25) A company that uses the perpetual inventory system purchased 500 pallets of industrial soap for

$10,000 and paid $950 for the freight-in. The company sold the whole lot to a supermarket chain for

$13,000 on account. Which of the following entries correctly records the sale?

A)

Accounts Receivable

13,000

Sales Revenue

13,000

Cost of Goods Sold

10,950

Merchandise Inventory

10,950

B)

Merchandise Inventory

13,000

Cost of Goods Sold

13,000

C)

Cost of Goods Sold

13,000

Sales Revenue

13,000

D)

Accounts Receivable

13,000

Sales Revenue

13,000

Cost of Goods Sold

10,000

Merchandise Inventory

10,000

26) Which of the following statements regarding FIFO is incorrect?

A) Ending inventory is based on the costs of the most recent purchases.

B) FIFO is consistent with the physical movement of inventory for most companies.

C) The first units to come in are assumed to be the first units sold.

D) FIFO is a specific identification costing method because companies sell their oldest inventory first.

27) James Sales sold 450 units of product to a customer on account. The company uses the perpetual

inventory system and the FIFO inventory costing method. The selling price was $28 per unit, and the

cost, according to the company‘s inventory records, was $12 per unit. Prepare the journal entries to record

the sale. Omit explanations.

28) Countrywide Sales sold 400 units of product to a customer on account. The selling price was $28 per

unit, and the cost, according to the company’s inventory records, was $14 per unit. Prepare the journal

entry to record the cost of goods sold. (Assume a perpetual inventory system and the FIFO inventory

costing method.) Omit explanation.

29) Costas, Inc. purchased inventory on account for $6,500. Prepare the journal entry to record the

purchase of inventory on account. (Assume a perpetual inventory system.) Omit explanation.

30) Western Sky, Inc. sold 500 units of inventory at $25 per unit for cash. The company uses the perpetual

inventory system and the FIFO inventory costing method. The beginning inventory included 550 units at

a cost of $15 per unit. The cost of the most recent purchases is $10 per unit. Prepare the journal entries to

record the sale. Omit explanations.

31) Meadows, Inc. sold 500 units of inventory at $25 per unit on account. The company uses the perpetual

inventory system and the FIFO inventory costing method. The beginning inventory included 400 units at

$15 per unit. The most recent purchases include 600 units at $18 per unit. Prepare the journal entries to

record the sale. Omit explanations.

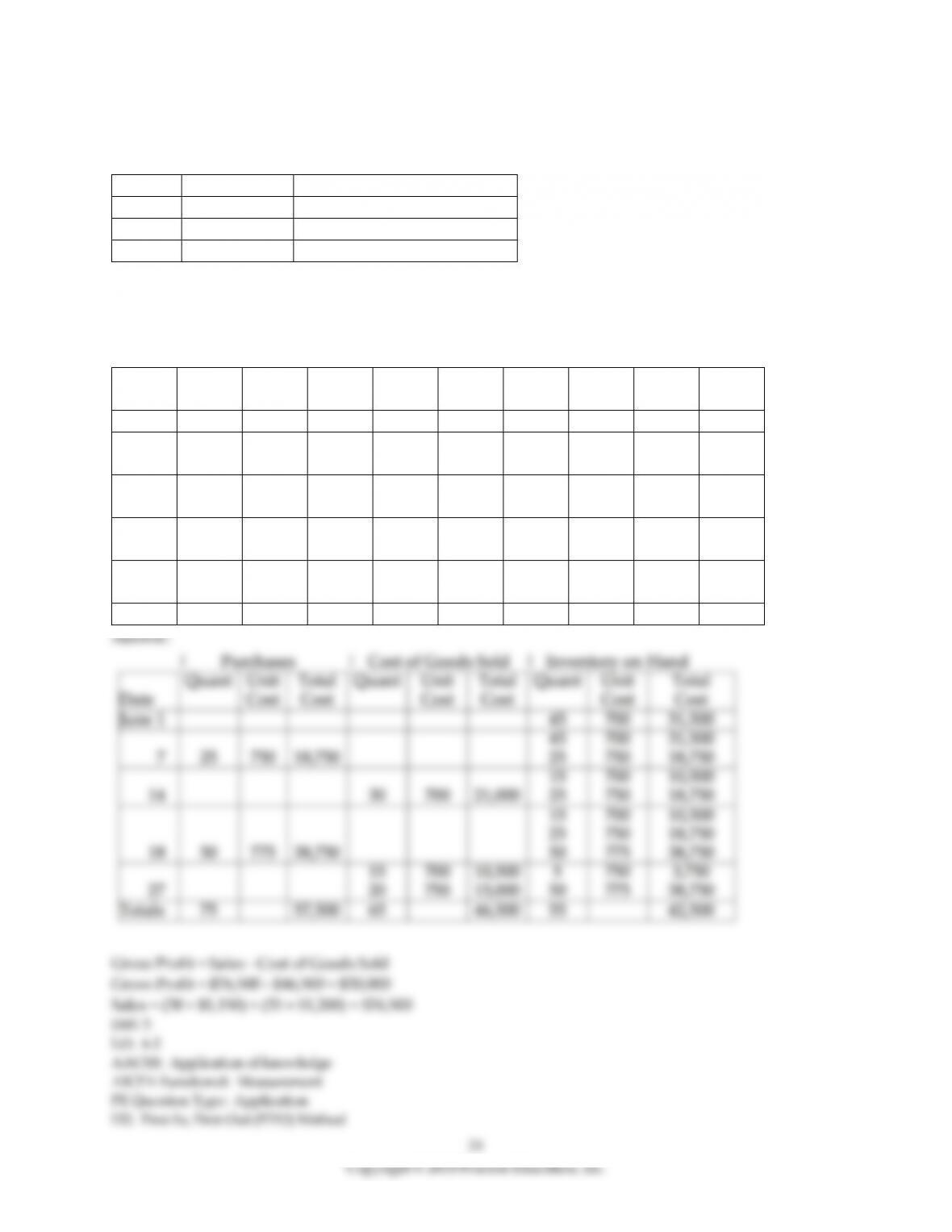

32) Modern Lifestyle Furniture began June with merchandise inventory of 45 sofas that cost a total of

$31,500. During the month, Modern purchased and sold merchandise on account as follows:

June 7

Purchase

25 sofas @ $750 each

14

Sale

30 sofas @ $1,150 each

18

Purchase

50 sofas @ $775 each

27

Sale

35 sofas @ $1,200 each

Prepare a perpetual inventory record, using the FIFO inventory costing method, and determine the

company’s cost of goods sold, ending merchandise inventory, and gross profit.

| Purchases | Cost of Goods Sold | Inventory on Hand |

Date

Quant

Unit

Cost

Total

Cost

Quant

Unit

Cost

Total

Cost

Quant

Unit

Cost

Total

Cost

33) Under the last-in, first-out (LIFO) method, the cost of goods sold is based on the oldest purchases.

34) The last-in, first-out (LIFO) costing system may or may not match the physical flow of goods.

35) The last-in, first-out (LIFO) costing system is permitted under International Financial Reporting

Standards (IFRS).

36) Under International Financial Reporting Standards (IFRS), companies may only use the specific

identification, FIFO, and weighted-average methods to cost inventory.

37) When a company uses the last-in, first-out (LIFO) method, the cost of goods sold represents the costs

of most recently purchased goods, and the ending inventory represents the oldest costs.

38) Which of the following inventory costing methods uses the costs of the oldest purchases to calculate

the value of the ending inventory?

A) specific identification

B) weighted-average

C) last-in, first-out

D) first-in, first-out

39) Which of the following statements regarding LIFO is incorrect?

A) The last units in are assumed to be the first units sold.

B) Ending inventory comes from the most recent purchases.

C) This method leaves the oldest costs in ending inventory.

D) LIFO is an assumption about how costs flow.

40) A company purchased 300 units for $20 each on January 31. It purchased 200 units for $40 each on

February 28. It sold a total of 250 units for $110 each from March 1 through December 31. If the company

uses the last-in, first-out inventory costing method, calculate the cost of ending inventory on December

31. (Assume that the company uses a perpetual inventory system.)

A) $10,000

B) $22,500

C) $5,000

D) $250

41) A company purchased 400 units for $30 each on January 31. It purchased 135 units for $40 each on

February 28. It sold 200 units for $55 each from March 1 through December 31. If the company uses the

last-in, first-out inventory costing method, what is the amount of Cost of Goods Sold on the income

statement for the year ending December 31? (Assume that the company uses a perpetual inventory

system.)

A) $7,350

B) $5,400

C) $12,000

D) $17,400

42) Rally Wheels, Inc. had the following balances and transactions during 2018:

Beginning Merchandise Inventory as of January 1, 2018

200 units at $71

March 10

Sold 50 units

June 10

Purchased 800 units at $76

October 30

Sold 175 units

What would the company’s ending merchandise inventory cost be on December 31, 2018 if the perpetual

inventory system and the last-in, first-out inventory costing method are used?

A) $16,850

B) $75,000

C) $58,150

D) $60,800

43) State the accounting term that applies to each of the following definitions.

Definition

Accounting Term

Businesses should use the same

accounting methods from period to

period.

Treats the oldest inventory purchases as

the first units sold.

Principle whose foundation is to exercise

caution in reporting financial information.

Treats the most recent/newest purchases

as cost of goods sold.

Definition

Accounting Term

Businesses should use the same

accounting methods from period to

period.

Consistency principle

Treats the oldest inventory purchases as

the first units sold.

First-in, first-out (FIFO)

Principle whose foundation is to exercise

caution in reporting financial information.

Conservatism principle

Treats the most recent/newest purchases

as cost of goods sold.

Last-in, first-out (LIFO)

44) State the accounting term that applies to each of the following definitions.

Definition

Accounting Term

Principle that states significant items must

conform to GAAP.

Treats the most recent/newest purchases

as the first units sold.

Requires that a company report enough

information for outsiders to make

knowledgeable decisions.

Identifies exactly which inventory item

was sold. Usually used for higher cost

inventory.

Principle that states significant items must

Materiality concept

Treats the most recent/newest purchases

as the first units sold.

Last-In, first-out (LIFO)

knowledgeable decisions.

Identifies exactly which inventory item

was sold. Usually used for higher cost

inventory.

Specific Identification