will pay the swap bank annual payments on $10,000,000 with the coupon rate of LIBOR − 0.15

percent; in exchange the swap bank will pay to company X interest payments on $10,000,000 at a

fixed rate of 9.90 percent. What is the value of this swap to company X?

A) Company X will lose money on the deal.

B) Company X will save 25 basis points per year on $10,000,000 = $25,000 per year.

C) Company X will only break even on the deal.

D) Company X will save 5 basis points per year on $10,000,000 = $5,000 per year.

17) Company X wants to borrow $10,000,000 floating for 5 years; company Y wants to borrow

$10,000,000 fixed for 5 years. Their external borrowing opportunities are shown here:

Fixed-Rate

Floating-Rate

Borrowing Cost

Borrowing Cost

Company X

10%

LIBOR

Company Y

12%

LIBOR + 1.5%

A swap bank proposes the following interest only swap:

Y will pay the swap bank annual payments on $10,000,000 with a fixed rate of rate of 9.90 percent.

In exchange the swap bank will pay to company Y interest payments on $10,000,000 at LIBOR −

0.15 percent; What is the value of this swap to company Y?

A) Company Y will save 15 basis points per year on $10,000,000 = $15,000 per year.

B) Company Y will save 45 basis points per year on $10,000,000 = $45,000 per year.

C) Company Y will save 5 basis points per year on $10,000,000 = $5,000 per year.

D) Company Y will only break even on the deal.

18) Company X wants to borrow $10,000,000 floating for 5 years; company Y wants to borrow

$10,000,000 fixed for 5 years. Their external borrowing opportunities are shown here:

Fixed-Rate

Floating-Rate

Borrowing Cost

Borrowing Cost

Company X

10%

LIBOR

Company Y

12%

LIBOR + 1.5%

A swap bank proposes the following interest only swap:

X will pay the swap bank annual payments on $10,000,000 with the coupon rate of LIBOR − 0.15

percent; in exchange the swap bank will pay to company X interest payments on $10,000,000 at a

fixed rate of 9.90 percent. Y will pay the swap bank interest payments on $10,000,000 at a fixed

rate of 10.30 percent and the swap bank will pay Y annual payments on $10,000,000 with the

coupon rate of LIBOR − 0.15 percent.

What is the value of this swap to the swap bank?

A) The swap bank will lose money on the deal.

B) The swap bank will earn 40 basis points per year on $10,000,000 = $40,000 per year.

C) The swap bank will break even.

D) none of the options

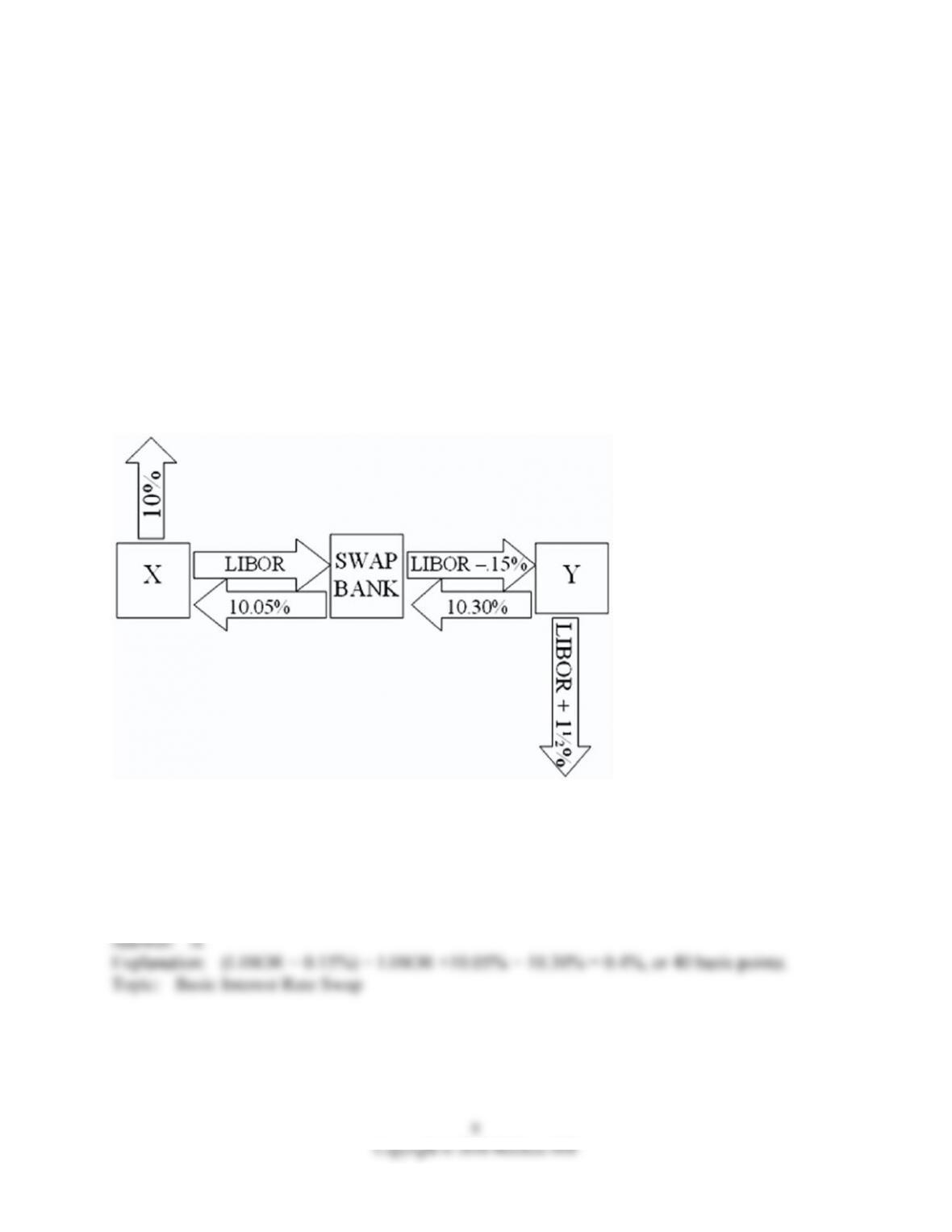

19) Company X wants to borrow $10,000,000 floating for 5 years; company Y wants to borrow

$10,000,000 fixed for 5 years. Their external borrowing opportunities are shown here:

Fixed-Rate

Floating-Rate

Borrowing Cost

Borrowing Cost

Company X

10%

LIBOR

Company Y

12%

LIBOR + 1.5%

A swap bank proposes the following interest only swap:

X will pay the swap bank annual payments on $10,000,000 with the coupon rate of LIBOR; in

exchange the swap bank will pay to company X interest payments on $10,000,000 at a fixed rate of

10.05 percent. Y will pay the swap bank interest payments on $10,000,000 at a fixed rate of 10.30

percent and the swap bank will pay Y annual payments on $10,000,000 with the coupon rate of

LIBOR − 0.15 percent.

What is the value of this swap to the swap bank?

A) The swap bank will earn 40 basis points per year on $10,000,000 = $40,000 per year.

B) The swap bank will earn 10 basis points per year on $10,000,000 = $10,000 per year.

C) The swap bank will lose money.

D) none of the options

9

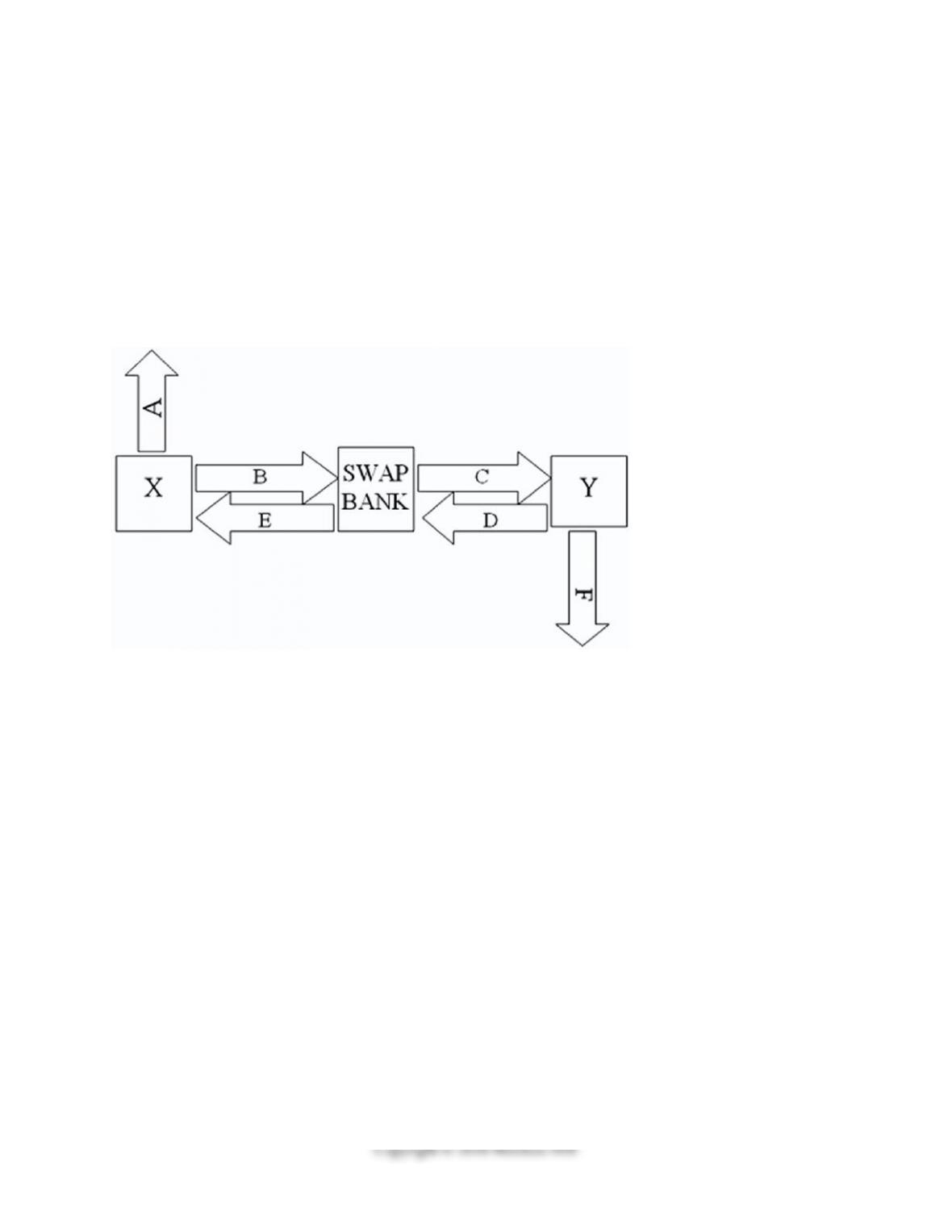

20) Company X wants to borrow $10,000,000 floating for 5 years; company Y wants to borrow

$10,000,000 fixed for 5 years. Their external borrowing opportunities are shown here:

Fixed-Rate

Floating-Rate

Borrowing Cost

Borrowing Cost

Company X

10%

LIBOR

Company Y

12%

LIBOR + 1.5%

A swap bank is involved and quotes the following rates five-year dollar interest rate swaps at 10.05

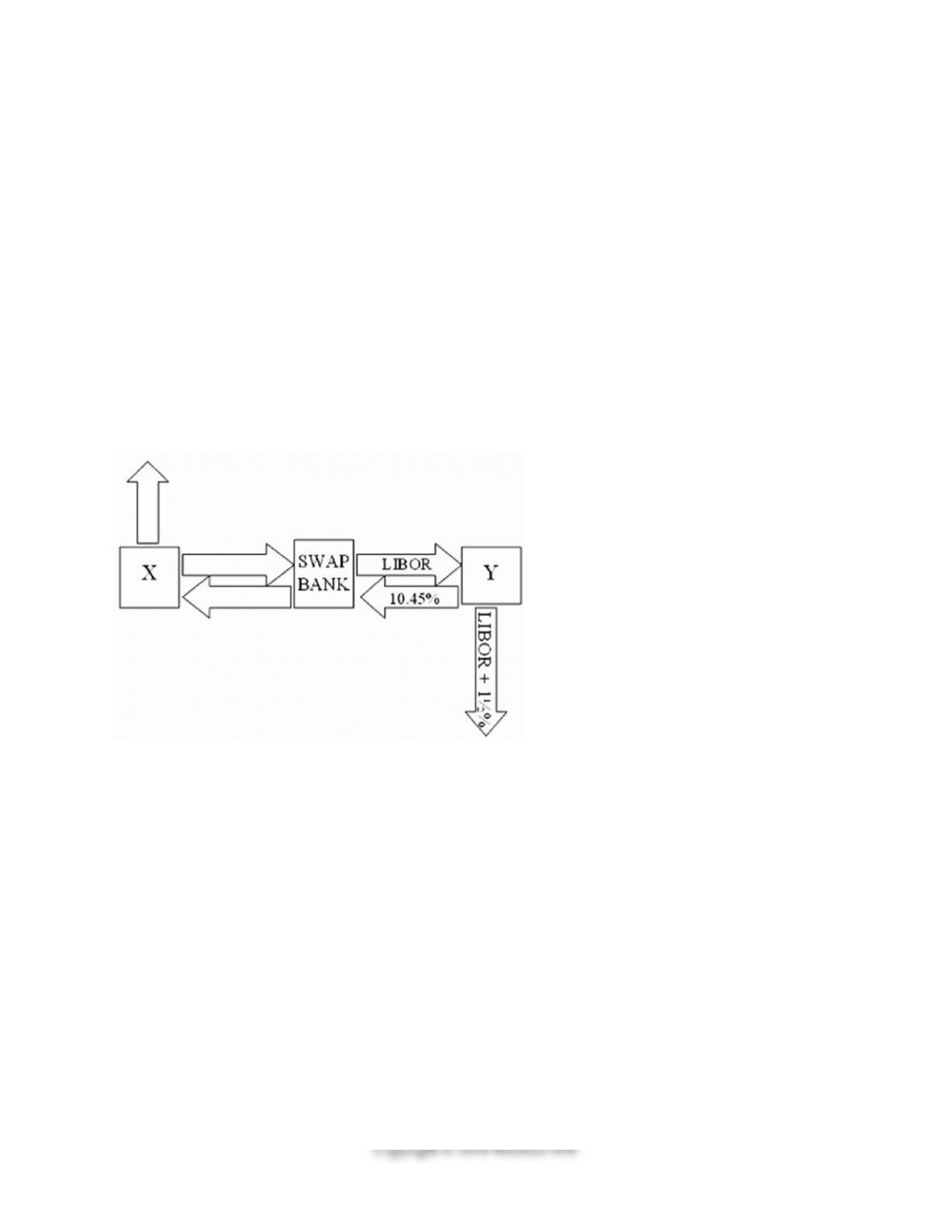

percent−10.45 percent against LIBOR flat.

Assume both X and Y agree to the swap bank’s terms. Fill in the values for A, B, C, D, E, & F on

the diagram.

A) A = LIBOR; B = 10.45%; C = 10.05%; D = LIBOR; E = LIBOR; F = 12%

B) A = 10%; B = 10.45%; C = 10.05%; D = LIBOR; E = LIBOR; F = LIBOR + 1½%

C) A = 10%; B = 10.45%; C = LIBOR; D = LIBOR; E = 10.05%; F = LIBOR + 1½%

D) A = 10%; B = LIBOR; C = LIBOR; D = 10.45%; E = 10.05%; F = LIBOR + 1½%

10

Copyright © 2018 McGraw-Hill

Answer: D

Explanation:

Topic: Basic Interest Rate Swap

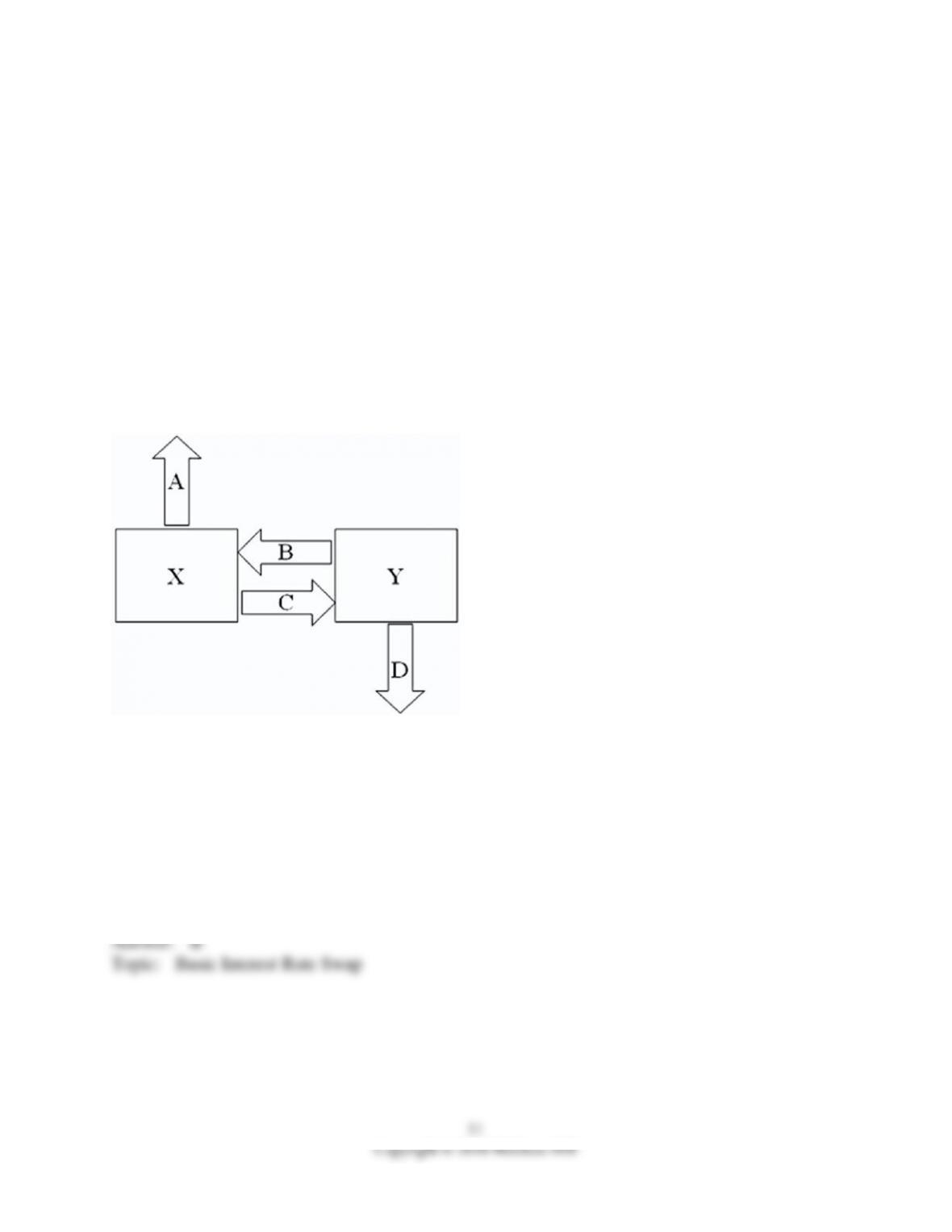

21) Company X wants to borrow $10,000,000 floating for 5 years; company Y wants to borrow

$10,000,000 fixed for 5 years. Their external borrowing opportunities are shown here:

Fixed-Rate

Floating-Rate

Borrowing Cost

Borrowing Cost

Company X

10%

LIBOR

Company Y

12%

LIBOR + 1.5%

Design a mutually beneficial interest only swap for X and Y with a notational principal of $10

million by having appropriate values for;

A = Company X’s external borrowing rate

B = Company Y’s payment to X (rate)

C = Company X’s payment to Y (rate)

D = Company Y’s external borrowing rate

a) A = 10%; B = 11.75%; C = LIBOR – .25%; D = LIBOR + 1.5%

b) A = 10%; B = 10%; C = LIBOR – .25%; D = LIBOR + 1.5%

c) A = LIBOR; B = 10%; C = LIBOR – .25%; D = 12%

d) A = LIBOR; B = LIBOR; C = LIBOR – .25%; D = 12%

A) Option a

B) Option b

C) Option c

D) Option d

22) Suppose ABC Investment Banker Ltd., is quoting swap rates as follows: 7.50 − 7.85 annually

against six-month dollar LIBOR for dollars, and 11.00 percent−11.30 percent annually against

six-month dollar LIBOR for British pound sterling. ABC would enter into a $/£ currency swap in

which:

A) it would pay annual fixed-rate dollar payments of 7.5 percent in return for receiving annual

fixed-rate £ payments at 11.3 percent.

B) it will receive annual fixed-rate dollar payments at 7.85 percent against paying annual

fixed-rate £ payments at 11 percent.

C) it would pay annual fixed-rate dollar payments of 7.5 percent in return for receiving annual

fixed-rate £ payments at 11.3 percent, and it will receive annual fixed-rate dollar payments at 7.85

percent against paying annual fixed-rate £ payments at 11 percent.

D) none of the options

23) Use the following information to calculate the quality spread differential (QSD).

Fixed-Rate Borrowing

Cost

Floating-Rate Borrowing

Cost

Company X

10

%

LIBOR

Company Y

12

%

LIBOR + 1.5

%

A) 0.50 percent

B) 1.00 percent

C) 1.50 percent

D) 2.00 percent

13

24) Company X wants to borrow $10,000,000 floating for 5 years; company Y wants to borrow

$10,000,000 fixed for 5 years. Their external borrowing opportunities are shown below.

Fixed-Rate Borrowing

Cost

Floating-Rate Borrowing

Cost

Company X

10

%

LIBOR

Company Y

12

%

LIBOR + 1.5

%

A swap bank is involved and quotes the following rates five-year dollar interest rate swaps at 10.05

percent –10.45 percent against LIBOR flat.

Assume company Y has agreed, but company X will only agree to the swap if the bank offers

better terms.

What are the absolute best terms the bank can offer X, given that it already booked Y?

A) 10.45% −10.45% against LIBOR flat.

B) 10.45%−10.05% against LIBOR flat.

C) 10.50%−10.50% against LIBOR flat.

D) none of the options

14

Copyright © 2018 McGraw-Hill

Answer: A

Explanation:

Topic: Basic Interest Rate Swap

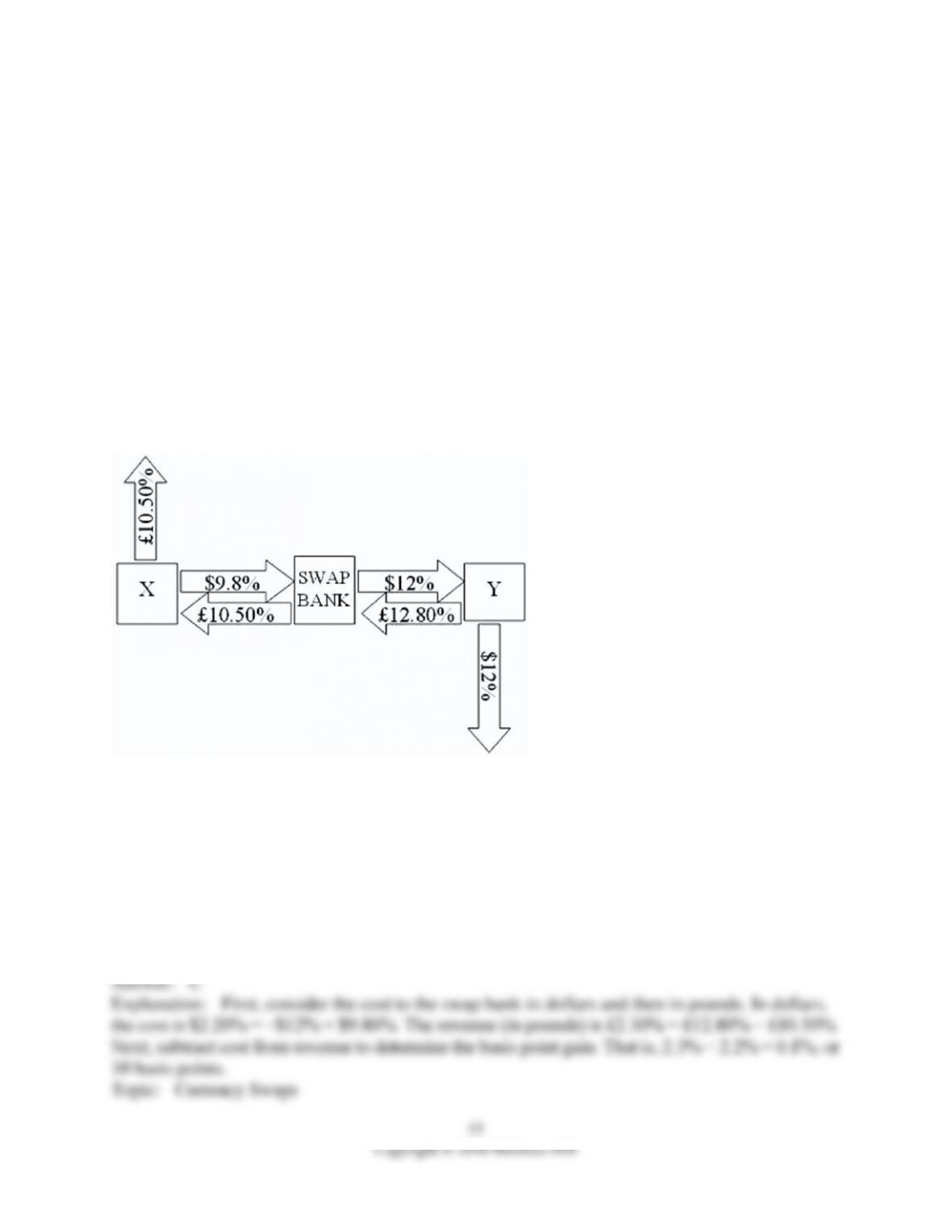

25) Company X wants to borrow $10,000,000 for 5 years; company Y wants to borrow £5,000,000

for 5 years. The exchange rate is $2 = £1 and is not expected to change over the next 5 years. Their

external borrowing opportunities are shown here:

$ Borrowing

£ Borrowing

Cost

Cost

Company X

$

10

%

£

10.5

%

Company Y

$

12

%

£

13

%

A swap bank proposes the following interest only swap:

X will pay the swap bank annual payments on $10,000,000 with the coupon rate of 9.80 percent; in

exchange the swap bank will pay to company X interest payments on £5,000,000 at a fixed rate of

10.5 percent. Y will pay the swap bank interest payments on £5,000,000 at a fixed rate of 12.80

percent and the swap bank will pay Y annual payments on $10,000,000 with the coupon rate of 12

percent.

What is the value of this swap to the swap bank?

A) The swap bank will earn 10 basis points per year; the only risk is default risk.

B) The swap bank will earn 10 basis points per year but has exchange rate risk: dollar-denominated

income and pound-denominated costs and default risk.

C) The swap bank will earn 10 basis points per year but has exchange rate risk:

pound-denominated income and dollar-denominated costs and default risk.

D) The swap bank will earn 20 basis points per year in dollars but has exchange rate risk:

pound-denominated income and dollar-denominated costs and default risk.

26) Swaps are said to offer market completeness.

A) This means that all types of debt instruments are not regularly available for all borrowers. Thus

interest rate swap markets assist in tailoring financing to the type desired by a particular borrower.

B) In that the swap market offers price discovery to the market

C) Because you can trade across both currencies and fixed and floating market segments

D) none of the options

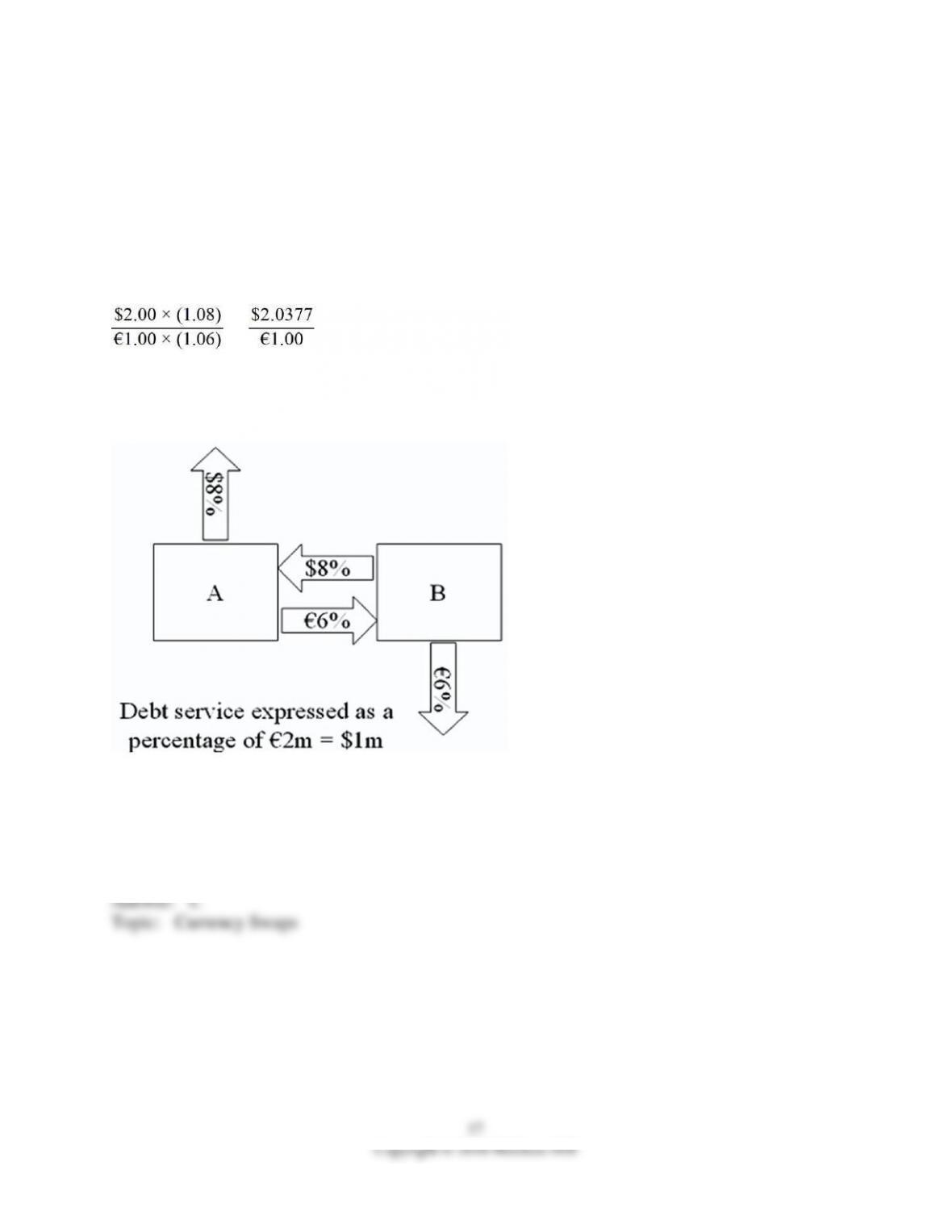

27) Consider the dollar- and euro-based borrowing opportunities of companies A and B.

€ borrowing

$ borrowing

A

€

7

%

$

8

%

B

€

6

%

$

9

%

A is a U.S.-based MNC with AAA credit; B is an Italian firm with AAA credit. Firm A wants to

borrow €1,000,000 for one year and B wants to borrow $2,000,000 for one year. The spot

exchange rate is $2.00 = €1.00 and the one-year forward rate is given by IRP as

= .

Suppose they agree to the swap shown here. Is this mutually beneficial swap equally fair to both

parties?

A) Yes, QSD = [€7% − €6% × $2.00/€1.00] − ($8% − $9%) = $2% + $1% = $3%.

B) No, company A borrows at 6 percent in euro but company B borrows at 8 percent in dollars.

C) Yes, A will be better off by €1 percent on €1m; B by 1 percent on $2m and $2.00 = €1.00.

D) No, company A saves 1 percent in euro but company B saves only 1 percent in dollars when the

spot exchange rate is $2.00 = €1.00—A is twice as better off as B.

28) A is a U.S.-based MNC with AAA credit; B is an Italian firm with AAA credit. Firm A wants

to borrow €1,000,000 for one year and B wants to borrow $2,000,000 for one year. The spot

exchange rate is $2.00 = €1.00, a swap bank makes the following quotes for 1-year swaps and

AAA-rated firms against USD LIBOR.

USD Euro

Bid

Ask

Bid

Ask

8

%

8.1

%

6

%

6.1

%

The firms external borrowing opportunities are

€ borrowing

$ borrowing

A

€

7

%

$

8

%

B

€

6

%

$

9

%

A) Firm A does 2 swaps with the swap bank, $ at bid and € at ask. Firm B does 2 swaps with the

swap bank, $ at ask and € at bid. Firms A and B would each save 90bp and the swap bank would

earn 20bp.

B) There is no mutually beneficial swap at these prices.

C) Firm A does 2 swaps with the swap bank, $ at ask and € at bid. Firm B does 2 swaps with the

swap bank, $ at bid and € at ask. Firms A and B would each save 90bp and the swap bank would

earn 20bp.

D) none of the options

29) Consider the dollar- and euro-based borrowing opportunities of companies A and B.

€ borrowing

$ borrowing

A

€

7

%

$

8

%

B

€

6

%

$

9

%

A is a U.S.-based MNC with AAA credit; B is an Italian firm with AAA credit. Firm A wants to

borrow €1,000,000 for one year and B wants to borrow $2,000,000 for one year. The spot

exchange rate is $2.00 = €1.00 and the one-year forward rate is given by IRP as $2.00 ×

(1.08)/€1.00 × (1.06) = $2.0377/€1.

Is there a mutually beneficial swap?

A) No, QSD = 0

B) Yes, QSD = 2% = (7% − 6%) − (8% − 9%) = 1% − (−1%)

C) Yes, QSD = [€7% − €6%] × $2.00/€1.00 − ($8% − $9%) = $2% + $1% = $3%

D) Yes, QSD = [€7% − €6%] − ($8% − $9%) × €1.00/$2.00 = €1½%

30) Pricing an interest-only single currency swap after inception involves

A) sending a market order to a swap dealer.

B) finding the difference between the present values of the payments streams the party will receive

and pay.

C) finding the sum of the present values of the payments streams that each party will receive in one

currency and pay in the other currency, converted to a common currency.

D) none of the options

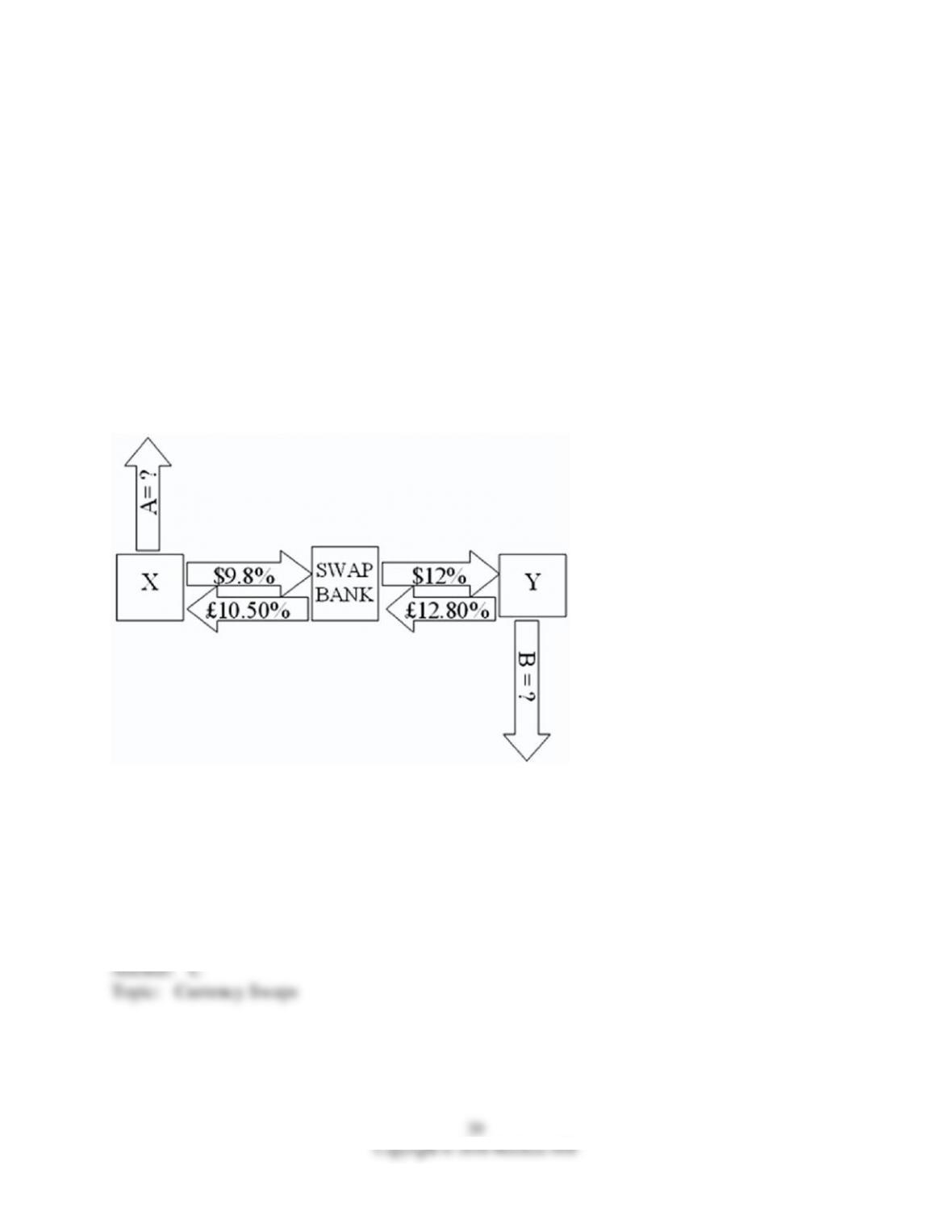

31) Company X wants to borrow $10,000,000 floating for 5 years; company Y wants to borrow

£5,000,000 fixed for 5 years. The exchange rate is $2 = £1 and is not expected to change over the

next 5 years. Their external borrowing opportunities are:

$ Borrowing

£ Borrowing

Cost

Cost

Company X

$

10

%

£

10.5

%

Company Y

$

12

%

£

13

%

A swap bank proposes the following interest-only swap: Company X will pay the swap bank

annual payments on $10,000,000 at an interest rate of $9.80 percent; in exchange the swap bank

will pay to company X interest payments on £5,000,000 at a fixed rate of 10.5 percent. Y will pay

the swap bank interest payments on £5,000,000 at a fixed rate of 12.80 percent and the swap bank

will pay Y annual payments on $10,000,000 with the coupon rate of 12 percent.

If company X takes on the swap, what external actions should they engage in?

A) They should borrow $10,000,000 at $10 percent.

B) They should borrow £5,000,000 at 10.50 percent interest-only for five years; translate pounds

to dollars at the spot rate.

C) They should borrow £5,000,000 at £10.50 percent interest-only for five years; translate pounds

to dollars at the spot rate; enter long position in a forward contract to buy £5,000,000 in five years.

D) none of the options