22) Please use a figure to discuss whether or not a devaluation under a fixed exchange rate has

the same long-run effect as a proportional increase in the money supply under a floating rate.

23) Please draw a figure illustrating the actions the central bank must take to maintain a fixed

exchange rate following an increase in output.

18.5 Balance of Payments Crises and Capital Flight

1) A balance of payments crisis is best described as

A) a sharp change in interest rates sparked by a change in expectations about the level of

imports.

B) a sharp change in foreign reserves sparked by a change in expectations about the future

exchange rate.

C) a sharp change in interest rates sparked by a change in expectations about the level of exports.

D) a sharp change in foreign reserves sparked by a change in expectations about the level of

imports.

E) a sharp change in foreign reserves sparked by a change in expectations about domestic

production.

2) The expectation of future devaluation causes a balance of payments crisis marked by

A) a sharp rise in reserves and a fall in the home interest rate below the world interest rate.

B) a sharp fall in reserves and an even bigger fall in the home interest rate below the world

interest rate.

C) a sharp fall in reserves and a rise in the home interest rate above the world interest rate.

D) a sharp rise in reserves and an even greater rise in the home interest rate above the world

interest.

E) a sharp rise in reserves and a rise in the home interest rate to the level of the world interest.

3) The expectation of future revaluation causes a balance of payments crisis marked by

A) a sharp rise in reserves and a fall in the home interest rate below the world interest rate.

B) a sharp fall in reserves and an even bigger fall in the home interest rate below the world

interest rate.

C) a sharp fall in reserves and a rise in the home interest rate above the world interest rate.

D) a sharp rise in reserves and an even greater rise in the home interest rate above the world

interest.

E) a sharp fall in reserves and an unchanged home interest rate.

4) Capital flight

A) increases reserves.

B) is never associated with the expectation of devaluation.

C) may undo expected devaluation.

D) reduces losses during a devaluation scare.

E) decreases reserves and may induce devaluation.

5) Currency crises may result from

A) central bank balance sheets with higher liabilities than assets.

B) political upheaval leading to lowering exports.

C) a reconfiguration of central bank balance sheets.

D) speculative attacks on the currency or central banks purchasing excessive amounts of

government bonds.

E) depreciation of foreign reserves.

1) Imperfect asset substitutability assumes

A) the returns on foreign and domestic currency bonds are identical.

B) the returns on foreign and domestic currency are unrelated.

C) the risks of holding foreign and domestic currency are identical.

D) the risks of holding foreign and domestic currency are unrelated to returns.

E) the returns on foreign and domestic currency differ and are influenced by risk.

2) The global financial crisis of 2007-2008 resulted in a(n) ________ of the Swiss franc as

foreign currency flowed ________ the country. As a result, Swiss products became ________

competitive in world markets.

A) depreciation; out of; more

B) depreciation; into; more

C) appreciation; out of; less

D) depreciation; out of; less

E) appreciation; into; less

3) The global financial crisis of 2007-2008 resulted in a(n) ________ of the Swiss franc. In 2011,

the Swiss central bank intervened in order to cause a(n) ________ of the franc.

A) appreciation; appreciation

B) depreciation; depreciation

C) appreciation; revaluation

D) depreciation; appreciation

E) appreciation; depreciation

4) Perfect asset substitutability is the assumption that

A) the foreign exchange market is in equilibrium only when expected returns on domestic assets

are greater than returns on foreign currency bonds.

B) the foreign exchange market is in equilibrium only when expected returns on foreign currency

bonds are greater than returns on domestic assets.

C) the foreign exchange market is in equilibrium only when expected returns on all assets are

negative.

D) the foreign exchange market is in equilibrium only when expected returns on domestic assets

are equal to returns on foreign currency bonds.

E) the foreign exchange market is in equilibrium only when domestic assets are risk-free.

5) Imperfect asset substitutability exists

A) when it is possible for the expected returns on two assets to be different.

B) when the expected returns on two assets are the same.

C) only when one asset is foreign and the other is domestic.

D) when there is risk in the foreign exchange market.

E) when assets are liquid.

6) The interest parity condition can be written as

A) R = R – (Ee – E)/E.

B) R = R + (Ee – E)/E.

C) R = R2 – (Ee – E)/E.

D) R = R /(Ee – E).

E) R = R + (Ee + E)/E.

7) When domestic and foreign currency bonds are imperfect substitutes, the domestic interest

rate (R) can be written as

A) R = R – (Ee – E)/E + ρ.

B) R = R – (Ee – E)/E.

C) R = R + (Ee – E)/E + ρ.

D) R = R – (Ee + E)/E + ρ.

E) R = R – (Ee – E)ρ.

8) In the interest rate parity condition with imperfect substitutes and a risk premium of ρ

A) an increased stock of domestic government debt will raise the difference between the

expected returns on domestic and foreign currency bonds.

B) a decreased stock of domestic government debt will raise the difference between the expected

returns on domestic and foreign currency bonds.

C) an increased stock of domestic government debt will reduce the difference between the

expected returns on domestic and foreign currency bonds.

D) an increased stock of domestic government debt will have no effect on the difference between

the expected returns on domestic and foreign currency bonds.

E) a decreased stock of domestic government debt will have no effect on the difference between

the expected returns on domestic and foreign currency bonds.

9) The signaling effect of foreign exchange intervention

A) never has any effect on exchange rates.

B) can alter the market’s view of exchange rates independent from the stance of monetary and

fiscal policies.

C) cannot cause an immediate exchange rate change when bonds denominated in different

currencies are perfect substitutes.

D) never leads to actual changes in monetary or fiscal policy.

E) can alter the market’s view of future monetary policies and cause an immediate exchange rate

change.

10) Please describe in detail a self-fulfilling currency crisis.

11) Describe the effect of the 2008-2009 global financial crisis on the Swiss franc and the central

bank’s efforts to respond to the resulting problems.

12) Use a figure to explain how a balance of payments crisis occurs and its hand in capital flight.

13) Assuming perfect asset substitutability, can sterilized intervention by the central bank be

effective? Please discuss.

1) Briefly describe two systems for fixing the exchange rates of all currencies against each other

and the time periods in which they were used.

2) This question concerns the mechanism of a reserve currency standard.

Two countries, X and Y, have two currencies, x and y, fixed to the reserve currency, the U.S.

dollar. Suppose the exchange rate between x and the U.S. dollar is 3x per dollar. Suppose the

exchange rate between y and the U.S. dollar is 5y per dollar. Explain (using numbers) the

mechanism if the x-y exchange rate was 0.5 x per y.

3) This question concerns the mechanism of a reserve currency standard.

Two countries, X and Y, have two currencies, x and y, fixed to the reserve currency, the U.S.

dollar. Suppose the exchange rate between x and the U.S. dollar is 3x per dollar. Suppose the

exchange rate between y and the U.S. dollar is 5y per dollar. Explain (using numbers) the

mechanism if the x-y exchange rate was 0.8 x per y.

4) Explain how a country whose currency is the reserve currency can use monetary policy for

macroeconomic stabilization. In particular, explain the result if that country doubled its domestic

money supply.

1) From 1837 and up until the Civil War, the United States adhered to a

A) gold standard.

B) silver standard.

C) bimetallic standard.

D) bronze standard.

E) copper standard.

2) From the Civil War up to 1914, the United States adhered to a

A) gold standard.

B) silver standard.

C) bimetallic standard.

D) bronze standard.

E) copper standard.

3) Does the signalling effect of foreign exchange intervention support or refute the claim that

assets cannot be perfect substitutes if sterilized intervention is going to have any effect? Please

explain.

4) Briefly discuss the main advantage of the bimetallic standard over the gold standard.

5) List the drawbacks of the gold standard.

6) Describe the mechanism which would take place if the Bank of England decides to increase its

money supply by purchasing domestic assets under the gold standard.

7) Please briefly describe what is meant by a gold exchange standard.

8) Use a figure to show the effect of a sterilized central bank purchase of foreign assets under the

imperfect asset substitutability assumption.

9) Assume that initially, the risk premium, ρ = 0 and that the domestic and foreign interest rates

are given by R = .06, R* = .05. Suppose that the risk premium depends linearly on the difference

between domestic government debt, B, and domestic assets of the central bank, A, i.e.,

ρ =

Find the new domestic interest rate if a sterilized purchase of foreign assets adjusts A s.t.

(a) B – A = -.01/

(b) B – A = .01/

(c) B – A = .03/

10) Assume that initially, the risk premium, ρ = 0 and that the domestic and foreign interest rates

are given by R = .06, R* = .05. Suppose that the risk premium depends linearly on the difference

between domestic government debt, B, and domestic assets of the central bank, A, i.e.,

ρ =

How much will the central bank have to reduce domestic assets A s.t. the domestic interest rate

will increase by (a) 1% (b) 4%?

11) Under the gold standard, if the dollar price of gold is pegged at $35 per ounce and the euro

price of gold is pegged at 12 euro per ounce, what is the dollar/euro exchange rate?

12) Under the gold standard, if the dollar price of gold is pegged at $35 per ounce and the

dollar/euro exchange rate is set at $2.40 per euro, what must the euro price of gold be pegged at?

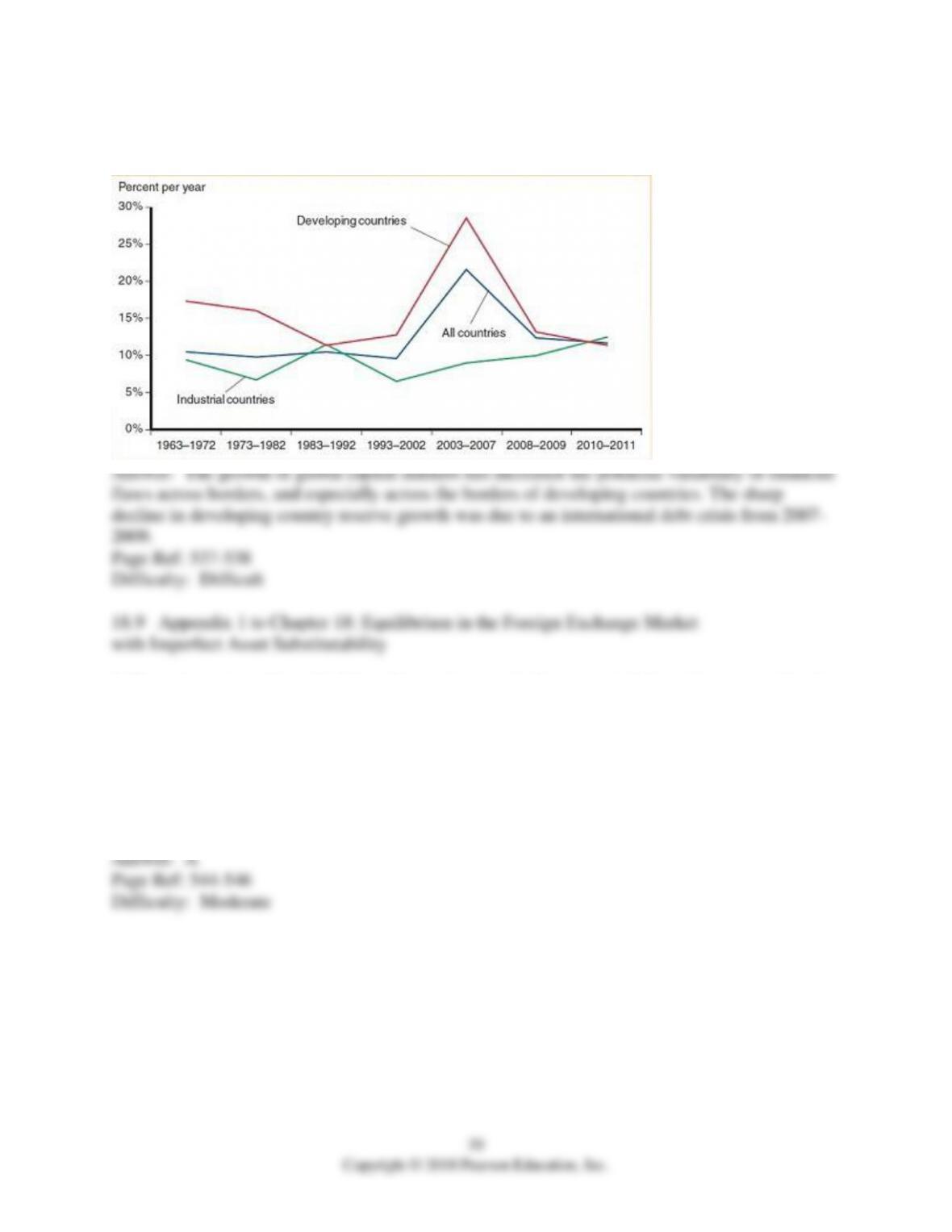

13) From the figure below, please provide an explanation for the large decline in the growth rate

of international reserves held by developing countries in the 2008-2009 period.

1) If assets are imperfect substitutes, then an increase in the amount of domestic currency bonds

held by the public will ________ the risk premium and ________ the amount of domestic

currency bonds held by the central bank.

A) increase; leave unchanged

B) increase; decrease

C) increase; increase

D) decrease; decrease

E) leave unchanged; decrease

2) If assets are imperfect substitutes, then a decrease in the amount of domestic currency bonds

held by the public will ________ the risk premium and ________ the amount of domestic

currency bonds held by the central bank.

A) decrease; leave unchanged

B) increase; decrease

C) increase; increase

D) decrease; decrease

E) leave unchanged; decrease

1) Balance of payments crises under fixed exchange rates occur because of

A) government policies that are inconsistent with fixed exchange rates.

B) punitive currency wars.

C) global inflation and trade imbalances due to war.

D) excessive exports and imports that overload the global system.

E) monotonic expansion in global currency volume.

2) A balance of payments crises under fixed exchange rates occurs when

A) marginal returns on foreign exchange investments approach zero.

B) a country runs out of foreign reserves.

C) a country is in a liquidity trap.

D) forward currency markets undergo high volatility.

E) exports and imports expand beyond some point.